Loxam SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Loxam’s SWOT highlights strong market leadership and fleet scale, regional expansion opportunities, and operational efficiency—but also exposure to cyclical construction demand and integration challenges. Want the full picture with actionable insights and editable deliverables? Purchase the complete SWOT analysis to plan, pitch, or invest with confidence.

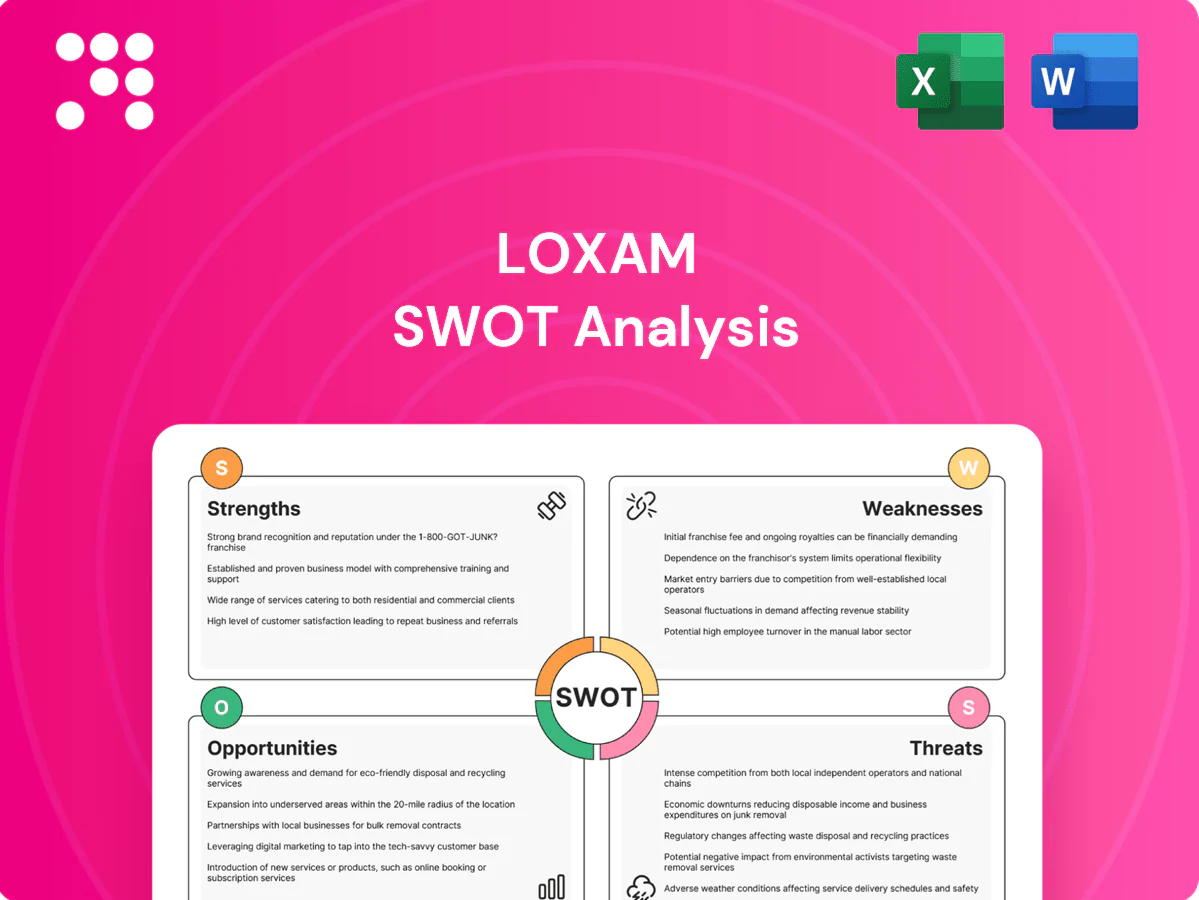

Strengths

European market leadership

Loxam’s scale and European market leadership—with presence in 30+ countries and 2023 revenue above €3bn—drives strong brand recognition, supplier bargaining power, and the ability to offer preferential terms to large clients.

Leadership enables higher fleet utilization and disciplined pricing across cycles, supporting margin resilience and cash flow stability.

It also amplifies negotiating leverage in M&A and partnerships and reinforces trust across construction, industrial and public-sector customers.

Comprehensive multi-sector fleet

Loxam’s comprehensive fleet spans earthmoving, access, power, tools and event equipment, enabling one-stop solutions and bundled contracts across its presence in 30 countries. Depth and breadth balance short-cycle tool rentals with long-term project machinery, smoothing demand volatility and supporting stable utilization. Customers gain simplified procurement, standardized safety and compliance across a network of around 1,200 branches.

Flexible rental value proposition

Loxam’s flexible rental converts capex into opex, boosting client cash flow and ROIC; Loxam reported roughly €2.3bn revenue in 2023, reflecting strong demand for this model. Customers avoid ownership risks such as maintenance, storage and obsolescence, reducing total cost of ownership. Variable-term options align precisely with project timelines, driving repeat business and higher lifetime value.

Extensive branch network

Loxam’s extensive network of over 1,150 branches across more than 30 countries brings equipment closer to job sites, cutting delivery times and transport costs and supporting faster swaps and maintenance response for projects. Proximity strengthens relationships with SMEs and public agencies and enables coverage for national and cross-border contracts, helping sustain market share and recurring revenue streams.

- +1,150 branches (30+ countries)

- Reduced delivery time and cost

- Faster service, swaps, maintenance

- Strong SME & public agency relationships

Operational know-how and service

Operational know-how—rooted in decades of maintenance, safety compliance and logistics—boosts uptime for clients and underpins Loxam’s service differentiation versus smaller local rivals. Standardized processes and certified safety programs are applied across 30 countries and 1,100+ branches, ensuring consistent reliability. Trained crews plus telematics-driven dispatching raise fleet utilization and allocation efficiency.

- Presence: 30 countries, 1,100+ branches

- Standardization: group-wide processes

- Tech: telematics for allocation

- Advantage: service quality vs local rivals

Global equipment rental scale across 30+ countries, 1,150+ branches and >€3bn revenue

Loxam’s scale—30+ countries, >1,150 branches and 2023 revenue >€3bn—delivers strong brand, supplier leverage and preferential terms for large clients.

High fleet breadth (earthmoving, access, power, tools) and telematics-driven operations raise utilization and margin resilience across cycles.

Proximity, standardized safety and flexible rental convert client capex to opex, driving repeat business and stable cash flow.

| Metric | Value |

|---|---|

| Countries | 30+ |

| Branches | >1,150 |

| Revenue (2023) | >€3bn |

What is included in the product

Provides a focused SWOT analysis of Loxam, highlighting internal strengths and weaknesses and external opportunities and threats shaping its equipment rental business and competitive position.

Provides a concise, editable SWOT matrix tailored to Loxam for fast strategic alignment and stakeholder-ready snapshots, simplifying updates as market conditions and rental trends evolve.

Weaknesses

Capital-intensive business

Large, ongoing investments are required to refresh and expand Loxam’s fleet — the post-Ramirent group reported pro forma revenue around €4.6bn, driving capex needs that often run near industry c.10% of sales. Depreciation and financing costs compress margins in slower markets, with interest and write-downs magnifying volatility. Fleet-mix missteps can lock in underperforming assets, so high capex demands disciplined asset rotation and resale strategies.

Cyclical end-market exposure

Cyclical end-market exposure leaves Loxam vulnerable as construction and public-works cycles drive utilization and pricing; Loxam, Europe’s largest rental group, reported roughly €3.8bn revenue in 2023, tying performance to sector demand. Project delays or public budget cuts quickly reduce rental days and rates, while industrial slowdowns compound softness across segments. Cash flows can swing sharply in macro downturns, stressing liquidity and fleet investment planning.

Complex operations and logistics

Coordinating deliveries, retrievals and maintenance across over 1,000 branches in 30+ countries creates logistical complexity that strains scheduling and spare-part flows. Misallocation of assets reduces fleet utilization and pushes up transport costs, eroding margins against Loxam’s ~€3.5bn 2023 revenue. Service variability between locations can harm customer satisfaction and churn. Systems and training must scale continuously as the network expands.

Price competition in commoditized categories

Standard tool and small equipment rentals face intense local price pressure; Loxam, present in about 30 countries with ~1,200 branches, sees discounting to defend share erode margins and compress profitability. Differentiation depends on costly service, availability and fleet reliability, while procurement-led tenders limit upsell to higher-margin solutions.

- Local price pressure

- Margin erosion from discounts

- High cost of service/availability

- Tenders limit upsell

Dependence on OEM supply and parts

Dependence on OEM supply and parts lengthens fleet renewal when manufacturer lead times and pricing tighten, constraining capital deployment. Parts shortages increase downtime and lower utilization, eroding rental revenue. Rapid OEM technology shifts can accelerate obsolescence of older assets and concentrated suppliers reduce Loxam’s bargaining flexibility.

- Lead times/pricing pressure

- Parts shortages -> downtime

- OEM tech obsolescence

- Supplier concentration risk

High fleet capex and financing strain margins; pro forma revenue €4.6bn amid volatile utilisation

High ongoing fleet capex (~10% of sales) and depreciation/financing compress margins; pro forma group revenue ~€4.6bn while reported 2023 sales ranged ~€3.5–3.8bn. Cyclical construction exposure drives volatile utilisation and cash flow. Complex logistics across ~1,200 branches in 30+ countries and supplier/parts constraints raise downtime and operating costs.

| Metric | Value |

|---|---|

| 2023 revenue | €3.5–3.8bn |

| Pro forma (post-Ramirent) | €4.6bn |

| Capex | ~10% sales |

| Branches / countries | ~1,200 / 30+ |

Preview Before You Purchase

Loxam SWOT Analysis

This is the actual Loxam SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable file you’ll download post-checkout. Buy now to unlock the complete in-depth version.

Dive Deeper Into the Company’s Strategic Blueprint

Loxam’s SWOT highlights strong market leadership and fleet scale, regional expansion opportunities, and operational efficiency—but also exposure to cyclical construction demand and integration challenges. Want the full picture with actionable insights and editable deliverables? Purchase the complete SWOT analysis to plan, pitch, or invest with confidence.

Strengths

European market leadership

Loxam’s scale and European market leadership—with presence in 30+ countries and 2023 revenue above €3bn—drives strong brand recognition, supplier bargaining power, and the ability to offer preferential terms to large clients.

Leadership enables higher fleet utilization and disciplined pricing across cycles, supporting margin resilience and cash flow stability.

It also amplifies negotiating leverage in M&A and partnerships and reinforces trust across construction, industrial and public-sector customers.

Comprehensive multi-sector fleet

Loxam’s comprehensive fleet spans earthmoving, access, power, tools and event equipment, enabling one-stop solutions and bundled contracts across its presence in 30 countries. Depth and breadth balance short-cycle tool rentals with long-term project machinery, smoothing demand volatility and supporting stable utilization. Customers gain simplified procurement, standardized safety and compliance across a network of around 1,200 branches.

Flexible rental value proposition

Loxam’s flexible rental converts capex into opex, boosting client cash flow and ROIC; Loxam reported roughly €2.3bn revenue in 2023, reflecting strong demand for this model. Customers avoid ownership risks such as maintenance, storage and obsolescence, reducing total cost of ownership. Variable-term options align precisely with project timelines, driving repeat business and higher lifetime value.

Extensive branch network

Loxam’s extensive network of over 1,150 branches across more than 30 countries brings equipment closer to job sites, cutting delivery times and transport costs and supporting faster swaps and maintenance response for projects. Proximity strengthens relationships with SMEs and public agencies and enables coverage for national and cross-border contracts, helping sustain market share and recurring revenue streams.

- +1,150 branches (30+ countries)

- Reduced delivery time and cost

- Faster service, swaps, maintenance

- Strong SME & public agency relationships

Operational know-how and service

Operational know-how—rooted in decades of maintenance, safety compliance and logistics—boosts uptime for clients and underpins Loxam’s service differentiation versus smaller local rivals. Standardized processes and certified safety programs are applied across 30 countries and 1,100+ branches, ensuring consistent reliability. Trained crews plus telematics-driven dispatching raise fleet utilization and allocation efficiency.

- Presence: 30 countries, 1,100+ branches

- Standardization: group-wide processes

- Tech: telematics for allocation

- Advantage: service quality vs local rivals

Global equipment rental scale across 30+ countries, 1,150+ branches and >€3bn revenue

Loxam’s scale—30+ countries, >1,150 branches and 2023 revenue >€3bn—delivers strong brand, supplier leverage and preferential terms for large clients.

High fleet breadth (earthmoving, access, power, tools) and telematics-driven operations raise utilization and margin resilience across cycles.

Proximity, standardized safety and flexible rental convert client capex to opex, driving repeat business and stable cash flow.

| Metric | Value |

|---|---|

| Countries | 30+ |

| Branches | >1,150 |

| Revenue (2023) | >€3bn |

What is included in the product

Provides a focused SWOT analysis of Loxam, highlighting internal strengths and weaknesses and external opportunities and threats shaping its equipment rental business and competitive position.

Provides a concise, editable SWOT matrix tailored to Loxam for fast strategic alignment and stakeholder-ready snapshots, simplifying updates as market conditions and rental trends evolve.

Weaknesses

Capital-intensive business

Large, ongoing investments are required to refresh and expand Loxam’s fleet — the post-Ramirent group reported pro forma revenue around €4.6bn, driving capex needs that often run near industry c.10% of sales. Depreciation and financing costs compress margins in slower markets, with interest and write-downs magnifying volatility. Fleet-mix missteps can lock in underperforming assets, so high capex demands disciplined asset rotation and resale strategies.

Cyclical end-market exposure

Cyclical end-market exposure leaves Loxam vulnerable as construction and public-works cycles drive utilization and pricing; Loxam, Europe’s largest rental group, reported roughly €3.8bn revenue in 2023, tying performance to sector demand. Project delays or public budget cuts quickly reduce rental days and rates, while industrial slowdowns compound softness across segments. Cash flows can swing sharply in macro downturns, stressing liquidity and fleet investment planning.

Complex operations and logistics

Coordinating deliveries, retrievals and maintenance across over 1,000 branches in 30+ countries creates logistical complexity that strains scheduling and spare-part flows. Misallocation of assets reduces fleet utilization and pushes up transport costs, eroding margins against Loxam’s ~€3.5bn 2023 revenue. Service variability between locations can harm customer satisfaction and churn. Systems and training must scale continuously as the network expands.

Price competition in commoditized categories

Standard tool and small equipment rentals face intense local price pressure; Loxam, present in about 30 countries with ~1,200 branches, sees discounting to defend share erode margins and compress profitability. Differentiation depends on costly service, availability and fleet reliability, while procurement-led tenders limit upsell to higher-margin solutions.

- Local price pressure

- Margin erosion from discounts

- High cost of service/availability

- Tenders limit upsell

Dependence on OEM supply and parts

Dependence on OEM supply and parts lengthens fleet renewal when manufacturer lead times and pricing tighten, constraining capital deployment. Parts shortages increase downtime and lower utilization, eroding rental revenue. Rapid OEM technology shifts can accelerate obsolescence of older assets and concentrated suppliers reduce Loxam’s bargaining flexibility.

- Lead times/pricing pressure

- Parts shortages -> downtime

- OEM tech obsolescence

- Supplier concentration risk

High fleet capex and financing strain margins; pro forma revenue €4.6bn amid volatile utilisation

High ongoing fleet capex (~10% of sales) and depreciation/financing compress margins; pro forma group revenue ~€4.6bn while reported 2023 sales ranged ~€3.5–3.8bn. Cyclical construction exposure drives volatile utilisation and cash flow. Complex logistics across ~1,200 branches in 30+ countries and supplier/parts constraints raise downtime and operating costs.

| Metric | Value |

|---|---|

| 2023 revenue | €3.5–3.8bn |

| Pro forma (post-Ramirent) | €4.6bn |

| Capex | ~10% sales |

| Branches / countries | ~1,200 / 30+ |

Preview Before You Purchase

Loxam SWOT Analysis

This is the actual Loxam SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable file you’ll download post-checkout. Buy now to unlock the complete in-depth version.

Description

Dive Deeper Into the Company’s Strategic Blueprint

Loxam’s SWOT highlights strong market leadership and fleet scale, regional expansion opportunities, and operational efficiency—but also exposure to cyclical construction demand and integration challenges. Want the full picture with actionable insights and editable deliverables? Purchase the complete SWOT analysis to plan, pitch, or invest with confidence.

Strengths

European market leadership

Loxam’s scale and European market leadership—with presence in 30+ countries and 2023 revenue above €3bn—drives strong brand recognition, supplier bargaining power, and the ability to offer preferential terms to large clients.

Leadership enables higher fleet utilization and disciplined pricing across cycles, supporting margin resilience and cash flow stability.

It also amplifies negotiating leverage in M&A and partnerships and reinforces trust across construction, industrial and public-sector customers.

Comprehensive multi-sector fleet

Loxam’s comprehensive fleet spans earthmoving, access, power, tools and event equipment, enabling one-stop solutions and bundled contracts across its presence in 30 countries. Depth and breadth balance short-cycle tool rentals with long-term project machinery, smoothing demand volatility and supporting stable utilization. Customers gain simplified procurement, standardized safety and compliance across a network of around 1,200 branches.

Flexible rental value proposition

Loxam’s flexible rental converts capex into opex, boosting client cash flow and ROIC; Loxam reported roughly €2.3bn revenue in 2023, reflecting strong demand for this model. Customers avoid ownership risks such as maintenance, storage and obsolescence, reducing total cost of ownership. Variable-term options align precisely with project timelines, driving repeat business and higher lifetime value.

Extensive branch network

Loxam’s extensive network of over 1,150 branches across more than 30 countries brings equipment closer to job sites, cutting delivery times and transport costs and supporting faster swaps and maintenance response for projects. Proximity strengthens relationships with SMEs and public agencies and enables coverage for national and cross-border contracts, helping sustain market share and recurring revenue streams.

- +1,150 branches (30+ countries)

- Reduced delivery time and cost

- Faster service, swaps, maintenance

- Strong SME & public agency relationships

Operational know-how and service

Operational know-how—rooted in decades of maintenance, safety compliance and logistics—boosts uptime for clients and underpins Loxam’s service differentiation versus smaller local rivals. Standardized processes and certified safety programs are applied across 30 countries and 1,100+ branches, ensuring consistent reliability. Trained crews plus telematics-driven dispatching raise fleet utilization and allocation efficiency.

- Presence: 30 countries, 1,100+ branches

- Standardization: group-wide processes

- Tech: telematics for allocation

- Advantage: service quality vs local rivals

Global equipment rental scale across 30+ countries, 1,150+ branches and >€3bn revenue

Loxam’s scale—30+ countries, >1,150 branches and 2023 revenue >€3bn—delivers strong brand, supplier leverage and preferential terms for large clients.

High fleet breadth (earthmoving, access, power, tools) and telematics-driven operations raise utilization and margin resilience across cycles.

Proximity, standardized safety and flexible rental convert client capex to opex, driving repeat business and stable cash flow.

| Metric | Value |

|---|---|

| Countries | 30+ |

| Branches | >1,150 |

| Revenue (2023) | >€3bn |

What is included in the product

Provides a focused SWOT analysis of Loxam, highlighting internal strengths and weaknesses and external opportunities and threats shaping its equipment rental business and competitive position.

Provides a concise, editable SWOT matrix tailored to Loxam for fast strategic alignment and stakeholder-ready snapshots, simplifying updates as market conditions and rental trends evolve.

Weaknesses

Capital-intensive business

Large, ongoing investments are required to refresh and expand Loxam’s fleet — the post-Ramirent group reported pro forma revenue around €4.6bn, driving capex needs that often run near industry c.10% of sales. Depreciation and financing costs compress margins in slower markets, with interest and write-downs magnifying volatility. Fleet-mix missteps can lock in underperforming assets, so high capex demands disciplined asset rotation and resale strategies.

Cyclical end-market exposure

Cyclical end-market exposure leaves Loxam vulnerable as construction and public-works cycles drive utilization and pricing; Loxam, Europe’s largest rental group, reported roughly €3.8bn revenue in 2023, tying performance to sector demand. Project delays or public budget cuts quickly reduce rental days and rates, while industrial slowdowns compound softness across segments. Cash flows can swing sharply in macro downturns, stressing liquidity and fleet investment planning.

Complex operations and logistics

Coordinating deliveries, retrievals and maintenance across over 1,000 branches in 30+ countries creates logistical complexity that strains scheduling and spare-part flows. Misallocation of assets reduces fleet utilization and pushes up transport costs, eroding margins against Loxam’s ~€3.5bn 2023 revenue. Service variability between locations can harm customer satisfaction and churn. Systems and training must scale continuously as the network expands.

Price competition in commoditized categories

Standard tool and small equipment rentals face intense local price pressure; Loxam, present in about 30 countries with ~1,200 branches, sees discounting to defend share erode margins and compress profitability. Differentiation depends on costly service, availability and fleet reliability, while procurement-led tenders limit upsell to higher-margin solutions.

- Local price pressure

- Margin erosion from discounts

- High cost of service/availability

- Tenders limit upsell

Dependence on OEM supply and parts

Dependence on OEM supply and parts lengthens fleet renewal when manufacturer lead times and pricing tighten, constraining capital deployment. Parts shortages increase downtime and lower utilization, eroding rental revenue. Rapid OEM technology shifts can accelerate obsolescence of older assets and concentrated suppliers reduce Loxam’s bargaining flexibility.

- Lead times/pricing pressure

- Parts shortages -> downtime

- OEM tech obsolescence

- Supplier concentration risk

High fleet capex and financing strain margins; pro forma revenue €4.6bn amid volatile utilisation

High ongoing fleet capex (~10% of sales) and depreciation/financing compress margins; pro forma group revenue ~€4.6bn while reported 2023 sales ranged ~€3.5–3.8bn. Cyclical construction exposure drives volatile utilisation and cash flow. Complex logistics across ~1,200 branches in 30+ countries and supplier/parts constraints raise downtime and operating costs.

| Metric | Value |

|---|---|

| 2023 revenue | €3.5–3.8bn |

| Pro forma (post-Ramirent) | €4.6bn |

| Capex | ~10% sales |

| Branches / countries | ~1,200 / 30+ |

Preview Before You Purchase

Loxam SWOT Analysis

This is the actual Loxam SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, editable file you’ll download post-checkout. Buy now to unlock the complete in-depth version.