Louisiana-Pacific PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock how political, economic, social, technological, legal, and environmental forces are reshaping Louisiana‑Pacific’s strategy and risk profile in our concise PESTLE overview; the full report delivers data-driven insights, scenario impacts, and strategic recommendations to inform investment and planning decisions—purchase the complete analysis for immediate, actionable intelligence.

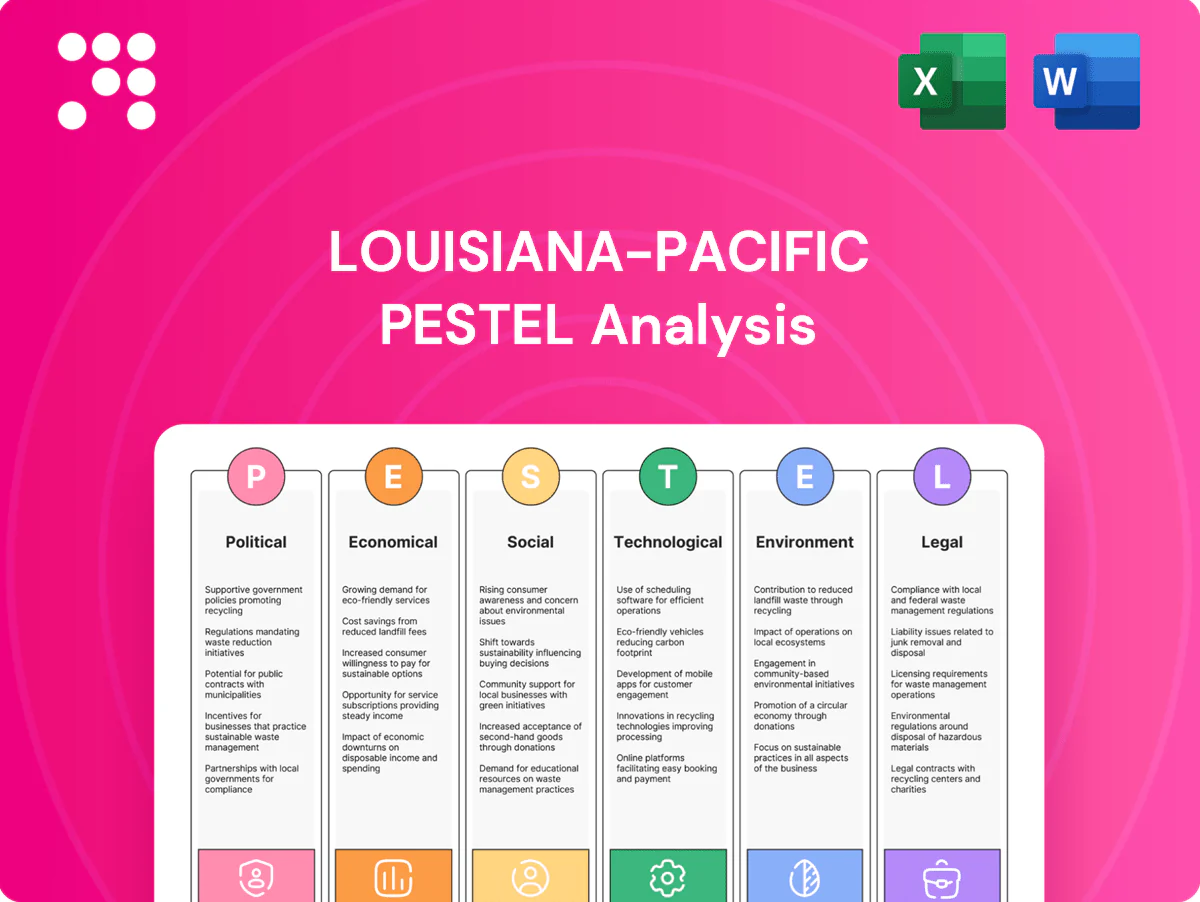

Political factors

Trade and tariff exposure

LPX supply chains for OSB and siding span the U.S., Canada and Latin America, exposing Louisiana-Pacific to tariffs and countervailing duties that in past softwood disputes have reached 20–25%, and to trade-dispute-driven cost swings. Changes in U.S.–Canada softwood policy or Mercosur trade terms can shift fiber and finished‑goods cost curves and compress LPX margins or force costly re‑routing. Active government relations reduce lead time for mitigation.

Housing and infrastructure policy

Federal housing and resilience programs, alongside the $1.2 trillion Infrastructure Investment and Jobs Act, boost demand for engineered wood by funding affordable housing and retrofit projects. Increased infrastructure spending supports the roughly 7.5 million US construction jobs (2024), improving logistics and throughput for Louisiana-Pacific. Local upzoning and infill reforms drive higher material volumes per site. Policy delays or funding gaps can defer multi‑year project volumes.

Regional incentives and siting

Plant siting decisions hinge on state tax credits, energy incentives and workforce grants; all 50 states offer some form of site-selection incentives as of 2024. Stable political environments reduce permitting risk and cycle time, while gubernatorial terms of four years mean shifts in priorities can disrupt subsidy continuity. LP can diversify its U.S. footprint across states to balance political risk and preserve project economics.

Environmental and forest policy

Environmental and forest policy—including forestry regulations, harvest quotas and public land management (USFS manages 193 million acres)—directly affects LPX fiber availability and price; biodiversity and wildfire mitigation measures have increased stumpage and access constraints, while policy-driven carbon markets create potential credits or compliance costs, making agency engagement critical for supply stability.

International operations risk

International operations in Chile and Brazil face election cycles, policy swings and occasional currency controls that can alter costs and repatriation; export licenses and customs procedures lengthen lead times for lumber and engineered wood shipments. Political unrest and strikes can block key transport corridors, raising logistics costs and inventory risk. Scenario planning and hedging reduce geopolitical exposure.

- Election/policy volatility

- Currency control risk

- Export/customs delays

- Transport corridor disruptions

- Scenario planning/hedging

Softwood faces 20–25% tariff risk; $1.2T infra lifts engineered‑wood demand

LPX is exposed to 20–25% softwood tariff risk and trade‑driven cost swings across US, Canada and Latin America. Federal programs including the $1.2T Infrastructure Law and ~7.5M US construction jobs (2024) boost engineered‑wood demand but funding delays can defer volumes. Forestry rules (USFS 193M acres) and carbon markets affect fiber costs; election/currency risk raises export and repatriation uncertainty.

| Factor | 2024/25 Metric | Impact |

|---|---|---|

| Tariffs | 20–25% | Margin compression |

| Infrastructure | $1.2T | Demand tailwind |

| Construction jobs | 7.5M | Improved demand/logistics |

| Forestry | USFS 193M acres | Fiber/access constraints |

What is included in the product

Provides a concise PESTLE analysis of Louisiana-Pacific, examining Political, Economic, Social, Technological, Environmental and Legal factors and their specific impacts on LP’s operations and strategy. Each section is data-driven, regionally grounded and includes forward-looking implications to inform executives, investors and planners.

A concise, visually segmented Louisiana‑Pacific PESTLE summary that fits into presentations or strategy packs, supports quick team alignment, and lets users add region‑ or business‑specific notes to ease external risk discussions and planning.

Economic factors

Housing cycle sensitivity

LP volumes move with U.S. housing starts (about 1.4M annualized in 2024 per U.S. Census) and repair/remodel spending; with 30-year mortgage rates near 7% in 2024 (Freddie Mac), new construction has softened while R&R demand has held up. Regional housing strength can offset national slowdowns, and builder backlogs of roughly 4–5 months (NAHB early‑2024) drive near‑term LP orders.

Commodity price volatility

OSB pricing is highly cyclical, with spot prices historically swinging more than 50% year-over-year as supply-demand balances shift; Louisiana-Pacific earnings move with those cycles. Input costs for resins, waxes and energy—which accounted for a meaningful portion of manufacturing cost in LP filings—add margin variability. Hedging programs and flexible sales contracts help stabilize EBITDA, while industry-wide capacity discipline remains a primary driver of price recovery.

Labor and logistics costs

Tight labor markets (US unemployment 2024 avg 3.7%) pushed manufacturing wage growth about 4.3% in 2024, raising mill and contractor labor costs for Louisiana-Pacific. Trucking availability, rail service and diesel at roughly $4.03/gal (2024 avg, EIA) materially affect delivered costs. LPX’s seven-mill North American OSB network and near-shoring shorten hauls, while ongoing efficiency projects aim to offset structural cost inflation.

Foreign exchange impacts

USD volatility versus CAD (≈1.36 mid‑2025), BRL (≈5.20) and MXN (≈17.8) affects LP’s cross‑border costs and translation; a strong USD can pressure exports while lowering imported input costs. Local sourcing creates natural hedges that cut transaction exposure, and treasury strategies (forwards, netting) manage residual FX risk.

- USD/CAD ≈1.36 — translation risk

- BRL ≈5.20, MXN ≈17.8 — regional cost swings

- Treasury: forwards, netting, local financing

Business mix resilience

Louisiana-Pacific's mix tilt toward siding and value-added products cushions revenue versus commodity OSB, whose spot prices swung from about $1,100/MSF at the 2021 peak to roughly $300–400/MSF by 2023, amplifying margins in durable channels. Growing repair/remodel and light-commercial sales smooth demand cycles and support margin floors, while active capacity allocation lets LPX pivot between OSB and specialty lines to match market conditions.

- Siding/value-added: steadier pricing, higher margin resilience

- OSB volatility: $1,100/MSF peak (2021) to ~$300–400/MSF (2023)

- Repair/remodel + light commercial: demand smoothing

- Balanced capacity allocation: aligns supply with pricing signals

Softwood faces 20–25% tariff risk; $1.2T infra lifts engineered‑wood demand

LP volumes follow US housing starts (~1.4M annualized in 2024) and R&R; 30‑yr mortgage ~7% in 2024 dampened new builds while R&R held. OSB price cyclicality (peak ~$1,100/MSF 2021 to ~$300–400/MSF 2023) and resin/energy costs drive earnings volatility. Tight labor (2024 unemployment ~3.7%) and diesel ~$4.03/gal raise delivered costs; USD/CAD ~1.36 (mid‑2025) and hedging limit FX impact.

| Metric | Value |

|---|---|

| Housing starts (2024) | ~1.4M |

| 30‑yr mortgage (2024) | ~7% |

| OSB price swing | $1,100 → $300–400/MSF |

| Unemployment (2024) | ~3.7% |

| Diesel (2024 avg) | $4.03/gal |

| USD/CAD (mid‑2025) | ~1.36 |

Same Document Delivered

Louisiana-Pacific PESTLE Analysis

The preview shown here is the exact Louisiana‑Pacific PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product with no placeholders or surprises. The content, layout, and sections visible are the final downloadable file. Immediate download follows checkout.

Your Competitive Advantage Starts with This Report

Unlock how political, economic, social, technological, legal, and environmental forces are reshaping Louisiana‑Pacific’s strategy and risk profile in our concise PESTLE overview; the full report delivers data-driven insights, scenario impacts, and strategic recommendations to inform investment and planning decisions—purchase the complete analysis for immediate, actionable intelligence.

Political factors

Trade and tariff exposure

LPX supply chains for OSB and siding span the U.S., Canada and Latin America, exposing Louisiana-Pacific to tariffs and countervailing duties that in past softwood disputes have reached 20–25%, and to trade-dispute-driven cost swings. Changes in U.S.–Canada softwood policy or Mercosur trade terms can shift fiber and finished‑goods cost curves and compress LPX margins or force costly re‑routing. Active government relations reduce lead time for mitigation.

Housing and infrastructure policy

Federal housing and resilience programs, alongside the $1.2 trillion Infrastructure Investment and Jobs Act, boost demand for engineered wood by funding affordable housing and retrofit projects. Increased infrastructure spending supports the roughly 7.5 million US construction jobs (2024), improving logistics and throughput for Louisiana-Pacific. Local upzoning and infill reforms drive higher material volumes per site. Policy delays or funding gaps can defer multi‑year project volumes.

Regional incentives and siting

Plant siting decisions hinge on state tax credits, energy incentives and workforce grants; all 50 states offer some form of site-selection incentives as of 2024. Stable political environments reduce permitting risk and cycle time, while gubernatorial terms of four years mean shifts in priorities can disrupt subsidy continuity. LP can diversify its U.S. footprint across states to balance political risk and preserve project economics.

Environmental and forest policy

Environmental and forest policy—including forestry regulations, harvest quotas and public land management (USFS manages 193 million acres)—directly affects LPX fiber availability and price; biodiversity and wildfire mitigation measures have increased stumpage and access constraints, while policy-driven carbon markets create potential credits or compliance costs, making agency engagement critical for supply stability.

International operations risk

International operations in Chile and Brazil face election cycles, policy swings and occasional currency controls that can alter costs and repatriation; export licenses and customs procedures lengthen lead times for lumber and engineered wood shipments. Political unrest and strikes can block key transport corridors, raising logistics costs and inventory risk. Scenario planning and hedging reduce geopolitical exposure.

- Election/policy volatility

- Currency control risk

- Export/customs delays

- Transport corridor disruptions

- Scenario planning/hedging

Softwood faces 20–25% tariff risk; $1.2T infra lifts engineered‑wood demand

LPX is exposed to 20–25% softwood tariff risk and trade‑driven cost swings across US, Canada and Latin America. Federal programs including the $1.2T Infrastructure Law and ~7.5M US construction jobs (2024) boost engineered‑wood demand but funding delays can defer volumes. Forestry rules (USFS 193M acres) and carbon markets affect fiber costs; election/currency risk raises export and repatriation uncertainty.

| Factor | 2024/25 Metric | Impact |

|---|---|---|

| Tariffs | 20–25% | Margin compression |

| Infrastructure | $1.2T | Demand tailwind |

| Construction jobs | 7.5M | Improved demand/logistics |

| Forestry | USFS 193M acres | Fiber/access constraints |

What is included in the product

Provides a concise PESTLE analysis of Louisiana-Pacific, examining Political, Economic, Social, Technological, Environmental and Legal factors and their specific impacts on LP’s operations and strategy. Each section is data-driven, regionally grounded and includes forward-looking implications to inform executives, investors and planners.

A concise, visually segmented Louisiana‑Pacific PESTLE summary that fits into presentations or strategy packs, supports quick team alignment, and lets users add region‑ or business‑specific notes to ease external risk discussions and planning.

Economic factors

Housing cycle sensitivity

LP volumes move with U.S. housing starts (about 1.4M annualized in 2024 per U.S. Census) and repair/remodel spending; with 30-year mortgage rates near 7% in 2024 (Freddie Mac), new construction has softened while R&R demand has held up. Regional housing strength can offset national slowdowns, and builder backlogs of roughly 4–5 months (NAHB early‑2024) drive near‑term LP orders.

Commodity price volatility

OSB pricing is highly cyclical, with spot prices historically swinging more than 50% year-over-year as supply-demand balances shift; Louisiana-Pacific earnings move with those cycles. Input costs for resins, waxes and energy—which accounted for a meaningful portion of manufacturing cost in LP filings—add margin variability. Hedging programs and flexible sales contracts help stabilize EBITDA, while industry-wide capacity discipline remains a primary driver of price recovery.

Labor and logistics costs

Tight labor markets (US unemployment 2024 avg 3.7%) pushed manufacturing wage growth about 4.3% in 2024, raising mill and contractor labor costs for Louisiana-Pacific. Trucking availability, rail service and diesel at roughly $4.03/gal (2024 avg, EIA) materially affect delivered costs. LPX’s seven-mill North American OSB network and near-shoring shorten hauls, while ongoing efficiency projects aim to offset structural cost inflation.

Foreign exchange impacts

USD volatility versus CAD (≈1.36 mid‑2025), BRL (≈5.20) and MXN (≈17.8) affects LP’s cross‑border costs and translation; a strong USD can pressure exports while lowering imported input costs. Local sourcing creates natural hedges that cut transaction exposure, and treasury strategies (forwards, netting) manage residual FX risk.

- USD/CAD ≈1.36 — translation risk

- BRL ≈5.20, MXN ≈17.8 — regional cost swings

- Treasury: forwards, netting, local financing

Business mix resilience

Louisiana-Pacific's mix tilt toward siding and value-added products cushions revenue versus commodity OSB, whose spot prices swung from about $1,100/MSF at the 2021 peak to roughly $300–400/MSF by 2023, amplifying margins in durable channels. Growing repair/remodel and light-commercial sales smooth demand cycles and support margin floors, while active capacity allocation lets LPX pivot between OSB and specialty lines to match market conditions.

- Siding/value-added: steadier pricing, higher margin resilience

- OSB volatility: $1,100/MSF peak (2021) to ~$300–400/MSF (2023)

- Repair/remodel + light commercial: demand smoothing

- Balanced capacity allocation: aligns supply with pricing signals

Softwood faces 20–25% tariff risk; $1.2T infra lifts engineered‑wood demand

LP volumes follow US housing starts (~1.4M annualized in 2024) and R&R; 30‑yr mortgage ~7% in 2024 dampened new builds while R&R held. OSB price cyclicality (peak ~$1,100/MSF 2021 to ~$300–400/MSF 2023) and resin/energy costs drive earnings volatility. Tight labor (2024 unemployment ~3.7%) and diesel ~$4.03/gal raise delivered costs; USD/CAD ~1.36 (mid‑2025) and hedging limit FX impact.

| Metric | Value |

|---|---|

| Housing starts (2024) | ~1.4M |

| 30‑yr mortgage (2024) | ~7% |

| OSB price swing | $1,100 → $300–400/MSF |

| Unemployment (2024) | ~3.7% |

| Diesel (2024 avg) | $4.03/gal |

| USD/CAD (mid‑2025) | ~1.36 |

Same Document Delivered

Louisiana-Pacific PESTLE Analysis

The preview shown here is the exact Louisiana‑Pacific PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product with no placeholders or surprises. The content, layout, and sections visible are the final downloadable file. Immediate download follows checkout.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock how political, economic, social, technological, legal, and environmental forces are reshaping Louisiana‑Pacific’s strategy and risk profile in our concise PESTLE overview; the full report delivers data-driven insights, scenario impacts, and strategic recommendations to inform investment and planning decisions—purchase the complete analysis for immediate, actionable intelligence.

Political factors

Trade and tariff exposure

LPX supply chains for OSB and siding span the U.S., Canada and Latin America, exposing Louisiana-Pacific to tariffs and countervailing duties that in past softwood disputes have reached 20–25%, and to trade-dispute-driven cost swings. Changes in U.S.–Canada softwood policy or Mercosur trade terms can shift fiber and finished‑goods cost curves and compress LPX margins or force costly re‑routing. Active government relations reduce lead time for mitigation.

Housing and infrastructure policy

Federal housing and resilience programs, alongside the $1.2 trillion Infrastructure Investment and Jobs Act, boost demand for engineered wood by funding affordable housing and retrofit projects. Increased infrastructure spending supports the roughly 7.5 million US construction jobs (2024), improving logistics and throughput for Louisiana-Pacific. Local upzoning and infill reforms drive higher material volumes per site. Policy delays or funding gaps can defer multi‑year project volumes.

Regional incentives and siting

Plant siting decisions hinge on state tax credits, energy incentives and workforce grants; all 50 states offer some form of site-selection incentives as of 2024. Stable political environments reduce permitting risk and cycle time, while gubernatorial terms of four years mean shifts in priorities can disrupt subsidy continuity. LP can diversify its U.S. footprint across states to balance political risk and preserve project economics.

Environmental and forest policy

Environmental and forest policy—including forestry regulations, harvest quotas and public land management (USFS manages 193 million acres)—directly affects LPX fiber availability and price; biodiversity and wildfire mitigation measures have increased stumpage and access constraints, while policy-driven carbon markets create potential credits or compliance costs, making agency engagement critical for supply stability.

International operations risk

International operations in Chile and Brazil face election cycles, policy swings and occasional currency controls that can alter costs and repatriation; export licenses and customs procedures lengthen lead times for lumber and engineered wood shipments. Political unrest and strikes can block key transport corridors, raising logistics costs and inventory risk. Scenario planning and hedging reduce geopolitical exposure.

- Election/policy volatility

- Currency control risk

- Export/customs delays

- Transport corridor disruptions

- Scenario planning/hedging

Softwood faces 20–25% tariff risk; $1.2T infra lifts engineered‑wood demand

LPX is exposed to 20–25% softwood tariff risk and trade‑driven cost swings across US, Canada and Latin America. Federal programs including the $1.2T Infrastructure Law and ~7.5M US construction jobs (2024) boost engineered‑wood demand but funding delays can defer volumes. Forestry rules (USFS 193M acres) and carbon markets affect fiber costs; election/currency risk raises export and repatriation uncertainty.

| Factor | 2024/25 Metric | Impact |

|---|---|---|

| Tariffs | 20–25% | Margin compression |

| Infrastructure | $1.2T | Demand tailwind |

| Construction jobs | 7.5M | Improved demand/logistics |

| Forestry | USFS 193M acres | Fiber/access constraints |

What is included in the product

Provides a concise PESTLE analysis of Louisiana-Pacific, examining Political, Economic, Social, Technological, Environmental and Legal factors and their specific impacts on LP’s operations and strategy. Each section is data-driven, regionally grounded and includes forward-looking implications to inform executives, investors and planners.

A concise, visually segmented Louisiana‑Pacific PESTLE summary that fits into presentations or strategy packs, supports quick team alignment, and lets users add region‑ or business‑specific notes to ease external risk discussions and planning.

Economic factors

Housing cycle sensitivity

LP volumes move with U.S. housing starts (about 1.4M annualized in 2024 per U.S. Census) and repair/remodel spending; with 30-year mortgage rates near 7% in 2024 (Freddie Mac), new construction has softened while R&R demand has held up. Regional housing strength can offset national slowdowns, and builder backlogs of roughly 4–5 months (NAHB early‑2024) drive near‑term LP orders.

Commodity price volatility

OSB pricing is highly cyclical, with spot prices historically swinging more than 50% year-over-year as supply-demand balances shift; Louisiana-Pacific earnings move with those cycles. Input costs for resins, waxes and energy—which accounted for a meaningful portion of manufacturing cost in LP filings—add margin variability. Hedging programs and flexible sales contracts help stabilize EBITDA, while industry-wide capacity discipline remains a primary driver of price recovery.

Labor and logistics costs

Tight labor markets (US unemployment 2024 avg 3.7%) pushed manufacturing wage growth about 4.3% in 2024, raising mill and contractor labor costs for Louisiana-Pacific. Trucking availability, rail service and diesel at roughly $4.03/gal (2024 avg, EIA) materially affect delivered costs. LPX’s seven-mill North American OSB network and near-shoring shorten hauls, while ongoing efficiency projects aim to offset structural cost inflation.

Foreign exchange impacts

USD volatility versus CAD (≈1.36 mid‑2025), BRL (≈5.20) and MXN (≈17.8) affects LP’s cross‑border costs and translation; a strong USD can pressure exports while lowering imported input costs. Local sourcing creates natural hedges that cut transaction exposure, and treasury strategies (forwards, netting) manage residual FX risk.

- USD/CAD ≈1.36 — translation risk

- BRL ≈5.20, MXN ≈17.8 — regional cost swings

- Treasury: forwards, netting, local financing

Business mix resilience

Louisiana-Pacific's mix tilt toward siding and value-added products cushions revenue versus commodity OSB, whose spot prices swung from about $1,100/MSF at the 2021 peak to roughly $300–400/MSF by 2023, amplifying margins in durable channels. Growing repair/remodel and light-commercial sales smooth demand cycles and support margin floors, while active capacity allocation lets LPX pivot between OSB and specialty lines to match market conditions.

- Siding/value-added: steadier pricing, higher margin resilience

- OSB volatility: $1,100/MSF peak (2021) to ~$300–400/MSF (2023)

- Repair/remodel + light commercial: demand smoothing

- Balanced capacity allocation: aligns supply with pricing signals

Softwood faces 20–25% tariff risk; $1.2T infra lifts engineered‑wood demand

LP volumes follow US housing starts (~1.4M annualized in 2024) and R&R; 30‑yr mortgage ~7% in 2024 dampened new builds while R&R held. OSB price cyclicality (peak ~$1,100/MSF 2021 to ~$300–400/MSF 2023) and resin/energy costs drive earnings volatility. Tight labor (2024 unemployment ~3.7%) and diesel ~$4.03/gal raise delivered costs; USD/CAD ~1.36 (mid‑2025) and hedging limit FX impact.

| Metric | Value |

|---|---|

| Housing starts (2024) | ~1.4M |

| 30‑yr mortgage (2024) | ~7% |

| OSB price swing | $1,100 → $300–400/MSF |

| Unemployment (2024) | ~3.7% |

| Diesel (2024 avg) | $4.03/gal |

| USD/CAD (mid‑2025) | ~1.36 |

Same Document Delivered

Louisiana-Pacific PESTLE Analysis

The preview shown here is the exact Louisiana‑Pacific PESTLE Analysis you’ll receive after purchase—fully formatted, professionally structured, and ready to use. This is a real screenshot of the product with no placeholders or surprises. The content, layout, and sections visible are the final downloadable file. Immediate download follows checkout.