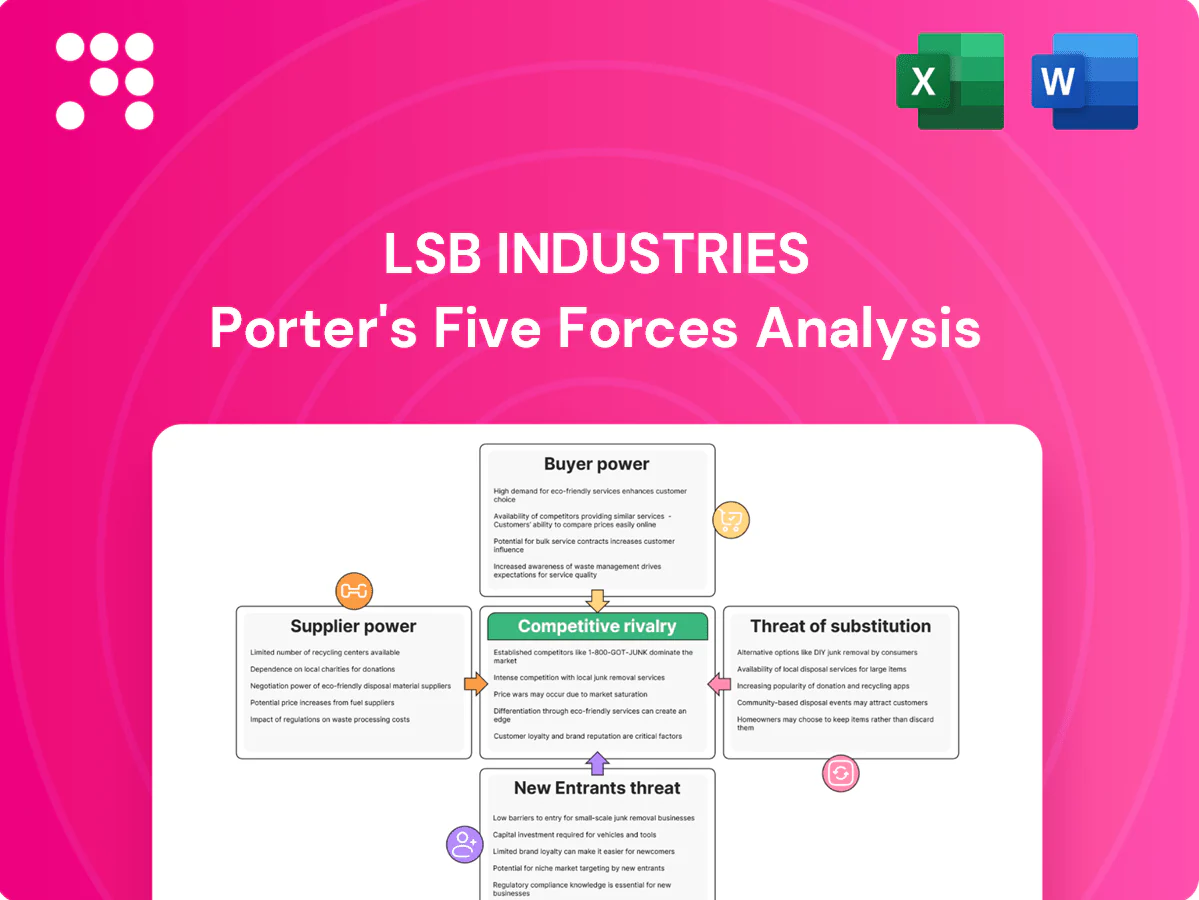

LSB Industries Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

LSB Industries faces moderate supplier power, cyclical demand and regulatory headwinds that shape pricing and margin pressure; substitutes and new entrants pose limited but growing threats as market consolidation shifts dynamics. This brief highlights key competitive pressures and strategic levers. The complete report reveals the real forces shaping LSB Industries’s industry—from supplier influence to threat of new entrants. Unlock the full Porter's Five Forces Analysis to explore LSB Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Natural gas feedstock dependency

LSB’s ammonia and nitrate production is highly feedstock‑intensive, tying costs to natural gas — Henry Hub averaged about $3/MMBtu in 2024, with regional basis differentials of up to $1/MMBtu that can widen or compress margins. Long‑term gas hedges reduce exposure to spikes (which briefly exceeded $8/MMBtu in winter 2024) but do not remove supply‑risk, giving suppliers leverage during tight market or low‑storage periods.

Limited alternative feedstocks

Ammonia and nitrogen chemistry depend on hydrogen from natural gas and specific catalysts, making feedstock changes operationally impractical; globally in 2024 over 95% of ammonia capacity remained fossil-based. Retrofitting or building green-hydrogen feedstock routes is capex-intensive and time-consuming. This constraint limits substitution away from existing suppliers and modestly elevates supplier power for LSB Industries.

Rail, trucking, and terminal logistics

Outbound and inbound logistics for LSB Industries depend on railcars, trucking fleets, and storage terminals; trucking moves about 72% of US freight by weight (ATA) while rail accounts for roughly 42% of intercity ton‑miles as of 2024 (AAR), concentrating supplier leverage. Tight equipment availability or terminal congestion during peaks raises spot rates and delays, giving carriers and terminal operators pricing power. Long‑term contracts and capacity reservations can partially offset this volatility and cap exposure to spot spikes.

Catalysts, equipment, and maintenance parts

Specialized catalysts and OEM maintenance parts for nitric-acid and fertilizer plants are supplied by few qualified vendors, creating concentrated supplier power and long lead times (often 12–24 weeks) for critical replacements.

Planned turnarounds compress demand into short windows, driving urgency premiums and spot-price spikes that materially raise outage costs; supplier technical know-how and warranty terms create switching frictions and contractual stickiness.

Multi-sourcing and inventory buffering reduce but do not eliminate dependence on specialist vendors, leaving LSB exposed to supplier-led schedule and price risk.

- Few qualified vendors — long lead times (12–24 weeks)

- Turnarounds concentrate demand — urgency premiums and spot spikes

- Supplier know-how + warranties increase switching costs

- Multi-sourcing mitigates but cannot remove dependence

Utilities and reliability constraints

Nitrogen production is energy- and water-intensive—Haber-Bosch synthesis typically requires about 8–10 MWh per tonne of ammonia and plants target >90–95% uptime, making continuous feedstocks and utilities critical. Grid reliability issues and limited water access can force curtailments that weaken LSB Industries’ negotiating leverage. Utilities commonly pass through fuel and infrastructure-driven rate hikes, and while onsite redundancy and long-term power/water contracts reduce risk, they do not eliminate exposure to outages or tariff shocks.

- Energy intensity: 8–10 MWh/tonne

- Target uptime: >90–95%

- Grid/water constraints → curtailed output, weaker supplier leverage

- Utilities can pass through rate increases

- Mitigants: onsite redundancy, long-term contracts (partial protection)

Suppliers wield leverage: gas spikes, 95% fossil ammonia, long lead times

Suppliers hold moderate-to-high power: 2024 Henry Hub averaged ~$3/MMBtu (spikes >$8), ~95% of ammonia capacity remained fossil‑based, limiting substitution; specialist catalysts/parts have 12–24 week lead times and turnarounds drive urgency premiums. Logistics concentration (truck 72% freight by weight; rail 42% intercity ton‑miles) and energy intensity (8–10 MWh/tonne; uptime >90%) reinforce supplier leverage.

| Factor | 2024 datapoint |

|---|---|

| Natural gas price | $3/MMBtu avg; spikes >$8 |

| Ammonia feedstock | ~95% fossil |

| Lead times | 12–24 weeks |

| Energy use | 8–10 MWh/tonne |

What is included in the product

Tailored Porter’s Five Forces analysis of LSB Industries uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptions affecting pricing, margins, and market share.

Concise one-sheet Porter's Five Forces for LSB Industries that visualizes competitive pressure and risks, customizable by scenario, export-ready for decks, no macros, easy to edit, and integrates seamlessly into broader reports.

Customers Bargaining Power

Commodity product and price sensitivity

Nitrogen fertilizers and many industrial nitrogen products are largely undifferentiated, so buyers benchmark offers against spot indexes such as Argus and Green Markets and against import prices. Small price gaps, often single-digit percent differences, routinely trigger switching to alternative suppliers or imports. This high price sensitivity materially strengthens buyer bargaining power for LSB Industries.

Agriculture seasonality and bulk distributors

Seasonal demand concentrates purchases into 4–8 week planting windows, compressing LSB’s selling period and intensifying buyer leverage. Large distributors and co-ops aggregate volumes—often representing regional demand peaks—and negotiate aggressively on price and logistics. Off-season programs trade price concessions for 6–12 month volume commitments, and the resulting timing pressure further strengthens buyer bargaining power.

Industrial and mining contracts

Industrial and mining customers typically sign multi-year, formula-based contracts (commonly 3–5 years) that stabilize volumes for LSB Industries by locking demand and reducing sales volatility.

Index-linked pricing in those contracts ties LSB receipts to commodity indices, which limits upside for the company when spot market tightness occurs.

Large buyers with access to alternative suppliers or backward integration therefore retain meaningful negotiating clout on price, volume and contract terms.

Freight economics and regional options

Delivered cost for LSB Industries is freight-sensitive; as of 2024 U.S. railroads account for roughly 40% of freight ton-miles, so buyers inside LSB’s rail radius can accept smaller discounts because rail savings lower delivered cost. Distant buyers face higher transport and can leverage imports to pressure prices, while geographic proximity moderates but does not eliminate buyer bargaining power.

- Inside rail radius: lower delivered cost, less discount pressure

- Distant buyers: import competition elevates bargaining power

- 2024 rail share ~40% of ton-miles supports proximity advantage

Product quality and reliability expectations

Product quality, consistency, on-time delivery and safety are critical for LSB; failures can halt planting or industrial operations and sharply raise switching threats, especially during peak 2024 planting windows.

Strong after-sales service and reliability can reduce buyer focus on price somewhat, but price remains the dominant decision factor for most agricultural and industrial customers in 2024.

- Consistency: prevents operational shutdowns

- On-time delivery: critical during planting season

- Safety: regulatory and liability implications

- Service: moderates but does not eliminate price sensitivity

Buyers dominate pricing; import pressure persists despite rail ~40% share

Buyers have high bargaining power: undifferentiated nitrogen products, index-linked pricing and easy import substitution make price dominant. Seasonal 4–8 week demand peaks and large distributor aggregation intensify leverage, though 3–5 year industrial contracts stabilize volumes. Rail proximity reduces delivered cost but 2024 U.S. rail share (~40% ton-miles) still leaves import pressure for distant buyers.

| Metric | Value (2024) |

|---|---|

| Rail share of ton-miles | ~40% |

| Typical contract length | 3–5 years |

| Seasonal buying window | 4–8 weeks |

| Price sensitivity | High; single-digit gaps trigger switching |

What You See Is What You Get

LSB Industries Porter's Five Forces Analysis

This Porter's Five Forces analysis of LSB Industries evaluates competitive rivalry, supplier and buyer power, threats of substitutes, and barriers to entry, with actionable implications for strategy and valuation. This preview shows the exact document you'll receive—no surprises, no placeholders. The file is fully formatted and ready for immediate download and use upon purchase.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

LSB Industries faces moderate supplier power, cyclical demand and regulatory headwinds that shape pricing and margin pressure; substitutes and new entrants pose limited but growing threats as market consolidation shifts dynamics. This brief highlights key competitive pressures and strategic levers. The complete report reveals the real forces shaping LSB Industries’s industry—from supplier influence to threat of new entrants. Unlock the full Porter's Five Forces Analysis to explore LSB Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Natural gas feedstock dependency

LSB’s ammonia and nitrate production is highly feedstock‑intensive, tying costs to natural gas — Henry Hub averaged about $3/MMBtu in 2024, with regional basis differentials of up to $1/MMBtu that can widen or compress margins. Long‑term gas hedges reduce exposure to spikes (which briefly exceeded $8/MMBtu in winter 2024) but do not remove supply‑risk, giving suppliers leverage during tight market or low‑storage periods.

Limited alternative feedstocks

Ammonia and nitrogen chemistry depend on hydrogen from natural gas and specific catalysts, making feedstock changes operationally impractical; globally in 2024 over 95% of ammonia capacity remained fossil-based. Retrofitting or building green-hydrogen feedstock routes is capex-intensive and time-consuming. This constraint limits substitution away from existing suppliers and modestly elevates supplier power for LSB Industries.

Rail, trucking, and terminal logistics

Outbound and inbound logistics for LSB Industries depend on railcars, trucking fleets, and storage terminals; trucking moves about 72% of US freight by weight (ATA) while rail accounts for roughly 42% of intercity ton‑miles as of 2024 (AAR), concentrating supplier leverage. Tight equipment availability or terminal congestion during peaks raises spot rates and delays, giving carriers and terminal operators pricing power. Long‑term contracts and capacity reservations can partially offset this volatility and cap exposure to spot spikes.

Catalysts, equipment, and maintenance parts

Specialized catalysts and OEM maintenance parts for nitric-acid and fertilizer plants are supplied by few qualified vendors, creating concentrated supplier power and long lead times (often 12–24 weeks) for critical replacements.

Planned turnarounds compress demand into short windows, driving urgency premiums and spot-price spikes that materially raise outage costs; supplier technical know-how and warranty terms create switching frictions and contractual stickiness.

Multi-sourcing and inventory buffering reduce but do not eliminate dependence on specialist vendors, leaving LSB exposed to supplier-led schedule and price risk.

- Few qualified vendors — long lead times (12–24 weeks)

- Turnarounds concentrate demand — urgency premiums and spot spikes

- Supplier know-how + warranties increase switching costs

- Multi-sourcing mitigates but cannot remove dependence

Utilities and reliability constraints

Nitrogen production is energy- and water-intensive—Haber-Bosch synthesis typically requires about 8–10 MWh per tonne of ammonia and plants target >90–95% uptime, making continuous feedstocks and utilities critical. Grid reliability issues and limited water access can force curtailments that weaken LSB Industries’ negotiating leverage. Utilities commonly pass through fuel and infrastructure-driven rate hikes, and while onsite redundancy and long-term power/water contracts reduce risk, they do not eliminate exposure to outages or tariff shocks.

- Energy intensity: 8–10 MWh/tonne

- Target uptime: >90–95%

- Grid/water constraints → curtailed output, weaker supplier leverage

- Utilities can pass through rate increases

- Mitigants: onsite redundancy, long-term contracts (partial protection)

Suppliers wield leverage: gas spikes, 95% fossil ammonia, long lead times

Suppliers hold moderate-to-high power: 2024 Henry Hub averaged ~$3/MMBtu (spikes >$8), ~95% of ammonia capacity remained fossil‑based, limiting substitution; specialist catalysts/parts have 12–24 week lead times and turnarounds drive urgency premiums. Logistics concentration (truck 72% freight by weight; rail 42% intercity ton‑miles) and energy intensity (8–10 MWh/tonne; uptime >90%) reinforce supplier leverage.

| Factor | 2024 datapoint |

|---|---|

| Natural gas price | $3/MMBtu avg; spikes >$8 |

| Ammonia feedstock | ~95% fossil |

| Lead times | 12–24 weeks |

| Energy use | 8–10 MWh/tonne |

What is included in the product

Tailored Porter’s Five Forces analysis of LSB Industries uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptions affecting pricing, margins, and market share.

Concise one-sheet Porter's Five Forces for LSB Industries that visualizes competitive pressure and risks, customizable by scenario, export-ready for decks, no macros, easy to edit, and integrates seamlessly into broader reports.

Customers Bargaining Power

Commodity product and price sensitivity

Nitrogen fertilizers and many industrial nitrogen products are largely undifferentiated, so buyers benchmark offers against spot indexes such as Argus and Green Markets and against import prices. Small price gaps, often single-digit percent differences, routinely trigger switching to alternative suppliers or imports. This high price sensitivity materially strengthens buyer bargaining power for LSB Industries.

Agriculture seasonality and bulk distributors

Seasonal demand concentrates purchases into 4–8 week planting windows, compressing LSB’s selling period and intensifying buyer leverage. Large distributors and co-ops aggregate volumes—often representing regional demand peaks—and negotiate aggressively on price and logistics. Off-season programs trade price concessions for 6–12 month volume commitments, and the resulting timing pressure further strengthens buyer bargaining power.

Industrial and mining contracts

Industrial and mining customers typically sign multi-year, formula-based contracts (commonly 3–5 years) that stabilize volumes for LSB Industries by locking demand and reducing sales volatility.

Index-linked pricing in those contracts ties LSB receipts to commodity indices, which limits upside for the company when spot market tightness occurs.

Large buyers with access to alternative suppliers or backward integration therefore retain meaningful negotiating clout on price, volume and contract terms.

Freight economics and regional options

Delivered cost for LSB Industries is freight-sensitive; as of 2024 U.S. railroads account for roughly 40% of freight ton-miles, so buyers inside LSB’s rail radius can accept smaller discounts because rail savings lower delivered cost. Distant buyers face higher transport and can leverage imports to pressure prices, while geographic proximity moderates but does not eliminate buyer bargaining power.

- Inside rail radius: lower delivered cost, less discount pressure

- Distant buyers: import competition elevates bargaining power

- 2024 rail share ~40% of ton-miles supports proximity advantage

Product quality and reliability expectations

Product quality, consistency, on-time delivery and safety are critical for LSB; failures can halt planting or industrial operations and sharply raise switching threats, especially during peak 2024 planting windows.

Strong after-sales service and reliability can reduce buyer focus on price somewhat, but price remains the dominant decision factor for most agricultural and industrial customers in 2024.

- Consistency: prevents operational shutdowns

- On-time delivery: critical during planting season

- Safety: regulatory and liability implications

- Service: moderates but does not eliminate price sensitivity

Buyers dominate pricing; import pressure persists despite rail ~40% share

Buyers have high bargaining power: undifferentiated nitrogen products, index-linked pricing and easy import substitution make price dominant. Seasonal 4–8 week demand peaks and large distributor aggregation intensify leverage, though 3–5 year industrial contracts stabilize volumes. Rail proximity reduces delivered cost but 2024 U.S. rail share (~40% ton-miles) still leaves import pressure for distant buyers.

| Metric | Value (2024) |

|---|---|

| Rail share of ton-miles | ~40% |

| Typical contract length | 3–5 years |

| Seasonal buying window | 4–8 weeks |

| Price sensitivity | High; single-digit gaps trigger switching |

What You See Is What You Get

LSB Industries Porter's Five Forces Analysis

This Porter's Five Forces analysis of LSB Industries evaluates competitive rivalry, supplier and buyer power, threats of substitutes, and barriers to entry, with actionable implications for strategy and valuation. This preview shows the exact document you'll receive—no surprises, no placeholders. The file is fully formatted and ready for immediate download and use upon purchase.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

LSB Industries faces moderate supplier power, cyclical demand and regulatory headwinds that shape pricing and margin pressure; substitutes and new entrants pose limited but growing threats as market consolidation shifts dynamics. This brief highlights key competitive pressures and strategic levers. The complete report reveals the real forces shaping LSB Industries’s industry—from supplier influence to threat of new entrants. Unlock the full Porter's Five Forces Analysis to explore LSB Industries’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Natural gas feedstock dependency

LSB’s ammonia and nitrate production is highly feedstock‑intensive, tying costs to natural gas — Henry Hub averaged about $3/MMBtu in 2024, with regional basis differentials of up to $1/MMBtu that can widen or compress margins. Long‑term gas hedges reduce exposure to spikes (which briefly exceeded $8/MMBtu in winter 2024) but do not remove supply‑risk, giving suppliers leverage during tight market or low‑storage periods.

Limited alternative feedstocks

Ammonia and nitrogen chemistry depend on hydrogen from natural gas and specific catalysts, making feedstock changes operationally impractical; globally in 2024 over 95% of ammonia capacity remained fossil-based. Retrofitting or building green-hydrogen feedstock routes is capex-intensive and time-consuming. This constraint limits substitution away from existing suppliers and modestly elevates supplier power for LSB Industries.

Rail, trucking, and terminal logistics

Outbound and inbound logistics for LSB Industries depend on railcars, trucking fleets, and storage terminals; trucking moves about 72% of US freight by weight (ATA) while rail accounts for roughly 42% of intercity ton‑miles as of 2024 (AAR), concentrating supplier leverage. Tight equipment availability or terminal congestion during peaks raises spot rates and delays, giving carriers and terminal operators pricing power. Long‑term contracts and capacity reservations can partially offset this volatility and cap exposure to spot spikes.

Catalysts, equipment, and maintenance parts

Specialized catalysts and OEM maintenance parts for nitric-acid and fertilizer plants are supplied by few qualified vendors, creating concentrated supplier power and long lead times (often 12–24 weeks) for critical replacements.

Planned turnarounds compress demand into short windows, driving urgency premiums and spot-price spikes that materially raise outage costs; supplier technical know-how and warranty terms create switching frictions and contractual stickiness.

Multi-sourcing and inventory buffering reduce but do not eliminate dependence on specialist vendors, leaving LSB exposed to supplier-led schedule and price risk.

- Few qualified vendors — long lead times (12–24 weeks)

- Turnarounds concentrate demand — urgency premiums and spot spikes

- Supplier know-how + warranties increase switching costs

- Multi-sourcing mitigates but cannot remove dependence

Utilities and reliability constraints

Nitrogen production is energy- and water-intensive—Haber-Bosch synthesis typically requires about 8–10 MWh per tonne of ammonia and plants target >90–95% uptime, making continuous feedstocks and utilities critical. Grid reliability issues and limited water access can force curtailments that weaken LSB Industries’ negotiating leverage. Utilities commonly pass through fuel and infrastructure-driven rate hikes, and while onsite redundancy and long-term power/water contracts reduce risk, they do not eliminate exposure to outages or tariff shocks.

- Energy intensity: 8–10 MWh/tonne

- Target uptime: >90–95%

- Grid/water constraints → curtailed output, weaker supplier leverage

- Utilities can pass through rate increases

- Mitigants: onsite redundancy, long-term contracts (partial protection)

Suppliers wield leverage: gas spikes, 95% fossil ammonia, long lead times

Suppliers hold moderate-to-high power: 2024 Henry Hub averaged ~$3/MMBtu (spikes >$8), ~95% of ammonia capacity remained fossil‑based, limiting substitution; specialist catalysts/parts have 12–24 week lead times and turnarounds drive urgency premiums. Logistics concentration (truck 72% freight by weight; rail 42% intercity ton‑miles) and energy intensity (8–10 MWh/tonne; uptime >90%) reinforce supplier leverage.

| Factor | 2024 datapoint |

|---|---|

| Natural gas price | $3/MMBtu avg; spikes >$8 |

| Ammonia feedstock | ~95% fossil |

| Lead times | 12–24 weeks |

| Energy use | 8–10 MWh/tonne |

What is included in the product

Tailored Porter’s Five Forces analysis of LSB Industries uncovering competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and emerging disruptions affecting pricing, margins, and market share.

Concise one-sheet Porter's Five Forces for LSB Industries that visualizes competitive pressure and risks, customizable by scenario, export-ready for decks, no macros, easy to edit, and integrates seamlessly into broader reports.

Customers Bargaining Power

Commodity product and price sensitivity

Nitrogen fertilizers and many industrial nitrogen products are largely undifferentiated, so buyers benchmark offers against spot indexes such as Argus and Green Markets and against import prices. Small price gaps, often single-digit percent differences, routinely trigger switching to alternative suppliers or imports. This high price sensitivity materially strengthens buyer bargaining power for LSB Industries.

Agriculture seasonality and bulk distributors

Seasonal demand concentrates purchases into 4–8 week planting windows, compressing LSB’s selling period and intensifying buyer leverage. Large distributors and co-ops aggregate volumes—often representing regional demand peaks—and negotiate aggressively on price and logistics. Off-season programs trade price concessions for 6–12 month volume commitments, and the resulting timing pressure further strengthens buyer bargaining power.

Industrial and mining contracts

Industrial and mining customers typically sign multi-year, formula-based contracts (commonly 3–5 years) that stabilize volumes for LSB Industries by locking demand and reducing sales volatility.

Index-linked pricing in those contracts ties LSB receipts to commodity indices, which limits upside for the company when spot market tightness occurs.

Large buyers with access to alternative suppliers or backward integration therefore retain meaningful negotiating clout on price, volume and contract terms.

Freight economics and regional options

Delivered cost for LSB Industries is freight-sensitive; as of 2024 U.S. railroads account for roughly 40% of freight ton-miles, so buyers inside LSB’s rail radius can accept smaller discounts because rail savings lower delivered cost. Distant buyers face higher transport and can leverage imports to pressure prices, while geographic proximity moderates but does not eliminate buyer bargaining power.

- Inside rail radius: lower delivered cost, less discount pressure

- Distant buyers: import competition elevates bargaining power

- 2024 rail share ~40% of ton-miles supports proximity advantage

Product quality and reliability expectations

Product quality, consistency, on-time delivery and safety are critical for LSB; failures can halt planting or industrial operations and sharply raise switching threats, especially during peak 2024 planting windows.

Strong after-sales service and reliability can reduce buyer focus on price somewhat, but price remains the dominant decision factor for most agricultural and industrial customers in 2024.

- Consistency: prevents operational shutdowns

- On-time delivery: critical during planting season

- Safety: regulatory and liability implications

- Service: moderates but does not eliminate price sensitivity

Buyers dominate pricing; import pressure persists despite rail ~40% share

Buyers have high bargaining power: undifferentiated nitrogen products, index-linked pricing and easy import substitution make price dominant. Seasonal 4–8 week demand peaks and large distributor aggregation intensify leverage, though 3–5 year industrial contracts stabilize volumes. Rail proximity reduces delivered cost but 2024 U.S. rail share (~40% ton-miles) still leaves import pressure for distant buyers.

| Metric | Value (2024) |

|---|---|

| Rail share of ton-miles | ~40% |

| Typical contract length | 3–5 years |

| Seasonal buying window | 4–8 weeks |

| Price sensitivity | High; single-digit gaps trigger switching |

What You See Is What You Get

LSB Industries Porter's Five Forces Analysis

This Porter's Five Forces analysis of LSB Industries evaluates competitive rivalry, supplier and buyer power, threats of substitutes, and barriers to entry, with actionable implications for strategy and valuation. This preview shows the exact document you'll receive—no surprises, no placeholders. The file is fully formatted and ready for immediate download and use upon purchase.