LS Corp Boston Consulting Group Matrix

Actionable Strategy Starts Here

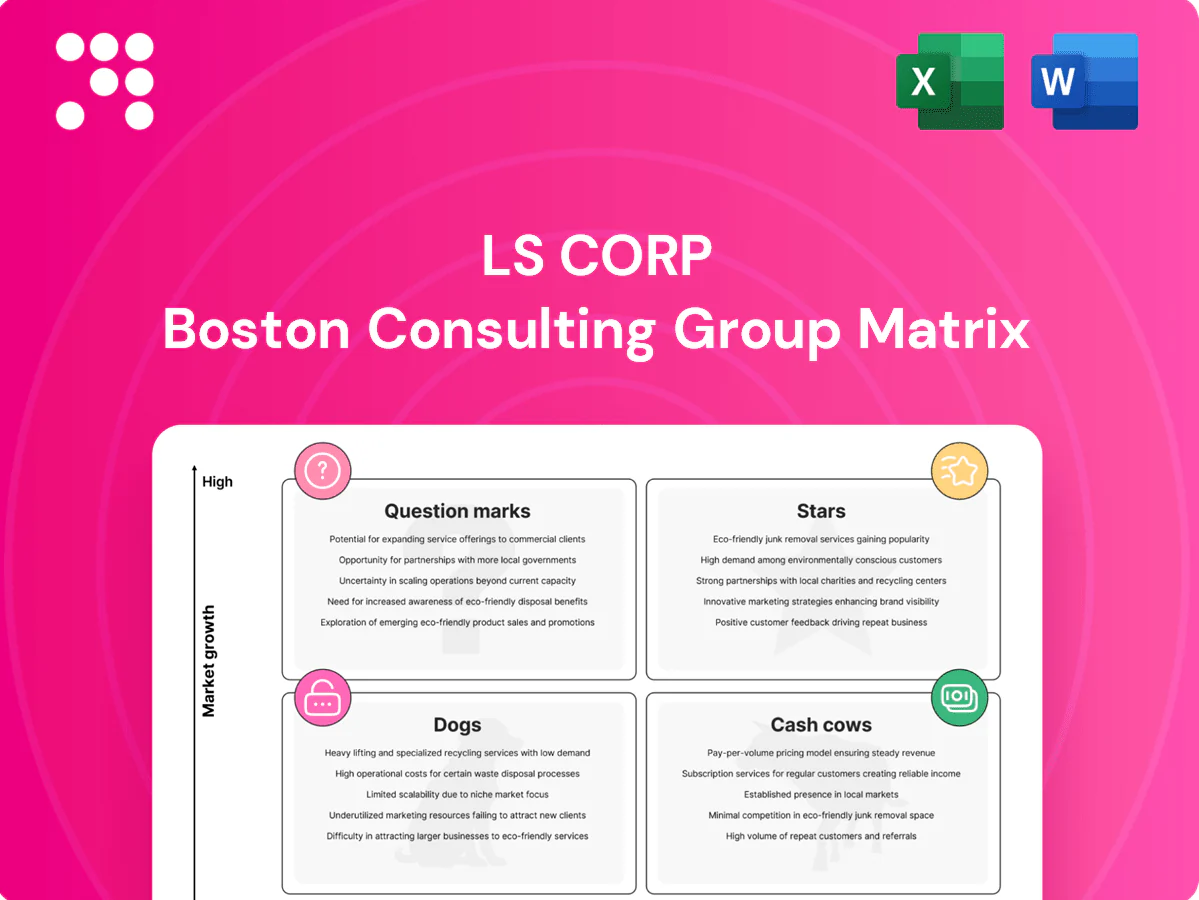

Curious where LS Corp’s products really sit—Stars, Cash Cows, Dogs, or Question Marks? This preview scratches the surface; the full BCG Matrix gives you quadrant-by-quadrant placements, data-backed recommendations, and a clear action plan. Buy the complete report for a Word analysis plus an Excel summary you can present and act on immediately.

Stars

Utility‑scale renewable cabling

Utility-scale renewable cabling is a Star: high-margin HV/DC export and array cables tied to offshore wind and large solar are surging, with the global offshore wind pipeline topping 500 GW by 2024 and utility-scale solar additions running in the several-hundreds of GW range. LS already wins major tenders and holds strong share as projects stack, driving volume payback despite heavy capex for plants, testing and vessels. Continue feeding capacity and locking long-term frame agreements to capture scale and margin.

Grid‑scale battery systems & EPC

Grid-scale battery deployments accelerated with renewables, with global annual battery additions ~20 GW in 2024, and LS’s integrated cables, switchgear and EPC delivery give it a competitive edge. Pipeline visibility is improving quarter over quarter, while current buildouts and balance‑of‑plant needs leave cash in roughly matching cash out. Recommend doubling down now to cement leadership before market growth plateaus.

HV/MV substations and grid upgrade packages

Electrification and grid reinforcement are driving strong demand for HV/MV substations, and LS’s turnkey packages align with utilities’ preference for integrated suppliers, yielding higher win rates where specs match LS gear.

Projects are capital intensive and engineering heavy, tightening working capital; contract margins hinge on delivery speed and financing terms.

Investing in engineering talent and modular designs will let LS scale faster than rivals and shorten CAPEX cycles.

EV power components (charging cables, connectors, harnesses)

EV power components (charging cables, connectors, harnesses) are a Star for LS: global charging equipment demand is growing double digits, with market forecasts >20% CAGR to 2030 (BNEF 2024) and rising OEM/CPO spend; LS holds credible share with Tier-1 OEMs and major CPOs and benefits from certification moats that raise switching costs.

- Promote aggressively

- Lock channel partnerships

- Commit capacity

- Protect certifications

- Hold share to convert Star → Cash Cow

Industrial automation power systems for fabs

Industrial automation power systems for fabs serve semiconductor and battery gigafactories requiring ultra-reliable distribution and clean, contamination-controlled cabling; LS secures marquee projects and repeat orders across leading fab builders. High engineering hours and specialized materials make scaling cash-thirsty, so LS must keep investing in standard modules and supplier lock-ins to defend premium pricing.

- Market: fab-grade power & clean cabling demand

- Strength: marquee projects, repeat orders

- Weakness: high OPEX and capex for scale

- Strategy: standard modules, supplier lock-in to protect margins

Scale converts >500 GW offshore, ~20 GW batteries & 20%+ EV growth into cash

Stars: utility-scale HV/DC cables, grid-scale batteries, EV charging components and fab-grade power show high growth and margin; offshore wind pipeline >500 GW (2024), battery additions ~20 GW (2024), EV charging CAGR >20% to 2030 (BNEF 2024). Scale requires capex, engineering and long-term contracts to convert Stars into cash cows.

| Segment | 2024 metric | Priority |

|---|---|---|

| Offshore cables | 500+ GW pipeline | Capacity + LTAs |

| Batteries | ~20 GW/yr additions | Integrated EPC |

| EV charging | >20% CAGR | Certs + share |

What is included in the product

Comprehensive BCG analysis of LS Corp's units, with clear strategic actions—invest, hold, or divest—plus risks and trends per quadrant.

One-page LS Corp BCG Matrix that maps units into quadrants — clean, export-ready and C-level friendly for fast decision-making.

Cash Cows

Low‑voltage building wires (domestic and commercial)

Mature category with dominant domestic share and predictable project and retrofit orders; global wire and cable market ~USD 210 billion in 2024, supporting steady demand. Margins benefit from scale and contractor brand trust, allowing GM premiums vs smaller players. Promo needs are light—availability and lead‑times win bids. Focus on plant utilization and tighter logistics to sustain cash generation.

Medium‑voltage utility cables (core catalog)

Medium‑voltage utility cables (core catalog) deliver steady, spec‑driven replacement and expansion volumes; APAC accounted for over 50% of global cable demand in 2024, keeping throughput high. LS is on approved vendor lists across APAC, protecting share and supporting mid‑single‑digit growth. Margins remain healthy via operational excellence, with focus on throughput, scrap reduction and strict service SLAs.

Conventional transformers and switchgear service

Installed base is huge and service contracts renew like clockwork, producing dependable parts and maintenance cash that underpins LS Corp’s conventional transformers and switchgear segment. The market is mature with price competition, but LS’s entrenched footprint preserves share and margins. Prioritizing standardized service kits and remote diagnostics in 2024 will widen the competitive gap and increase recurring revenue visibility.

Industrial machinery spare parts & retrofits

Industrial machinery spare parts & retrofits deliver steady cash flows for LS Corp: 2024 aftermarket gross margins ~30% versus new-build ~12%, aftermarket now ~35% of group service revenue; LS owns drawings so service volatility is lower and customers pay for uptime, not novelty. Low marketing spend yields solid contribution; digitized ordering and bundled warranties can lift attach rates 15–25% and reduce churn.

- Aftermarket margin ~30%

- New-build margin ~12%

- Aftermarket share ~35% of service revenue

- Attach-rate uplift 15–25% via digitize+warranty

- Low marketing spend, high contribution

Commodity copper cables for export

Commodity copper cables for export are a cash cow for LS: scale procurement and efficient plants keep unit costs low, with LME copper averaging about 9,200 USD/t in 2024 and industry EBITDA around 6–8%, so cash generation outweighs modest growth prospects. Demand is steady—infrastructure and industrial replacement markets—not flashy, supporting predictable free cash flow. Continue hedging metals and automating lines to protect margins and capex efficiency.

- cost-competitive: scale procurement, efficient plants

- market: steady demand, infrastructure-led

- finance: strong cash generation vs low growth

- risk mitigation: metal hedging, line automation

Mature wires, MV cables & spares drive steady high-margin cash; aftermarket GM ~30%

LS Corp cash cows: mature wire & cable, MV utility cables, transformers/switchgear services and aftermarket spares deliver steady high-margin cash flow (aftermarket GM ~30% vs new-build ~12%; aftermarket ~35% of service revenue in 2024). Global wire market ~USD 210bn (2024); LME copper ~USD 9,200/t (2024). Focus: plant utilization, hedging, digitized service attach.

| Segment | 2024 metric | GM/EBITDA | Notes |

|---|---|---|---|

| Wire & cable | Market USD 210bn | Premium vs peers | Scale, lead‑time wins |

| Aftermarket | 35% service rev | GM ~30% | High recurring cash |

| Commodity copper | LME 9,200 USD/t | EBITDA 6–8% | Hedge+automation |

What You See Is What You Get

LS Corp BCG Matrix

The file you're previewing is the exact LS Corp BCG Matrix you’ll receive after purchase. No watermarks, no demo content—just a fully formatted, ready-to-use strategic report designed for clear decision-making. It's editable, print-ready, and crafted by strategy pros so you can present or plug it into planning immediately. One one-time purchase, instant download, no surprises.

Actionable Strategy Starts Here

Curious where LS Corp’s products really sit—Stars, Cash Cows, Dogs, or Question Marks? This preview scratches the surface; the full BCG Matrix gives you quadrant-by-quadrant placements, data-backed recommendations, and a clear action plan. Buy the complete report for a Word analysis plus an Excel summary you can present and act on immediately.

Stars

Utility‑scale renewable cabling

Utility-scale renewable cabling is a Star: high-margin HV/DC export and array cables tied to offshore wind and large solar are surging, with the global offshore wind pipeline topping 500 GW by 2024 and utility-scale solar additions running in the several-hundreds of GW range. LS already wins major tenders and holds strong share as projects stack, driving volume payback despite heavy capex for plants, testing and vessels. Continue feeding capacity and locking long-term frame agreements to capture scale and margin.

Grid‑scale battery systems & EPC

Grid-scale battery deployments accelerated with renewables, with global annual battery additions ~20 GW in 2024, and LS’s integrated cables, switchgear and EPC delivery give it a competitive edge. Pipeline visibility is improving quarter over quarter, while current buildouts and balance‑of‑plant needs leave cash in roughly matching cash out. Recommend doubling down now to cement leadership before market growth plateaus.

HV/MV substations and grid upgrade packages

Electrification and grid reinforcement are driving strong demand for HV/MV substations, and LS’s turnkey packages align with utilities’ preference for integrated suppliers, yielding higher win rates where specs match LS gear.

Projects are capital intensive and engineering heavy, tightening working capital; contract margins hinge on delivery speed and financing terms.

Investing in engineering talent and modular designs will let LS scale faster than rivals and shorten CAPEX cycles.

EV power components (charging cables, connectors, harnesses)

EV power components (charging cables, connectors, harnesses) are a Star for LS: global charging equipment demand is growing double digits, with market forecasts >20% CAGR to 2030 (BNEF 2024) and rising OEM/CPO spend; LS holds credible share with Tier-1 OEMs and major CPOs and benefits from certification moats that raise switching costs.

- Promote aggressively

- Lock channel partnerships

- Commit capacity

- Protect certifications

- Hold share to convert Star → Cash Cow

Industrial automation power systems for fabs

Industrial automation power systems for fabs serve semiconductor and battery gigafactories requiring ultra-reliable distribution and clean, contamination-controlled cabling; LS secures marquee projects and repeat orders across leading fab builders. High engineering hours and specialized materials make scaling cash-thirsty, so LS must keep investing in standard modules and supplier lock-ins to defend premium pricing.

- Market: fab-grade power & clean cabling demand

- Strength: marquee projects, repeat orders

- Weakness: high OPEX and capex for scale

- Strategy: standard modules, supplier lock-in to protect margins

Scale converts >500 GW offshore, ~20 GW batteries & 20%+ EV growth into cash

Stars: utility-scale HV/DC cables, grid-scale batteries, EV charging components and fab-grade power show high growth and margin; offshore wind pipeline >500 GW (2024), battery additions ~20 GW (2024), EV charging CAGR >20% to 2030 (BNEF 2024). Scale requires capex, engineering and long-term contracts to convert Stars into cash cows.

| Segment | 2024 metric | Priority |

|---|---|---|

| Offshore cables | 500+ GW pipeline | Capacity + LTAs |

| Batteries | ~20 GW/yr additions | Integrated EPC |

| EV charging | >20% CAGR | Certs + share |

What is included in the product

Comprehensive BCG analysis of LS Corp's units, with clear strategic actions—invest, hold, or divest—plus risks and trends per quadrant.

One-page LS Corp BCG Matrix that maps units into quadrants — clean, export-ready and C-level friendly for fast decision-making.

Cash Cows

Low‑voltage building wires (domestic and commercial)

Mature category with dominant domestic share and predictable project and retrofit orders; global wire and cable market ~USD 210 billion in 2024, supporting steady demand. Margins benefit from scale and contractor brand trust, allowing GM premiums vs smaller players. Promo needs are light—availability and lead‑times win bids. Focus on plant utilization and tighter logistics to sustain cash generation.

Medium‑voltage utility cables (core catalog)

Medium‑voltage utility cables (core catalog) deliver steady, spec‑driven replacement and expansion volumes; APAC accounted for over 50% of global cable demand in 2024, keeping throughput high. LS is on approved vendor lists across APAC, protecting share and supporting mid‑single‑digit growth. Margins remain healthy via operational excellence, with focus on throughput, scrap reduction and strict service SLAs.

Conventional transformers and switchgear service

Installed base is huge and service contracts renew like clockwork, producing dependable parts and maintenance cash that underpins LS Corp’s conventional transformers and switchgear segment. The market is mature with price competition, but LS’s entrenched footprint preserves share and margins. Prioritizing standardized service kits and remote diagnostics in 2024 will widen the competitive gap and increase recurring revenue visibility.

Industrial machinery spare parts & retrofits

Industrial machinery spare parts & retrofits deliver steady cash flows for LS Corp: 2024 aftermarket gross margins ~30% versus new-build ~12%, aftermarket now ~35% of group service revenue; LS owns drawings so service volatility is lower and customers pay for uptime, not novelty. Low marketing spend yields solid contribution; digitized ordering and bundled warranties can lift attach rates 15–25% and reduce churn.

- Aftermarket margin ~30%

- New-build margin ~12%

- Aftermarket share ~35% of service revenue

- Attach-rate uplift 15–25% via digitize+warranty

- Low marketing spend, high contribution

Commodity copper cables for export

Commodity copper cables for export are a cash cow for LS: scale procurement and efficient plants keep unit costs low, with LME copper averaging about 9,200 USD/t in 2024 and industry EBITDA around 6–8%, so cash generation outweighs modest growth prospects. Demand is steady—infrastructure and industrial replacement markets—not flashy, supporting predictable free cash flow. Continue hedging metals and automating lines to protect margins and capex efficiency.

- cost-competitive: scale procurement, efficient plants

- market: steady demand, infrastructure-led

- finance: strong cash generation vs low growth

- risk mitigation: metal hedging, line automation

Mature wires, MV cables & spares drive steady high-margin cash; aftermarket GM ~30%

LS Corp cash cows: mature wire & cable, MV utility cables, transformers/switchgear services and aftermarket spares deliver steady high-margin cash flow (aftermarket GM ~30% vs new-build ~12%; aftermarket ~35% of service revenue in 2024). Global wire market ~USD 210bn (2024); LME copper ~USD 9,200/t (2024). Focus: plant utilization, hedging, digitized service attach.

| Segment | 2024 metric | GM/EBITDA | Notes |

|---|---|---|---|

| Wire & cable | Market USD 210bn | Premium vs peers | Scale, lead‑time wins |

| Aftermarket | 35% service rev | GM ~30% | High recurring cash |

| Commodity copper | LME 9,200 USD/t | EBITDA 6–8% | Hedge+automation |

What You See Is What You Get

LS Corp BCG Matrix

The file you're previewing is the exact LS Corp BCG Matrix you’ll receive after purchase. No watermarks, no demo content—just a fully formatted, ready-to-use strategic report designed for clear decision-making. It's editable, print-ready, and crafted by strategy pros so you can present or plug it into planning immediately. One one-time purchase, instant download, no surprises.

Original: $10.00

-65%$10.00

$3.50Description

Actionable Strategy Starts Here

Curious where LS Corp’s products really sit—Stars, Cash Cows, Dogs, or Question Marks? This preview scratches the surface; the full BCG Matrix gives you quadrant-by-quadrant placements, data-backed recommendations, and a clear action plan. Buy the complete report for a Word analysis plus an Excel summary you can present and act on immediately.

Stars

Utility‑scale renewable cabling

Utility-scale renewable cabling is a Star: high-margin HV/DC export and array cables tied to offshore wind and large solar are surging, with the global offshore wind pipeline topping 500 GW by 2024 and utility-scale solar additions running in the several-hundreds of GW range. LS already wins major tenders and holds strong share as projects stack, driving volume payback despite heavy capex for plants, testing and vessels. Continue feeding capacity and locking long-term frame agreements to capture scale and margin.

Grid‑scale battery systems & EPC

Grid-scale battery deployments accelerated with renewables, with global annual battery additions ~20 GW in 2024, and LS’s integrated cables, switchgear and EPC delivery give it a competitive edge. Pipeline visibility is improving quarter over quarter, while current buildouts and balance‑of‑plant needs leave cash in roughly matching cash out. Recommend doubling down now to cement leadership before market growth plateaus.

HV/MV substations and grid upgrade packages

Electrification and grid reinforcement are driving strong demand for HV/MV substations, and LS’s turnkey packages align with utilities’ preference for integrated suppliers, yielding higher win rates where specs match LS gear.

Projects are capital intensive and engineering heavy, tightening working capital; contract margins hinge on delivery speed and financing terms.

Investing in engineering talent and modular designs will let LS scale faster than rivals and shorten CAPEX cycles.

EV power components (charging cables, connectors, harnesses)

EV power components (charging cables, connectors, harnesses) are a Star for LS: global charging equipment demand is growing double digits, with market forecasts >20% CAGR to 2030 (BNEF 2024) and rising OEM/CPO spend; LS holds credible share with Tier-1 OEMs and major CPOs and benefits from certification moats that raise switching costs.

- Promote aggressively

- Lock channel partnerships

- Commit capacity

- Protect certifications

- Hold share to convert Star → Cash Cow

Industrial automation power systems for fabs

Industrial automation power systems for fabs serve semiconductor and battery gigafactories requiring ultra-reliable distribution and clean, contamination-controlled cabling; LS secures marquee projects and repeat orders across leading fab builders. High engineering hours and specialized materials make scaling cash-thirsty, so LS must keep investing in standard modules and supplier lock-ins to defend premium pricing.

- Market: fab-grade power & clean cabling demand

- Strength: marquee projects, repeat orders

- Weakness: high OPEX and capex for scale

- Strategy: standard modules, supplier lock-in to protect margins

Scale converts >500 GW offshore, ~20 GW batteries & 20%+ EV growth into cash

Stars: utility-scale HV/DC cables, grid-scale batteries, EV charging components and fab-grade power show high growth and margin; offshore wind pipeline >500 GW (2024), battery additions ~20 GW (2024), EV charging CAGR >20% to 2030 (BNEF 2024). Scale requires capex, engineering and long-term contracts to convert Stars into cash cows.

| Segment | 2024 metric | Priority |

|---|---|---|

| Offshore cables | 500+ GW pipeline | Capacity + LTAs |

| Batteries | ~20 GW/yr additions | Integrated EPC |

| EV charging | >20% CAGR | Certs + share |

What is included in the product

Comprehensive BCG analysis of LS Corp's units, with clear strategic actions—invest, hold, or divest—plus risks and trends per quadrant.

One-page LS Corp BCG Matrix that maps units into quadrants — clean, export-ready and C-level friendly for fast decision-making.

Cash Cows

Low‑voltage building wires (domestic and commercial)

Mature category with dominant domestic share and predictable project and retrofit orders; global wire and cable market ~USD 210 billion in 2024, supporting steady demand. Margins benefit from scale and contractor brand trust, allowing GM premiums vs smaller players. Promo needs are light—availability and lead‑times win bids. Focus on plant utilization and tighter logistics to sustain cash generation.

Medium‑voltage utility cables (core catalog)

Medium‑voltage utility cables (core catalog) deliver steady, spec‑driven replacement and expansion volumes; APAC accounted for over 50% of global cable demand in 2024, keeping throughput high. LS is on approved vendor lists across APAC, protecting share and supporting mid‑single‑digit growth. Margins remain healthy via operational excellence, with focus on throughput, scrap reduction and strict service SLAs.

Conventional transformers and switchgear service

Installed base is huge and service contracts renew like clockwork, producing dependable parts and maintenance cash that underpins LS Corp’s conventional transformers and switchgear segment. The market is mature with price competition, but LS’s entrenched footprint preserves share and margins. Prioritizing standardized service kits and remote diagnostics in 2024 will widen the competitive gap and increase recurring revenue visibility.

Industrial machinery spare parts & retrofits

Industrial machinery spare parts & retrofits deliver steady cash flows for LS Corp: 2024 aftermarket gross margins ~30% versus new-build ~12%, aftermarket now ~35% of group service revenue; LS owns drawings so service volatility is lower and customers pay for uptime, not novelty. Low marketing spend yields solid contribution; digitized ordering and bundled warranties can lift attach rates 15–25% and reduce churn.

- Aftermarket margin ~30%

- New-build margin ~12%

- Aftermarket share ~35% of service revenue

- Attach-rate uplift 15–25% via digitize+warranty

- Low marketing spend, high contribution

Commodity copper cables for export

Commodity copper cables for export are a cash cow for LS: scale procurement and efficient plants keep unit costs low, with LME copper averaging about 9,200 USD/t in 2024 and industry EBITDA around 6–8%, so cash generation outweighs modest growth prospects. Demand is steady—infrastructure and industrial replacement markets—not flashy, supporting predictable free cash flow. Continue hedging metals and automating lines to protect margins and capex efficiency.

- cost-competitive: scale procurement, efficient plants

- market: steady demand, infrastructure-led

- finance: strong cash generation vs low growth

- risk mitigation: metal hedging, line automation

Mature wires, MV cables & spares drive steady high-margin cash; aftermarket GM ~30%

LS Corp cash cows: mature wire & cable, MV utility cables, transformers/switchgear services and aftermarket spares deliver steady high-margin cash flow (aftermarket GM ~30% vs new-build ~12%; aftermarket ~35% of service revenue in 2024). Global wire market ~USD 210bn (2024); LME copper ~USD 9,200/t (2024). Focus: plant utilization, hedging, digitized service attach.

| Segment | 2024 metric | GM/EBITDA | Notes |

|---|---|---|---|

| Wire & cable | Market USD 210bn | Premium vs peers | Scale, lead‑time wins |

| Aftermarket | 35% service rev | GM ~30% | High recurring cash |

| Commodity copper | LME 9,200 USD/t | EBITDA 6–8% | Hedge+automation |

What You See Is What You Get

LS Corp BCG Matrix

The file you're previewing is the exact LS Corp BCG Matrix you’ll receive after purchase. No watermarks, no demo content—just a fully formatted, ready-to-use strategic report designed for clear decision-making. It's editable, print-ready, and crafted by strategy pros so you can present or plug it into planning immediately. One one-time purchase, instant download, no surprises.