LS SWOT Analysis

Make Insightful Decisions Backed by Expert Research

Unlock LS’s strategic roadmap with our full SWOT analysis — three-plus pages of research-backed strengths, risks, and growth levers tailored for investors and strategists. Purchase the complete report for editable Word and Excel files, expert commentary, and actionable recommendations to inform pitches, planning, and portfolio decisions.

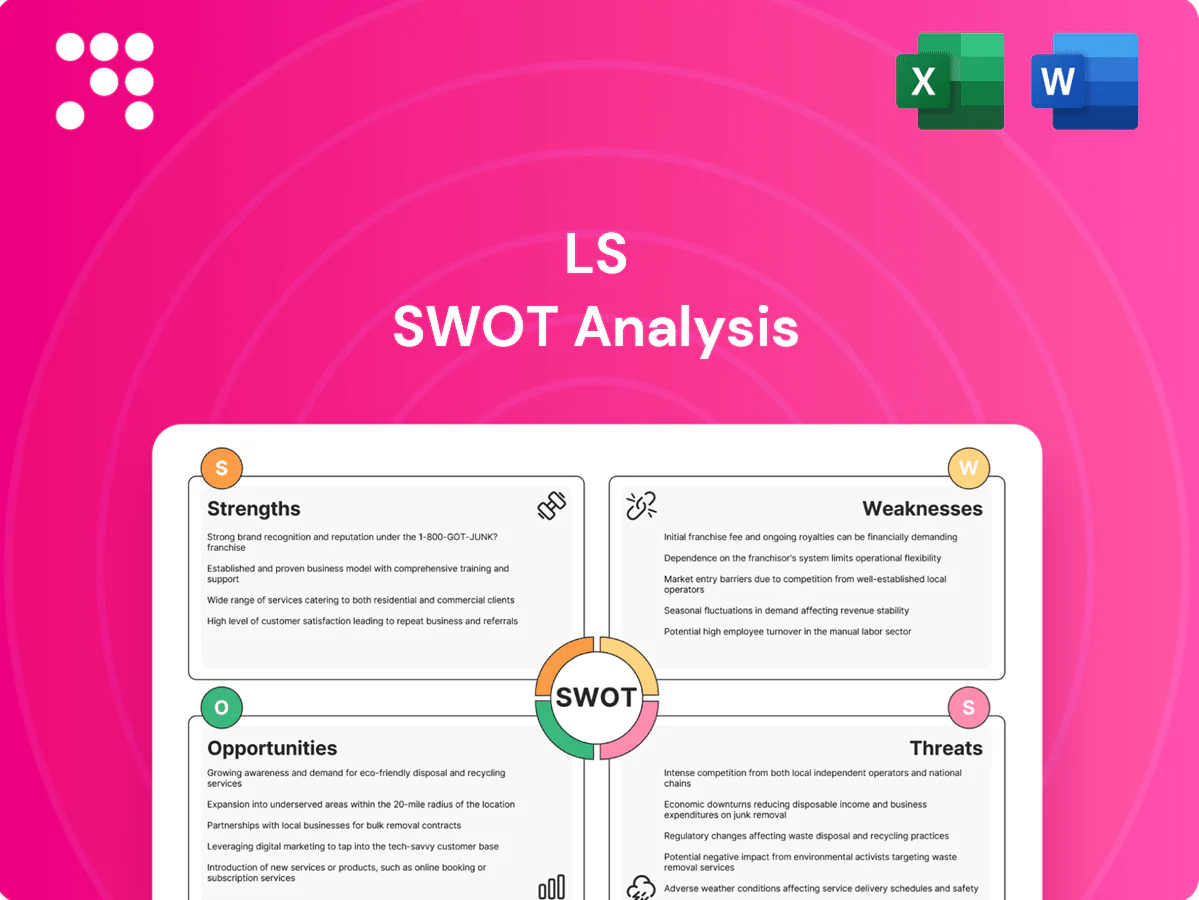

Strengths

Diversified industrial portfolio

LS spans power cables, electrical equipment, industrial machinery and electronic components, reducing reliance on any single revenue stream. This spread helps balance cyclical swings across end-markets, smoothing demand volatility. Cross-selling and shared engineering deliver cost leverage through common platforms and pooled R&D. The portfolio mix strengthens resilience during sector-specific downturns.

Deep power and grid expertise

Core competence in transmission, distribution and power materials positions LS to capture accelerating grid expansion; proven engineering capabilities and international certifications enable bids on complex high-voltage projects. A documented track record lifts win rates and pricing power, supporting entry into premium niches such as HV and specialty cables.

Vertical integration in materials

Vertical integration from conductive materials to finished systems lets LS control quality and cost across the chain, reducing external procurement and inspection needs. Owning copper, aluminum and specialty polymer inputs mitigates supply risk and price pass-through volatility. Close ties between materials and product teams shorten innovation cycles and enable margin expansion through value capture at multiple stages.

Innovation and R&D focus

Investment in advanced cables, components and factory automation drives clear performance differentiation, with proprietary processes and design know-how creating high technical barriers to entry and protecting margin. R&D alignment with electrification and sustainability trends enhances customer relevance and supports long-term product roadmaps, enabling iterative platform upgrades and modular solutions.

- Performance differentiation via advanced materials and automation

- Barriers to entry from proprietary processes

- Sustainability-aligned R&D boosts customer relevance

- R&D underpins long-term roadmaps

Strong home base with global reach

South Korea's advanced domestic market—GDP about $1.8 trillion (IMF 2024) and R&D intensity 4.63% of GDP (OECD 2023)—provides high-tech reference projects; international subsidiaries and export channels scale operations and learning, supported by Korea's $655 billion in goods exports in 2023 (KCS). Regional diversification across Asia‑Pacific opens growth corridors and improves procurement and customer proximity.

- R&D: 4.63% of GDP (OECD 2023)

- Exports: $655B (KCS 2023)

- GDP: ~$1.8T (IMF 2024)

Electrification specialist: vertical integration and proprietary manufacturing fuel margin gains

LS combines diversified product lines, vertical integration and proprietary manufacturing to lower costs, shorten development cycles and protect margins. Strong engineering and HV credentials support premium project wins and cross-selling. R&D focus aligns with electrification and sustainability, leveraging South Korea's high-tech ecosystem and export channels to scale internationally.

| Metric | Value | Source/Year |

|---|---|---|

| KR GDP | ~$1.8T | IMF 2024 |

| R&D Intensity | 4.63% GDP | OECD 2023 |

| Goods Exports | $655B | KCS 2023 |

What is included in the product

Delivers a strategic overview of LS’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and guide strategic decision-making.

LS SWOT Analysis delivers a focused, editable template that converts complex strategic gaps into clear action items, enabling faster cross-team alignment and quicker decision-making.

Weaknesses

Capex-heavy, long-cycle business

Project-driven revenues create timing risk and lumpy cash flows as large contracts need bonding, upfront working capital and complex execution across multi-year schedules. Returns can be delayed by permitting or client financing, pushing paybacks beyond original forecasts and magnifying exposure to a weak cycle; IMF data show world GDP grew 3.0% in 2024, underscoring macro sensitivity. Such dynamics raise downside risk in slowdowns.

Exposure to commodity volatility

Inputs like copper (LME avg ~$9,500/t in 2024) and aluminum (~$2,300/t) drive LS cost base and contract pricing. Hedging reduces but does not eliminate margin risk, leaving residual exposure to market moves. Rapid swings can compress mid-project profitability. Customers may delay or cancel orders during price spikes, as seen in 2022–24 episodes.

Conglomerate complexity

Multiple subsidiaries can dilute LSs strategic focus and agility, contributing to the well-documented conglomerate discount of roughly 15% in firm valuations versus focused peers. Intercompany dependencies obscure performance transparency, complicating segment-level margins and cash flows. Governance and capital-allocation trade-offs often lead to suboptimal investment choices, while integration and restructuring costs can shave several percentage points off near-term ROIC.

High fixed costs and utilization risk

High fixed costs mean manufacturing footprints need steady volume to absorb overheads; US manufacturing capacity utilization averaged about 76% in 2024 (Federal Reserve), so downturns quickly erode margins. Underutilization in troughs forces margin compression, and scaling down capacity is costly and slow given multi-year plant exit timelines. Pricing discipline can be tested as firms cut prices to keep lines running and preserve fixed-cost absorption.

- Fixed-cost intensity: large share of COGS tied to overhead

- Utilization risk: ~76% US manufacturing utilization in 2024

- Exit cost: plant closures take years and incur write-downs

- Price pressure: risk of margin dilution to maintain throughput

Foreign exchange and geopolitical exposure

Export sales and overseas operations expose LS to significant FX volatility; global foreign exchange turnover was $7.5 trillion per day (BIS, 2019), amplifying translation and transaction risk. Regional tensions and 2023 Red Sea disruptions forced rerouting and lifted logistics and insurance costs. Multijurisdictional compliance increases administrative burdens and can raise financing spreads.

- FX exposure — global FX turnover $7.5T/day (BIS 2019)

- Logistics disruption — 2023 Red Sea rerouting increased freight/insurance

- Cost pressure — higher compliance, insurance and financing spreads

Project revenues lumpy; GDP 3.0%, copper $9,500/t

Project-driven revenues create lumpy cash flow and permit/finance delays; world GDP grew 3.0% in 2024, heightening cycle sensitivity. Input cost exposure (copper ~9,500/t; aluminum ~2,300/t in 2024) and hedging gaps can compress mid-project margins. High fixed costs (US utilization ~76% in 2024) and conglomerate discount (~15%) reduce agility. FX/logistics risk persists (FX turnover $7.5T/day).

| Metric | 2024 |

|---|---|

| World GDP growth (IMF) | 3.0% |

| Copper (LME avg) | $9,500/t |

| Aluminum | $2,300/t |

| US manuf. utilization (Fed) | 76% |

| Conglomerate discount | ~15% |

| FX turnover (BIS) | $7.5T/day |

What You See Is What You Get

LS SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the complete report you'll get; purchase unlocks the full, editable version. You’re viewing a live preview of the real file—complete content becomes available immediately after checkout.

Make Insightful Decisions Backed by Expert Research

Unlock LS’s strategic roadmap with our full SWOT analysis — three-plus pages of research-backed strengths, risks, and growth levers tailored for investors and strategists. Purchase the complete report for editable Word and Excel files, expert commentary, and actionable recommendations to inform pitches, planning, and portfolio decisions.

Strengths

Diversified industrial portfolio

LS spans power cables, electrical equipment, industrial machinery and electronic components, reducing reliance on any single revenue stream. This spread helps balance cyclical swings across end-markets, smoothing demand volatility. Cross-selling and shared engineering deliver cost leverage through common platforms and pooled R&D. The portfolio mix strengthens resilience during sector-specific downturns.

Deep power and grid expertise

Core competence in transmission, distribution and power materials positions LS to capture accelerating grid expansion; proven engineering capabilities and international certifications enable bids on complex high-voltage projects. A documented track record lifts win rates and pricing power, supporting entry into premium niches such as HV and specialty cables.

Vertical integration in materials

Vertical integration from conductive materials to finished systems lets LS control quality and cost across the chain, reducing external procurement and inspection needs. Owning copper, aluminum and specialty polymer inputs mitigates supply risk and price pass-through volatility. Close ties between materials and product teams shorten innovation cycles and enable margin expansion through value capture at multiple stages.

Innovation and R&D focus

Investment in advanced cables, components and factory automation drives clear performance differentiation, with proprietary processes and design know-how creating high technical barriers to entry and protecting margin. R&D alignment with electrification and sustainability trends enhances customer relevance and supports long-term product roadmaps, enabling iterative platform upgrades and modular solutions.

- Performance differentiation via advanced materials and automation

- Barriers to entry from proprietary processes

- Sustainability-aligned R&D boosts customer relevance

- R&D underpins long-term roadmaps

Strong home base with global reach

South Korea's advanced domestic market—GDP about $1.8 trillion (IMF 2024) and R&D intensity 4.63% of GDP (OECD 2023)—provides high-tech reference projects; international subsidiaries and export channels scale operations and learning, supported by Korea's $655 billion in goods exports in 2023 (KCS). Regional diversification across Asia‑Pacific opens growth corridors and improves procurement and customer proximity.

- R&D: 4.63% of GDP (OECD 2023)

- Exports: $655B (KCS 2023)

- GDP: ~$1.8T (IMF 2024)

Electrification specialist: vertical integration and proprietary manufacturing fuel margin gains

LS combines diversified product lines, vertical integration and proprietary manufacturing to lower costs, shorten development cycles and protect margins. Strong engineering and HV credentials support premium project wins and cross-selling. R&D focus aligns with electrification and sustainability, leveraging South Korea's high-tech ecosystem and export channels to scale internationally.

| Metric | Value | Source/Year |

|---|---|---|

| KR GDP | ~$1.8T | IMF 2024 |

| R&D Intensity | 4.63% GDP | OECD 2023 |

| Goods Exports | $655B | KCS 2023 |

What is included in the product

Delivers a strategic overview of LS’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and guide strategic decision-making.

LS SWOT Analysis delivers a focused, editable template that converts complex strategic gaps into clear action items, enabling faster cross-team alignment and quicker decision-making.

Weaknesses

Capex-heavy, long-cycle business

Project-driven revenues create timing risk and lumpy cash flows as large contracts need bonding, upfront working capital and complex execution across multi-year schedules. Returns can be delayed by permitting or client financing, pushing paybacks beyond original forecasts and magnifying exposure to a weak cycle; IMF data show world GDP grew 3.0% in 2024, underscoring macro sensitivity. Such dynamics raise downside risk in slowdowns.

Exposure to commodity volatility

Inputs like copper (LME avg ~$9,500/t in 2024) and aluminum (~$2,300/t) drive LS cost base and contract pricing. Hedging reduces but does not eliminate margin risk, leaving residual exposure to market moves. Rapid swings can compress mid-project profitability. Customers may delay or cancel orders during price spikes, as seen in 2022–24 episodes.

Conglomerate complexity

Multiple subsidiaries can dilute LSs strategic focus and agility, contributing to the well-documented conglomerate discount of roughly 15% in firm valuations versus focused peers. Intercompany dependencies obscure performance transparency, complicating segment-level margins and cash flows. Governance and capital-allocation trade-offs often lead to suboptimal investment choices, while integration and restructuring costs can shave several percentage points off near-term ROIC.

High fixed costs and utilization risk

High fixed costs mean manufacturing footprints need steady volume to absorb overheads; US manufacturing capacity utilization averaged about 76% in 2024 (Federal Reserve), so downturns quickly erode margins. Underutilization in troughs forces margin compression, and scaling down capacity is costly and slow given multi-year plant exit timelines. Pricing discipline can be tested as firms cut prices to keep lines running and preserve fixed-cost absorption.

- Fixed-cost intensity: large share of COGS tied to overhead

- Utilization risk: ~76% US manufacturing utilization in 2024

- Exit cost: plant closures take years and incur write-downs

- Price pressure: risk of margin dilution to maintain throughput

Foreign exchange and geopolitical exposure

Export sales and overseas operations expose LS to significant FX volatility; global foreign exchange turnover was $7.5 trillion per day (BIS, 2019), amplifying translation and transaction risk. Regional tensions and 2023 Red Sea disruptions forced rerouting and lifted logistics and insurance costs. Multijurisdictional compliance increases administrative burdens and can raise financing spreads.

- FX exposure — global FX turnover $7.5T/day (BIS 2019)

- Logistics disruption — 2023 Red Sea rerouting increased freight/insurance

- Cost pressure — higher compliance, insurance and financing spreads

Project revenues lumpy; GDP 3.0%, copper $9,500/t

Project-driven revenues create lumpy cash flow and permit/finance delays; world GDP grew 3.0% in 2024, heightening cycle sensitivity. Input cost exposure (copper ~9,500/t; aluminum ~2,300/t in 2024) and hedging gaps can compress mid-project margins. High fixed costs (US utilization ~76% in 2024) and conglomerate discount (~15%) reduce agility. FX/logistics risk persists (FX turnover $7.5T/day).

| Metric | 2024 |

|---|---|

| World GDP growth (IMF) | 3.0% |

| Copper (LME avg) | $9,500/t |

| Aluminum | $2,300/t |

| US manuf. utilization (Fed) | 76% |

| Conglomerate discount | ~15% |

| FX turnover (BIS) | $7.5T/day |

What You See Is What You Get

LS SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the complete report you'll get; purchase unlocks the full, editable version. You’re viewing a live preview of the real file—complete content becomes available immediately after checkout.

Description

Make Insightful Decisions Backed by Expert Research

Unlock LS’s strategic roadmap with our full SWOT analysis — three-plus pages of research-backed strengths, risks, and growth levers tailored for investors and strategists. Purchase the complete report for editable Word and Excel files, expert commentary, and actionable recommendations to inform pitches, planning, and portfolio decisions.

Strengths

Diversified industrial portfolio

LS spans power cables, electrical equipment, industrial machinery and electronic components, reducing reliance on any single revenue stream. This spread helps balance cyclical swings across end-markets, smoothing demand volatility. Cross-selling and shared engineering deliver cost leverage through common platforms and pooled R&D. The portfolio mix strengthens resilience during sector-specific downturns.

Deep power and grid expertise

Core competence in transmission, distribution and power materials positions LS to capture accelerating grid expansion; proven engineering capabilities and international certifications enable bids on complex high-voltage projects. A documented track record lifts win rates and pricing power, supporting entry into premium niches such as HV and specialty cables.

Vertical integration in materials

Vertical integration from conductive materials to finished systems lets LS control quality and cost across the chain, reducing external procurement and inspection needs. Owning copper, aluminum and specialty polymer inputs mitigates supply risk and price pass-through volatility. Close ties between materials and product teams shorten innovation cycles and enable margin expansion through value capture at multiple stages.

Innovation and R&D focus

Investment in advanced cables, components and factory automation drives clear performance differentiation, with proprietary processes and design know-how creating high technical barriers to entry and protecting margin. R&D alignment with electrification and sustainability trends enhances customer relevance and supports long-term product roadmaps, enabling iterative platform upgrades and modular solutions.

- Performance differentiation via advanced materials and automation

- Barriers to entry from proprietary processes

- Sustainability-aligned R&D boosts customer relevance

- R&D underpins long-term roadmaps

Strong home base with global reach

South Korea's advanced domestic market—GDP about $1.8 trillion (IMF 2024) and R&D intensity 4.63% of GDP (OECD 2023)—provides high-tech reference projects; international subsidiaries and export channels scale operations and learning, supported by Korea's $655 billion in goods exports in 2023 (KCS). Regional diversification across Asia‑Pacific opens growth corridors and improves procurement and customer proximity.

- R&D: 4.63% of GDP (OECD 2023)

- Exports: $655B (KCS 2023)

- GDP: ~$1.8T (IMF 2024)

Electrification specialist: vertical integration and proprietary manufacturing fuel margin gains

LS combines diversified product lines, vertical integration and proprietary manufacturing to lower costs, shorten development cycles and protect margins. Strong engineering and HV credentials support premium project wins and cross-selling. R&D focus aligns with electrification and sustainability, leveraging South Korea's high-tech ecosystem and export channels to scale internationally.

| Metric | Value | Source/Year |

|---|---|---|

| KR GDP | ~$1.8T | IMF 2024 |

| R&D Intensity | 4.63% GDP | OECD 2023 |

| Goods Exports | $655B | KCS 2023 |

What is included in the product

Delivers a strategic overview of LS’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and guide strategic decision-making.

LS SWOT Analysis delivers a focused, editable template that converts complex strategic gaps into clear action items, enabling faster cross-team alignment and quicker decision-making.

Weaknesses

Capex-heavy, long-cycle business

Project-driven revenues create timing risk and lumpy cash flows as large contracts need bonding, upfront working capital and complex execution across multi-year schedules. Returns can be delayed by permitting or client financing, pushing paybacks beyond original forecasts and magnifying exposure to a weak cycle; IMF data show world GDP grew 3.0% in 2024, underscoring macro sensitivity. Such dynamics raise downside risk in slowdowns.

Exposure to commodity volatility

Inputs like copper (LME avg ~$9,500/t in 2024) and aluminum (~$2,300/t) drive LS cost base and contract pricing. Hedging reduces but does not eliminate margin risk, leaving residual exposure to market moves. Rapid swings can compress mid-project profitability. Customers may delay or cancel orders during price spikes, as seen in 2022–24 episodes.

Conglomerate complexity

Multiple subsidiaries can dilute LSs strategic focus and agility, contributing to the well-documented conglomerate discount of roughly 15% in firm valuations versus focused peers. Intercompany dependencies obscure performance transparency, complicating segment-level margins and cash flows. Governance and capital-allocation trade-offs often lead to suboptimal investment choices, while integration and restructuring costs can shave several percentage points off near-term ROIC.

High fixed costs and utilization risk

High fixed costs mean manufacturing footprints need steady volume to absorb overheads; US manufacturing capacity utilization averaged about 76% in 2024 (Federal Reserve), so downturns quickly erode margins. Underutilization in troughs forces margin compression, and scaling down capacity is costly and slow given multi-year plant exit timelines. Pricing discipline can be tested as firms cut prices to keep lines running and preserve fixed-cost absorption.

- Fixed-cost intensity: large share of COGS tied to overhead

- Utilization risk: ~76% US manufacturing utilization in 2024

- Exit cost: plant closures take years and incur write-downs

- Price pressure: risk of margin dilution to maintain throughput

Foreign exchange and geopolitical exposure

Export sales and overseas operations expose LS to significant FX volatility; global foreign exchange turnover was $7.5 trillion per day (BIS, 2019), amplifying translation and transaction risk. Regional tensions and 2023 Red Sea disruptions forced rerouting and lifted logistics and insurance costs. Multijurisdictional compliance increases administrative burdens and can raise financing spreads.

- FX exposure — global FX turnover $7.5T/day (BIS 2019)

- Logistics disruption — 2023 Red Sea rerouting increased freight/insurance

- Cost pressure — higher compliance, insurance and financing spreads

Project revenues lumpy; GDP 3.0%, copper $9,500/t

Project-driven revenues create lumpy cash flow and permit/finance delays; world GDP grew 3.0% in 2024, heightening cycle sensitivity. Input cost exposure (copper ~9,500/t; aluminum ~2,300/t in 2024) and hedging gaps can compress mid-project margins. High fixed costs (US utilization ~76% in 2024) and conglomerate discount (~15%) reduce agility. FX/logistics risk persists (FX turnover $7.5T/day).

| Metric | 2024 |

|---|---|

| World GDP growth (IMF) | 3.0% |

| Copper (LME avg) | $9,500/t |

| Aluminum | $2,300/t |

| US manuf. utilization (Fed) | 76% |

| Conglomerate discount | ~15% |

| FX turnover (BIS) | $7.5T/day |

What You See Is What You Get

LS SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the complete report you'll get; purchase unlocks the full, editable version. You’re viewing a live preview of the real file—complete content becomes available immediately after checkout.