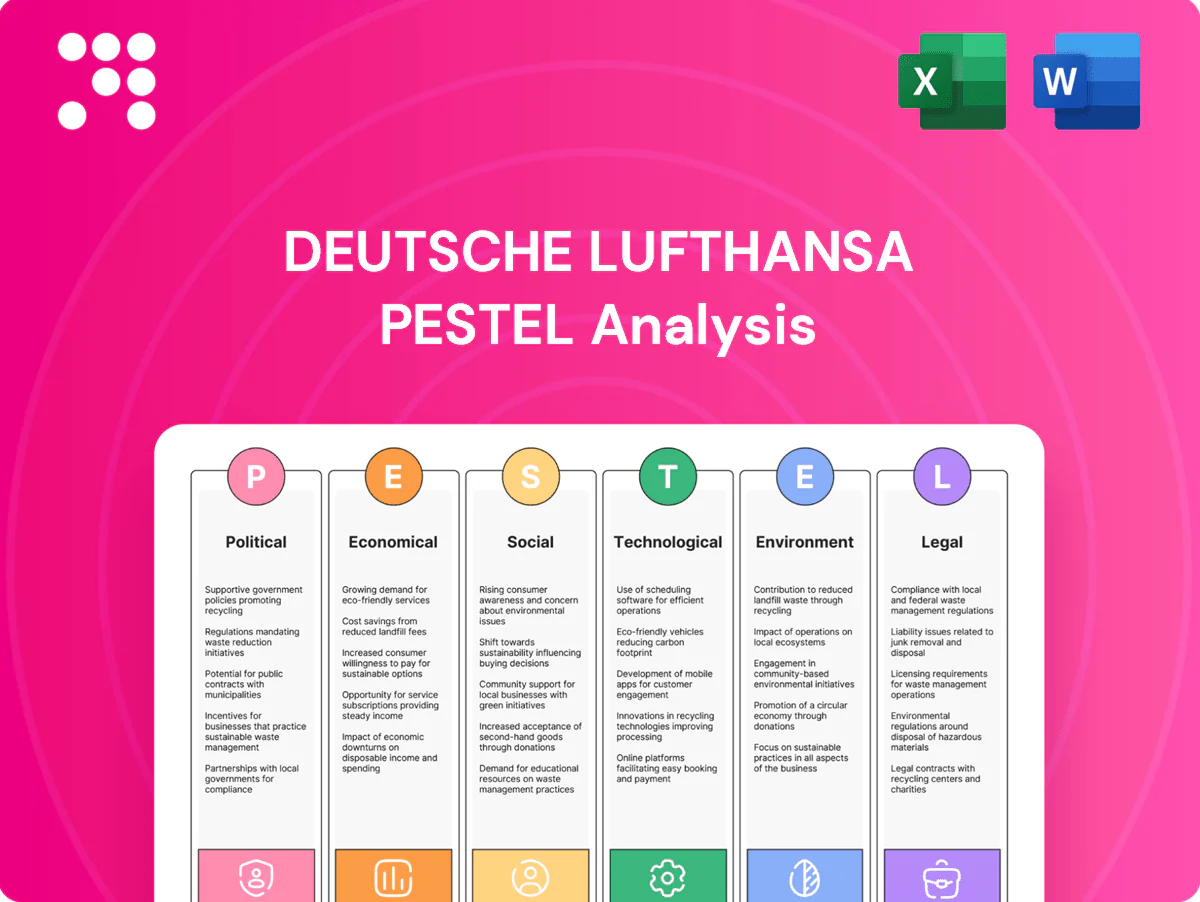

Deutsche Lufthansa PESTLE Analysis

Your Competitive Advantage Starts with This Report

Discover how geopolitical shifts, fuel price volatility, and evolving aviation regulations are reshaping Deutsche Lufthansa’s strategic landscape in our concise PESTLE snapshot—ideal for investors and strategists. This expert analysis highlights risks and opportunities across political, economic, social, technological, legal, and environmental fronts. Purchase the full PESTLE to get detailed, actionable insights and ready-to-use slides for decision-making.

Political factors

EU aviation policy and state aid

Brussels sets competition rules, traffic rights and sustainability mandates—Fit for 55 targets at least 55% GHG cuts by 2030 versus 1990—shaping Lufthansa’s network and costs. EU approval of up to €9bn German aid in 2020 increased post-crisis state aid scrutiny, limiting restructuring and M&A flexibility. Single European Sky reforms promise ~10–15% efficiency gains but can shift cost bases, so ongoing EU engagement is required to secure favorable terms and green funding.

Geopolitical tensions and airspace

Since the Feb 2022 Russia-Ukraine conflict closed significant airspace corridors, Deutsche Lufthansa has faced longer routings and higher fuel burn on affected Europe-Asia sectors, with persistent overflight bans forcing costly reroutes that compress schedules and reduce yields. Diplomatic volatility also disrupts cargo flows and reduces MRO demand from sanctioned regions. Lufthansa uses scenario planning and flexible crew/capacity rosters to mitigate sudden repositioning and capacity shocks.

Bilateral and Open Skies agreements

Access to long-haul markets for Deutsche Lufthansa hinges on bilateral rights and fifth‑freedom allowances, affecting route rights and revenue potential; the Group operates over 700 aircraft across its network. Changes in EU‑US, EU‑Asia and intra‑Europe regimes reshape alliances and competitive dynamics. Slot coordination at congested hubs like Frankfurt (cap ~88 movements/hour) ties political decisions directly to market share. Proactive lobbying helps safeguard strategic gateways for the Group.

Infrastructure and ATC governance

Government-controlled airports and national ANSPs shape Lufthansa punctuality and capacity; over 50% of European major airports remain publicly owned, influencing runway and terminal investment cycles. Investment choices and SESAR deployment timelines materially affect on‑time performance and capacity utilisation; EU ATM modernisation programs are projected to be central to capacity gains through 2025. ATC or public-sector strikes (e.g., major European disruptions in 2022–24) cause systemic delays and direct cost penalties for carriers and supply chains; regulatory partnerships accelerate resilience and modernisation for Lufthansa.

- Public ownership: >50% European major airports publicly owned

- SESAR/ATM: central to capacity improvements through 2025

- Strikes: recurring 2022–24 disruptions drove significant delays/costs

- Regulatory partnerships: speed up modernisation and operational resilience

Labor relations and public policy

Political climates shape collective bargaining and strike laws that directly affect Deutsche Lufthansa’s labor costs and operations; stable social pacts across the group lower disruption risk for its roughly 110,000-strong workforce. National priorities on wages, training and mobility influence crew availability and unit costs, while public scrutiny of fares and state aid has prompted EU probes and regulatory reviews in recent years.

- Collective bargaining: national laws + strike rules

- Crew availability: wages, training, mobility

- Public scrutiny: fares, subsidies → investigations

- Stable pacts reduce disruption risk

EU Fit for 55%, SESAR 10–15% reshape aviation costs

EU Fit for 55 (55% GHG cut by 2030) and approved €9bn German aid (2020) constrain costs and restructuring; SESAR/Single European Sky target ~10–15% efficiency gains affecting cost base. Russia‑Ukraine airspace closures since 2022 raised network costs and rerouting needs; Frankfurt cap ~88 movements/hour and >50% major European airports public shape slots and investment. Workforce ~110,000—collective bargaining and strike laws drive labour risk.

| Factor | Key data |

|---|---|

| Fit for 55 | 55% GHG cut by 2030 (vs 1990) |

| State aid | €9bn approved (DE, 2020) |

| SESAR/SES gains | ~10–15% efficiency |

| Frankfurt capacity | ~88 movements/hour |

| Airports ownership | >50% public |

| Workforce | ~110,000 employees |

What is included in the product

Explores how macro-environmental factors uniquely affect Deutsche Lufthansa across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities; designed for executives, advisors and investors and delivered in clean, report-ready format reflecting current market and regulatory dynamics.

A clean, summarized Deutsche Lufthansa PESTLE analysis, visually segmented by categories, provides an easily shareable, slide-ready summary that relieves meeting prep pain and supports rapid alignment on external risks and market positioning.

Economic factors

Fuel and energy price volatility

Fuel and energy price volatility hits Lufthansa margins — jet fuel and SAF spreads especially on long-haul — so the group relies on hedging, fleet efficiency and surcharges; fuel and oil costs were about EUR 6.9bn in 2023, underscoring scale. European energy costs also raise MRO and catering expenses, and disciplined fuel risk management underpins earnings stability.

Demand cycles and macro growth

Passenger and cargo volumes closely track GDP, trade and consumer confidence — IMF projected global GDP growth at 3.0% for 2024, supporting near‑prepandemic travel demand. Business travel recovery versus leisure mix continues to shape yields and cabin configurations, with premium demand sensitive to downturns while cargo partially offsets revenue swings. Flexible capacity and dynamic pricing protect load factors and RASK as markets fluctuate.

Inflation, wages, and interest rates

High inflation has pushed crew, airport and supplier expenses, squeezing unit costs and prompting Lufthansa to defend margins through productivity drives and higher ancillary revenue. ECB interest rates around 4% raise the cost of financing fleet renewals and press on liquidity buffers, while Lufthansa’s annual fleet capex guidance near €4bn requires stable funding. Wage settlements remain pivotal for cost trajectories and industrial peace.

FX movements and global revenues

Deutsche Lufthansa’s multi-currency sales and costs expose earnings to EUR, USD, GBP and CHF swings; the Group reported €32.8bn revenue in 2023, highlighting scale of FX exposure. USD-denominated fuel and aircraft payments amplify currency risk, natural hedges across routes and supplier mixes are helpful but imperfect, and active treasury hedging smooths cash flows and leverage metrics.

- FX exposure: EUR/USD/GBP/CHF

- 2023 revenue: €32.8bn

- Fuel/aircraft payments: predominantly USD

- Treasury hedging: mitigates but does not eliminate risk

Supply chain and capacity constraints

Supply chain and capacity constraints have curtailed available seat kilometers for Deutsche Lufthansa as aircraft delivery delays and engine shop bottlenecks limit fleet utilization, while parts shortages extend MRO and ground-op turnaround times, increasing cancellations and delays.

Capacity tightness can support fares but strains reliability; vendor diversification and higher inventory buffers are being used to reduce disruption and protect schedules.

- Aircraft delivery delays limit ASKs

- Engine shop bottlenecks lengthen shop visits

- Parts shortages slow MRO and ground ops

- Capacity tightness boosts fares but hurts reliability

- Vendor diversification and inventory buffers mitigate risk

EU Fit for 55%, SESAR 10–15% reshape aviation costs

Fuel volatility (jet fuel/SAF €6.9bn in 2023) and FX (2023 revenue €32.8bn) compress margins; capacity constraints and delivery delays limit ASKs while demand follows IMF 2024 GDP ~3.0%. Inflation and ECB rates ~4% raise unit costs and fleet financing needs (annual capex ~€4bn); active hedging and productivity lifts mitigate risks.

| Metric | Value |

|---|---|

| 2023 revenue | €32.8bn |

| Fuel/energy 2023 | €6.9bn |

| Annual fleet capex | ~€4bn |

| IMF global GDP 2024 | 3.0% |

| ECB rate (approx.) | 4% |

What You See Is What You Get

Deutsche Lufthansa PESTLE Analysis

The Deutsche Lufthansa PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal, and environmental factors affecting the airline; it highlights regulatory risks, macroeconomic exposures, technological trends, labor and sustainability issues. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it immediately for strategy, risk assessment, or investor briefings.

Your Competitive Advantage Starts with This Report

Discover how geopolitical shifts, fuel price volatility, and evolving aviation regulations are reshaping Deutsche Lufthansa’s strategic landscape in our concise PESTLE snapshot—ideal for investors and strategists. This expert analysis highlights risks and opportunities across political, economic, social, technological, legal, and environmental fronts. Purchase the full PESTLE to get detailed, actionable insights and ready-to-use slides for decision-making.

Political factors

EU aviation policy and state aid

Brussels sets competition rules, traffic rights and sustainability mandates—Fit for 55 targets at least 55% GHG cuts by 2030 versus 1990—shaping Lufthansa’s network and costs. EU approval of up to €9bn German aid in 2020 increased post-crisis state aid scrutiny, limiting restructuring and M&A flexibility. Single European Sky reforms promise ~10–15% efficiency gains but can shift cost bases, so ongoing EU engagement is required to secure favorable terms and green funding.

Geopolitical tensions and airspace

Since the Feb 2022 Russia-Ukraine conflict closed significant airspace corridors, Deutsche Lufthansa has faced longer routings and higher fuel burn on affected Europe-Asia sectors, with persistent overflight bans forcing costly reroutes that compress schedules and reduce yields. Diplomatic volatility also disrupts cargo flows and reduces MRO demand from sanctioned regions. Lufthansa uses scenario planning and flexible crew/capacity rosters to mitigate sudden repositioning and capacity shocks.

Bilateral and Open Skies agreements

Access to long-haul markets for Deutsche Lufthansa hinges on bilateral rights and fifth‑freedom allowances, affecting route rights and revenue potential; the Group operates over 700 aircraft across its network. Changes in EU‑US, EU‑Asia and intra‑Europe regimes reshape alliances and competitive dynamics. Slot coordination at congested hubs like Frankfurt (cap ~88 movements/hour) ties political decisions directly to market share. Proactive lobbying helps safeguard strategic gateways for the Group.

Infrastructure and ATC governance

Government-controlled airports and national ANSPs shape Lufthansa punctuality and capacity; over 50% of European major airports remain publicly owned, influencing runway and terminal investment cycles. Investment choices and SESAR deployment timelines materially affect on‑time performance and capacity utilisation; EU ATM modernisation programs are projected to be central to capacity gains through 2025. ATC or public-sector strikes (e.g., major European disruptions in 2022–24) cause systemic delays and direct cost penalties for carriers and supply chains; regulatory partnerships accelerate resilience and modernisation for Lufthansa.

- Public ownership: >50% European major airports publicly owned

- SESAR/ATM: central to capacity improvements through 2025

- Strikes: recurring 2022–24 disruptions drove significant delays/costs

- Regulatory partnerships: speed up modernisation and operational resilience

Labor relations and public policy

Political climates shape collective bargaining and strike laws that directly affect Deutsche Lufthansa’s labor costs and operations; stable social pacts across the group lower disruption risk for its roughly 110,000-strong workforce. National priorities on wages, training and mobility influence crew availability and unit costs, while public scrutiny of fares and state aid has prompted EU probes and regulatory reviews in recent years.

- Collective bargaining: national laws + strike rules

- Crew availability: wages, training, mobility

- Public scrutiny: fares, subsidies → investigations

- Stable pacts reduce disruption risk

EU Fit for 55%, SESAR 10–15% reshape aviation costs

EU Fit for 55 (55% GHG cut by 2030) and approved €9bn German aid (2020) constrain costs and restructuring; SESAR/Single European Sky target ~10–15% efficiency gains affecting cost base. Russia‑Ukraine airspace closures since 2022 raised network costs and rerouting needs; Frankfurt cap ~88 movements/hour and >50% major European airports public shape slots and investment. Workforce ~110,000—collective bargaining and strike laws drive labour risk.

| Factor | Key data |

|---|---|

| Fit for 55 | 55% GHG cut by 2030 (vs 1990) |

| State aid | €9bn approved (DE, 2020) |

| SESAR/SES gains | ~10–15% efficiency |

| Frankfurt capacity | ~88 movements/hour |

| Airports ownership | >50% public |

| Workforce | ~110,000 employees |

What is included in the product

Explores how macro-environmental factors uniquely affect Deutsche Lufthansa across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities; designed for executives, advisors and investors and delivered in clean, report-ready format reflecting current market and regulatory dynamics.

A clean, summarized Deutsche Lufthansa PESTLE analysis, visually segmented by categories, provides an easily shareable, slide-ready summary that relieves meeting prep pain and supports rapid alignment on external risks and market positioning.

Economic factors

Fuel and energy price volatility

Fuel and energy price volatility hits Lufthansa margins — jet fuel and SAF spreads especially on long-haul — so the group relies on hedging, fleet efficiency and surcharges; fuel and oil costs were about EUR 6.9bn in 2023, underscoring scale. European energy costs also raise MRO and catering expenses, and disciplined fuel risk management underpins earnings stability.

Demand cycles and macro growth

Passenger and cargo volumes closely track GDP, trade and consumer confidence — IMF projected global GDP growth at 3.0% for 2024, supporting near‑prepandemic travel demand. Business travel recovery versus leisure mix continues to shape yields and cabin configurations, with premium demand sensitive to downturns while cargo partially offsets revenue swings. Flexible capacity and dynamic pricing protect load factors and RASK as markets fluctuate.

Inflation, wages, and interest rates

High inflation has pushed crew, airport and supplier expenses, squeezing unit costs and prompting Lufthansa to defend margins through productivity drives and higher ancillary revenue. ECB interest rates around 4% raise the cost of financing fleet renewals and press on liquidity buffers, while Lufthansa’s annual fleet capex guidance near €4bn requires stable funding. Wage settlements remain pivotal for cost trajectories and industrial peace.

FX movements and global revenues

Deutsche Lufthansa’s multi-currency sales and costs expose earnings to EUR, USD, GBP and CHF swings; the Group reported €32.8bn revenue in 2023, highlighting scale of FX exposure. USD-denominated fuel and aircraft payments amplify currency risk, natural hedges across routes and supplier mixes are helpful but imperfect, and active treasury hedging smooths cash flows and leverage metrics.

- FX exposure: EUR/USD/GBP/CHF

- 2023 revenue: €32.8bn

- Fuel/aircraft payments: predominantly USD

- Treasury hedging: mitigates but does not eliminate risk

Supply chain and capacity constraints

Supply chain and capacity constraints have curtailed available seat kilometers for Deutsche Lufthansa as aircraft delivery delays and engine shop bottlenecks limit fleet utilization, while parts shortages extend MRO and ground-op turnaround times, increasing cancellations and delays.

Capacity tightness can support fares but strains reliability; vendor diversification and higher inventory buffers are being used to reduce disruption and protect schedules.

- Aircraft delivery delays limit ASKs

- Engine shop bottlenecks lengthen shop visits

- Parts shortages slow MRO and ground ops

- Capacity tightness boosts fares but hurts reliability

- Vendor diversification and inventory buffers mitigate risk

EU Fit for 55%, SESAR 10–15% reshape aviation costs

Fuel volatility (jet fuel/SAF €6.9bn in 2023) and FX (2023 revenue €32.8bn) compress margins; capacity constraints and delivery delays limit ASKs while demand follows IMF 2024 GDP ~3.0%. Inflation and ECB rates ~4% raise unit costs and fleet financing needs (annual capex ~€4bn); active hedging and productivity lifts mitigate risks.

| Metric | Value |

|---|---|

| 2023 revenue | €32.8bn |

| Fuel/energy 2023 | €6.9bn |

| Annual fleet capex | ~€4bn |

| IMF global GDP 2024 | 3.0% |

| ECB rate (approx.) | 4% |

What You See Is What You Get

Deutsche Lufthansa PESTLE Analysis

The Deutsche Lufthansa PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal, and environmental factors affecting the airline; it highlights regulatory risks, macroeconomic exposures, technological trends, labor and sustainability issues. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it immediately for strategy, risk assessment, or investor briefings.

Description

Your Competitive Advantage Starts with This Report

Discover how geopolitical shifts, fuel price volatility, and evolving aviation regulations are reshaping Deutsche Lufthansa’s strategic landscape in our concise PESTLE snapshot—ideal for investors and strategists. This expert analysis highlights risks and opportunities across political, economic, social, technological, legal, and environmental fronts. Purchase the full PESTLE to get detailed, actionable insights and ready-to-use slides for decision-making.

Political factors

EU aviation policy and state aid

Brussels sets competition rules, traffic rights and sustainability mandates—Fit for 55 targets at least 55% GHG cuts by 2030 versus 1990—shaping Lufthansa’s network and costs. EU approval of up to €9bn German aid in 2020 increased post-crisis state aid scrutiny, limiting restructuring and M&A flexibility. Single European Sky reforms promise ~10–15% efficiency gains but can shift cost bases, so ongoing EU engagement is required to secure favorable terms and green funding.

Geopolitical tensions and airspace

Since the Feb 2022 Russia-Ukraine conflict closed significant airspace corridors, Deutsche Lufthansa has faced longer routings and higher fuel burn on affected Europe-Asia sectors, with persistent overflight bans forcing costly reroutes that compress schedules and reduce yields. Diplomatic volatility also disrupts cargo flows and reduces MRO demand from sanctioned regions. Lufthansa uses scenario planning and flexible crew/capacity rosters to mitigate sudden repositioning and capacity shocks.

Bilateral and Open Skies agreements

Access to long-haul markets for Deutsche Lufthansa hinges on bilateral rights and fifth‑freedom allowances, affecting route rights and revenue potential; the Group operates over 700 aircraft across its network. Changes in EU‑US, EU‑Asia and intra‑Europe regimes reshape alliances and competitive dynamics. Slot coordination at congested hubs like Frankfurt (cap ~88 movements/hour) ties political decisions directly to market share. Proactive lobbying helps safeguard strategic gateways for the Group.

Infrastructure and ATC governance

Government-controlled airports and national ANSPs shape Lufthansa punctuality and capacity; over 50% of European major airports remain publicly owned, influencing runway and terminal investment cycles. Investment choices and SESAR deployment timelines materially affect on‑time performance and capacity utilisation; EU ATM modernisation programs are projected to be central to capacity gains through 2025. ATC or public-sector strikes (e.g., major European disruptions in 2022–24) cause systemic delays and direct cost penalties for carriers and supply chains; regulatory partnerships accelerate resilience and modernisation for Lufthansa.

- Public ownership: >50% European major airports publicly owned

- SESAR/ATM: central to capacity improvements through 2025

- Strikes: recurring 2022–24 disruptions drove significant delays/costs

- Regulatory partnerships: speed up modernisation and operational resilience

Labor relations and public policy

Political climates shape collective bargaining and strike laws that directly affect Deutsche Lufthansa’s labor costs and operations; stable social pacts across the group lower disruption risk for its roughly 110,000-strong workforce. National priorities on wages, training and mobility influence crew availability and unit costs, while public scrutiny of fares and state aid has prompted EU probes and regulatory reviews in recent years.

- Collective bargaining: national laws + strike rules

- Crew availability: wages, training, mobility

- Public scrutiny: fares, subsidies → investigations

- Stable pacts reduce disruption risk

EU Fit for 55%, SESAR 10–15% reshape aviation costs

EU Fit for 55 (55% GHG cut by 2030) and approved €9bn German aid (2020) constrain costs and restructuring; SESAR/Single European Sky target ~10–15% efficiency gains affecting cost base. Russia‑Ukraine airspace closures since 2022 raised network costs and rerouting needs; Frankfurt cap ~88 movements/hour and >50% major European airports public shape slots and investment. Workforce ~110,000—collective bargaining and strike laws drive labour risk.

| Factor | Key data |

|---|---|

| Fit for 55 | 55% GHG cut by 2030 (vs 1990) |

| State aid | €9bn approved (DE, 2020) |

| SESAR/SES gains | ~10–15% efficiency |

| Frankfurt capacity | ~88 movements/hour |

| Airports ownership | >50% public |

| Workforce | ~110,000 employees |

What is included in the product

Explores how macro-environmental factors uniquely affect Deutsche Lufthansa across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven trends and forward-looking insights to identify threats and opportunities; designed for executives, advisors and investors and delivered in clean, report-ready format reflecting current market and regulatory dynamics.

A clean, summarized Deutsche Lufthansa PESTLE analysis, visually segmented by categories, provides an easily shareable, slide-ready summary that relieves meeting prep pain and supports rapid alignment on external risks and market positioning.

Economic factors

Fuel and energy price volatility

Fuel and energy price volatility hits Lufthansa margins — jet fuel and SAF spreads especially on long-haul — so the group relies on hedging, fleet efficiency and surcharges; fuel and oil costs were about EUR 6.9bn in 2023, underscoring scale. European energy costs also raise MRO and catering expenses, and disciplined fuel risk management underpins earnings stability.

Demand cycles and macro growth

Passenger and cargo volumes closely track GDP, trade and consumer confidence — IMF projected global GDP growth at 3.0% for 2024, supporting near‑prepandemic travel demand. Business travel recovery versus leisure mix continues to shape yields and cabin configurations, with premium demand sensitive to downturns while cargo partially offsets revenue swings. Flexible capacity and dynamic pricing protect load factors and RASK as markets fluctuate.

Inflation, wages, and interest rates

High inflation has pushed crew, airport and supplier expenses, squeezing unit costs and prompting Lufthansa to defend margins through productivity drives and higher ancillary revenue. ECB interest rates around 4% raise the cost of financing fleet renewals and press on liquidity buffers, while Lufthansa’s annual fleet capex guidance near €4bn requires stable funding. Wage settlements remain pivotal for cost trajectories and industrial peace.

FX movements and global revenues

Deutsche Lufthansa’s multi-currency sales and costs expose earnings to EUR, USD, GBP and CHF swings; the Group reported €32.8bn revenue in 2023, highlighting scale of FX exposure. USD-denominated fuel and aircraft payments amplify currency risk, natural hedges across routes and supplier mixes are helpful but imperfect, and active treasury hedging smooths cash flows and leverage metrics.

- FX exposure: EUR/USD/GBP/CHF

- 2023 revenue: €32.8bn

- Fuel/aircraft payments: predominantly USD

- Treasury hedging: mitigates but does not eliminate risk

Supply chain and capacity constraints

Supply chain and capacity constraints have curtailed available seat kilometers for Deutsche Lufthansa as aircraft delivery delays and engine shop bottlenecks limit fleet utilization, while parts shortages extend MRO and ground-op turnaround times, increasing cancellations and delays.

Capacity tightness can support fares but strains reliability; vendor diversification and higher inventory buffers are being used to reduce disruption and protect schedules.

- Aircraft delivery delays limit ASKs

- Engine shop bottlenecks lengthen shop visits

- Parts shortages slow MRO and ground ops

- Capacity tightness boosts fares but hurts reliability

- Vendor diversification and inventory buffers mitigate risk

EU Fit for 55%, SESAR 10–15% reshape aviation costs

Fuel volatility (jet fuel/SAF €6.9bn in 2023) and FX (2023 revenue €32.8bn) compress margins; capacity constraints and delivery delays limit ASKs while demand follows IMF 2024 GDP ~3.0%. Inflation and ECB rates ~4% raise unit costs and fleet financing needs (annual capex ~€4bn); active hedging and productivity lifts mitigate risks.

| Metric | Value |

|---|---|

| 2023 revenue | €32.8bn |

| Fuel/energy 2023 | €6.9bn |

| Annual fleet capex | ~€4bn |

| IMF global GDP 2024 | 3.0% |

| ECB rate (approx.) | 4% |

What You See Is What You Get

Deutsche Lufthansa PESTLE Analysis

The Deutsche Lufthansa PESTLE Analysis provides a concise evaluation of political, economic, social, technological, legal, and environmental factors affecting the airline; it highlights regulatory risks, macroeconomic exposures, technological trends, labor and sustainability issues. The preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. Use it immediately for strategy, risk assessment, or investor briefings.