Lumen Technologies PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE analysis of Lumen Technologies. We map political, economic, social, technological, legal and environmental forces shaping its telecom transformation. Use these insights to anticipate risks and spot growth levers. Purchase the full report for an actionable, downloadable breakdown.

Political factors

Telecom policy and regulation

Regulatory stances on net neutrality, open access, and wholesale obligations directly shape Lumen’s pricing power and service design; shifts in interconnection or traffic management rules can compress margins on parts of Lumen’s $12.9B 2024 revenue base and affect enterprise broadband serving ~100M US households. Lumen must adapt product roadmaps and compliance processes to evolving rules, and proactive advocacy reduces risk of abrupt regulatory shocks.

Government procurement dynamics

Federal, state and international public-sector contracts offer scale but demand stringent compliance such as FedRAMP, FISMA and DoD SRG certifications. U.S. federal IT spending is about 100 billion dollars annually, so budget cycles and shifting priorities materially affect win rates and renewal risk. Political shifts from programs like the 1.2 trillion IIJA can reallocate funds between infrastructure and other areas. Stable engagement and contract diversification reduce revenue volatility.

Geopolitical risk and supply chains

Export controls, sanctions and US-China trade tensions constrain Lumen’s equipment sourcing and force vendor swaps after 2023-24 controls, raising procurement costs and testing resilience. Cross-border data flow rules and localization mandates in 20+ countries complicate global service delivery and increase compliance spend. Lumen must use multi-vendor strategies and regional inventories to keep deployments on schedule; scenario planning buffers lead-time and cost spikes.

Infrastructure incentives and funding

Public investments under IIJA and BEAD (BEAD $42.45B, overall IIJA broadband ~65B) plus NTIA Middle Mile grants ($1B) can subsidize Lumen’s expansion and upgrades. Accessing these funds requires eligibility checks, matching funds and compliance reporting. Competitors also benefit, intensifying regional buildouts. Targeted participation can materially lower unit economics in underserved areas.

- BEAD $42.45B

- IIJA broadband ~65B

- NTIA Middle Mile $1B

Cybersecurity national directives

Government cybersecurity directives raise baseline protections for critical infrastructure, driving mandatory incident reporting (often 72-hour windows) and accelerating zero-trust adoption—Gartner projects over 60% enterprise adoption by 2025—raising operating complexity and compliance costs; noncompliance risks contract loss, fines and reputational damage, while early alignment boosts credibility with enterprise and public customers.

- Mandatory 72-hour reporting

- Gartner: >60% zero-trust by 2025

- Higher compliance costs, contract risk

- Early alignment = stronger credibility

Regulatory shifts, IIJA/BEAD funding and cyber mandates squeeze pricing for major network operators

Regulatory shifts (net neutrality, interconnection, export controls) directly affect pricing, margins and sourcing for Lumen (2024 revenue $12.9B; ~100M US households reachable). Federal contracts and IIJA/BEAD funding (BEAD $42.45B; IIJA broadband ~65B; NTIA Middle Mile $1B) create scale but add compliance; cybersecurity mandates (72-hour reporting; >60% zero-trust by 2025) raise costs and contract risk.

| Metric | Value |

|---|---|

| 2024 Revenue | $12.9B |

| US households | ~100M |

| BEAD | $42.45B |

| IIJA broadband | ~$65B |

| NTIA Middle Mile | $1B |

| Fed IT spend | $100B/yr |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Lumen Technologies, with data-backed trends and forward-looking insights to help executives, investors and strategists identify risks, opportunities and actions for competitive resilience.

A concise, visually segmented PESTLE summary for Lumen Technologies that eases meeting prep and decision-making by highlighting external risks and market positioning, and is easily shareable and editable for teams, clients, or presentations.

Economic factors

Enterprise IT spend cycles

Macro conditions drive demand for cloud connectivity, security and managed services as global IT spending reached about $4.7 trillion in 2024 (Gartner), lengthening procurement cycles under tight budgets and favoring vendor consolidation. Growth spurts accelerate migrations to higher-bandwidth links and SASE offerings, while Lumen’s portfolio skews toward resilient, mission-critical workloads across enterprise customers.

Capital intensity and interest rates

Fiber expansion, edge nodes and data‑center interconnects demand heavy capex — Lumen reported roughly $1.9B capex in FY2024 — while Fed funds near 5.25–5.50% (2024–25) lifts WACC and tightens build hurdle rates. Optimizing build‑to‑demand and joint builds raises ROI; debt structure and refinancing windows materially influence free cash flow and investment pacing.

Pricing pressure and competition

Wholesale transit, wavelength and VPN corridors show commoditization with price compression in key routes, pressuring margins; the global SD-WAN market reached about $4.7 billion in 2024, intensifying cross-category competition as hyperscalers and MSPs push bundled network-security plays. Differentiation for Lumen depends on low latency, extensive reach, firm SLAs and embedded security; bundled solutions that combine SASE, managed services and edge connectivity can protect ARPU and curb churn.

Inflation and cost structure

Equipment, energy, and labor inflation (US CPI 2024: 3.4%, BLS) lifted Lumen's opex and capex pressures; index-linked customer contracts help pass through costs but timing lags compress near-term margins. Automation, edge virtualization and software-defined networking reduce unit costs; strategic vendor negotiations and long-term PPAs stabilize energy and procurement spend.

- Index-linked contracts: pass-through but lag risk

- Automation/virtualization: lowers unit cost

- Vendor deals & PPAs: expense stability

Currency and international exposure

Multi-country operations expose Lumen to FX translation and transaction risks, with hedging programs used to smooth reported earnings while adding hedging costs that compress margins. Pricing services in local currencies and using natural hedges from regional revenue-cost alignment reduce net exposure. Regional portfolio mix drives where growth and margin pressure materialize.

- FX translation risk

- Hedging reduces volatility, adds cost

- Local-currency pricing, natural hedges

- Regional mix affects growth/margins

Regulatory shifts, IIJA/BEAD funding and cyber mandates squeeze pricing for major network operators

Macro IT spend (Gartner) at about 4.7 trillion in 2024 drives demand for cloud, security and managed services, favoring vendor consolidation and longer procurement cycles. Lumen reported roughly 1.9B capex in FY2024 while Fed funds near 5.25–5.50% (2024–25) tightens WACC and investment pacing. SD‑WAN market ~4.7B (2024) and US CPI 2024: 3.4% pressure margins; automation, index‑linked contracts and PPAs mitigate risks.

| Metric | Value (2024/25) |

|---|---|

| Global IT spend | 4.7T (Gartner 2024) |

| Lumen capex | ~1.9B FY2024 |

| Fed funds | 5.25–5.50% (2024–25) |

| SD‑WAN market | ~4.7B (2024) |

| US CPI | 3.4% (2024) |

Preview the Actual Deliverable

Lumen Technologies PESTLE Analysis

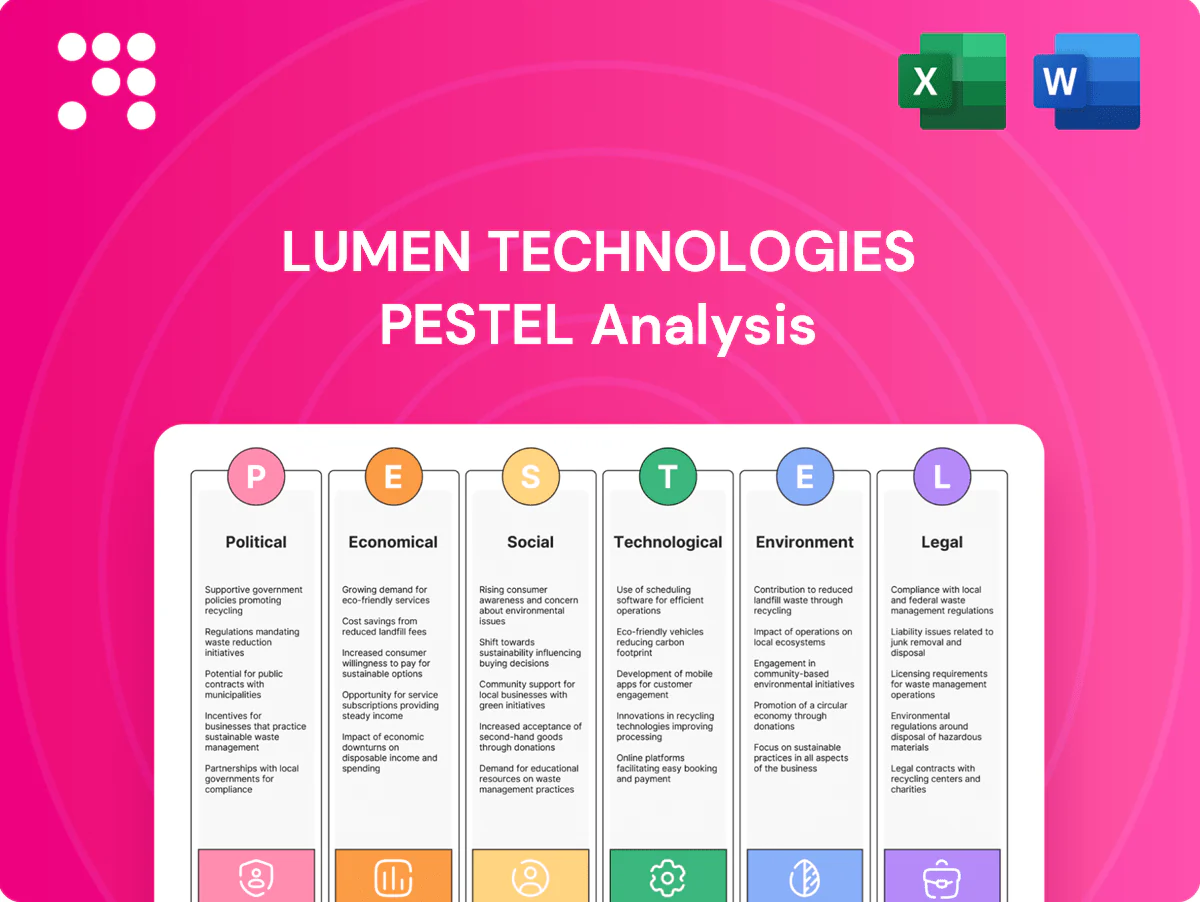

The preview shown here is the exact Lumen Technologies PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with professional structure and source citations. No placeholders or teasers; this is the final downloadable file available immediately after checkout.

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE analysis of Lumen Technologies. We map political, economic, social, technological, legal and environmental forces shaping its telecom transformation. Use these insights to anticipate risks and spot growth levers. Purchase the full report for an actionable, downloadable breakdown.

Political factors

Telecom policy and regulation

Regulatory stances on net neutrality, open access, and wholesale obligations directly shape Lumen’s pricing power and service design; shifts in interconnection or traffic management rules can compress margins on parts of Lumen’s $12.9B 2024 revenue base and affect enterprise broadband serving ~100M US households. Lumen must adapt product roadmaps and compliance processes to evolving rules, and proactive advocacy reduces risk of abrupt regulatory shocks.

Government procurement dynamics

Federal, state and international public-sector contracts offer scale but demand stringent compliance such as FedRAMP, FISMA and DoD SRG certifications. U.S. federal IT spending is about 100 billion dollars annually, so budget cycles and shifting priorities materially affect win rates and renewal risk. Political shifts from programs like the 1.2 trillion IIJA can reallocate funds between infrastructure and other areas. Stable engagement and contract diversification reduce revenue volatility.

Geopolitical risk and supply chains

Export controls, sanctions and US-China trade tensions constrain Lumen’s equipment sourcing and force vendor swaps after 2023-24 controls, raising procurement costs and testing resilience. Cross-border data flow rules and localization mandates in 20+ countries complicate global service delivery and increase compliance spend. Lumen must use multi-vendor strategies and regional inventories to keep deployments on schedule; scenario planning buffers lead-time and cost spikes.

Infrastructure incentives and funding

Public investments under IIJA and BEAD (BEAD $42.45B, overall IIJA broadband ~65B) plus NTIA Middle Mile grants ($1B) can subsidize Lumen’s expansion and upgrades. Accessing these funds requires eligibility checks, matching funds and compliance reporting. Competitors also benefit, intensifying regional buildouts. Targeted participation can materially lower unit economics in underserved areas.

- BEAD $42.45B

- IIJA broadband ~65B

- NTIA Middle Mile $1B

Cybersecurity national directives

Government cybersecurity directives raise baseline protections for critical infrastructure, driving mandatory incident reporting (often 72-hour windows) and accelerating zero-trust adoption—Gartner projects over 60% enterprise adoption by 2025—raising operating complexity and compliance costs; noncompliance risks contract loss, fines and reputational damage, while early alignment boosts credibility with enterprise and public customers.

- Mandatory 72-hour reporting

- Gartner: >60% zero-trust by 2025

- Higher compliance costs, contract risk

- Early alignment = stronger credibility

Regulatory shifts, IIJA/BEAD funding and cyber mandates squeeze pricing for major network operators

Regulatory shifts (net neutrality, interconnection, export controls) directly affect pricing, margins and sourcing for Lumen (2024 revenue $12.9B; ~100M US households reachable). Federal contracts and IIJA/BEAD funding (BEAD $42.45B; IIJA broadband ~65B; NTIA Middle Mile $1B) create scale but add compliance; cybersecurity mandates (72-hour reporting; >60% zero-trust by 2025) raise costs and contract risk.

| Metric | Value |

|---|---|

| 2024 Revenue | $12.9B |

| US households | ~100M |

| BEAD | $42.45B |

| IIJA broadband | ~$65B |

| NTIA Middle Mile | $1B |

| Fed IT spend | $100B/yr |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Lumen Technologies, with data-backed trends and forward-looking insights to help executives, investors and strategists identify risks, opportunities and actions for competitive resilience.

A concise, visually segmented PESTLE summary for Lumen Technologies that eases meeting prep and decision-making by highlighting external risks and market positioning, and is easily shareable and editable for teams, clients, or presentations.

Economic factors

Enterprise IT spend cycles

Macro conditions drive demand for cloud connectivity, security and managed services as global IT spending reached about $4.7 trillion in 2024 (Gartner), lengthening procurement cycles under tight budgets and favoring vendor consolidation. Growth spurts accelerate migrations to higher-bandwidth links and SASE offerings, while Lumen’s portfolio skews toward resilient, mission-critical workloads across enterprise customers.

Capital intensity and interest rates

Fiber expansion, edge nodes and data‑center interconnects demand heavy capex — Lumen reported roughly $1.9B capex in FY2024 — while Fed funds near 5.25–5.50% (2024–25) lifts WACC and tightens build hurdle rates. Optimizing build‑to‑demand and joint builds raises ROI; debt structure and refinancing windows materially influence free cash flow and investment pacing.

Pricing pressure and competition

Wholesale transit, wavelength and VPN corridors show commoditization with price compression in key routes, pressuring margins; the global SD-WAN market reached about $4.7 billion in 2024, intensifying cross-category competition as hyperscalers and MSPs push bundled network-security plays. Differentiation for Lumen depends on low latency, extensive reach, firm SLAs and embedded security; bundled solutions that combine SASE, managed services and edge connectivity can protect ARPU and curb churn.

Inflation and cost structure

Equipment, energy, and labor inflation (US CPI 2024: 3.4%, BLS) lifted Lumen's opex and capex pressures; index-linked customer contracts help pass through costs but timing lags compress near-term margins. Automation, edge virtualization and software-defined networking reduce unit costs; strategic vendor negotiations and long-term PPAs stabilize energy and procurement spend.

- Index-linked contracts: pass-through but lag risk

- Automation/virtualization: lowers unit cost

- Vendor deals & PPAs: expense stability

Currency and international exposure

Multi-country operations expose Lumen to FX translation and transaction risks, with hedging programs used to smooth reported earnings while adding hedging costs that compress margins. Pricing services in local currencies and using natural hedges from regional revenue-cost alignment reduce net exposure. Regional portfolio mix drives where growth and margin pressure materialize.

- FX translation risk

- Hedging reduces volatility, adds cost

- Local-currency pricing, natural hedges

- Regional mix affects growth/margins

Regulatory shifts, IIJA/BEAD funding and cyber mandates squeeze pricing for major network operators

Macro IT spend (Gartner) at about 4.7 trillion in 2024 drives demand for cloud, security and managed services, favoring vendor consolidation and longer procurement cycles. Lumen reported roughly 1.9B capex in FY2024 while Fed funds near 5.25–5.50% (2024–25) tightens WACC and investment pacing. SD‑WAN market ~4.7B (2024) and US CPI 2024: 3.4% pressure margins; automation, index‑linked contracts and PPAs mitigate risks.

| Metric | Value (2024/25) |

|---|---|

| Global IT spend | 4.7T (Gartner 2024) |

| Lumen capex | ~1.9B FY2024 |

| Fed funds | 5.25–5.50% (2024–25) |

| SD‑WAN market | ~4.7B (2024) |

| US CPI | 3.4% (2024) |

Preview the Actual Deliverable

Lumen Technologies PESTLE Analysis

The preview shown here is the exact Lumen Technologies PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with professional structure and source citations. No placeholders or teasers; this is the final downloadable file available immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Gain strategic clarity with our PESTLE analysis of Lumen Technologies. We map political, economic, social, technological, legal and environmental forces shaping its telecom transformation. Use these insights to anticipate risks and spot growth levers. Purchase the full report for an actionable, downloadable breakdown.

Political factors

Telecom policy and regulation

Regulatory stances on net neutrality, open access, and wholesale obligations directly shape Lumen’s pricing power and service design; shifts in interconnection or traffic management rules can compress margins on parts of Lumen’s $12.9B 2024 revenue base and affect enterprise broadband serving ~100M US households. Lumen must adapt product roadmaps and compliance processes to evolving rules, and proactive advocacy reduces risk of abrupt regulatory shocks.

Government procurement dynamics

Federal, state and international public-sector contracts offer scale but demand stringent compliance such as FedRAMP, FISMA and DoD SRG certifications. U.S. federal IT spending is about 100 billion dollars annually, so budget cycles and shifting priorities materially affect win rates and renewal risk. Political shifts from programs like the 1.2 trillion IIJA can reallocate funds between infrastructure and other areas. Stable engagement and contract diversification reduce revenue volatility.

Geopolitical risk and supply chains

Export controls, sanctions and US-China trade tensions constrain Lumen’s equipment sourcing and force vendor swaps after 2023-24 controls, raising procurement costs and testing resilience. Cross-border data flow rules and localization mandates in 20+ countries complicate global service delivery and increase compliance spend. Lumen must use multi-vendor strategies and regional inventories to keep deployments on schedule; scenario planning buffers lead-time and cost spikes.

Infrastructure incentives and funding

Public investments under IIJA and BEAD (BEAD $42.45B, overall IIJA broadband ~65B) plus NTIA Middle Mile grants ($1B) can subsidize Lumen’s expansion and upgrades. Accessing these funds requires eligibility checks, matching funds and compliance reporting. Competitors also benefit, intensifying regional buildouts. Targeted participation can materially lower unit economics in underserved areas.

- BEAD $42.45B

- IIJA broadband ~65B

- NTIA Middle Mile $1B

Cybersecurity national directives

Government cybersecurity directives raise baseline protections for critical infrastructure, driving mandatory incident reporting (often 72-hour windows) and accelerating zero-trust adoption—Gartner projects over 60% enterprise adoption by 2025—raising operating complexity and compliance costs; noncompliance risks contract loss, fines and reputational damage, while early alignment boosts credibility with enterprise and public customers.

- Mandatory 72-hour reporting

- Gartner: >60% zero-trust by 2025

- Higher compliance costs, contract risk

- Early alignment = stronger credibility

Regulatory shifts, IIJA/BEAD funding and cyber mandates squeeze pricing for major network operators

Regulatory shifts (net neutrality, interconnection, export controls) directly affect pricing, margins and sourcing for Lumen (2024 revenue $12.9B; ~100M US households reachable). Federal contracts and IIJA/BEAD funding (BEAD $42.45B; IIJA broadband ~65B; NTIA Middle Mile $1B) create scale but add compliance; cybersecurity mandates (72-hour reporting; >60% zero-trust by 2025) raise costs and contract risk.

| Metric | Value |

|---|---|

| 2024 Revenue | $12.9B |

| US households | ~100M |

| BEAD | $42.45B |

| IIJA broadband | ~$65B |

| NTIA Middle Mile | $1B |

| Fed IT spend | $100B/yr |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Lumen Technologies, with data-backed trends and forward-looking insights to help executives, investors and strategists identify risks, opportunities and actions for competitive resilience.

A concise, visually segmented PESTLE summary for Lumen Technologies that eases meeting prep and decision-making by highlighting external risks and market positioning, and is easily shareable and editable for teams, clients, or presentations.

Economic factors

Enterprise IT spend cycles

Macro conditions drive demand for cloud connectivity, security and managed services as global IT spending reached about $4.7 trillion in 2024 (Gartner), lengthening procurement cycles under tight budgets and favoring vendor consolidation. Growth spurts accelerate migrations to higher-bandwidth links and SASE offerings, while Lumen’s portfolio skews toward resilient, mission-critical workloads across enterprise customers.

Capital intensity and interest rates

Fiber expansion, edge nodes and data‑center interconnects demand heavy capex — Lumen reported roughly $1.9B capex in FY2024 — while Fed funds near 5.25–5.50% (2024–25) lifts WACC and tightens build hurdle rates. Optimizing build‑to‑demand and joint builds raises ROI; debt structure and refinancing windows materially influence free cash flow and investment pacing.

Pricing pressure and competition

Wholesale transit, wavelength and VPN corridors show commoditization with price compression in key routes, pressuring margins; the global SD-WAN market reached about $4.7 billion in 2024, intensifying cross-category competition as hyperscalers and MSPs push bundled network-security plays. Differentiation for Lumen depends on low latency, extensive reach, firm SLAs and embedded security; bundled solutions that combine SASE, managed services and edge connectivity can protect ARPU and curb churn.

Inflation and cost structure

Equipment, energy, and labor inflation (US CPI 2024: 3.4%, BLS) lifted Lumen's opex and capex pressures; index-linked customer contracts help pass through costs but timing lags compress near-term margins. Automation, edge virtualization and software-defined networking reduce unit costs; strategic vendor negotiations and long-term PPAs stabilize energy and procurement spend.

- Index-linked contracts: pass-through but lag risk

- Automation/virtualization: lowers unit cost

- Vendor deals & PPAs: expense stability

Currency and international exposure

Multi-country operations expose Lumen to FX translation and transaction risks, with hedging programs used to smooth reported earnings while adding hedging costs that compress margins. Pricing services in local currencies and using natural hedges from regional revenue-cost alignment reduce net exposure. Regional portfolio mix drives where growth and margin pressure materialize.

- FX translation risk

- Hedging reduces volatility, adds cost

- Local-currency pricing, natural hedges

- Regional mix affects growth/margins

Regulatory shifts, IIJA/BEAD funding and cyber mandates squeeze pricing for major network operators

Macro IT spend (Gartner) at about 4.7 trillion in 2024 drives demand for cloud, security and managed services, favoring vendor consolidation and longer procurement cycles. Lumen reported roughly 1.9B capex in FY2024 while Fed funds near 5.25–5.50% (2024–25) tightens WACC and investment pacing. SD‑WAN market ~4.7B (2024) and US CPI 2024: 3.4% pressure margins; automation, index‑linked contracts and PPAs mitigate risks.

| Metric | Value (2024/25) |

|---|---|

| Global IT spend | 4.7T (Gartner 2024) |

| Lumen capex | ~1.9B FY2024 |

| Fed funds | 5.25–5.50% (2024–25) |

| SD‑WAN market | ~4.7B (2024) |

| US CPI | 3.4% (2024) |

Preview the Actual Deliverable

Lumen Technologies PESTLE Analysis

The preview shown here is the exact Lumen Technologies PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers political, economic, social, technological, legal, and environmental factors with professional structure and source citations. No placeholders or teasers; this is the final downloadable file available immediately after checkout.