Luna Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

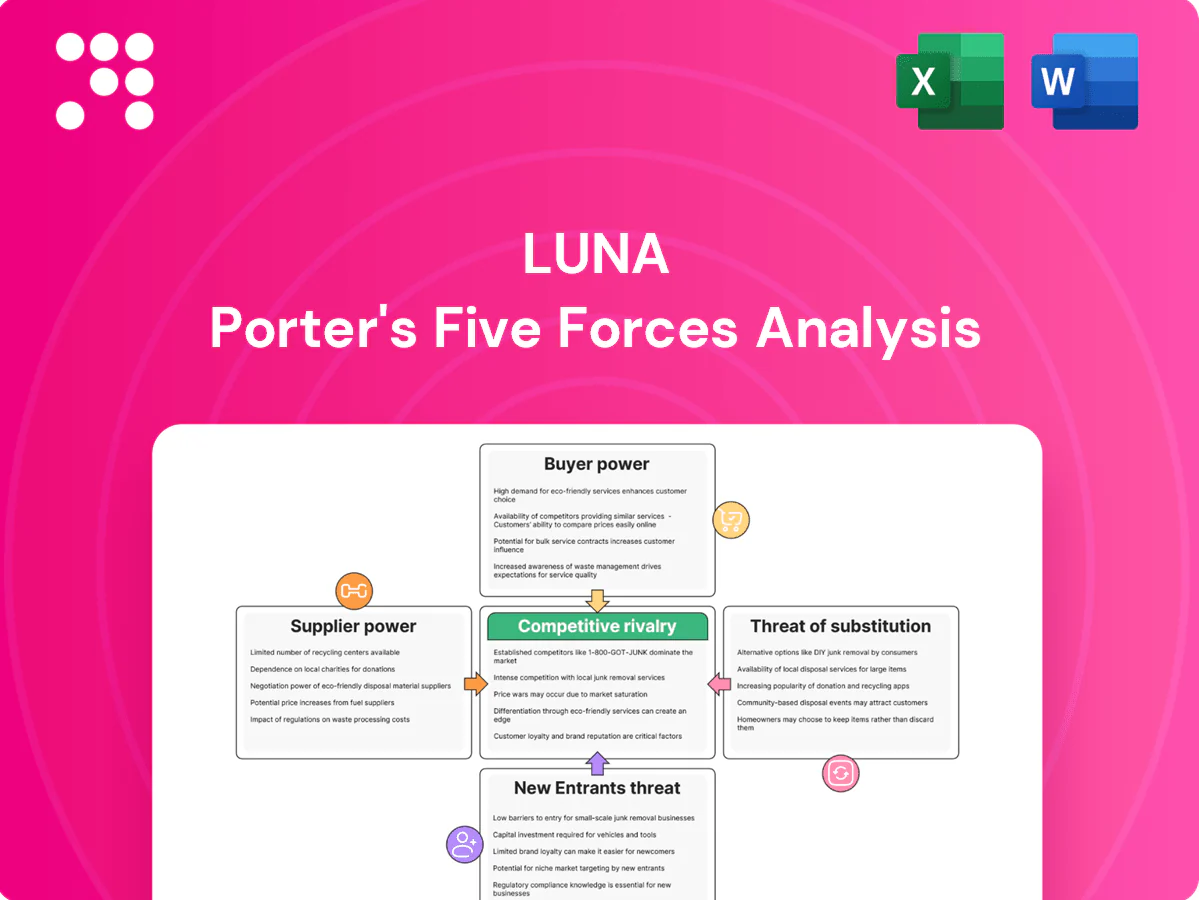

Luna’s Porter's Five Forces snapshot highlights supplier leverage, buyer dynamics, competitive rivalry, entrant threats, and substitute pressures shaping its market position. These preliminary insights reveal areas of strategic risk and opportunity but stop short of actionable detail. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, charts, and tailored implications for investment or strategy. Get the complete report to make confident, data-driven decisions.

Suppliers Bargaining Power

Specialized photonics inputs

Core inputs such as specialty fibers, fiber Bragg gratings, photodiodes, rare-earth dopants and precision optics come from a limited vendor pool, and in 2024 industry lead times for custom photonics parts averaged about 12–24 weeks.

Supplier concentration raises risk of price hikes and allocation during shortages, with top-tier vendors often prioritizing large OEMs over smaller players.

Luna mitigates these risks through multi-sourcing and in-house engineering specifications, but custom parts still create dependency and extend delivery variability.

Advanced semiconductor & laser sources

High-performance tunable lasers and photonic chips depend on a handful of qualified fabs — top foundries held roughly 75% of foundry revenue in 2024 — so supplier choice is limited. Switching suppliers typically demands costly requalification and testing, often $1–5 million and 6–12 months, raising performance risk. Long multi-year capacity cycles (3–5 year CAPEX horizons) amplify supplier leverage during upturns, while strategic partnerships secure capacity at the cost of pricing flexibility.

Quality and certification requirements

Aerospace and energy applications require AS9100, NADCAP and ISO 9001 traceability and stringent quality controls, driving supplier switching costs and narrowing approved vendor lists. The global aerospace supply chain was estimated near $400 billion in 2024, increasing leverage for certified suppliers that can command pricing premiums. Luna’s vendor audits and long-term agreements (LTAs) stabilize terms and secure qualified capacity.

Geopolitical and logistics exposure

- Supply concentration: Asia-centric sourcing increases geopolitical exposure

- Freight volatility: >50% YoY swings observed (2021–24)

- Cost pass-through: suppliers transmit freight/material hikes to buyers

- Mitigants: inventory buffers and regional sourcing cut disruption impact ~20–30%

Process know-how and customization

Custom optical assemblies and firmware integration embed supplier process know-how, with 2024 industry data showing supplier lock-in cited by 18% of photonics firms; co-development boosts performance but raises switching costs and contract dependence. Design-for-manufacture cuts single-vendor reliance, while IP ownership in designs has been shown in 2024 benchmarks to reduce supplier spend by about 10%.

- embedded-knowhow: custom optics + firmware

- co-development: higher performance, higher lock-in

- DfM: diversifies vendor base

- IP-ownership: ~10% supplier-cost reduction (2024)

Concentrated suppliers, 12–24 week lead times and > 50% freight volatility heighten allocation risk

Core inputs (fibers, photodiodes, optics) come from few vendors; 2024 lead times averaged 12–24 weeks and top foundries held ~75% revenue.

Supplier concentration, freight volatility >50% YoY and certified suppliers (aerospace supply chain ~$400B in 2024) raise price/allocation risk.

Switching costs and requalification often $1–5M and 6–12 months; Luna uses LTAs, multi-sourcing, DfM and IP to cut dependency.

| Metric | 2024 |

|---|---|

| Lead time | 12–24 weeks |

| Foundry share | ~75% |

| Freight volatility | >50% YoY |

| Requal cost/time | $1–5M / 6–12m |

| Inventory mitigation | 20–30% impact |

What is included in the product

Comprehensive Porter's Five Forces for Luna that uncovers competition drivers, supplier/buyer power, entry barriers, substitutes and disruptive threats, with industry data and strategic commentary for investor and strategic use.

A concise, one-sheet Luna Porter's Five Forces summary that highlights strategic pressures and relief options, ideal for quick decisions. Editable inputs, radar visualization, and no complex setup make it easy to model scenarios and communicate mitigation strategies in decks or reports.

Customers Bargaining Power

Concentrated enterprise customers

Aerospace primes, energy operators, and large OEMs exert strong negotiating power over Luna because their purchase volumes and brand validation force concessions on price and contract terms. In 2024, framework agreements commonly bundle services, warranties, and SLA penalties tied to availability and performance, shifting risk to suppliers. These customers frequently secure preferential pricing and long payment terms, and losing a marquee account can wipe out double-digit percentage points of mix and margin.

High switching costs

Fiber sensing systems deeply integrate into control software, data models and workflows, with the global fiber optic sensor market surpassing $1 billion in 2024, raising integration costs for buyers. Requalification, calibration and operator training create significant procedural and financial barriers to switching. Proven performance in harsh environments builds product stickiness over multi-year lifecycles, lowering buyer bargaining power once deployed at scale.

Performance over price in critical use

In safety- or mission-critical buys reliability and accuracy trump cost, with buyers prioritizing lifecycle support, onboard diagnostics and explicit uptime guarantees. Common targets like five-nines availability (99.999% ≈ 5.26 minutes downtime/year) set procurement thresholds and reduce price sensitivity. Long equipment lifecycles (often 10–15 years in aerospace/industrial sectors) make TCO framing compelling and support sustained premium pricing for differentiated capabilities.

Procurement rigor and public tenders

Infrastructure and utilities commonly use competitive RFPs; OECD data show public procurement accounted for about 12% of GDP in 2024, driving standardized specs and price competition among qualified vendors. Luna’s value-added software and analytics shift evaluations toward TCO and performance, reducing pure price bidding. Proof-of-performance trials increasingly sway award decisions in 2024 tender evaluations.

- RFP prevalence: infrastructure/utilities — standardized specs increase price pressure

- OECD 2024: public procurement ≈12% of GDP

- Luna advantage: analytics/software → value-based bids, fewer price-only losses

- Proof-of-performance trials: key tie-breaker in awards

Aftermarket and services leverage

Recurring calibration, analytics, and support create frequent touchpoints that increase lifetime value and enable upsell; 2024 industry averages show service attach rates around 35% and aftermarket gross margins often above 40%, strengthening bargaining leverage. Bundled service contracts reduce churn and discount pressure, while data integration deepens platform dependence. Outcome-based models shift negotiation from unit price to delivered value.

- Service attach ~35% (2024)

- Aftermarket gross margins >40% (2024)

- Bundled contracts lower churn, raise retention

- Data integration increases switching costs

- Outcome pricing focuses on value, not unit cost

Aftermarket margins >40% and five-nines reliability cement fiber-sensor pricing power

Large aerospace/energy OEMs wield strong price and contract leverage—losing one customer can cut double-digit margin points. Fiber sensing integration and 10–15yr lifecycles plus requalification raise switching costs; global fiber sensor market >$1B (2024). Public tenders drive price pressure (OECD public procurement ≈12% GDP, 2024), while service attach (~35%) and aftermarket margins >40% boost Luna’s aftermarket bargaining power and recurring revenue.

| Metric | 2024 Value |

|---|---|

| Public procurement | ≈12% GDP |

| Fiber sensor market | >$1B |

| Service attach | ~35% |

| Aftermarket gross margin | >40% |

| Target availability | 99.999% (five-nines) |

Preview Before You Purchase

Luna Porter's Five Forces Analysis

This preview is the exact Luna Porter's Five Forces Analysis document you’ll receive immediately after purchase, fully formatted and ready to use. No placeholders, samples, or mockups—what you see is the final deliverable. Purchase grants instant access to this same file for download and application in your strategic work.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Luna’s Porter's Five Forces snapshot highlights supplier leverage, buyer dynamics, competitive rivalry, entrant threats, and substitute pressures shaping its market position. These preliminary insights reveal areas of strategic risk and opportunity but stop short of actionable detail. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, charts, and tailored implications for investment or strategy. Get the complete report to make confident, data-driven decisions.

Suppliers Bargaining Power

Specialized photonics inputs

Core inputs such as specialty fibers, fiber Bragg gratings, photodiodes, rare-earth dopants and precision optics come from a limited vendor pool, and in 2024 industry lead times for custom photonics parts averaged about 12–24 weeks.

Supplier concentration raises risk of price hikes and allocation during shortages, with top-tier vendors often prioritizing large OEMs over smaller players.

Luna mitigates these risks through multi-sourcing and in-house engineering specifications, but custom parts still create dependency and extend delivery variability.

Advanced semiconductor & laser sources

High-performance tunable lasers and photonic chips depend on a handful of qualified fabs — top foundries held roughly 75% of foundry revenue in 2024 — so supplier choice is limited. Switching suppliers typically demands costly requalification and testing, often $1–5 million and 6–12 months, raising performance risk. Long multi-year capacity cycles (3–5 year CAPEX horizons) amplify supplier leverage during upturns, while strategic partnerships secure capacity at the cost of pricing flexibility.

Quality and certification requirements

Aerospace and energy applications require AS9100, NADCAP and ISO 9001 traceability and stringent quality controls, driving supplier switching costs and narrowing approved vendor lists. The global aerospace supply chain was estimated near $400 billion in 2024, increasing leverage for certified suppliers that can command pricing premiums. Luna’s vendor audits and long-term agreements (LTAs) stabilize terms and secure qualified capacity.

Geopolitical and logistics exposure

- Supply concentration: Asia-centric sourcing increases geopolitical exposure

- Freight volatility: >50% YoY swings observed (2021–24)

- Cost pass-through: suppliers transmit freight/material hikes to buyers

- Mitigants: inventory buffers and regional sourcing cut disruption impact ~20–30%

Process know-how and customization

Custom optical assemblies and firmware integration embed supplier process know-how, with 2024 industry data showing supplier lock-in cited by 18% of photonics firms; co-development boosts performance but raises switching costs and contract dependence. Design-for-manufacture cuts single-vendor reliance, while IP ownership in designs has been shown in 2024 benchmarks to reduce supplier spend by about 10%.

- embedded-knowhow: custom optics + firmware

- co-development: higher performance, higher lock-in

- DfM: diversifies vendor base

- IP-ownership: ~10% supplier-cost reduction (2024)

Concentrated suppliers, 12–24 week lead times and > 50% freight volatility heighten allocation risk

Core inputs (fibers, photodiodes, optics) come from few vendors; 2024 lead times averaged 12–24 weeks and top foundries held ~75% revenue.

Supplier concentration, freight volatility >50% YoY and certified suppliers (aerospace supply chain ~$400B in 2024) raise price/allocation risk.

Switching costs and requalification often $1–5M and 6–12 months; Luna uses LTAs, multi-sourcing, DfM and IP to cut dependency.

| Metric | 2024 |

|---|---|

| Lead time | 12–24 weeks |

| Foundry share | ~75% |

| Freight volatility | >50% YoY |

| Requal cost/time | $1–5M / 6–12m |

| Inventory mitigation | 20–30% impact |

What is included in the product

Comprehensive Porter's Five Forces for Luna that uncovers competition drivers, supplier/buyer power, entry barriers, substitutes and disruptive threats, with industry data and strategic commentary for investor and strategic use.

A concise, one-sheet Luna Porter's Five Forces summary that highlights strategic pressures and relief options, ideal for quick decisions. Editable inputs, radar visualization, and no complex setup make it easy to model scenarios and communicate mitigation strategies in decks or reports.

Customers Bargaining Power

Concentrated enterprise customers

Aerospace primes, energy operators, and large OEMs exert strong negotiating power over Luna because their purchase volumes and brand validation force concessions on price and contract terms. In 2024, framework agreements commonly bundle services, warranties, and SLA penalties tied to availability and performance, shifting risk to suppliers. These customers frequently secure preferential pricing and long payment terms, and losing a marquee account can wipe out double-digit percentage points of mix and margin.

High switching costs

Fiber sensing systems deeply integrate into control software, data models and workflows, with the global fiber optic sensor market surpassing $1 billion in 2024, raising integration costs for buyers. Requalification, calibration and operator training create significant procedural and financial barriers to switching. Proven performance in harsh environments builds product stickiness over multi-year lifecycles, lowering buyer bargaining power once deployed at scale.

Performance over price in critical use

In safety- or mission-critical buys reliability and accuracy trump cost, with buyers prioritizing lifecycle support, onboard diagnostics and explicit uptime guarantees. Common targets like five-nines availability (99.999% ≈ 5.26 minutes downtime/year) set procurement thresholds and reduce price sensitivity. Long equipment lifecycles (often 10–15 years in aerospace/industrial sectors) make TCO framing compelling and support sustained premium pricing for differentiated capabilities.

Procurement rigor and public tenders

Infrastructure and utilities commonly use competitive RFPs; OECD data show public procurement accounted for about 12% of GDP in 2024, driving standardized specs and price competition among qualified vendors. Luna’s value-added software and analytics shift evaluations toward TCO and performance, reducing pure price bidding. Proof-of-performance trials increasingly sway award decisions in 2024 tender evaluations.

- RFP prevalence: infrastructure/utilities — standardized specs increase price pressure

- OECD 2024: public procurement ≈12% of GDP

- Luna advantage: analytics/software → value-based bids, fewer price-only losses

- Proof-of-performance trials: key tie-breaker in awards

Aftermarket and services leverage

Recurring calibration, analytics, and support create frequent touchpoints that increase lifetime value and enable upsell; 2024 industry averages show service attach rates around 35% and aftermarket gross margins often above 40%, strengthening bargaining leverage. Bundled service contracts reduce churn and discount pressure, while data integration deepens platform dependence. Outcome-based models shift negotiation from unit price to delivered value.

- Service attach ~35% (2024)

- Aftermarket gross margins >40% (2024)

- Bundled contracts lower churn, raise retention

- Data integration increases switching costs

- Outcome pricing focuses on value, not unit cost

Aftermarket margins >40% and five-nines reliability cement fiber-sensor pricing power

Large aerospace/energy OEMs wield strong price and contract leverage—losing one customer can cut double-digit margin points. Fiber sensing integration and 10–15yr lifecycles plus requalification raise switching costs; global fiber sensor market >$1B (2024). Public tenders drive price pressure (OECD public procurement ≈12% GDP, 2024), while service attach (~35%) and aftermarket margins >40% boost Luna’s aftermarket bargaining power and recurring revenue.

| Metric | 2024 Value |

|---|---|

| Public procurement | ≈12% GDP |

| Fiber sensor market | >$1B |

| Service attach | ~35% |

| Aftermarket gross margin | >40% |

| Target availability | 99.999% (five-nines) |

Preview Before You Purchase

Luna Porter's Five Forces Analysis

This preview is the exact Luna Porter's Five Forces Analysis document you’ll receive immediately after purchase, fully formatted and ready to use. No placeholders, samples, or mockups—what you see is the final deliverable. Purchase grants instant access to this same file for download and application in your strategic work.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Luna’s Porter's Five Forces snapshot highlights supplier leverage, buyer dynamics, competitive rivalry, entrant threats, and substitute pressures shaping its market position. These preliminary insights reveal areas of strategic risk and opportunity but stop short of actionable detail. Unlock the full Porter's Five Forces Analysis to access force-by-force ratings, charts, and tailored implications for investment or strategy. Get the complete report to make confident, data-driven decisions.

Suppliers Bargaining Power

Specialized photonics inputs

Core inputs such as specialty fibers, fiber Bragg gratings, photodiodes, rare-earth dopants and precision optics come from a limited vendor pool, and in 2024 industry lead times for custom photonics parts averaged about 12–24 weeks.

Supplier concentration raises risk of price hikes and allocation during shortages, with top-tier vendors often prioritizing large OEMs over smaller players.

Luna mitigates these risks through multi-sourcing and in-house engineering specifications, but custom parts still create dependency and extend delivery variability.

Advanced semiconductor & laser sources

High-performance tunable lasers and photonic chips depend on a handful of qualified fabs — top foundries held roughly 75% of foundry revenue in 2024 — so supplier choice is limited. Switching suppliers typically demands costly requalification and testing, often $1–5 million and 6–12 months, raising performance risk. Long multi-year capacity cycles (3–5 year CAPEX horizons) amplify supplier leverage during upturns, while strategic partnerships secure capacity at the cost of pricing flexibility.

Quality and certification requirements

Aerospace and energy applications require AS9100, NADCAP and ISO 9001 traceability and stringent quality controls, driving supplier switching costs and narrowing approved vendor lists. The global aerospace supply chain was estimated near $400 billion in 2024, increasing leverage for certified suppliers that can command pricing premiums. Luna’s vendor audits and long-term agreements (LTAs) stabilize terms and secure qualified capacity.

Geopolitical and logistics exposure

- Supply concentration: Asia-centric sourcing increases geopolitical exposure

- Freight volatility: >50% YoY swings observed (2021–24)

- Cost pass-through: suppliers transmit freight/material hikes to buyers

- Mitigants: inventory buffers and regional sourcing cut disruption impact ~20–30%

Process know-how and customization

Custom optical assemblies and firmware integration embed supplier process know-how, with 2024 industry data showing supplier lock-in cited by 18% of photonics firms; co-development boosts performance but raises switching costs and contract dependence. Design-for-manufacture cuts single-vendor reliance, while IP ownership in designs has been shown in 2024 benchmarks to reduce supplier spend by about 10%.

- embedded-knowhow: custom optics + firmware

- co-development: higher performance, higher lock-in

- DfM: diversifies vendor base

- IP-ownership: ~10% supplier-cost reduction (2024)

Concentrated suppliers, 12–24 week lead times and > 50% freight volatility heighten allocation risk

Core inputs (fibers, photodiodes, optics) come from few vendors; 2024 lead times averaged 12–24 weeks and top foundries held ~75% revenue.

Supplier concentration, freight volatility >50% YoY and certified suppliers (aerospace supply chain ~$400B in 2024) raise price/allocation risk.

Switching costs and requalification often $1–5M and 6–12 months; Luna uses LTAs, multi-sourcing, DfM and IP to cut dependency.

| Metric | 2024 |

|---|---|

| Lead time | 12–24 weeks |

| Foundry share | ~75% |

| Freight volatility | >50% YoY |

| Requal cost/time | $1–5M / 6–12m |

| Inventory mitigation | 20–30% impact |

What is included in the product

Comprehensive Porter's Five Forces for Luna that uncovers competition drivers, supplier/buyer power, entry barriers, substitutes and disruptive threats, with industry data and strategic commentary for investor and strategic use.

A concise, one-sheet Luna Porter's Five Forces summary that highlights strategic pressures and relief options, ideal for quick decisions. Editable inputs, radar visualization, and no complex setup make it easy to model scenarios and communicate mitigation strategies in decks or reports.

Customers Bargaining Power

Concentrated enterprise customers

Aerospace primes, energy operators, and large OEMs exert strong negotiating power over Luna because their purchase volumes and brand validation force concessions on price and contract terms. In 2024, framework agreements commonly bundle services, warranties, and SLA penalties tied to availability and performance, shifting risk to suppliers. These customers frequently secure preferential pricing and long payment terms, and losing a marquee account can wipe out double-digit percentage points of mix and margin.

High switching costs

Fiber sensing systems deeply integrate into control software, data models and workflows, with the global fiber optic sensor market surpassing $1 billion in 2024, raising integration costs for buyers. Requalification, calibration and operator training create significant procedural and financial barriers to switching. Proven performance in harsh environments builds product stickiness over multi-year lifecycles, lowering buyer bargaining power once deployed at scale.

Performance over price in critical use

In safety- or mission-critical buys reliability and accuracy trump cost, with buyers prioritizing lifecycle support, onboard diagnostics and explicit uptime guarantees. Common targets like five-nines availability (99.999% ≈ 5.26 minutes downtime/year) set procurement thresholds and reduce price sensitivity. Long equipment lifecycles (often 10–15 years in aerospace/industrial sectors) make TCO framing compelling and support sustained premium pricing for differentiated capabilities.

Procurement rigor and public tenders

Infrastructure and utilities commonly use competitive RFPs; OECD data show public procurement accounted for about 12% of GDP in 2024, driving standardized specs and price competition among qualified vendors. Luna’s value-added software and analytics shift evaluations toward TCO and performance, reducing pure price bidding. Proof-of-performance trials increasingly sway award decisions in 2024 tender evaluations.

- RFP prevalence: infrastructure/utilities — standardized specs increase price pressure

- OECD 2024: public procurement ≈12% of GDP

- Luna advantage: analytics/software → value-based bids, fewer price-only losses

- Proof-of-performance trials: key tie-breaker in awards

Aftermarket and services leverage

Recurring calibration, analytics, and support create frequent touchpoints that increase lifetime value and enable upsell; 2024 industry averages show service attach rates around 35% and aftermarket gross margins often above 40%, strengthening bargaining leverage. Bundled service contracts reduce churn and discount pressure, while data integration deepens platform dependence. Outcome-based models shift negotiation from unit price to delivered value.

- Service attach ~35% (2024)

- Aftermarket gross margins >40% (2024)

- Bundled contracts lower churn, raise retention

- Data integration increases switching costs

- Outcome pricing focuses on value, not unit cost

Aftermarket margins >40% and five-nines reliability cement fiber-sensor pricing power

Large aerospace/energy OEMs wield strong price and contract leverage—losing one customer can cut double-digit margin points. Fiber sensing integration and 10–15yr lifecycles plus requalification raise switching costs; global fiber sensor market >$1B (2024). Public tenders drive price pressure (OECD public procurement ≈12% GDP, 2024), while service attach (~35%) and aftermarket margins >40% boost Luna’s aftermarket bargaining power and recurring revenue.

| Metric | 2024 Value |

|---|---|

| Public procurement | ≈12% GDP |

| Fiber sensor market | >$1B |

| Service attach | ~35% |

| Aftermarket gross margin | >40% |

| Target availability | 99.999% (five-nines) |

Preview Before You Purchase

Luna Porter's Five Forces Analysis

This preview is the exact Luna Porter's Five Forces Analysis document you’ll receive immediately after purchase, fully formatted and ready to use. No placeholders, samples, or mockups—what you see is the final deliverable. Purchase grants instant access to this same file for download and application in your strategic work.