Lundin Gold Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Lundin Gold faces concentrated supplier power, shifting buyer dynamics, and material threats from substitutes and regulatory shifts that shape its margin outlook and expansion potential. Our snapshot highlights key competitive levers and vulnerabilities investors should monitor. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lundin Gold’s competitive dynamics, market pressures, and strategic advantages in detail.

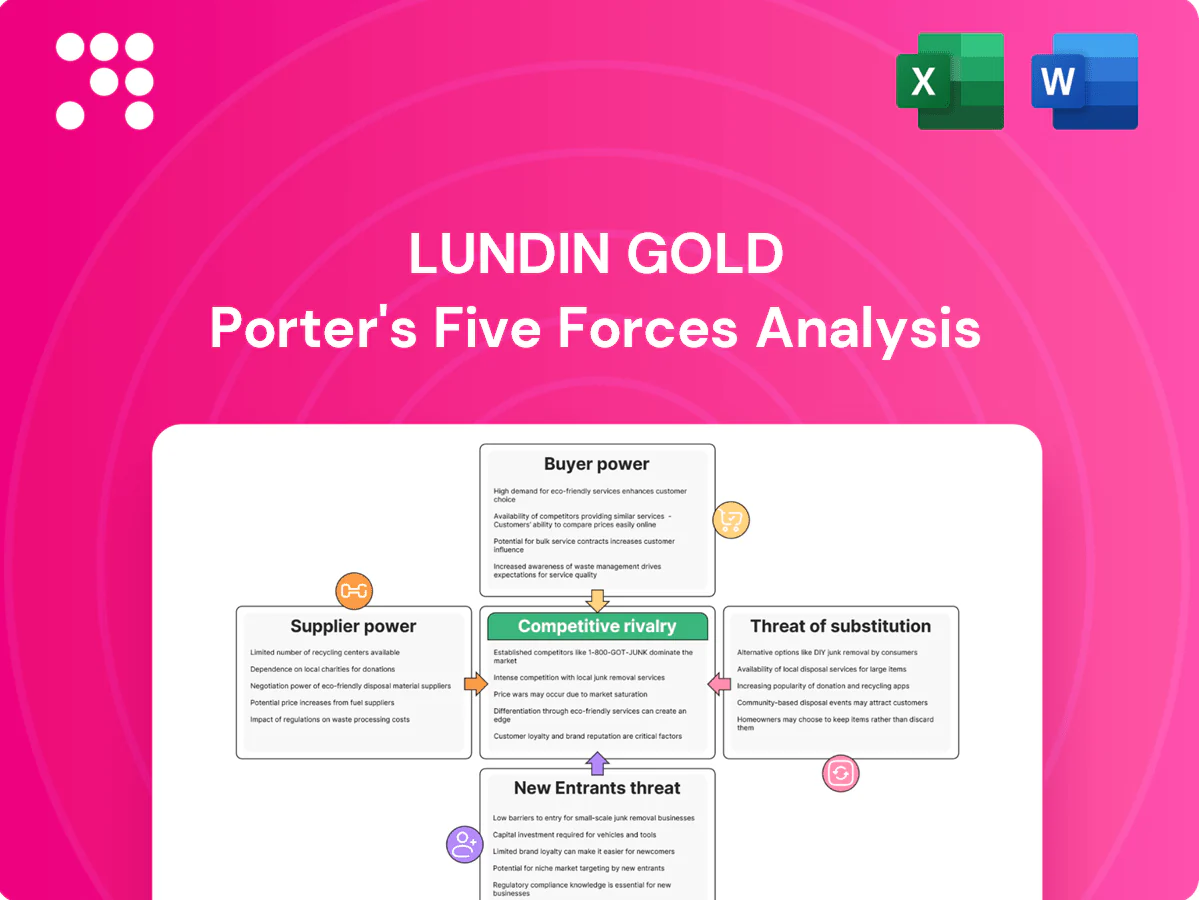

Suppliers Bargaining Power

Concentrated OEM and reagent suppliers

Lundin Gold’s Fruta del Norte relies on concentrated OEMs (Caterpillar, Sandvik, Epiroc) for underground fleets and reagent suppliers (Orica, Cyanco, Carus) for cyanide, creating switching costs and delivery risk. Concentration lets suppliers press pricing and service terms during industry upcycles, though long‑term purchase contracts and bundled maintenance mitigate some pressure; spares lead times of several months and Ecuador’s remote logistics amplify supplier leverage.

Energy and fuel dependency

Fruta del Norte's >200,000 oz annual output makes power and diesel availability critical; southeastern Ecuador's grid constraints and remote fuel import logistics give utilities and distributors situational bargaining power over operating continuity. Hedging and on-site storage limit price volatility but cannot remove outage or transport risks, while decarbonization can force higher-cost renewables or offsets, raising OPEX.

Specialized contractors and skilled labor

Underground mining at Fruta del Norte requires scarce specialized contractors, geotechnical experts and experienced miners, concentrating bargaining power with talent providers and driving wage and contractor-rate pressure. Building training pipelines and prioritizing community hiring can lower reliance over time, but near-term leverage remains with external specialists. Linking contractor pay to safety and productivity KPIs aligns incentives and mitigates cost escalation.

Logistics and export chain

Inbound heavy equipment and outbound doré/refined metal rely on secure road, port and refinery access; freight forwarders, security firms and refiners can raise fees or delay schedules, increasing supplier leverage during shipments.

- Multi-route access reduces concentration risk

- Multiple refiners lower counterparty power

- Political or weather shocks temporarily spike supplier leverage

ESG-compliant input standards

Responsible mining commitments at Lundin Gold narrow the supplier pool to ESG-compliant vendors, raising compliance costs and reducing procurement flexibility.

Certified cyanide and ethical sourcing standards increase supplier bargaining power where qualified providers are limited, but ESG alignment fosters deeper partnerships that lower operational and reputational risk.

Transparent procurement and public ESG criteria can attract competitive bids from qualified suppliers, partially offsetting higher costs.

- ESG limits supplier universe

- Certified inputs elevate supplier leverage

- Stronger partnerships reduce risk

- Transparency attracts competitive bids

Concentrated OEMs, reagent and fuel supply risks with 200,000 oz/yr exposure

Lundin Gold’s Fruta del Norte faces concentrated OEM and reagent suppliers creating switching costs and delivery risk; spares lead times of 3–6 months and >200,000 oz annual output heighten supplier leverage. Grid/fuel constraints make utilities and diesel suppliers critical to operations. ESG sourcing narrows the vendor pool, raising procurement costs despite long‑term contracts and partnerships that mitigate some pressure.

| Supplier category | Key risk | Metric (2024) |

|---|---|---|

| OEMs (Caterpillar/Sandvik/Epiroc) | Switching cost, lead times | Lead times 3–6 months |

| Reagents (cyanide) | Certified supplier concentration | Limited certified providers |

| Fuel/utilities | Operational continuity | Supports >200,000 oz/yr |

| Contractors | Skilled labour scarcity | High contractor rates |

What is included in the product

Tailored Porter's Five Forces for Lundin Gold uncovering the key drivers of competition, customer influence, supplier power, and market entry risks in the gold mining sector. It evaluates supplier and buyer control, identifies substitutes and disruptive threats, and highlights barriers protecting Lundin Gold’s margins and market position.

A clear one-sheet Porter's Five Forces summary for Lundin Gold—customize pressure levels with current commodity, regulatory and geopolitical data to instantly gauge strategic risk. Clean layout and spider chart make it slide-ready, easy to edit without macros and simple to integrate into executive decks or broader Excel dashboards.

Customers Bargaining Power

Commodity price-taking buyers

Gold is globally traded on deep venues such as the LBMA with annual mine supply around 3,000 tonnes, so Lundin sells into a liquid, standardized market where spot pricing dominates. Individual buyers like refiners and bullion banks have limited power over base price but can negotiate premiums, discounts and payment/hedging terms. Lundin’s offtake contracts and broad spot liquidity dilute any single buyer’s leverage.

Refiners and bullion banks concentration

There are fewer than 100 LBMA Good Delivery and similarly accredited refiners globally in 2024, concentrating negotiating leverage over refining charges and assays in the hands of refiners and large bullion banks (top dealers dominate OTC liquidity). Maintaining relationships with multiple qualified refiners and published, transparent assay protocols limits payment and assay disputes. Compliance with Responsible Gold standards narrows eligible refiners but improves access to premium markets and institutional buyers.

Investor and lender ESG expectations

Investor and lender ESG expectations are shifting capital terms for Lundin Gold, with sustainability covenants increasingly embedded in financing and offtake contracts, affecting pricing and access. Meeting benchmarks helps keep financing costs competitive but raises compliance burdens and reporting obligations. Failure to meet standards empowers buyers and creditors to demand tighter terms or higher premiums. Strong ESG performance can make Lundin a preferred supplier and tilt bargaining power in its favor.

Product differentiation via low costs

Fruta del Norte’s high reserve grade (8.8 g/t) and low AISC (≈$800/oz in 2024) strengthen Lundin Gold’s product differentiation via low costs, lowering pressure to offer concessional terms to buyers. Buyers’ preference for reliable, low‑risk supply and consistent quarterly deliveries (~340 koz 2024 guidance) reduces their leverage over a dependable producer. Hedging flexibility and steady quality further constrain customer bargaining power.

Currency and payment terms

Ecuador has been dollarized since 2000, simplifying USD settlement and removing FX negotiation as a bargaining lever; buyers still may press for tighter payment terms in demand softness. Lundin Gold mitigates this via buyer optionality, competitive cash costs and use of insurance and trade-credit instruments to limit counterparty leverage.

- Dollarized since 2000: USD settlement simplifies contracting

- Buyers push tighter terms in soft markets

- Lundin counters with multiple buyers and low cash costs

- Insurance/credit instruments reduce counterparty risk

High-grade, low-cost producer limits buyer leverage despite concentrated LBMA refiner market

Lundin sells into deep, liquid LBMA markets so spot pricing limits single-buyer control; offtakes and multiple refiners dilute leverage. Concentration among <100 LBMA refiners and ESG-linked finance raise negotiable fees and covenants. High grade (8.8 g/t), low AISC (~$800/oz) and ~340 koz 2024 guidance reduce need for concessional terms.

| Metric | 2024 |

|---|---|

| Grade | 8.8 g/t |

| AISC | ≈$800/oz |

| Guidance | ~340 koz |

| LBMA refiners | <100 |

Same Document Delivered

Lundin Gold Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Lundin Gold you'll receive after purchase—no placeholders. It assesses competitive rivalry, supplier and buyer power, and threats of substitutes and new entrants with concise, data-driven insights. The document is professionally formatted and ready for immediate download.

A Must-Have Tool for Decision-Makers

Lundin Gold faces concentrated supplier power, shifting buyer dynamics, and material threats from substitutes and regulatory shifts that shape its margin outlook and expansion potential. Our snapshot highlights key competitive levers and vulnerabilities investors should monitor. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lundin Gold’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated OEM and reagent suppliers

Lundin Gold’s Fruta del Norte relies on concentrated OEMs (Caterpillar, Sandvik, Epiroc) for underground fleets and reagent suppliers (Orica, Cyanco, Carus) for cyanide, creating switching costs and delivery risk. Concentration lets suppliers press pricing and service terms during industry upcycles, though long‑term purchase contracts and bundled maintenance mitigate some pressure; spares lead times of several months and Ecuador’s remote logistics amplify supplier leverage.

Energy and fuel dependency

Fruta del Norte's >200,000 oz annual output makes power and diesel availability critical; southeastern Ecuador's grid constraints and remote fuel import logistics give utilities and distributors situational bargaining power over operating continuity. Hedging and on-site storage limit price volatility but cannot remove outage or transport risks, while decarbonization can force higher-cost renewables or offsets, raising OPEX.

Specialized contractors and skilled labor

Underground mining at Fruta del Norte requires scarce specialized contractors, geotechnical experts and experienced miners, concentrating bargaining power with talent providers and driving wage and contractor-rate pressure. Building training pipelines and prioritizing community hiring can lower reliance over time, but near-term leverage remains with external specialists. Linking contractor pay to safety and productivity KPIs aligns incentives and mitigates cost escalation.

Logistics and export chain

Inbound heavy equipment and outbound doré/refined metal rely on secure road, port and refinery access; freight forwarders, security firms and refiners can raise fees or delay schedules, increasing supplier leverage during shipments.

- Multi-route access reduces concentration risk

- Multiple refiners lower counterparty power

- Political or weather shocks temporarily spike supplier leverage

ESG-compliant input standards

Responsible mining commitments at Lundin Gold narrow the supplier pool to ESG-compliant vendors, raising compliance costs and reducing procurement flexibility.

Certified cyanide and ethical sourcing standards increase supplier bargaining power where qualified providers are limited, but ESG alignment fosters deeper partnerships that lower operational and reputational risk.

Transparent procurement and public ESG criteria can attract competitive bids from qualified suppliers, partially offsetting higher costs.

- ESG limits supplier universe

- Certified inputs elevate supplier leverage

- Stronger partnerships reduce risk

- Transparency attracts competitive bids

Concentrated OEMs, reagent and fuel supply risks with 200,000 oz/yr exposure

Lundin Gold’s Fruta del Norte faces concentrated OEM and reagent suppliers creating switching costs and delivery risk; spares lead times of 3–6 months and >200,000 oz annual output heighten supplier leverage. Grid/fuel constraints make utilities and diesel suppliers critical to operations. ESG sourcing narrows the vendor pool, raising procurement costs despite long‑term contracts and partnerships that mitigate some pressure.

| Supplier category | Key risk | Metric (2024) |

|---|---|---|

| OEMs (Caterpillar/Sandvik/Epiroc) | Switching cost, lead times | Lead times 3–6 months |

| Reagents (cyanide) | Certified supplier concentration | Limited certified providers |

| Fuel/utilities | Operational continuity | Supports >200,000 oz/yr |

| Contractors | Skilled labour scarcity | High contractor rates |

What is included in the product

Tailored Porter's Five Forces for Lundin Gold uncovering the key drivers of competition, customer influence, supplier power, and market entry risks in the gold mining sector. It evaluates supplier and buyer control, identifies substitutes and disruptive threats, and highlights barriers protecting Lundin Gold’s margins and market position.

A clear one-sheet Porter's Five Forces summary for Lundin Gold—customize pressure levels with current commodity, regulatory and geopolitical data to instantly gauge strategic risk. Clean layout and spider chart make it slide-ready, easy to edit without macros and simple to integrate into executive decks or broader Excel dashboards.

Customers Bargaining Power

Commodity price-taking buyers

Gold is globally traded on deep venues such as the LBMA with annual mine supply around 3,000 tonnes, so Lundin sells into a liquid, standardized market where spot pricing dominates. Individual buyers like refiners and bullion banks have limited power over base price but can negotiate premiums, discounts and payment/hedging terms. Lundin’s offtake contracts and broad spot liquidity dilute any single buyer’s leverage.

Refiners and bullion banks concentration

There are fewer than 100 LBMA Good Delivery and similarly accredited refiners globally in 2024, concentrating negotiating leverage over refining charges and assays in the hands of refiners and large bullion banks (top dealers dominate OTC liquidity). Maintaining relationships with multiple qualified refiners and published, transparent assay protocols limits payment and assay disputes. Compliance with Responsible Gold standards narrows eligible refiners but improves access to premium markets and institutional buyers.

Investor and lender ESG expectations

Investor and lender ESG expectations are shifting capital terms for Lundin Gold, with sustainability covenants increasingly embedded in financing and offtake contracts, affecting pricing and access. Meeting benchmarks helps keep financing costs competitive but raises compliance burdens and reporting obligations. Failure to meet standards empowers buyers and creditors to demand tighter terms or higher premiums. Strong ESG performance can make Lundin a preferred supplier and tilt bargaining power in its favor.

Product differentiation via low costs

Fruta del Norte’s high reserve grade (8.8 g/t) and low AISC (≈$800/oz in 2024) strengthen Lundin Gold’s product differentiation via low costs, lowering pressure to offer concessional terms to buyers. Buyers’ preference for reliable, low‑risk supply and consistent quarterly deliveries (~340 koz 2024 guidance) reduces their leverage over a dependable producer. Hedging flexibility and steady quality further constrain customer bargaining power.

Currency and payment terms

Ecuador has been dollarized since 2000, simplifying USD settlement and removing FX negotiation as a bargaining lever; buyers still may press for tighter payment terms in demand softness. Lundin Gold mitigates this via buyer optionality, competitive cash costs and use of insurance and trade-credit instruments to limit counterparty leverage.

- Dollarized since 2000: USD settlement simplifies contracting

- Buyers push tighter terms in soft markets

- Lundin counters with multiple buyers and low cash costs

- Insurance/credit instruments reduce counterparty risk

High-grade, low-cost producer limits buyer leverage despite concentrated LBMA refiner market

Lundin sells into deep, liquid LBMA markets so spot pricing limits single-buyer control; offtakes and multiple refiners dilute leverage. Concentration among <100 LBMA refiners and ESG-linked finance raise negotiable fees and covenants. High grade (8.8 g/t), low AISC (~$800/oz) and ~340 koz 2024 guidance reduce need for concessional terms.

| Metric | 2024 |

|---|---|

| Grade | 8.8 g/t |

| AISC | ≈$800/oz |

| Guidance | ~340 koz |

| LBMA refiners | <100 |

Same Document Delivered

Lundin Gold Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Lundin Gold you'll receive after purchase—no placeholders. It assesses competitive rivalry, supplier and buyer power, and threats of substitutes and new entrants with concise, data-driven insights. The document is professionally formatted and ready for immediate download.

Description

A Must-Have Tool for Decision-Makers

Lundin Gold faces concentrated supplier power, shifting buyer dynamics, and material threats from substitutes and regulatory shifts that shape its margin outlook and expansion potential. Our snapshot highlights key competitive levers and vulnerabilities investors should monitor. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Lundin Gold’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated OEM and reagent suppliers

Lundin Gold’s Fruta del Norte relies on concentrated OEMs (Caterpillar, Sandvik, Epiroc) for underground fleets and reagent suppliers (Orica, Cyanco, Carus) for cyanide, creating switching costs and delivery risk. Concentration lets suppliers press pricing and service terms during industry upcycles, though long‑term purchase contracts and bundled maintenance mitigate some pressure; spares lead times of several months and Ecuador’s remote logistics amplify supplier leverage.

Energy and fuel dependency

Fruta del Norte's >200,000 oz annual output makes power and diesel availability critical; southeastern Ecuador's grid constraints and remote fuel import logistics give utilities and distributors situational bargaining power over operating continuity. Hedging and on-site storage limit price volatility but cannot remove outage or transport risks, while decarbonization can force higher-cost renewables or offsets, raising OPEX.

Specialized contractors and skilled labor

Underground mining at Fruta del Norte requires scarce specialized contractors, geotechnical experts and experienced miners, concentrating bargaining power with talent providers and driving wage and contractor-rate pressure. Building training pipelines and prioritizing community hiring can lower reliance over time, but near-term leverage remains with external specialists. Linking contractor pay to safety and productivity KPIs aligns incentives and mitigates cost escalation.

Logistics and export chain

Inbound heavy equipment and outbound doré/refined metal rely on secure road, port and refinery access; freight forwarders, security firms and refiners can raise fees or delay schedules, increasing supplier leverage during shipments.

- Multi-route access reduces concentration risk

- Multiple refiners lower counterparty power

- Political or weather shocks temporarily spike supplier leverage

ESG-compliant input standards

Responsible mining commitments at Lundin Gold narrow the supplier pool to ESG-compliant vendors, raising compliance costs and reducing procurement flexibility.

Certified cyanide and ethical sourcing standards increase supplier bargaining power where qualified providers are limited, but ESG alignment fosters deeper partnerships that lower operational and reputational risk.

Transparent procurement and public ESG criteria can attract competitive bids from qualified suppliers, partially offsetting higher costs.

- ESG limits supplier universe

- Certified inputs elevate supplier leverage

- Stronger partnerships reduce risk

- Transparency attracts competitive bids

Concentrated OEMs, reagent and fuel supply risks with 200,000 oz/yr exposure

Lundin Gold’s Fruta del Norte faces concentrated OEM and reagent suppliers creating switching costs and delivery risk; spares lead times of 3–6 months and >200,000 oz annual output heighten supplier leverage. Grid/fuel constraints make utilities and diesel suppliers critical to operations. ESG sourcing narrows the vendor pool, raising procurement costs despite long‑term contracts and partnerships that mitigate some pressure.

| Supplier category | Key risk | Metric (2024) |

|---|---|---|

| OEMs (Caterpillar/Sandvik/Epiroc) | Switching cost, lead times | Lead times 3–6 months |

| Reagents (cyanide) | Certified supplier concentration | Limited certified providers |

| Fuel/utilities | Operational continuity | Supports >200,000 oz/yr |

| Contractors | Skilled labour scarcity | High contractor rates |

What is included in the product

Tailored Porter's Five Forces for Lundin Gold uncovering the key drivers of competition, customer influence, supplier power, and market entry risks in the gold mining sector. It evaluates supplier and buyer control, identifies substitutes and disruptive threats, and highlights barriers protecting Lundin Gold’s margins and market position.

A clear one-sheet Porter's Five Forces summary for Lundin Gold—customize pressure levels with current commodity, regulatory and geopolitical data to instantly gauge strategic risk. Clean layout and spider chart make it slide-ready, easy to edit without macros and simple to integrate into executive decks or broader Excel dashboards.

Customers Bargaining Power

Commodity price-taking buyers

Gold is globally traded on deep venues such as the LBMA with annual mine supply around 3,000 tonnes, so Lundin sells into a liquid, standardized market where spot pricing dominates. Individual buyers like refiners and bullion banks have limited power over base price but can negotiate premiums, discounts and payment/hedging terms. Lundin’s offtake contracts and broad spot liquidity dilute any single buyer’s leverage.

Refiners and bullion banks concentration

There are fewer than 100 LBMA Good Delivery and similarly accredited refiners globally in 2024, concentrating negotiating leverage over refining charges and assays in the hands of refiners and large bullion banks (top dealers dominate OTC liquidity). Maintaining relationships with multiple qualified refiners and published, transparent assay protocols limits payment and assay disputes. Compliance with Responsible Gold standards narrows eligible refiners but improves access to premium markets and institutional buyers.

Investor and lender ESG expectations

Investor and lender ESG expectations are shifting capital terms for Lundin Gold, with sustainability covenants increasingly embedded in financing and offtake contracts, affecting pricing and access. Meeting benchmarks helps keep financing costs competitive but raises compliance burdens and reporting obligations. Failure to meet standards empowers buyers and creditors to demand tighter terms or higher premiums. Strong ESG performance can make Lundin a preferred supplier and tilt bargaining power in its favor.

Product differentiation via low costs

Fruta del Norte’s high reserve grade (8.8 g/t) and low AISC (≈$800/oz in 2024) strengthen Lundin Gold’s product differentiation via low costs, lowering pressure to offer concessional terms to buyers. Buyers’ preference for reliable, low‑risk supply and consistent quarterly deliveries (~340 koz 2024 guidance) reduces their leverage over a dependable producer. Hedging flexibility and steady quality further constrain customer bargaining power.

Currency and payment terms

Ecuador has been dollarized since 2000, simplifying USD settlement and removing FX negotiation as a bargaining lever; buyers still may press for tighter payment terms in demand softness. Lundin Gold mitigates this via buyer optionality, competitive cash costs and use of insurance and trade-credit instruments to limit counterparty leverage.

- Dollarized since 2000: USD settlement simplifies contracting

- Buyers push tighter terms in soft markets

- Lundin counters with multiple buyers and low cash costs

- Insurance/credit instruments reduce counterparty risk

High-grade, low-cost producer limits buyer leverage despite concentrated LBMA refiner market

Lundin sells into deep, liquid LBMA markets so spot pricing limits single-buyer control; offtakes and multiple refiners dilute leverage. Concentration among <100 LBMA refiners and ESG-linked finance raise negotiable fees and covenants. High grade (8.8 g/t), low AISC (~$800/oz) and ~340 koz 2024 guidance reduce need for concessional terms.

| Metric | 2024 |

|---|---|

| Grade | 8.8 g/t |

| AISC | ≈$800/oz |

| Guidance | ~340 koz |

| LBMA refiners | <100 |

Same Document Delivered

Lundin Gold Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Lundin Gold you'll receive after purchase—no placeholders. It assesses competitive rivalry, supplier and buyer power, and threats of substitutes and new entrants with concise, data-driven insights. The document is professionally formatted and ready for immediate download.