Lynas Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Lynas's Porter's Five Forces snapshot highlights strong supplier influence for rare-earth feedstock, moderate buyer power from specialized customers, and tangible threats from substitutes and regulatory shifts. This summary teases strategic pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights tailored to Lynas.

Suppliers Bargaining Power

Vertical integration buffers

Lynas sources its ore primarily from the Mount Weld deposit, removing reliance on third-party concentrate suppliers in 2024 and materially lowering supplier leverage over critical feedstock. Vertical integration gives Lynas tighter control over grade, scheduling and unit costs across its value chain. As a result, supplier power in 2024 is concentrated in non-ore inputs such as process chemicals, catalysts and energy.

Critical reagents exposure

Processing depends on sulfuric acid, caustic soda and specialty chemicals whose prices remained cyclical in 2024, and logistics to Mt Weld and Malaysian refining sites can tighten supply and raise landed reagent costs by around 10–15%. These inputs are commoditized and multi-sourced, but shipping delays and plant outages can cause short-term tightness. Price spikes compress margins when rare earth prices soften. Long-term contracts and targeted inventory buffer most exposure.

Specialized equipment/services

Cracking, leaching, solvent extraction and separation at Lynas demand specialized equipment and EPCM expertise concentrated in a small supplier base, constraining alternatives and raising switching costs. Lead times for bespoke units increase vendor leverage during capacity expansions, while standardization of some modules reduces but does not eliminate supplier bargaining power. Supply-chain concentration therefore remains a key strategic risk for processing scale-up.

Energy and logistics costs

High energy intensity and long-haul logistics expose Lynas to utility and freight providers; 2024 Brent averaged about 86 USD/barrel, so fuel and power tariffs feed directly into unit economics and margin pressure.

- Regional provider concentration limits bargaining leverage

- On-site efficiency reduces kWh/ton

- Multi-modal routing lowers freight volatility

Regulatory/license dependence

Permits for mining, processing and waste management act as quasi-supplies for Lynas; regulators set conditions that can quickly change costs and throughput. Compliance burdens for radioactive residues give regulators structural bargaining power over plant licensing and operating margins. Geographic diversification into Australia, Malaysia and the USA (3 jurisdictions as of 2024) reduces single-jurisdiction shutdown risk.

- Permits as supply control

- Regulatory conditions ↔ cost/throughput

- Radioactive-waste rules = structural power

- 3 jurisdictions (2024) lower single-jurisdiction risk

2024 vertical integration cuts ore risk, shifts supplier power to chemicals, energy, freight

Lynas’ 2024 vertical integration via Mount Weld cuts ore supplier leverage, shifting supplier power to chemicals, EPCM vendors, energy and freight; Brent ~86 USD/barrel (2024) and freight volatility (±10–15% landed reagent cost) tighten margins. Regulatory permits across 3 jurisdictions (2024) create structural supplier-like power over throughput. Long lead-times for bespoke processing units raise switching costs during scale-up.

| Item | 2024 metric | Impact |

|---|---|---|

| Ore sourcing | Mount Weld primary | Lower ore supplier power |

| Energy | Brent ~86 USD/bbl | Higher input cost exposure |

| Freight/reagents | ±10–15% landed cost | Margin vulnerability |

| Regulatory | 3 jurisdictions | Structural operating leverage |

What is included in the product

Tailored Porter's Five Forces analysis for Lynas that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats. Ready for inclusion in investor decks, strategy reports, or academic projects.

Clear, one-sheet Five Forces summary tailored to Lynas—instantly highlights supply-chain, regulatory and competitor pressures to speed strategic decisions. Customize force levels or swap data to model post-regulation, new entrants or shifting rare-earth demand for board-ready insights.

Customers Bargaining Power

Concentrated magnet makers

NdPr customers are relatively concentrated among large magnet and alloy producers such as Nidec, Hitachi Metals and Vacuumschmelze, giving buyers scale and negotiation leverage, especially in down cycles. However assured non-China supply remains scarce—China accounted for roughly 85% of rare earth processing in 2024—tempering buyer power. Strategic offtakes and long-term contracts can align interests and stabilize pricing and terms.

High qualification costs

Qualification for automotive and wind applications is lengthy and often spans 12–36 months, with OEMs demanding extensive testing and documentation. Switching suppliers risks performance, reliability and costly re‑certification, reducing buyer leverage once Lynas is qualified. These frictions drive multi‑year supply agreements, commonly 3–5 years, and raise the effective switching cost for customers.

Price transparency, cyclical

Benchmark price visibility lets large buyers time purchases and extract discounts during gluts, with rare earth oxide prices showing volatile swings of over 50% between 2020–24. In downturns buyers gain leverage on volumes and contractual terms, pressuring margins for producers like Lynas. In tight markets, premiums for traceable, ESG-friendly supply can flip bargaining power; China still accounts for roughly 80% of processing capacity (2023), shaping the cycle.

Product differentiation via ESG

Buyers increasingly value provenance, sustainability and regulatory compliance; Lynas’ non-China, regulated rare-earth supply gains priority as OEMs face disclosure rules like the EU CSRD, which expands reporting to about 50,000 companies from 2024. That ESG differentiation shrinks substitutable options and supports premium pricing or take-or-pay contracts for Lynas.

- Non-China supply = strategic advantage

- EU CSRD ~50,000 firms (2024)

- Leads to pricing power / take-or-pay

Government-backed demand

Government-backed defense, EV and renewables policies create strategic demand pools for critical materials. Public funding such as the US Inflation Reduction Act (~369 billion USD) and large defense procurements anchor long-term offtakes, reducing buyer opportunism. Where policy ties require non-China inputs, buyer alternatives shrink and buyer power falls for targeted volumes.

- Defense mandates: secured offtakes

- IRA ~369B USD: anchors demand

- Non-China sourcing rules: fewer alternatives

~85% China processing; IRA 369B anchors longterm offtakes

Customers concentrated among large magnet/alloy makers, giving scale leverage, but non-China supply scarcity (China ~85% processing in 2024) limits buyer power; strategic offtakes and long-term contracts stabilize terms. Qualification for autos/wind (12–36 months) raises switching costs after Lynas is approved. Policy demand and IRA ~369 billion USD (2022–24) anchor offtakes, reducing buyer opportunism.

| Metric | Value | Impact |

|---|---|---|

| China processing | ~85% (2024) | Limits buyer alternatives |

| EU CSRD | ~50,000 firms (2024) | Prioritizes traceable supply |

| IRA funding | ~369B USD | Anchors offtakes |

| Price volatility | >50% (2020–24) | Gives buyers timing leverage |

What You See Is What You Get

Lynas Porter's Five Forces Analysis

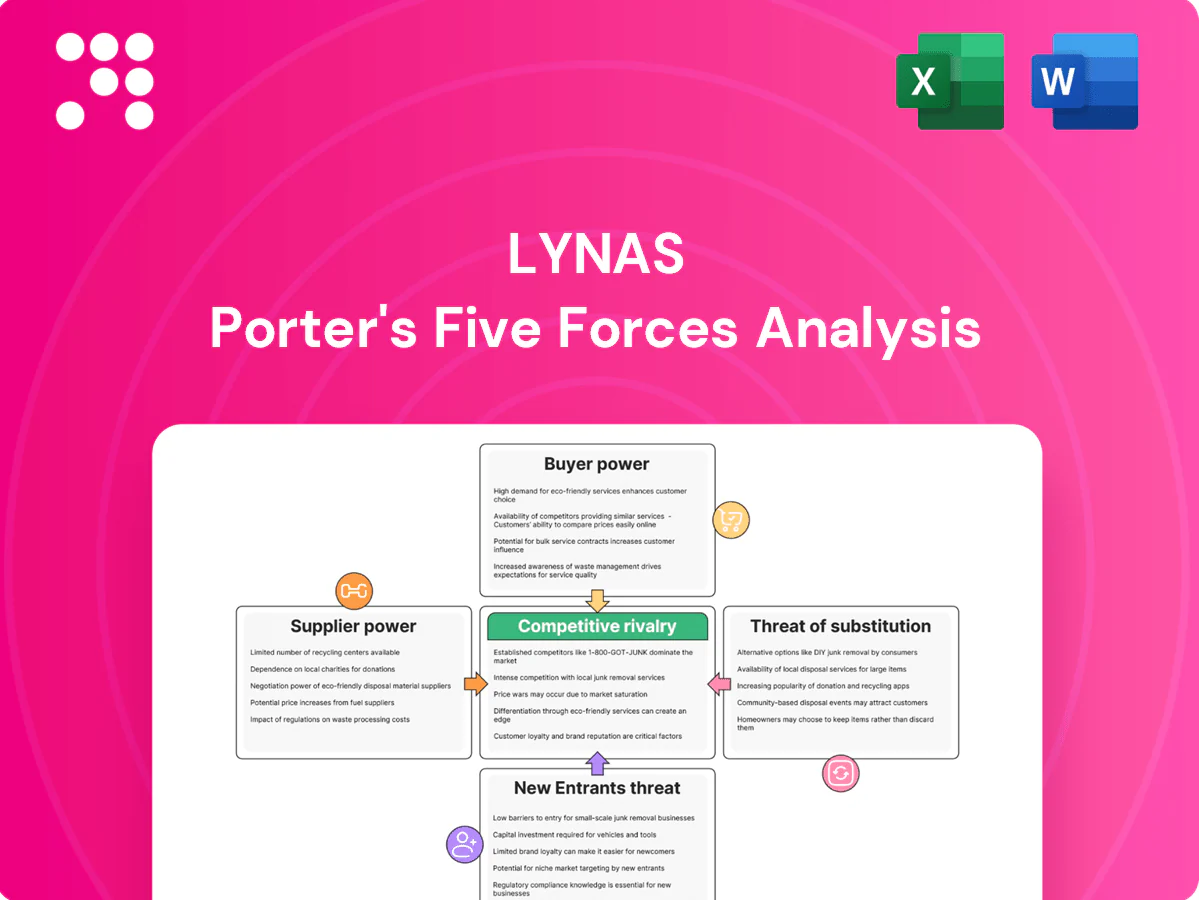

This preview shows the exact Lynas Porter's Five Forces analysis you'll receive—no mockups or placeholders. The document is the final, professionally written file covering supplier power, buyer power, competitive rivalry, threat of substitutes and new entrants. Purchase grants instant access to this ready-to-use report.

Don't Miss the Bigger Picture

Lynas's Porter's Five Forces snapshot highlights strong supplier influence for rare-earth feedstock, moderate buyer power from specialized customers, and tangible threats from substitutes and regulatory shifts. This summary teases strategic pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights tailored to Lynas.

Suppliers Bargaining Power

Vertical integration buffers

Lynas sources its ore primarily from the Mount Weld deposit, removing reliance on third-party concentrate suppliers in 2024 and materially lowering supplier leverage over critical feedstock. Vertical integration gives Lynas tighter control over grade, scheduling and unit costs across its value chain. As a result, supplier power in 2024 is concentrated in non-ore inputs such as process chemicals, catalysts and energy.

Critical reagents exposure

Processing depends on sulfuric acid, caustic soda and specialty chemicals whose prices remained cyclical in 2024, and logistics to Mt Weld and Malaysian refining sites can tighten supply and raise landed reagent costs by around 10–15%. These inputs are commoditized and multi-sourced, but shipping delays and plant outages can cause short-term tightness. Price spikes compress margins when rare earth prices soften. Long-term contracts and targeted inventory buffer most exposure.

Specialized equipment/services

Cracking, leaching, solvent extraction and separation at Lynas demand specialized equipment and EPCM expertise concentrated in a small supplier base, constraining alternatives and raising switching costs. Lead times for bespoke units increase vendor leverage during capacity expansions, while standardization of some modules reduces but does not eliminate supplier bargaining power. Supply-chain concentration therefore remains a key strategic risk for processing scale-up.

Energy and logistics costs

High energy intensity and long-haul logistics expose Lynas to utility and freight providers; 2024 Brent averaged about 86 USD/barrel, so fuel and power tariffs feed directly into unit economics and margin pressure.

- Regional provider concentration limits bargaining leverage

- On-site efficiency reduces kWh/ton

- Multi-modal routing lowers freight volatility

Regulatory/license dependence

Permits for mining, processing and waste management act as quasi-supplies for Lynas; regulators set conditions that can quickly change costs and throughput. Compliance burdens for radioactive residues give regulators structural bargaining power over plant licensing and operating margins. Geographic diversification into Australia, Malaysia and the USA (3 jurisdictions as of 2024) reduces single-jurisdiction shutdown risk.

- Permits as supply control

- Regulatory conditions ↔ cost/throughput

- Radioactive-waste rules = structural power

- 3 jurisdictions (2024) lower single-jurisdiction risk

2024 vertical integration cuts ore risk, shifts supplier power to chemicals, energy, freight

Lynas’ 2024 vertical integration via Mount Weld cuts ore supplier leverage, shifting supplier power to chemicals, EPCM vendors, energy and freight; Brent ~86 USD/barrel (2024) and freight volatility (±10–15% landed reagent cost) tighten margins. Regulatory permits across 3 jurisdictions (2024) create structural supplier-like power over throughput. Long lead-times for bespoke processing units raise switching costs during scale-up.

| Item | 2024 metric | Impact |

|---|---|---|

| Ore sourcing | Mount Weld primary | Lower ore supplier power |

| Energy | Brent ~86 USD/bbl | Higher input cost exposure |

| Freight/reagents | ±10–15% landed cost | Margin vulnerability |

| Regulatory | 3 jurisdictions | Structural operating leverage |

What is included in the product

Tailored Porter's Five Forces analysis for Lynas that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats. Ready for inclusion in investor decks, strategy reports, or academic projects.

Clear, one-sheet Five Forces summary tailored to Lynas—instantly highlights supply-chain, regulatory and competitor pressures to speed strategic decisions. Customize force levels or swap data to model post-regulation, new entrants or shifting rare-earth demand for board-ready insights.

Customers Bargaining Power

Concentrated magnet makers

NdPr customers are relatively concentrated among large magnet and alloy producers such as Nidec, Hitachi Metals and Vacuumschmelze, giving buyers scale and negotiation leverage, especially in down cycles. However assured non-China supply remains scarce—China accounted for roughly 85% of rare earth processing in 2024—tempering buyer power. Strategic offtakes and long-term contracts can align interests and stabilize pricing and terms.

High qualification costs

Qualification for automotive and wind applications is lengthy and often spans 12–36 months, with OEMs demanding extensive testing and documentation. Switching suppliers risks performance, reliability and costly re‑certification, reducing buyer leverage once Lynas is qualified. These frictions drive multi‑year supply agreements, commonly 3–5 years, and raise the effective switching cost for customers.

Price transparency, cyclical

Benchmark price visibility lets large buyers time purchases and extract discounts during gluts, with rare earth oxide prices showing volatile swings of over 50% between 2020–24. In downturns buyers gain leverage on volumes and contractual terms, pressuring margins for producers like Lynas. In tight markets, premiums for traceable, ESG-friendly supply can flip bargaining power; China still accounts for roughly 80% of processing capacity (2023), shaping the cycle.

Product differentiation via ESG

Buyers increasingly value provenance, sustainability and regulatory compliance; Lynas’ non-China, regulated rare-earth supply gains priority as OEMs face disclosure rules like the EU CSRD, which expands reporting to about 50,000 companies from 2024. That ESG differentiation shrinks substitutable options and supports premium pricing or take-or-pay contracts for Lynas.

- Non-China supply = strategic advantage

- EU CSRD ~50,000 firms (2024)

- Leads to pricing power / take-or-pay

Government-backed demand

Government-backed defense, EV and renewables policies create strategic demand pools for critical materials. Public funding such as the US Inflation Reduction Act (~369 billion USD) and large defense procurements anchor long-term offtakes, reducing buyer opportunism. Where policy ties require non-China inputs, buyer alternatives shrink and buyer power falls for targeted volumes.

- Defense mandates: secured offtakes

- IRA ~369B USD: anchors demand

- Non-China sourcing rules: fewer alternatives

~85% China processing; IRA 369B anchors longterm offtakes

Customers concentrated among large magnet/alloy makers, giving scale leverage, but non-China supply scarcity (China ~85% processing in 2024) limits buyer power; strategic offtakes and long-term contracts stabilize terms. Qualification for autos/wind (12–36 months) raises switching costs after Lynas is approved. Policy demand and IRA ~369 billion USD (2022–24) anchor offtakes, reducing buyer opportunism.

| Metric | Value | Impact |

|---|---|---|

| China processing | ~85% (2024) | Limits buyer alternatives |

| EU CSRD | ~50,000 firms (2024) | Prioritizes traceable supply |

| IRA funding | ~369B USD | Anchors offtakes |

| Price volatility | >50% (2020–24) | Gives buyers timing leverage |

What You See Is What You Get

Lynas Porter's Five Forces Analysis

This preview shows the exact Lynas Porter's Five Forces analysis you'll receive—no mockups or placeholders. The document is the final, professionally written file covering supplier power, buyer power, competitive rivalry, threat of substitutes and new entrants. Purchase grants instant access to this ready-to-use report.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Lynas's Porter's Five Forces snapshot highlights strong supplier influence for rare-earth feedstock, moderate buyer power from specialized customers, and tangible threats from substitutes and regulatory shifts. This summary teases strategic pressures but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights tailored to Lynas.

Suppliers Bargaining Power

Vertical integration buffers

Lynas sources its ore primarily from the Mount Weld deposit, removing reliance on third-party concentrate suppliers in 2024 and materially lowering supplier leverage over critical feedstock. Vertical integration gives Lynas tighter control over grade, scheduling and unit costs across its value chain. As a result, supplier power in 2024 is concentrated in non-ore inputs such as process chemicals, catalysts and energy.

Critical reagents exposure

Processing depends on sulfuric acid, caustic soda and specialty chemicals whose prices remained cyclical in 2024, and logistics to Mt Weld and Malaysian refining sites can tighten supply and raise landed reagent costs by around 10–15%. These inputs are commoditized and multi-sourced, but shipping delays and plant outages can cause short-term tightness. Price spikes compress margins when rare earth prices soften. Long-term contracts and targeted inventory buffer most exposure.

Specialized equipment/services

Cracking, leaching, solvent extraction and separation at Lynas demand specialized equipment and EPCM expertise concentrated in a small supplier base, constraining alternatives and raising switching costs. Lead times for bespoke units increase vendor leverage during capacity expansions, while standardization of some modules reduces but does not eliminate supplier bargaining power. Supply-chain concentration therefore remains a key strategic risk for processing scale-up.

Energy and logistics costs

High energy intensity and long-haul logistics expose Lynas to utility and freight providers; 2024 Brent averaged about 86 USD/barrel, so fuel and power tariffs feed directly into unit economics and margin pressure.

- Regional provider concentration limits bargaining leverage

- On-site efficiency reduces kWh/ton

- Multi-modal routing lowers freight volatility

Regulatory/license dependence

Permits for mining, processing and waste management act as quasi-supplies for Lynas; regulators set conditions that can quickly change costs and throughput. Compliance burdens for radioactive residues give regulators structural bargaining power over plant licensing and operating margins. Geographic diversification into Australia, Malaysia and the USA (3 jurisdictions as of 2024) reduces single-jurisdiction shutdown risk.

- Permits as supply control

- Regulatory conditions ↔ cost/throughput

- Radioactive-waste rules = structural power

- 3 jurisdictions (2024) lower single-jurisdiction risk

2024 vertical integration cuts ore risk, shifts supplier power to chemicals, energy, freight

Lynas’ 2024 vertical integration via Mount Weld cuts ore supplier leverage, shifting supplier power to chemicals, EPCM vendors, energy and freight; Brent ~86 USD/barrel (2024) and freight volatility (±10–15% landed reagent cost) tighten margins. Regulatory permits across 3 jurisdictions (2024) create structural supplier-like power over throughput. Long lead-times for bespoke processing units raise switching costs during scale-up.

| Item | 2024 metric | Impact |

|---|---|---|

| Ore sourcing | Mount Weld primary | Lower ore supplier power |

| Energy | Brent ~86 USD/bbl | Higher input cost exposure |

| Freight/reagents | ±10–15% landed cost | Margin vulnerability |

| Regulatory | 3 jurisdictions | Structural operating leverage |

What is included in the product

Tailored Porter's Five Forces analysis for Lynas that uncovers competitive drivers, supplier and buyer power, entry barriers, substitutes, and emerging threats. Ready for inclusion in investor decks, strategy reports, or academic projects.

Clear, one-sheet Five Forces summary tailored to Lynas—instantly highlights supply-chain, regulatory and competitor pressures to speed strategic decisions. Customize force levels or swap data to model post-regulation, new entrants or shifting rare-earth demand for board-ready insights.

Customers Bargaining Power

Concentrated magnet makers

NdPr customers are relatively concentrated among large magnet and alloy producers such as Nidec, Hitachi Metals and Vacuumschmelze, giving buyers scale and negotiation leverage, especially in down cycles. However assured non-China supply remains scarce—China accounted for roughly 85% of rare earth processing in 2024—tempering buyer power. Strategic offtakes and long-term contracts can align interests and stabilize pricing and terms.

High qualification costs

Qualification for automotive and wind applications is lengthy and often spans 12–36 months, with OEMs demanding extensive testing and documentation. Switching suppliers risks performance, reliability and costly re‑certification, reducing buyer leverage once Lynas is qualified. These frictions drive multi‑year supply agreements, commonly 3–5 years, and raise the effective switching cost for customers.

Price transparency, cyclical

Benchmark price visibility lets large buyers time purchases and extract discounts during gluts, with rare earth oxide prices showing volatile swings of over 50% between 2020–24. In downturns buyers gain leverage on volumes and contractual terms, pressuring margins for producers like Lynas. In tight markets, premiums for traceable, ESG-friendly supply can flip bargaining power; China still accounts for roughly 80% of processing capacity (2023), shaping the cycle.

Product differentiation via ESG

Buyers increasingly value provenance, sustainability and regulatory compliance; Lynas’ non-China, regulated rare-earth supply gains priority as OEMs face disclosure rules like the EU CSRD, which expands reporting to about 50,000 companies from 2024. That ESG differentiation shrinks substitutable options and supports premium pricing or take-or-pay contracts for Lynas.

- Non-China supply = strategic advantage

- EU CSRD ~50,000 firms (2024)

- Leads to pricing power / take-or-pay

Government-backed demand

Government-backed defense, EV and renewables policies create strategic demand pools for critical materials. Public funding such as the US Inflation Reduction Act (~369 billion USD) and large defense procurements anchor long-term offtakes, reducing buyer opportunism. Where policy ties require non-China inputs, buyer alternatives shrink and buyer power falls for targeted volumes.

- Defense mandates: secured offtakes

- IRA ~369B USD: anchors demand

- Non-China sourcing rules: fewer alternatives

~85% China processing; IRA 369B anchors longterm offtakes

Customers concentrated among large magnet/alloy makers, giving scale leverage, but non-China supply scarcity (China ~85% processing in 2024) limits buyer power; strategic offtakes and long-term contracts stabilize terms. Qualification for autos/wind (12–36 months) raises switching costs after Lynas is approved. Policy demand and IRA ~369 billion USD (2022–24) anchor offtakes, reducing buyer opportunism.

| Metric | Value | Impact |

|---|---|---|

| China processing | ~85% (2024) | Limits buyer alternatives |

| EU CSRD | ~50,000 firms (2024) | Prioritizes traceable supply |

| IRA funding | ~369B USD | Anchors offtakes |

| Price volatility | >50% (2020–24) | Gives buyers timing leverage |

What You See Is What You Get

Lynas Porter's Five Forces Analysis

This preview shows the exact Lynas Porter's Five Forces analysis you'll receive—no mockups or placeholders. The document is the final, professionally written file covering supplier power, buyer power, competitive rivalry, threat of substitutes and new entrants. Purchase grants instant access to this ready-to-use report.