Macromill PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Macromill PESTLE analysis—three concise sections reveal how political shifts, economic trends, and technology disruption shape performance. Ideal for investors and strategists, it turns external risk into actionable opportunity. Purchase the full report to access the complete, editable insights now.

Political factors

Data sovereignty and localization

Governments are tightening rules on where citizen data can be stored and processed, notably GDPR across 27 EU member states and China’s 2021 Data Security and Personal Information Protection laws requiring local handling for sensitive data. Divergent localization mandates complicate cross-border panel operations and analytics delivery. Macromill may need regional data lakes and modular architectures to stay compliant, raising IT and compliance costs but serving as a trust differentiator with regulated clients.

Geopolitical risk and market access

Sanctions, trade tensions, and export controls can limit Macromill’s access to survey tools, analytics partners, and client sectors, forcing shifts in vendor relationships and pricing models. Political instability in client markets disrupts fieldwork, panel recruitment, and on-the-ground research, increasing project delays and operational costs. Macromill must diversify country exposure, develop contingency sourcing and scenario plans to mitigate revenue concentration and delivery risks.

Public-sector digital agendas

Government funding for digital transformation and AI—notably the EU Recovery and Resilience Facility of €723.8bn—boosts demand for evidence-based insights and analytics. Public tenders increasingly mandate stringent data security and ethical AI standards, reflecting procurement rules that cover roughly 12% of EU GDP. Winning framework agreements can unlock multi-year pipelines and aligning offerings with national digital priorities builds credibility and scale.

Advertising and platform policy shifts

Political scrutiny of big tech, notably EU Digital Markets Act enforcement from March 2024 and prior Apple ATT (2021), has tightened data access and platform measurement APIs, constraining deterministic identifiers.

Platform policy shifts cascade into targeting and attribution, forcing publishers and vendors like Macromill to adopt probabilistic measurement and privacy-preserving APIs to avoid signal loss.

Macromill must develop adaptive methodologies and strategic partnerships for early compliant access to measurement solutions to mitigate revenue and accuracy impacts.

- DMA enforcement: March 2024

- Apple ATT: 2021

- Ad measurement: shift to probabilistic/PPC-resilient methods

- Strategy: secure partnerships for early API access

Tax regimes and incentives

Changes in corporate tax and introduction of digital services taxes (commonly 2–3%) directly compress margins; US federal rate remains 21% while Japan's combined statutory rate is about 30.62% and OECD average ~23%. R&D tax credits routinely cut effective tax by several percentage points, and AI R&D incentives (grants/credits) can subsidize analytics development. Vigilant cross-border compliance avoids fines and reputational damage.

- Tax rates: US 21%, Japan ~30.62%, OECD avg ~23%

- DSTs: typical 2–3% on digital revenue

- R&D credits: reduce effective tax by several ppts

- Optimize entities across JP/EU/US to lower ETR

- AI R&D incentives fund analytics; strict compliance required

Regulatory fragmentation and platform rules raise data, IT and tax costs globally

Regulatory fragmentation (GDPR; China PIPL/DSL) forces regional data stacks and raises IT/compliance costs. Platform rules (DMA enforcement Mar 2024; Apple ATT 2021) reduce deterministic measurement, pushing probabilistic/privacy-preserving methods. Trade sanctions and instability increase fieldwork/delivery risk; diversify country exposure. Tax/DSTs (US 21%, Japan ~30.62%, DSTs 2–3%) compress margins but R&D/AI credits partially offset costs.

| Issue | Stat | Impact |

|---|---|---|

| EU Recovery | €723.8bn | Boosts analytics demand |

| DMA/ATT | Mar 2024 / 2021 | Limits deterministic IDs |

| Tax/DST | US21% JP30.62% DST2–3% | Margin pressure |

What is included in the product

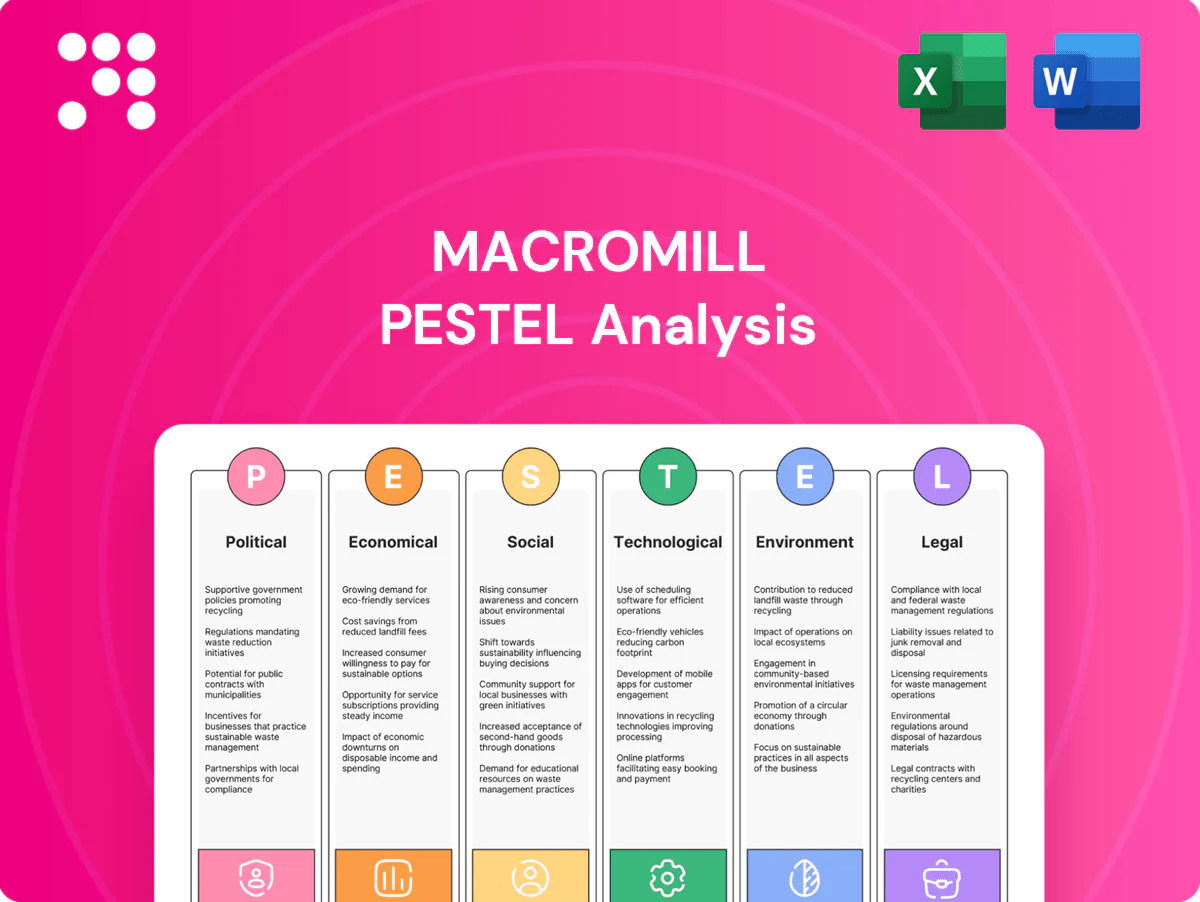

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Macromill’s market research and insights business, with data-backed trends and region-specific context. Designed for executives and investors to identify threats, opportunities and actionable scenarios.

Macromill's PESTLE analysis condenses complex external factors into a clean, visually segmented summary for quick reference in meetings or presentations, and is easily editable for regional or business-line notes to support strategic discussions and client reports.

Economic factors

Marketing spend cyclicality

Insights budgets track GDP and ad-spend cycles: IMF data show global GDP fell 3.4% in 2020 then rose ~6.0% in 2021, driving sharp ad‑spend cuts and recoveries that compress research budgets in downturns. Clients cut discretionary research and elongate sales cycles in slowdowns. Counter‑cyclical, ROI‑focused offerings help defend wallet share, while diversifying into compliance and product analytics reduces revenue volatility.

Currency and cost pressures

Revenue and costs in multiple currencies expose Macromill to FX swings as USD/JPY traded near 155 in 2024–2025, amplifying dollar-priced cloud and software spend. A weak yen inflates import bills, making active hedging essential. Wage inflation for data talent (roughly mid-single digits in 2024) pressures margins, so pricing must enable cost pass-through while reflecting delivered value.

Client mix and vertical exposure

Resilience hinges on Macromill's balance across CPG, tech, finance, healthcare and public-sector clients; heavy exposure to ad-sensitive CPG and tech amplifies revenue volatility during advertising slowdowns.

Shifting mix toward regulated sectors and recurring insights services—medical, financial compliance, subscription panels—raises revenue stickiness and margin predictability.

Account-based expansion reduces acquisition costs and churn, improving lifetime value and smoothing quarter-to-quarter performance.

Digital transformation demand

Demand for digital transformation keeps Macromill's analytics services resilient as firms prioritize data-driven decisions; Gartner 2024 estimates the data and analytics market near $260 billion, supporting sustained spend. Products that link insights to commercial outcomes command premium pricing, while embedded dashboards boost client stickiness and outcome-based contracts align fees with measurable impact.

- data-driven adoption: sustained enterprise spend (Gartner 2024)

- premium pricing: outcome-linked insights

- stickiness: embedded dashboards

- contracts: fees tied to measurable impact

M&A and consolidation dynamics

Research and martech industries continue consolidating, creating larger, scale competitors that pressure pricing and innovation for firms like Macromill. Selective acquisitions can add panels, new geographies, or proprietary tech IP, but integration discipline is essential to realize cost and revenue synergies while protecting panel quality and data integrity. Joint ventures offer a faster, lower‑risk route to enter markets and access local panels without full ownership.

- Tags: M&A

- Tags: consolidation

- Tags: integration discipline

- Tags: panel quality

- Tags: joint ventures

Regulatory fragmentation and platform rules raise data, IT and tax costs globally

Economic cycles drive insights budgets: global GDP fell 3.4% in 2020 then rose ~6.0% in 2021, compressing research spend in downturns. FX volatility (USD/JPY ~155 in 2024–25) and mid-single-digit 2024 wage inflation pressure margins. Shift to recurring, regulated services increases revenue stickiness.

| Metric | Value |

|---|---|

| Global GDP rebound | ~+6.0% (2021) |

| USD/JPY | ~155 (2024–25) |

| Data & analytics market | $260B (Gartner 2024) |

| Wage inflation | ~4–6% (2024) |

What You See Is What You Get

Macromill PESTLE Analysis

The Macromill PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the same content, layout, and insights visible now, with no placeholders or edits required. After payment you’ll instantly download this finished file.

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Macromill PESTLE analysis—three concise sections reveal how political shifts, economic trends, and technology disruption shape performance. Ideal for investors and strategists, it turns external risk into actionable opportunity. Purchase the full report to access the complete, editable insights now.

Political factors

Data sovereignty and localization

Governments are tightening rules on where citizen data can be stored and processed, notably GDPR across 27 EU member states and China’s 2021 Data Security and Personal Information Protection laws requiring local handling for sensitive data. Divergent localization mandates complicate cross-border panel operations and analytics delivery. Macromill may need regional data lakes and modular architectures to stay compliant, raising IT and compliance costs but serving as a trust differentiator with regulated clients.

Geopolitical risk and market access

Sanctions, trade tensions, and export controls can limit Macromill’s access to survey tools, analytics partners, and client sectors, forcing shifts in vendor relationships and pricing models. Political instability in client markets disrupts fieldwork, panel recruitment, and on-the-ground research, increasing project delays and operational costs. Macromill must diversify country exposure, develop contingency sourcing and scenario plans to mitigate revenue concentration and delivery risks.

Public-sector digital agendas

Government funding for digital transformation and AI—notably the EU Recovery and Resilience Facility of €723.8bn—boosts demand for evidence-based insights and analytics. Public tenders increasingly mandate stringent data security and ethical AI standards, reflecting procurement rules that cover roughly 12% of EU GDP. Winning framework agreements can unlock multi-year pipelines and aligning offerings with national digital priorities builds credibility and scale.

Advertising and platform policy shifts

Political scrutiny of big tech, notably EU Digital Markets Act enforcement from March 2024 and prior Apple ATT (2021), has tightened data access and platform measurement APIs, constraining deterministic identifiers.

Platform policy shifts cascade into targeting and attribution, forcing publishers and vendors like Macromill to adopt probabilistic measurement and privacy-preserving APIs to avoid signal loss.

Macromill must develop adaptive methodologies and strategic partnerships for early compliant access to measurement solutions to mitigate revenue and accuracy impacts.

- DMA enforcement: March 2024

- Apple ATT: 2021

- Ad measurement: shift to probabilistic/PPC-resilient methods

- Strategy: secure partnerships for early API access

Tax regimes and incentives

Changes in corporate tax and introduction of digital services taxes (commonly 2–3%) directly compress margins; US federal rate remains 21% while Japan's combined statutory rate is about 30.62% and OECD average ~23%. R&D tax credits routinely cut effective tax by several percentage points, and AI R&D incentives (grants/credits) can subsidize analytics development. Vigilant cross-border compliance avoids fines and reputational damage.

- Tax rates: US 21%, Japan ~30.62%, OECD avg ~23%

- DSTs: typical 2–3% on digital revenue

- R&D credits: reduce effective tax by several ppts

- Optimize entities across JP/EU/US to lower ETR

- AI R&D incentives fund analytics; strict compliance required

Regulatory fragmentation and platform rules raise data, IT and tax costs globally

Regulatory fragmentation (GDPR; China PIPL/DSL) forces regional data stacks and raises IT/compliance costs. Platform rules (DMA enforcement Mar 2024; Apple ATT 2021) reduce deterministic measurement, pushing probabilistic/privacy-preserving methods. Trade sanctions and instability increase fieldwork/delivery risk; diversify country exposure. Tax/DSTs (US 21%, Japan ~30.62%, DSTs 2–3%) compress margins but R&D/AI credits partially offset costs.

| Issue | Stat | Impact |

|---|---|---|

| EU Recovery | €723.8bn | Boosts analytics demand |

| DMA/ATT | Mar 2024 / 2021 | Limits deterministic IDs |

| Tax/DST | US21% JP30.62% DST2–3% | Margin pressure |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Macromill’s market research and insights business, with data-backed trends and region-specific context. Designed for executives and investors to identify threats, opportunities and actionable scenarios.

Macromill's PESTLE analysis condenses complex external factors into a clean, visually segmented summary for quick reference in meetings or presentations, and is easily editable for regional or business-line notes to support strategic discussions and client reports.

Economic factors

Marketing spend cyclicality

Insights budgets track GDP and ad-spend cycles: IMF data show global GDP fell 3.4% in 2020 then rose ~6.0% in 2021, driving sharp ad‑spend cuts and recoveries that compress research budgets in downturns. Clients cut discretionary research and elongate sales cycles in slowdowns. Counter‑cyclical, ROI‑focused offerings help defend wallet share, while diversifying into compliance and product analytics reduces revenue volatility.

Currency and cost pressures

Revenue and costs in multiple currencies expose Macromill to FX swings as USD/JPY traded near 155 in 2024–2025, amplifying dollar-priced cloud and software spend. A weak yen inflates import bills, making active hedging essential. Wage inflation for data talent (roughly mid-single digits in 2024) pressures margins, so pricing must enable cost pass-through while reflecting delivered value.

Client mix and vertical exposure

Resilience hinges on Macromill's balance across CPG, tech, finance, healthcare and public-sector clients; heavy exposure to ad-sensitive CPG and tech amplifies revenue volatility during advertising slowdowns.

Shifting mix toward regulated sectors and recurring insights services—medical, financial compliance, subscription panels—raises revenue stickiness and margin predictability.

Account-based expansion reduces acquisition costs and churn, improving lifetime value and smoothing quarter-to-quarter performance.

Digital transformation demand

Demand for digital transformation keeps Macromill's analytics services resilient as firms prioritize data-driven decisions; Gartner 2024 estimates the data and analytics market near $260 billion, supporting sustained spend. Products that link insights to commercial outcomes command premium pricing, while embedded dashboards boost client stickiness and outcome-based contracts align fees with measurable impact.

- data-driven adoption: sustained enterprise spend (Gartner 2024)

- premium pricing: outcome-linked insights

- stickiness: embedded dashboards

- contracts: fees tied to measurable impact

M&A and consolidation dynamics

Research and martech industries continue consolidating, creating larger, scale competitors that pressure pricing and innovation for firms like Macromill. Selective acquisitions can add panels, new geographies, or proprietary tech IP, but integration discipline is essential to realize cost and revenue synergies while protecting panel quality and data integrity. Joint ventures offer a faster, lower‑risk route to enter markets and access local panels without full ownership.

- Tags: M&A

- Tags: consolidation

- Tags: integration discipline

- Tags: panel quality

- Tags: joint ventures

Regulatory fragmentation and platform rules raise data, IT and tax costs globally

Economic cycles drive insights budgets: global GDP fell 3.4% in 2020 then rose ~6.0% in 2021, compressing research spend in downturns. FX volatility (USD/JPY ~155 in 2024–25) and mid-single-digit 2024 wage inflation pressure margins. Shift to recurring, regulated services increases revenue stickiness.

| Metric | Value |

|---|---|

| Global GDP rebound | ~+6.0% (2021) |

| USD/JPY | ~155 (2024–25) |

| Data & analytics market | $260B (Gartner 2024) |

| Wage inflation | ~4–6% (2024) |

What You See Is What You Get

Macromill PESTLE Analysis

The Macromill PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the same content, layout, and insights visible now, with no placeholders or edits required. After payment you’ll instantly download this finished file.

Original: $10.00

-65%$10.00

$3.50Description

Your Shortcut to Market Insight Starts Here

Unlock strategic clarity with our Macromill PESTLE analysis—three concise sections reveal how political shifts, economic trends, and technology disruption shape performance. Ideal for investors and strategists, it turns external risk into actionable opportunity. Purchase the full report to access the complete, editable insights now.

Political factors

Data sovereignty and localization

Governments are tightening rules on where citizen data can be stored and processed, notably GDPR across 27 EU member states and China’s 2021 Data Security and Personal Information Protection laws requiring local handling for sensitive data. Divergent localization mandates complicate cross-border panel operations and analytics delivery. Macromill may need regional data lakes and modular architectures to stay compliant, raising IT and compliance costs but serving as a trust differentiator with regulated clients.

Geopolitical risk and market access

Sanctions, trade tensions, and export controls can limit Macromill’s access to survey tools, analytics partners, and client sectors, forcing shifts in vendor relationships and pricing models. Political instability in client markets disrupts fieldwork, panel recruitment, and on-the-ground research, increasing project delays and operational costs. Macromill must diversify country exposure, develop contingency sourcing and scenario plans to mitigate revenue concentration and delivery risks.

Public-sector digital agendas

Government funding for digital transformation and AI—notably the EU Recovery and Resilience Facility of €723.8bn—boosts demand for evidence-based insights and analytics. Public tenders increasingly mandate stringent data security and ethical AI standards, reflecting procurement rules that cover roughly 12% of EU GDP. Winning framework agreements can unlock multi-year pipelines and aligning offerings with national digital priorities builds credibility and scale.

Advertising and platform policy shifts

Political scrutiny of big tech, notably EU Digital Markets Act enforcement from March 2024 and prior Apple ATT (2021), has tightened data access and platform measurement APIs, constraining deterministic identifiers.

Platform policy shifts cascade into targeting and attribution, forcing publishers and vendors like Macromill to adopt probabilistic measurement and privacy-preserving APIs to avoid signal loss.

Macromill must develop adaptive methodologies and strategic partnerships for early compliant access to measurement solutions to mitigate revenue and accuracy impacts.

- DMA enforcement: March 2024

- Apple ATT: 2021

- Ad measurement: shift to probabilistic/PPC-resilient methods

- Strategy: secure partnerships for early API access

Tax regimes and incentives

Changes in corporate tax and introduction of digital services taxes (commonly 2–3%) directly compress margins; US federal rate remains 21% while Japan's combined statutory rate is about 30.62% and OECD average ~23%. R&D tax credits routinely cut effective tax by several percentage points, and AI R&D incentives (grants/credits) can subsidize analytics development. Vigilant cross-border compliance avoids fines and reputational damage.

- Tax rates: US 21%, Japan ~30.62%, OECD avg ~23%

- DSTs: typical 2–3% on digital revenue

- R&D credits: reduce effective tax by several ppts

- Optimize entities across JP/EU/US to lower ETR

- AI R&D incentives fund analytics; strict compliance required

Regulatory fragmentation and platform rules raise data, IT and tax costs globally

Regulatory fragmentation (GDPR; China PIPL/DSL) forces regional data stacks and raises IT/compliance costs. Platform rules (DMA enforcement Mar 2024; Apple ATT 2021) reduce deterministic measurement, pushing probabilistic/privacy-preserving methods. Trade sanctions and instability increase fieldwork/delivery risk; diversify country exposure. Tax/DSTs (US 21%, Japan ~30.62%, DSTs 2–3%) compress margins but R&D/AI credits partially offset costs.

| Issue | Stat | Impact |

|---|---|---|

| EU Recovery | €723.8bn | Boosts analytics demand |

| DMA/ATT | Mar 2024 / 2021 | Limits deterministic IDs |

| Tax/DST | US21% JP30.62% DST2–3% | Margin pressure |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Macromill’s market research and insights business, with data-backed trends and region-specific context. Designed for executives and investors to identify threats, opportunities and actionable scenarios.

Macromill's PESTLE analysis condenses complex external factors into a clean, visually segmented summary for quick reference in meetings or presentations, and is easily editable for regional or business-line notes to support strategic discussions and client reports.

Economic factors

Marketing spend cyclicality

Insights budgets track GDP and ad-spend cycles: IMF data show global GDP fell 3.4% in 2020 then rose ~6.0% in 2021, driving sharp ad‑spend cuts and recoveries that compress research budgets in downturns. Clients cut discretionary research and elongate sales cycles in slowdowns. Counter‑cyclical, ROI‑focused offerings help defend wallet share, while diversifying into compliance and product analytics reduces revenue volatility.

Currency and cost pressures

Revenue and costs in multiple currencies expose Macromill to FX swings as USD/JPY traded near 155 in 2024–2025, amplifying dollar-priced cloud and software spend. A weak yen inflates import bills, making active hedging essential. Wage inflation for data talent (roughly mid-single digits in 2024) pressures margins, so pricing must enable cost pass-through while reflecting delivered value.

Client mix and vertical exposure

Resilience hinges on Macromill's balance across CPG, tech, finance, healthcare and public-sector clients; heavy exposure to ad-sensitive CPG and tech amplifies revenue volatility during advertising slowdowns.

Shifting mix toward regulated sectors and recurring insights services—medical, financial compliance, subscription panels—raises revenue stickiness and margin predictability.

Account-based expansion reduces acquisition costs and churn, improving lifetime value and smoothing quarter-to-quarter performance.

Digital transformation demand

Demand for digital transformation keeps Macromill's analytics services resilient as firms prioritize data-driven decisions; Gartner 2024 estimates the data and analytics market near $260 billion, supporting sustained spend. Products that link insights to commercial outcomes command premium pricing, while embedded dashboards boost client stickiness and outcome-based contracts align fees with measurable impact.

- data-driven adoption: sustained enterprise spend (Gartner 2024)

- premium pricing: outcome-linked insights

- stickiness: embedded dashboards

- contracts: fees tied to measurable impact

M&A and consolidation dynamics

Research and martech industries continue consolidating, creating larger, scale competitors that pressure pricing and innovation for firms like Macromill. Selective acquisitions can add panels, new geographies, or proprietary tech IP, but integration discipline is essential to realize cost and revenue synergies while protecting panel quality and data integrity. Joint ventures offer a faster, lower‑risk route to enter markets and access local panels without full ownership.

- Tags: M&A

- Tags: consolidation

- Tags: integration discipline

- Tags: panel quality

- Tags: joint ventures

Regulatory fragmentation and platform rules raise data, IT and tax costs globally

Economic cycles drive insights budgets: global GDP fell 3.4% in 2020 then rose ~6.0% in 2021, compressing research spend in downturns. FX volatility (USD/JPY ~155 in 2024–25) and mid-single-digit 2024 wage inflation pressure margins. Shift to recurring, regulated services increases revenue stickiness.

| Metric | Value |

|---|---|

| Global GDP rebound | ~+6.0% (2021) |

| USD/JPY | ~155 (2024–25) |

| Data & analytics market | $260B (Gartner 2024) |

| Wage inflation | ~4–6% (2024) |

What You See Is What You Get

Macromill PESTLE Analysis

The Macromill PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted, professionally structured, and ready to use. It contains the same content, layout, and insights visible now, with no placeholders or edits required. After payment you’ll instantly download this finished file.