Macy's PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

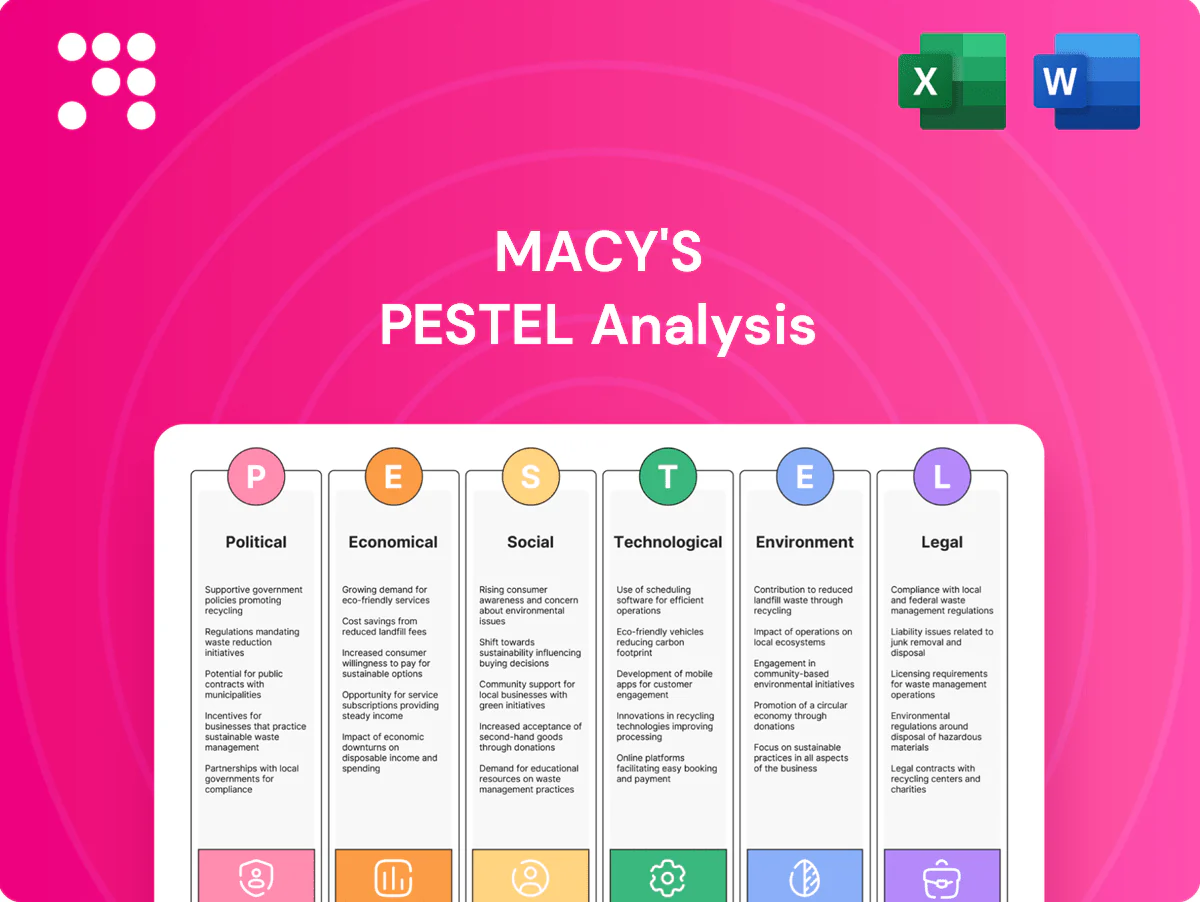

Discover how political, economic, social, technological, legal and environmental forces are reshaping Macy's competitive landscape. Our PESTLE highlights regulatory risks, consumer trends and digital disruption in actionable detail. Ideal for investors and strategists—buy the full report to download editable, ready-to-use insights now.

Political factors

Trade and tariff volatility

Shifts in U.S.–China and other trade policies can raise landed costs for apparel, accessories and home goods Macy’s sources globally; tariffs enacted since 2018 cover roughly $370 billion of Chinese goods. Tariff hikes compress margins or force price rises that risk demand for Macy’s roughly $24.5 billion FY2023 sales. Diversifying sourcing and stronger vendor terms are critical mitigations, alongside close monitoring of trade agreements and port policy.

Labor policy and minimum wage shifts

Changes to federal and state minimum wages (federal floor $7.25) and rising state/local rates—with many jurisdictions at or above $15—directly lift store and distribution center labor costs across Macy’s ~450 stores and roughly 68,000 employees. Overtime rule shifts and union activity reduce staffing flexibility during holiday spikes, pressuring margins. Macy’s must accelerate workforce-management tech and productivity programs and use scenario planning to protect service levels and margins.

Tax incentives and retail revitalization

Local tax incentives, zoning shifts, and urban revitalization programs materially affect economics of Macy’s roughly 550-store footprint, lowering remodel costs through tools like tax increment financing that can cover up to 30% of redevelopment expenses. Policy support for downtown recovery—foot-traffic rebounds of about 15% year-over-year in many U.S. downtowns in 2024—increases visit rates and improves lease leverage. Conversely, municipal budget shortfalls can cut incentive pools or raise property taxes; Macy’s can partner with civic leaders to align store investment with community development priorities.

Public safety and urban policy

Rising metro crime and enforcement shifts drive higher shrink, security spend, and weaker shopper sentiment; 2023–24 retail surveys show organized retail crime (ORC) cited by about 80% of retailers as a major concern, prompting coordinated retailer–law enforcement initiatives and new ORC statutes that materially reduce losses. Enhanced protocols raise operating costs and must preserve customer experience; policy advocacy remains key to lowering ORC risk.

- 80% retailers cite ORC

- Coordinated law-enforcement reduces shrink

- Security spend up; experience trade-offs

- Policy advocacy lowers organized-crime exposure

Geopolitical supply chain risks

Conflicts, sanctions and shipping-route disruptions can delay Macy's inventory flow and raise freight costs, prompting shifts to nearshore sourcing that reduce exposure but require vendor development and longer onboarding. Macy's needs multi-node logistics, inventory buffers for peak seasons and political risk insurance alongside scenario playbooks to maintain assortment and margin stability.

- Multi-node logistics

- Nearshore vendor development

- Inventory buffers for peaks

- Political risk insurance

- Scenario playbooks

Tariffs on $370B imports, labor & ORC squeeze $24.5B retailer

Tariff exposure (tariffs on ~$370B Chinese goods) risks margins on Macy’s ~$24.5B FY2023 sales. Labor cost pressure from ~68,000 employees across ~450 stores and rising state/local wages compresses margins. ORC cited by ~80% of retailers raises security spend and shrink, forcing capital and policy responses.

| Issue | Metric | Near-term Impact |

|---|---|---|

| Tariffs | $370B scope / $24.5B sales | Margin pressure |

| Labor | 68,000 employees / ~450 stores | Higher Opex |

| ORC | 80% retailers | Shrink↑, security spend↑ |

What is included in the product

Explores how macro-environmental factors uniquely affect Macy's across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and forward-looking scenarios specific to the U.S. retail sector to support executives, consultants and investors in strategy and risk planning.

A clean, summarized Macy's PESTLE analysis for easy reference in meetings or presentations. Visually segmented by PESTLE categories and editable so teams can add region- or business-line specific notes for quick alignment and decision-making.

Economic factors

Consumer confidence and discretionary spend

Macroeconomic sentiment drives demand for apparel, beauty and home categories; with U.S. unemployment near 3.6% in mid‑2024 (BLS), stronger labor markets and wealth effects lift premium and occasion purchases. Weak confidence shifts baskets to promotions and essentials, pressuring AUR and gross margin. Macy’s must flex pricing, marketing cadence and assortment depth to protect share and margin.

Inflation and pricing power

Input-cost inflation across materials, freight and labor—with US CPI averaging 3.4% in 2024—tests Macy’s ability to fully pass prices to consumers. Elasticity varies by category and brand tier, so fine-tuned pricing analytics and promo optimization are required. Expanding private brands can improve value perception and gross-margin control, while strict clearance discipline preserves profitability when demand softens.

Interest rates and credit conditions

Rising borrowing costs (federal funds ~5.25% in June 2025) lift Macy’s financing and can slow big-ticket home purchases, pressuring furniture and home categories; US credit card debt near $1.1 trillion (Q1 2025) and tighter underwriting may dampen BNPL and private‑label card spend. Conversely, rate cuts typically revive traffic and raise average transaction values. Macy’s should align inventory buys with the rate outlook and credit trends.

Channel mix and margin structure

Store sales carry higher fixed-cost leverage versus e-commerce, which in 2024 accounted for about 33% of Macy’s sales and bears fulfillment and ~20–30% online returns costs.

Optimizing omnichannel profitability hinges on improving pick, pack, ship and BOPIS economics to cut unit fulfillment costs and lift margins.

Regional fleet rationalization and investments in returns prevention and recommerce can boost four-wall productivity and mitigate margin drag.

Luxury–value bifurcation

Luxury–value bifurcation: affluent cohorts continued to sustain Bloomingdale’s and prestige beauty, with Macy’s Inc. reporting Bloomingdale’s as roughly 9% of total revenue in 2024 and beauty/makeup categories outpacing apparel in margin growth (company filings, 2024).

- Affluent demand: supports Bloomingdale’s & prestige beauty (~9% revenue share, 2024)

- Value focus: promotions & private labels drive traffic and volume

- Segmentation: tight assortment/marketing by income and occasion needed

- Risk mix: balanced exposure smooths cycle volatility

Tariffs on $370B imports, labor & ORC squeeze $24.5B retailer

Macroeconomic strength (U.S. unemployment ~3.6% mid‑2024) supports premium and occasion spend but weak confidence shifts demand to promotions, pressuring AUR and margins. Input‑cost inflation (CPI ~3.4% in 2024) and higher rates (fed funds ~5.25% June 2025) squeeze margins and big‑ticket home sales; omnichannel cost control and private‑brand expansion are pivotal.

| Metric | Value |

|---|---|

| Unemployment | ~3.6% (mid‑2024) |

| CPI | 3.4% (2024) |

| Fed funds | ~5.25% (Jun 2025) |

| E‑commerce share | ~33% (2024) |

| Online returns | 20–30% |

| Bloomingdale’s rev | ~9% (2024) |

Full Version Awaits

Macy's PESTLE Analysis

The preview shown here is the exact Macy's PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers—this is the final, professional document.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal and environmental forces are reshaping Macy's competitive landscape. Our PESTLE highlights regulatory risks, consumer trends and digital disruption in actionable detail. Ideal for investors and strategists—buy the full report to download editable, ready-to-use insights now.

Political factors

Trade and tariff volatility

Shifts in U.S.–China and other trade policies can raise landed costs for apparel, accessories and home goods Macy’s sources globally; tariffs enacted since 2018 cover roughly $370 billion of Chinese goods. Tariff hikes compress margins or force price rises that risk demand for Macy’s roughly $24.5 billion FY2023 sales. Diversifying sourcing and stronger vendor terms are critical mitigations, alongside close monitoring of trade agreements and port policy.

Labor policy and minimum wage shifts

Changes to federal and state minimum wages (federal floor $7.25) and rising state/local rates—with many jurisdictions at or above $15—directly lift store and distribution center labor costs across Macy’s ~450 stores and roughly 68,000 employees. Overtime rule shifts and union activity reduce staffing flexibility during holiday spikes, pressuring margins. Macy’s must accelerate workforce-management tech and productivity programs and use scenario planning to protect service levels and margins.

Tax incentives and retail revitalization

Local tax incentives, zoning shifts, and urban revitalization programs materially affect economics of Macy’s roughly 550-store footprint, lowering remodel costs through tools like tax increment financing that can cover up to 30% of redevelopment expenses. Policy support for downtown recovery—foot-traffic rebounds of about 15% year-over-year in many U.S. downtowns in 2024—increases visit rates and improves lease leverage. Conversely, municipal budget shortfalls can cut incentive pools or raise property taxes; Macy’s can partner with civic leaders to align store investment with community development priorities.

Public safety and urban policy

Rising metro crime and enforcement shifts drive higher shrink, security spend, and weaker shopper sentiment; 2023–24 retail surveys show organized retail crime (ORC) cited by about 80% of retailers as a major concern, prompting coordinated retailer–law enforcement initiatives and new ORC statutes that materially reduce losses. Enhanced protocols raise operating costs and must preserve customer experience; policy advocacy remains key to lowering ORC risk.

- 80% retailers cite ORC

- Coordinated law-enforcement reduces shrink

- Security spend up; experience trade-offs

- Policy advocacy lowers organized-crime exposure

Geopolitical supply chain risks

Conflicts, sanctions and shipping-route disruptions can delay Macy's inventory flow and raise freight costs, prompting shifts to nearshore sourcing that reduce exposure but require vendor development and longer onboarding. Macy's needs multi-node logistics, inventory buffers for peak seasons and political risk insurance alongside scenario playbooks to maintain assortment and margin stability.

- Multi-node logistics

- Nearshore vendor development

- Inventory buffers for peaks

- Political risk insurance

- Scenario playbooks

Tariffs on $370B imports, labor & ORC squeeze $24.5B retailer

Tariff exposure (tariffs on ~$370B Chinese goods) risks margins on Macy’s ~$24.5B FY2023 sales. Labor cost pressure from ~68,000 employees across ~450 stores and rising state/local wages compresses margins. ORC cited by ~80% of retailers raises security spend and shrink, forcing capital and policy responses.

| Issue | Metric | Near-term Impact |

|---|---|---|

| Tariffs | $370B scope / $24.5B sales | Margin pressure |

| Labor | 68,000 employees / ~450 stores | Higher Opex |

| ORC | 80% retailers | Shrink↑, security spend↑ |

What is included in the product

Explores how macro-environmental factors uniquely affect Macy's across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and forward-looking scenarios specific to the U.S. retail sector to support executives, consultants and investors in strategy and risk planning.

A clean, summarized Macy's PESTLE analysis for easy reference in meetings or presentations. Visually segmented by PESTLE categories and editable so teams can add region- or business-line specific notes for quick alignment and decision-making.

Economic factors

Consumer confidence and discretionary spend

Macroeconomic sentiment drives demand for apparel, beauty and home categories; with U.S. unemployment near 3.6% in mid‑2024 (BLS), stronger labor markets and wealth effects lift premium and occasion purchases. Weak confidence shifts baskets to promotions and essentials, pressuring AUR and gross margin. Macy’s must flex pricing, marketing cadence and assortment depth to protect share and margin.

Inflation and pricing power

Input-cost inflation across materials, freight and labor—with US CPI averaging 3.4% in 2024—tests Macy’s ability to fully pass prices to consumers. Elasticity varies by category and brand tier, so fine-tuned pricing analytics and promo optimization are required. Expanding private brands can improve value perception and gross-margin control, while strict clearance discipline preserves profitability when demand softens.

Interest rates and credit conditions

Rising borrowing costs (federal funds ~5.25% in June 2025) lift Macy’s financing and can slow big-ticket home purchases, pressuring furniture and home categories; US credit card debt near $1.1 trillion (Q1 2025) and tighter underwriting may dampen BNPL and private‑label card spend. Conversely, rate cuts typically revive traffic and raise average transaction values. Macy’s should align inventory buys with the rate outlook and credit trends.

Channel mix and margin structure

Store sales carry higher fixed-cost leverage versus e-commerce, which in 2024 accounted for about 33% of Macy’s sales and bears fulfillment and ~20–30% online returns costs.

Optimizing omnichannel profitability hinges on improving pick, pack, ship and BOPIS economics to cut unit fulfillment costs and lift margins.

Regional fleet rationalization and investments in returns prevention and recommerce can boost four-wall productivity and mitigate margin drag.

Luxury–value bifurcation

Luxury–value bifurcation: affluent cohorts continued to sustain Bloomingdale’s and prestige beauty, with Macy’s Inc. reporting Bloomingdale’s as roughly 9% of total revenue in 2024 and beauty/makeup categories outpacing apparel in margin growth (company filings, 2024).

- Affluent demand: supports Bloomingdale’s & prestige beauty (~9% revenue share, 2024)

- Value focus: promotions & private labels drive traffic and volume

- Segmentation: tight assortment/marketing by income and occasion needed

- Risk mix: balanced exposure smooths cycle volatility

Tariffs on $370B imports, labor & ORC squeeze $24.5B retailer

Macroeconomic strength (U.S. unemployment ~3.6% mid‑2024) supports premium and occasion spend but weak confidence shifts demand to promotions, pressuring AUR and margins. Input‑cost inflation (CPI ~3.4% in 2024) and higher rates (fed funds ~5.25% June 2025) squeeze margins and big‑ticket home sales; omnichannel cost control and private‑brand expansion are pivotal.

| Metric | Value |

|---|---|

| Unemployment | ~3.6% (mid‑2024) |

| CPI | 3.4% (2024) |

| Fed funds | ~5.25% (Jun 2025) |

| E‑commerce share | ~33% (2024) |

| Online returns | 20–30% |

| Bloomingdale’s rev | ~9% (2024) |

Full Version Awaits

Macy's PESTLE Analysis

The preview shown here is the exact Macy's PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers—this is the final, professional document.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political, economic, social, technological, legal and environmental forces are reshaping Macy's competitive landscape. Our PESTLE highlights regulatory risks, consumer trends and digital disruption in actionable detail. Ideal for investors and strategists—buy the full report to download editable, ready-to-use insights now.

Political factors

Trade and tariff volatility

Shifts in U.S.–China and other trade policies can raise landed costs for apparel, accessories and home goods Macy’s sources globally; tariffs enacted since 2018 cover roughly $370 billion of Chinese goods. Tariff hikes compress margins or force price rises that risk demand for Macy’s roughly $24.5 billion FY2023 sales. Diversifying sourcing and stronger vendor terms are critical mitigations, alongside close monitoring of trade agreements and port policy.

Labor policy and minimum wage shifts

Changes to federal and state minimum wages (federal floor $7.25) and rising state/local rates—with many jurisdictions at or above $15—directly lift store and distribution center labor costs across Macy’s ~450 stores and roughly 68,000 employees. Overtime rule shifts and union activity reduce staffing flexibility during holiday spikes, pressuring margins. Macy’s must accelerate workforce-management tech and productivity programs and use scenario planning to protect service levels and margins.

Tax incentives and retail revitalization

Local tax incentives, zoning shifts, and urban revitalization programs materially affect economics of Macy’s roughly 550-store footprint, lowering remodel costs through tools like tax increment financing that can cover up to 30% of redevelopment expenses. Policy support for downtown recovery—foot-traffic rebounds of about 15% year-over-year in many U.S. downtowns in 2024—increases visit rates and improves lease leverage. Conversely, municipal budget shortfalls can cut incentive pools or raise property taxes; Macy’s can partner with civic leaders to align store investment with community development priorities.

Public safety and urban policy

Rising metro crime and enforcement shifts drive higher shrink, security spend, and weaker shopper sentiment; 2023–24 retail surveys show organized retail crime (ORC) cited by about 80% of retailers as a major concern, prompting coordinated retailer–law enforcement initiatives and new ORC statutes that materially reduce losses. Enhanced protocols raise operating costs and must preserve customer experience; policy advocacy remains key to lowering ORC risk.

- 80% retailers cite ORC

- Coordinated law-enforcement reduces shrink

- Security spend up; experience trade-offs

- Policy advocacy lowers organized-crime exposure

Geopolitical supply chain risks

Conflicts, sanctions and shipping-route disruptions can delay Macy's inventory flow and raise freight costs, prompting shifts to nearshore sourcing that reduce exposure but require vendor development and longer onboarding. Macy's needs multi-node logistics, inventory buffers for peak seasons and political risk insurance alongside scenario playbooks to maintain assortment and margin stability.

- Multi-node logistics

- Nearshore vendor development

- Inventory buffers for peaks

- Political risk insurance

- Scenario playbooks

Tariffs on $370B imports, labor & ORC squeeze $24.5B retailer

Tariff exposure (tariffs on ~$370B Chinese goods) risks margins on Macy’s ~$24.5B FY2023 sales. Labor cost pressure from ~68,000 employees across ~450 stores and rising state/local wages compresses margins. ORC cited by ~80% of retailers raises security spend and shrink, forcing capital and policy responses.

| Issue | Metric | Near-term Impact |

|---|---|---|

| Tariffs | $370B scope / $24.5B sales | Margin pressure |

| Labor | 68,000 employees / ~450 stores | Higher Opex |

| ORC | 80% retailers | Shrink↑, security spend↑ |

What is included in the product

Explores how macro-environmental factors uniquely affect Macy's across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven insights and forward-looking scenarios specific to the U.S. retail sector to support executives, consultants and investors in strategy and risk planning.

A clean, summarized Macy's PESTLE analysis for easy reference in meetings or presentations. Visually segmented by PESTLE categories and editable so teams can add region- or business-line specific notes for quick alignment and decision-making.

Economic factors

Consumer confidence and discretionary spend

Macroeconomic sentiment drives demand for apparel, beauty and home categories; with U.S. unemployment near 3.6% in mid‑2024 (BLS), stronger labor markets and wealth effects lift premium and occasion purchases. Weak confidence shifts baskets to promotions and essentials, pressuring AUR and gross margin. Macy’s must flex pricing, marketing cadence and assortment depth to protect share and margin.

Inflation and pricing power

Input-cost inflation across materials, freight and labor—with US CPI averaging 3.4% in 2024—tests Macy’s ability to fully pass prices to consumers. Elasticity varies by category and brand tier, so fine-tuned pricing analytics and promo optimization are required. Expanding private brands can improve value perception and gross-margin control, while strict clearance discipline preserves profitability when demand softens.

Interest rates and credit conditions

Rising borrowing costs (federal funds ~5.25% in June 2025) lift Macy’s financing and can slow big-ticket home purchases, pressuring furniture and home categories; US credit card debt near $1.1 trillion (Q1 2025) and tighter underwriting may dampen BNPL and private‑label card spend. Conversely, rate cuts typically revive traffic and raise average transaction values. Macy’s should align inventory buys with the rate outlook and credit trends.

Channel mix and margin structure

Store sales carry higher fixed-cost leverage versus e-commerce, which in 2024 accounted for about 33% of Macy’s sales and bears fulfillment and ~20–30% online returns costs.

Optimizing omnichannel profitability hinges on improving pick, pack, ship and BOPIS economics to cut unit fulfillment costs and lift margins.

Regional fleet rationalization and investments in returns prevention and recommerce can boost four-wall productivity and mitigate margin drag.

Luxury–value bifurcation

Luxury–value bifurcation: affluent cohorts continued to sustain Bloomingdale’s and prestige beauty, with Macy’s Inc. reporting Bloomingdale’s as roughly 9% of total revenue in 2024 and beauty/makeup categories outpacing apparel in margin growth (company filings, 2024).

- Affluent demand: supports Bloomingdale’s & prestige beauty (~9% revenue share, 2024)

- Value focus: promotions & private labels drive traffic and volume

- Segmentation: tight assortment/marketing by income and occasion needed

- Risk mix: balanced exposure smooths cycle volatility

Tariffs on $370B imports, labor & ORC squeeze $24.5B retailer

Macroeconomic strength (U.S. unemployment ~3.6% mid‑2024) supports premium and occasion spend but weak confidence shifts demand to promotions, pressuring AUR and margins. Input‑cost inflation (CPI ~3.4% in 2024) and higher rates (fed funds ~5.25% June 2025) squeeze margins and big‑ticket home sales; omnichannel cost control and private‑brand expansion are pivotal.

| Metric | Value |

|---|---|

| Unemployment | ~3.6% (mid‑2024) |

| CPI | 3.4% (2024) |

| Fed funds | ~5.25% (Jun 2025) |

| E‑commerce share | ~33% (2024) |

| Online returns | 20–30% |

| Bloomingdale’s rev | ~9% (2024) |

Full Version Awaits

Macy's PESTLE Analysis

The preview shown here is the exact Macy's PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. The layout, content, and structure visible are identical to the downloadable file. No placeholders or teasers—this is the final, professional document.