MagnaChip Porter's Five Forces Analysis

From Overview to Strategy Blueprint

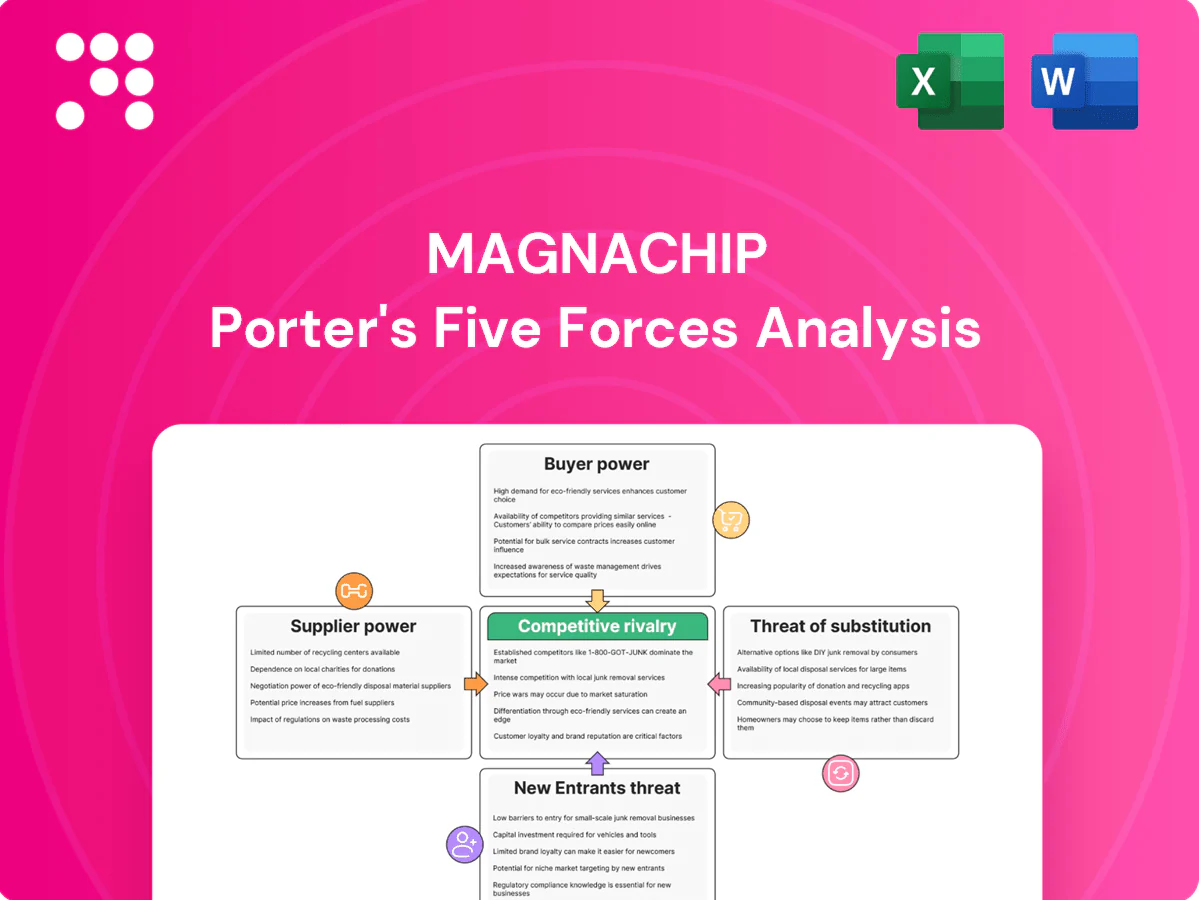

MagnaChip faces moderate supplier power, intense rivalry among semiconductor peers, and growing buyer sophistication as IoT and automotive demand rises; threats from substitutes and new entrants are tempered by capital intensity and IP. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore MagnaChip’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated foundry capacity

MagnaChip depends on a limited pool of specialty foundries for mixed-signal, BCD and display-driver processes, a market where the top three foundries controlled over 70% of advanced capacity in 2024. Capacity is cyclical and during 2023–24 tightness pushed lead times to several months, with allocations favoring larger OEMs first. This concentration gives foundries leverage over pricing, delivery and process roadmaps. Dual-sourcing reduces but does not remove dependence on constrained nodes.

OSAT and advanced packaging reliance

Outsourced assembly and test providers are essential for MagnaChip power IC and display driver packaging. Advanced packages and automotive-grade qualification narrow the supplier set; 2024 global OSAT market was about 52 billion USD. Tight OSAT capacity pushed lead times to 12–20 weeks and raised unit costs roughly 10%. Long-term agreements (1–3 year) mitigate risk but switching costs remain meaningful.

Specialty wafer and materials scarcity

Sources for high-voltage, epitaxial and specialty wafers are concentrated: Shin-Etsu, SUMCO and GlobalWafers accounted for over 80% of global silicon wafer capacity in 2024, limiting supplier options for MagnaChip. Supply shocks in gases and specialty chemicals compress yields and output and transmit volatility through the chain. Vendors have historically passed through higher costs in tight markets, while inventory buffering provides only partial protection due to long lead times and wafer MOQs.

EDA/IP toolchain lock-in

EDA/IP toolchain lock-in gives suppliers strong leverage: the top three EDA vendors control roughly 80% of the market and ARM-based IP underpins over 90% of smartphone SoCs, making switching costly due to retraining, requalification, and schedule risk. Vendors can increment maintenance and licensing fees; volume discounts mitigate but do not eliminate pricing power, leaving MagnaChip exposed to supplier-driven margin pressure.

- High concentration: top 3 ≈80% market share

- IP dominance: ARM >90% smartphone CPU IP

- Switching costs: retraining, requalification, schedule risk

- Pricing: maintenance/licensing increases; volume discounts only partially offset

Geopolitical and compliance constraints

Export controls in 2024, notably US restrictions limiting advanced chipmaking-related exports to certain regions, constrain MagnaChip's access to tools, nodes and equipment and raise supplier leverage. Requalification to alternate suppliers extends lead times and creates incremental CAPEX and qualification costs. Currency swings in 2024 further complicate input pricing and suppliers may reprioritize regions based on regulatory risk.

- export-controls-2024

- requalification-delay-cost

- currency-volatility

- supplier-regional-reprioritization

Foundry concentration >70%; OSAT $52B; EDA/IP ~80%

Supplier power is high: top 3 foundries >70% advanced capacity in 2024, OSAT market ≈52bn USD with 12–20 week lead times, and top wafer suppliers >80% capacity. EDA/IP dominance (top 3 ≈80%; ARM >90% smartphone IP) raises switching costs and pricing leverage. Export controls and currency volatility add requalification and CAPEX risks.

| Metric | 2024 |

|---|---|

| Foundry concentration | >70% top 3 |

| OSAT market | 52bn USD; LT 12–20w |

| Wafer share | >80% top suppliers |

What is included in the product

Comprehensive Porter's Five Forces for MagnaChip, identifying key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and disruptive risks to market share—actionable insights for strategy, investor presentations, and internal planning.

A one-sheet Porter's Five Forces for MagnaChip distills semiconductor competitive pressures into clear, actionable insights—ideal for quick board or investor decisions. No macros, easy to customize with updated data or scenarios for immediate strategic use.

Customers Bargaining Power

Consolidated OEM and panel customers

Display and consumer electronics buyers are concentrated and large in 2024, with panel makers such as BOE, Samsung Display, LG Display, AU Optronics and Innolux dictating tough pricing and payment terms.

Tier-1 OEMs and panel customers routinely drive product specifications and roadmaps, forcing MagnaChip to align R&D and manufacturing to customer requirements.

Losing a top account can materially cut volumes, while multi-year agreements provide revenue visibility at the cost of negotiated concessions.

Design-in stickiness vs price pressure

Design-in stickiness for MagnaChip is strong because replacement triggers costly validation cycles (often 6–18 months), but customers expect annual cost-downs; in 2024 OEMs demanded rebates and shared productivity gains as standard, pressuring ASPs despite a global semiconductor market near $600B in 2024, so MagnaChip must layer value-add features to defend pricing.

Automotive qualification leverage

Automotive customers insist on AEC-Q qualification and PPAP sign-off, creating high technical and documentation hurdles for MagnaChip. Program lifecycles typically run 7–10 years, but OEMs enforce target price erosion of roughly 3–5% annually, squeezing margins. OEMs also demand stringent quality metrics and warranty terms, and dual-sourcing rules frequently cap a supplier’s program share at about 50%, limiting pricing power.

Demand volatility and scheduling power

Buyers shift forecasts rapidly with end-market swings, demanding flexible rescheduling and buffer-stock support, which transfers inventory and seasonality risk upstream to MagnaChip and its suppliers. Priority access is frequently conditional on price concessions or volume commitments, pressuring margins and capacity planning.

- Buyers: rapid forecast swings

- Requests: rescheduling + buffer-stock

- Risk: inventory shifted upstream

- Trade-offs: price or volume commitments for priority

Information asymmetry narrowing

Buyers increasingly benchmark MagnaChip solutions against global suppliers in 2024 as teardown reports and reference designs from firms like TechInsights and Broadcom reduce supplier differentiation, forcing price and feature comparisons; procurement analytics sharpen negotiations and demand clear measurable TCO benefits from MagnaChip.

- Benchmarking: cross-supplier comparisons

- Teardowns: reference designs reduce differentiation

- Procurement analytics: sharper negotiations

- Demand: measurable TCO proof from MagnaChip

Panel pricing forces 3-5% ASP cuts in a $600B market

Display and consumer electronics buyers remain concentrated in 2024, with panel makers (BOE, Samsung Display, LGD, AUO, Innolux) dictating pricing and terms, pressuring ASPs despite a ~600B global semiconductor market in 2024.

Design-in stickiness (validation 6–18 months) and long automotive programs (7–10 years) raise switching costs, yet OEMs force 3–5% annual price erosion and dual-sourcing caps ~50%.

Rapid forecast swings, rescheduling, buffer-stock, rebates and TCO demands shift inventory risk upstream and tighten negotiations.

| Metric | Value |

|---|---|

| Market size 2024 | $600B |

| Price erosion | 3–5% p.a. |

| Validation | 6–18 months |

| Program life | 7–10 years |

| Dual-source cap | ~50% |

Same Document Delivered

MagnaChip Porter's Five Forces Analysis

This preview shows the exact MagnaChip Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The document is fully formatted and ready for download the moment you buy. What you see here is the final deliverable, complete and immediately accessible.

From Overview to Strategy Blueprint

MagnaChip faces moderate supplier power, intense rivalry among semiconductor peers, and growing buyer sophistication as IoT and automotive demand rises; threats from substitutes and new entrants are tempered by capital intensity and IP. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore MagnaChip’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated foundry capacity

MagnaChip depends on a limited pool of specialty foundries for mixed-signal, BCD and display-driver processes, a market where the top three foundries controlled over 70% of advanced capacity in 2024. Capacity is cyclical and during 2023–24 tightness pushed lead times to several months, with allocations favoring larger OEMs first. This concentration gives foundries leverage over pricing, delivery and process roadmaps. Dual-sourcing reduces but does not remove dependence on constrained nodes.

OSAT and advanced packaging reliance

Outsourced assembly and test providers are essential for MagnaChip power IC and display driver packaging. Advanced packages and automotive-grade qualification narrow the supplier set; 2024 global OSAT market was about 52 billion USD. Tight OSAT capacity pushed lead times to 12–20 weeks and raised unit costs roughly 10%. Long-term agreements (1–3 year) mitigate risk but switching costs remain meaningful.

Specialty wafer and materials scarcity

Sources for high-voltage, epitaxial and specialty wafers are concentrated: Shin-Etsu, SUMCO and GlobalWafers accounted for over 80% of global silicon wafer capacity in 2024, limiting supplier options for MagnaChip. Supply shocks in gases and specialty chemicals compress yields and output and transmit volatility through the chain. Vendors have historically passed through higher costs in tight markets, while inventory buffering provides only partial protection due to long lead times and wafer MOQs.

EDA/IP toolchain lock-in

EDA/IP toolchain lock-in gives suppliers strong leverage: the top three EDA vendors control roughly 80% of the market and ARM-based IP underpins over 90% of smartphone SoCs, making switching costly due to retraining, requalification, and schedule risk. Vendors can increment maintenance and licensing fees; volume discounts mitigate but do not eliminate pricing power, leaving MagnaChip exposed to supplier-driven margin pressure.

- High concentration: top 3 ≈80% market share

- IP dominance: ARM >90% smartphone CPU IP

- Switching costs: retraining, requalification, schedule risk

- Pricing: maintenance/licensing increases; volume discounts only partially offset

Geopolitical and compliance constraints

Export controls in 2024, notably US restrictions limiting advanced chipmaking-related exports to certain regions, constrain MagnaChip's access to tools, nodes and equipment and raise supplier leverage. Requalification to alternate suppliers extends lead times and creates incremental CAPEX and qualification costs. Currency swings in 2024 further complicate input pricing and suppliers may reprioritize regions based on regulatory risk.

- export-controls-2024

- requalification-delay-cost

- currency-volatility

- supplier-regional-reprioritization

Foundry concentration >70%; OSAT $52B; EDA/IP ~80%

Supplier power is high: top 3 foundries >70% advanced capacity in 2024, OSAT market ≈52bn USD with 12–20 week lead times, and top wafer suppliers >80% capacity. EDA/IP dominance (top 3 ≈80%; ARM >90% smartphone IP) raises switching costs and pricing leverage. Export controls and currency volatility add requalification and CAPEX risks.

| Metric | 2024 |

|---|---|

| Foundry concentration | >70% top 3 |

| OSAT market | 52bn USD; LT 12–20w |

| Wafer share | >80% top suppliers |

What is included in the product

Comprehensive Porter's Five Forces for MagnaChip, identifying key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and disruptive risks to market share—actionable insights for strategy, investor presentations, and internal planning.

A one-sheet Porter's Five Forces for MagnaChip distills semiconductor competitive pressures into clear, actionable insights—ideal for quick board or investor decisions. No macros, easy to customize with updated data or scenarios for immediate strategic use.

Customers Bargaining Power

Consolidated OEM and panel customers

Display and consumer electronics buyers are concentrated and large in 2024, with panel makers such as BOE, Samsung Display, LG Display, AU Optronics and Innolux dictating tough pricing and payment terms.

Tier-1 OEMs and panel customers routinely drive product specifications and roadmaps, forcing MagnaChip to align R&D and manufacturing to customer requirements.

Losing a top account can materially cut volumes, while multi-year agreements provide revenue visibility at the cost of negotiated concessions.

Design-in stickiness vs price pressure

Design-in stickiness for MagnaChip is strong because replacement triggers costly validation cycles (often 6–18 months), but customers expect annual cost-downs; in 2024 OEMs demanded rebates and shared productivity gains as standard, pressuring ASPs despite a global semiconductor market near $600B in 2024, so MagnaChip must layer value-add features to defend pricing.

Automotive qualification leverage

Automotive customers insist on AEC-Q qualification and PPAP sign-off, creating high technical and documentation hurdles for MagnaChip. Program lifecycles typically run 7–10 years, but OEMs enforce target price erosion of roughly 3–5% annually, squeezing margins. OEMs also demand stringent quality metrics and warranty terms, and dual-sourcing rules frequently cap a supplier’s program share at about 50%, limiting pricing power.

Demand volatility and scheduling power

Buyers shift forecasts rapidly with end-market swings, demanding flexible rescheduling and buffer-stock support, which transfers inventory and seasonality risk upstream to MagnaChip and its suppliers. Priority access is frequently conditional on price concessions or volume commitments, pressuring margins and capacity planning.

- Buyers: rapid forecast swings

- Requests: rescheduling + buffer-stock

- Risk: inventory shifted upstream

- Trade-offs: price or volume commitments for priority

Information asymmetry narrowing

Buyers increasingly benchmark MagnaChip solutions against global suppliers in 2024 as teardown reports and reference designs from firms like TechInsights and Broadcom reduce supplier differentiation, forcing price and feature comparisons; procurement analytics sharpen negotiations and demand clear measurable TCO benefits from MagnaChip.

- Benchmarking: cross-supplier comparisons

- Teardowns: reference designs reduce differentiation

- Procurement analytics: sharper negotiations

- Demand: measurable TCO proof from MagnaChip

Panel pricing forces 3-5% ASP cuts in a $600B market

Display and consumer electronics buyers remain concentrated in 2024, with panel makers (BOE, Samsung Display, LGD, AUO, Innolux) dictating pricing and terms, pressuring ASPs despite a ~600B global semiconductor market in 2024.

Design-in stickiness (validation 6–18 months) and long automotive programs (7–10 years) raise switching costs, yet OEMs force 3–5% annual price erosion and dual-sourcing caps ~50%.

Rapid forecast swings, rescheduling, buffer-stock, rebates and TCO demands shift inventory risk upstream and tighten negotiations.

| Metric | Value |

|---|---|

| Market size 2024 | $600B |

| Price erosion | 3–5% p.a. |

| Validation | 6–18 months |

| Program life | 7–10 years |

| Dual-source cap | ~50% |

Same Document Delivered

MagnaChip Porter's Five Forces Analysis

This preview shows the exact MagnaChip Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The document is fully formatted and ready for download the moment you buy. What you see here is the final deliverable, complete and immediately accessible.

Description

From Overview to Strategy Blueprint

MagnaChip faces moderate supplier power, intense rivalry among semiconductor peers, and growing buyer sophistication as IoT and automotive demand rises; threats from substitutes and new entrants are tempered by capital intensity and IP. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore MagnaChip’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated foundry capacity

MagnaChip depends on a limited pool of specialty foundries for mixed-signal, BCD and display-driver processes, a market where the top three foundries controlled over 70% of advanced capacity in 2024. Capacity is cyclical and during 2023–24 tightness pushed lead times to several months, with allocations favoring larger OEMs first. This concentration gives foundries leverage over pricing, delivery and process roadmaps. Dual-sourcing reduces but does not remove dependence on constrained nodes.

OSAT and advanced packaging reliance

Outsourced assembly and test providers are essential for MagnaChip power IC and display driver packaging. Advanced packages and automotive-grade qualification narrow the supplier set; 2024 global OSAT market was about 52 billion USD. Tight OSAT capacity pushed lead times to 12–20 weeks and raised unit costs roughly 10%. Long-term agreements (1–3 year) mitigate risk but switching costs remain meaningful.

Specialty wafer and materials scarcity

Sources for high-voltage, epitaxial and specialty wafers are concentrated: Shin-Etsu, SUMCO and GlobalWafers accounted for over 80% of global silicon wafer capacity in 2024, limiting supplier options for MagnaChip. Supply shocks in gases and specialty chemicals compress yields and output and transmit volatility through the chain. Vendors have historically passed through higher costs in tight markets, while inventory buffering provides only partial protection due to long lead times and wafer MOQs.

EDA/IP toolchain lock-in

EDA/IP toolchain lock-in gives suppliers strong leverage: the top three EDA vendors control roughly 80% of the market and ARM-based IP underpins over 90% of smartphone SoCs, making switching costly due to retraining, requalification, and schedule risk. Vendors can increment maintenance and licensing fees; volume discounts mitigate but do not eliminate pricing power, leaving MagnaChip exposed to supplier-driven margin pressure.

- High concentration: top 3 ≈80% market share

- IP dominance: ARM >90% smartphone CPU IP

- Switching costs: retraining, requalification, schedule risk

- Pricing: maintenance/licensing increases; volume discounts only partially offset

Geopolitical and compliance constraints

Export controls in 2024, notably US restrictions limiting advanced chipmaking-related exports to certain regions, constrain MagnaChip's access to tools, nodes and equipment and raise supplier leverage. Requalification to alternate suppliers extends lead times and creates incremental CAPEX and qualification costs. Currency swings in 2024 further complicate input pricing and suppliers may reprioritize regions based on regulatory risk.

- export-controls-2024

- requalification-delay-cost

- currency-volatility

- supplier-regional-reprioritization

Foundry concentration >70%; OSAT $52B; EDA/IP ~80%

Supplier power is high: top 3 foundries >70% advanced capacity in 2024, OSAT market ≈52bn USD with 12–20 week lead times, and top wafer suppliers >80% capacity. EDA/IP dominance (top 3 ≈80%; ARM >90% smartphone IP) raises switching costs and pricing leverage. Export controls and currency volatility add requalification and CAPEX risks.

| Metric | 2024 |

|---|---|

| Foundry concentration | >70% top 3 |

| OSAT market | 52bn USD; LT 12–20w |

| Wafer share | >80% top suppliers |

What is included in the product

Comprehensive Porter's Five Forces for MagnaChip, identifying key competitive drivers, supplier and buyer power, threat of substitutes and new entrants, and disruptive risks to market share—actionable insights for strategy, investor presentations, and internal planning.

A one-sheet Porter's Five Forces for MagnaChip distills semiconductor competitive pressures into clear, actionable insights—ideal for quick board or investor decisions. No macros, easy to customize with updated data or scenarios for immediate strategic use.

Customers Bargaining Power

Consolidated OEM and panel customers

Display and consumer electronics buyers are concentrated and large in 2024, with panel makers such as BOE, Samsung Display, LG Display, AU Optronics and Innolux dictating tough pricing and payment terms.

Tier-1 OEMs and panel customers routinely drive product specifications and roadmaps, forcing MagnaChip to align R&D and manufacturing to customer requirements.

Losing a top account can materially cut volumes, while multi-year agreements provide revenue visibility at the cost of negotiated concessions.

Design-in stickiness vs price pressure

Design-in stickiness for MagnaChip is strong because replacement triggers costly validation cycles (often 6–18 months), but customers expect annual cost-downs; in 2024 OEMs demanded rebates and shared productivity gains as standard, pressuring ASPs despite a global semiconductor market near $600B in 2024, so MagnaChip must layer value-add features to defend pricing.

Automotive qualification leverage

Automotive customers insist on AEC-Q qualification and PPAP sign-off, creating high technical and documentation hurdles for MagnaChip. Program lifecycles typically run 7–10 years, but OEMs enforce target price erosion of roughly 3–5% annually, squeezing margins. OEMs also demand stringent quality metrics and warranty terms, and dual-sourcing rules frequently cap a supplier’s program share at about 50%, limiting pricing power.

Demand volatility and scheduling power

Buyers shift forecasts rapidly with end-market swings, demanding flexible rescheduling and buffer-stock support, which transfers inventory and seasonality risk upstream to MagnaChip and its suppliers. Priority access is frequently conditional on price concessions or volume commitments, pressuring margins and capacity planning.

- Buyers: rapid forecast swings

- Requests: rescheduling + buffer-stock

- Risk: inventory shifted upstream

- Trade-offs: price or volume commitments for priority

Information asymmetry narrowing

Buyers increasingly benchmark MagnaChip solutions against global suppliers in 2024 as teardown reports and reference designs from firms like TechInsights and Broadcom reduce supplier differentiation, forcing price and feature comparisons; procurement analytics sharpen negotiations and demand clear measurable TCO benefits from MagnaChip.

- Benchmarking: cross-supplier comparisons

- Teardowns: reference designs reduce differentiation

- Procurement analytics: sharper negotiations

- Demand: measurable TCO proof from MagnaChip

Panel pricing forces 3-5% ASP cuts in a $600B market

Display and consumer electronics buyers remain concentrated in 2024, with panel makers (BOE, Samsung Display, LGD, AUO, Innolux) dictating pricing and terms, pressuring ASPs despite a ~600B global semiconductor market in 2024.

Design-in stickiness (validation 6–18 months) and long automotive programs (7–10 years) raise switching costs, yet OEMs force 3–5% annual price erosion and dual-sourcing caps ~50%.

Rapid forecast swings, rescheduling, buffer-stock, rebates and TCO demands shift inventory risk upstream and tighten negotiations.

| Metric | Value |

|---|---|

| Market size 2024 | $600B |

| Price erosion | 3–5% p.a. |

| Validation | 6–18 months |

| Program life | 7–10 years |

| Dual-source cap | ~50% |

Same Document Delivered

MagnaChip Porter's Five Forces Analysis

This preview shows the exact MagnaChip Porter's Five Forces Analysis you'll receive after purchase—no placeholders or samples. The document is fully formatted and ready for download the moment you buy. What you see here is the final deliverable, complete and immediately accessible.