Major Cineplex Group Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

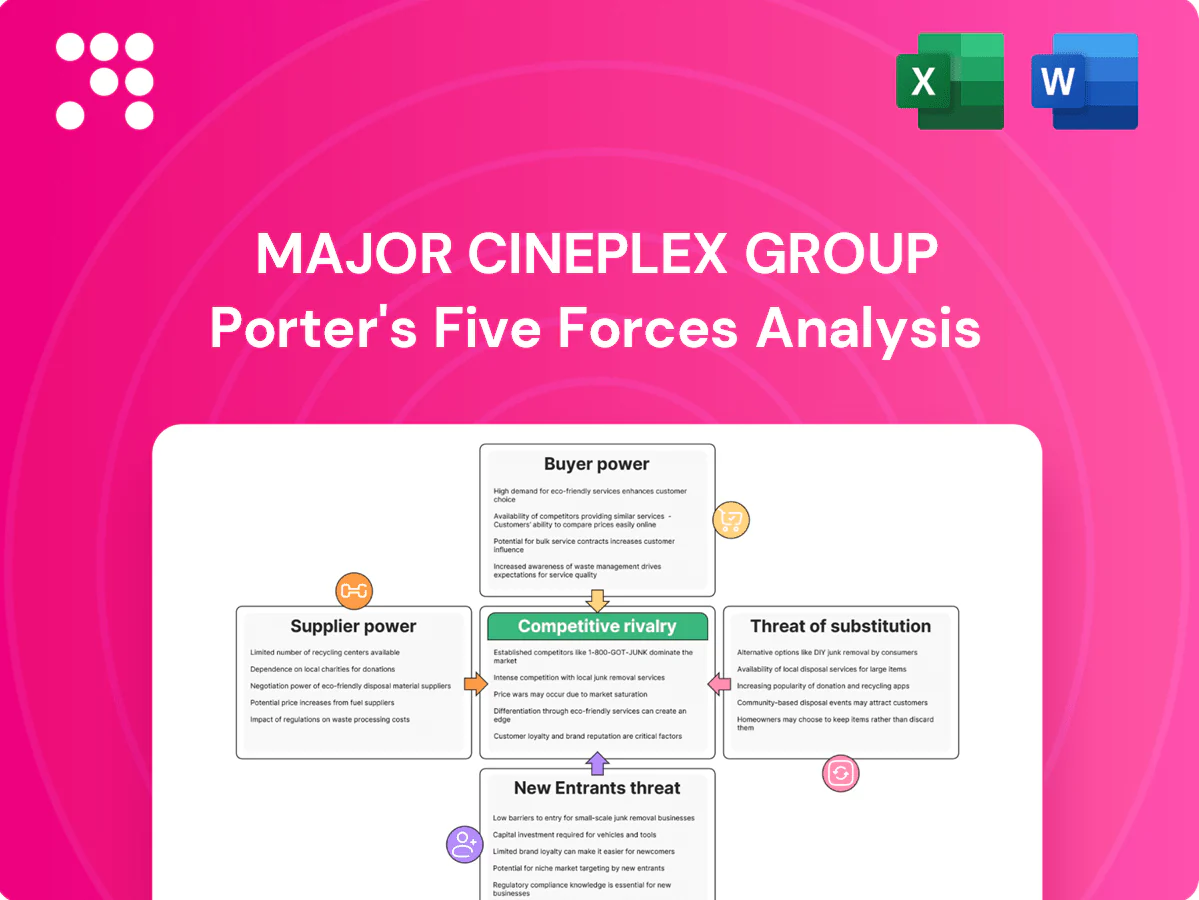

Major Cineplex faces moderate buyer power, strong substitutability from streaming and entertainment, and significant rivalry within Thailand's cinema market, while supplier influence and entry barriers vary by location and scale. This snapshot teases critical dynamics—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic recommendations to inform investment or strategy.

Suppliers Bargaining Power

Studio content concentration

Major depends on a concentrated set of Hollywood studios and key Thai producers for tentpole releases, giving suppliers leverage over rental terms and theatrical windowing in 2024.

Major’s distribution arm partially offsets this by securing local content and negotiating package deals to smooth supply risk.

Seasonal blockbuster slates in 2024 can still swing bargaining power firmly toward suppliers during peak periods.

Premium tech vendors

Premium tech vendors such as IMAX, 4DX, Dolby and laser projection suppliers are few and highly specialized, raising switching costs and granting pricing power. Vendor certification and multi‑year service contracts (typically 3–7 years) lock in terms and maintenance fees. Major Cineplex, as Thailand’s largest exhibitor with market share above 50%, gains negotiating leverage, but true alternatives for flagship formats remain limited.

Real estate and mall partners

Cinema locations hinge on prime mall anchors and long leases (often 10–20 years), giving landlords leverage via rent hikes, mall revamps and co‑marketing clauses; Major Cineplex, with over 500 screens across 120+ sites as of 2024, mitigates this by spreading risk across a multi‑site portfolio and acting as an anchor traffic driver, while landlord power eases in secondary cities where tenant mix needs boost Major’s negotiating leverage.

F&B and concession inputs

Popcorn, beverage and packaging inputs for Major Cineplex face wide supplier pools, reducing individual supplier leverage as many inputs are commodity-like and can be multi-sourced. Branded beverage deals still carry minimums and co-marketing obligations that restrict flexibility. Inflation spikes in input costs often pass through with a lag, compressing concession margins until pricing and cost recovery align.

- Broad supplier base — low switching cost

- Commoditized inputs — multi-sourcing possible

- Branded drinks — minimums and marketing tie-ins

- Inflation pass-through lag — margin pressure

Utilities and labor

Electricity for HVAC, projection and LED screens plus skilled projection technicians are essential for Major Cineplex; commercial tariffs in Thailand rose to about 5.0 THB/kWh in 2024, constraining margins while utility monopolies limit negotiation. Labor markets are moderately competitive, with certified projection and premium-format training adding incremental wages ~5–8% above base pay. Automation and optimized scheduling have begun reducing technician hours and softening supplier leverage.

- Essential inputs: electricity, skilled technicians

- 2024 tariff: ~5.0 THB/kWh

- Training premium: +5–8% wage cost

- Mitigants: automation, scheduling

Moderate supplier power: exhibitor scale offsets studio/tech leverage, tariffs and wage pressures

Supplier power is moderate: Hollywood studios and tech vendors (IMAX/4DX) exert strong leverage during blockbusters and for premium formats, while Major’s >50% market share, 500+ screens (120+ sites) and in‑house distribution mitigate some risk. Long mall leases (10–20 yrs) and utility tariffs (~5.0 THB/kWh) constrain flexibility; concessions inputs remain low‑power but branded deals and wage premiums (+5–8%) limit pass‑through.

| Factor | 2024 Metric |

|---|---|

| Market share | >50% |

| Screens/sites | 500+/120+ |

| Tariff | ~5.0 THB/kWh |

| Technician wage premium | +5–8% |

What is included in the product

Tailored Porter's Five Forces analysis for Major Cineplex Group uncovering competitive rivalry, buyer and supplier leverage, threats from new entrants and substitutes, and strategic barriers that shape pricing, profitability, and market resilience.

A concise one-sheet Porter's Five Forces for Major Cineplex Group—instantly highlights competitive intensity, supplier and buyer power, and substitute/entry threats to relieve analysis bottlenecks. Clean, slide-ready layout with adjustable pressure levels so teams can tailor scenarios and make faster strategic decisions.

Customers Bargaining Power

Price sensitivity and elasticity

Thai moviegoers are value conscious, especially outside Bangkok, where urban concentration and a 2024 population of about 71 million shape demand sensitivity; Major Cineplex, Thailand's largest operator, sees ticket volumes react to price, promotions and content quality. Premium formats (VIP/IMAX) sustain a notable willingness to pay, while standard screens face discount pressure; family bundles and off‑peak pricing cut churn.

Abundant entertainment choices

Customers can switch to streaming, gaming, or dining with minimal friction as global SVoD subscriptions topped 1 billion by 2024 and gaming revenues exceeded $200 billion in 2023, raising buyer power for casual visits. Low switching costs push price sensitivity; experiential differentiation — premium seating, F&B, IMAX — is key to avoid price-based comparison. Event cinema, theatrical exclusives and limited windows reduce substitutability and strengthen retention.

Loyalty and membership programs

Major Cineplex's memberships, points and tiered benefits lock in repeat visits by creating switching costs and raising lifetime value; data-driven personalized offers in 2024 have reduced effective buyer power through targeted discounts and upsells. Corporate and student segments are fenced with tailored pricing and bulk packages, while weak engagement or low redemption rates would increase churn and shift bargaining leverage back to customers.

Group and corporate buyers

In 2024 group and corporate buyers leveraged bulk bookings and private-screening demand to secure notable discounts and bundled add-ons, using volume and repeat contracts to push pricing down; their lead-time and exclusivity requirements intensified capacity planning across Major Cineplex venues, while a wider corporate client mix reduced dependence on any single buyer.

- Bulk bookings: discount leverage

- Volume grants pricing/add-ons power

- Lead time/exclusivity strains capacity

- Diversified clients lower concentration risk

Geographic convenience

Proximity of Major Cineplex locations in Bangkok cores (metro population ~10.8 million in 2024) reduces customer bargaining power as malls and transit lower switching costs, though single‑multiplex towns leave patrons with limited choice. In central Bangkok multiple complexes drive cross‑shopping, raising price sensitivity. Parking, safety and onsite amenities often decide venue choice beyond ticket price.

- Convenience lowers bargaining power

- Single‑multiplex areas = limited choice

- Bangkok cores = higher cross‑shopping

- Amenities (parking, safety, F&B) sway selection

Outside Bangkok price sensitivity vs premium formats and memberships shaping buyer power

Customers are price sensitive outside Bangkok (Thailand pop ~71m in 2024) while premium formats sustain willingness to pay; low switching costs to SVoD (1bn subs by 2024) and gaming (>$200bn 2023) boost buyer power. Memberships and corporate bulk bookings reduce elasticity; Bangkok metro (~10.8m 2024) convenience lowers bargaining leverage.

| Metric | 2023–24 |

|---|---|

| Thailand pop | ~71m (2024) |

| Bangkok metro | ~10.8m (2024) |

| SVoD subs | ~1bn (2024) |

| Gaming revenue | >$200bn (2023) |

Preview Before You Purchase

Major Cineplex Group Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Major Cineplex Group is the full, professionally formatted document you’re previewing and the exact file the customer will receive after purchase. It lays out competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications in ready-to-use form. No placeholders or samples—instant download upon payment.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Major Cineplex faces moderate buyer power, strong substitutability from streaming and entertainment, and significant rivalry within Thailand's cinema market, while supplier influence and entry barriers vary by location and scale. This snapshot teases critical dynamics—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic recommendations to inform investment or strategy.

Suppliers Bargaining Power

Studio content concentration

Major depends on a concentrated set of Hollywood studios and key Thai producers for tentpole releases, giving suppliers leverage over rental terms and theatrical windowing in 2024.

Major’s distribution arm partially offsets this by securing local content and negotiating package deals to smooth supply risk.

Seasonal blockbuster slates in 2024 can still swing bargaining power firmly toward suppliers during peak periods.

Premium tech vendors

Premium tech vendors such as IMAX, 4DX, Dolby and laser projection suppliers are few and highly specialized, raising switching costs and granting pricing power. Vendor certification and multi‑year service contracts (typically 3–7 years) lock in terms and maintenance fees. Major Cineplex, as Thailand’s largest exhibitor with market share above 50%, gains negotiating leverage, but true alternatives for flagship formats remain limited.

Real estate and mall partners

Cinema locations hinge on prime mall anchors and long leases (often 10–20 years), giving landlords leverage via rent hikes, mall revamps and co‑marketing clauses; Major Cineplex, with over 500 screens across 120+ sites as of 2024, mitigates this by spreading risk across a multi‑site portfolio and acting as an anchor traffic driver, while landlord power eases in secondary cities where tenant mix needs boost Major’s negotiating leverage.

F&B and concession inputs

Popcorn, beverage and packaging inputs for Major Cineplex face wide supplier pools, reducing individual supplier leverage as many inputs are commodity-like and can be multi-sourced. Branded beverage deals still carry minimums and co-marketing obligations that restrict flexibility. Inflation spikes in input costs often pass through with a lag, compressing concession margins until pricing and cost recovery align.

- Broad supplier base — low switching cost

- Commoditized inputs — multi-sourcing possible

- Branded drinks — minimums and marketing tie-ins

- Inflation pass-through lag — margin pressure

Utilities and labor

Electricity for HVAC, projection and LED screens plus skilled projection technicians are essential for Major Cineplex; commercial tariffs in Thailand rose to about 5.0 THB/kWh in 2024, constraining margins while utility monopolies limit negotiation. Labor markets are moderately competitive, with certified projection and premium-format training adding incremental wages ~5–8% above base pay. Automation and optimized scheduling have begun reducing technician hours and softening supplier leverage.

- Essential inputs: electricity, skilled technicians

- 2024 tariff: ~5.0 THB/kWh

- Training premium: +5–8% wage cost

- Mitigants: automation, scheduling

Moderate supplier power: exhibitor scale offsets studio/tech leverage, tariffs and wage pressures

Supplier power is moderate: Hollywood studios and tech vendors (IMAX/4DX) exert strong leverage during blockbusters and for premium formats, while Major’s >50% market share, 500+ screens (120+ sites) and in‑house distribution mitigate some risk. Long mall leases (10–20 yrs) and utility tariffs (~5.0 THB/kWh) constrain flexibility; concessions inputs remain low‑power but branded deals and wage premiums (+5–8%) limit pass‑through.

| Factor | 2024 Metric |

|---|---|

| Market share | >50% |

| Screens/sites | 500+/120+ |

| Tariff | ~5.0 THB/kWh |

| Technician wage premium | +5–8% |

What is included in the product

Tailored Porter's Five Forces analysis for Major Cineplex Group uncovering competitive rivalry, buyer and supplier leverage, threats from new entrants and substitutes, and strategic barriers that shape pricing, profitability, and market resilience.

A concise one-sheet Porter's Five Forces for Major Cineplex Group—instantly highlights competitive intensity, supplier and buyer power, and substitute/entry threats to relieve analysis bottlenecks. Clean, slide-ready layout with adjustable pressure levels so teams can tailor scenarios and make faster strategic decisions.

Customers Bargaining Power

Price sensitivity and elasticity

Thai moviegoers are value conscious, especially outside Bangkok, where urban concentration and a 2024 population of about 71 million shape demand sensitivity; Major Cineplex, Thailand's largest operator, sees ticket volumes react to price, promotions and content quality. Premium formats (VIP/IMAX) sustain a notable willingness to pay, while standard screens face discount pressure; family bundles and off‑peak pricing cut churn.

Abundant entertainment choices

Customers can switch to streaming, gaming, or dining with minimal friction as global SVoD subscriptions topped 1 billion by 2024 and gaming revenues exceeded $200 billion in 2023, raising buyer power for casual visits. Low switching costs push price sensitivity; experiential differentiation — premium seating, F&B, IMAX — is key to avoid price-based comparison. Event cinema, theatrical exclusives and limited windows reduce substitutability and strengthen retention.

Loyalty and membership programs

Major Cineplex's memberships, points and tiered benefits lock in repeat visits by creating switching costs and raising lifetime value; data-driven personalized offers in 2024 have reduced effective buyer power through targeted discounts and upsells. Corporate and student segments are fenced with tailored pricing and bulk packages, while weak engagement or low redemption rates would increase churn and shift bargaining leverage back to customers.

Group and corporate buyers

In 2024 group and corporate buyers leveraged bulk bookings and private-screening demand to secure notable discounts and bundled add-ons, using volume and repeat contracts to push pricing down; their lead-time and exclusivity requirements intensified capacity planning across Major Cineplex venues, while a wider corporate client mix reduced dependence on any single buyer.

- Bulk bookings: discount leverage

- Volume grants pricing/add-ons power

- Lead time/exclusivity strains capacity

- Diversified clients lower concentration risk

Geographic convenience

Proximity of Major Cineplex locations in Bangkok cores (metro population ~10.8 million in 2024) reduces customer bargaining power as malls and transit lower switching costs, though single‑multiplex towns leave patrons with limited choice. In central Bangkok multiple complexes drive cross‑shopping, raising price sensitivity. Parking, safety and onsite amenities often decide venue choice beyond ticket price.

- Convenience lowers bargaining power

- Single‑multiplex areas = limited choice

- Bangkok cores = higher cross‑shopping

- Amenities (parking, safety, F&B) sway selection

Outside Bangkok price sensitivity vs premium formats and memberships shaping buyer power

Customers are price sensitive outside Bangkok (Thailand pop ~71m in 2024) while premium formats sustain willingness to pay; low switching costs to SVoD (1bn subs by 2024) and gaming (>$200bn 2023) boost buyer power. Memberships and corporate bulk bookings reduce elasticity; Bangkok metro (~10.8m 2024) convenience lowers bargaining leverage.

| Metric | 2023–24 |

|---|---|

| Thailand pop | ~71m (2024) |

| Bangkok metro | ~10.8m (2024) |

| SVoD subs | ~1bn (2024) |

| Gaming revenue | >$200bn (2023) |

Preview Before You Purchase

Major Cineplex Group Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Major Cineplex Group is the full, professionally formatted document you’re previewing and the exact file the customer will receive after purchase. It lays out competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications in ready-to-use form. No placeholders or samples—instant download upon payment.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Major Cineplex faces moderate buyer power, strong substitutability from streaming and entertainment, and significant rivalry within Thailand's cinema market, while supplier influence and entry barriers vary by location and scale. This snapshot teases critical dynamics—unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and strategic recommendations to inform investment or strategy.

Suppliers Bargaining Power

Studio content concentration

Major depends on a concentrated set of Hollywood studios and key Thai producers for tentpole releases, giving suppliers leverage over rental terms and theatrical windowing in 2024.

Major’s distribution arm partially offsets this by securing local content and negotiating package deals to smooth supply risk.

Seasonal blockbuster slates in 2024 can still swing bargaining power firmly toward suppliers during peak periods.

Premium tech vendors

Premium tech vendors such as IMAX, 4DX, Dolby and laser projection suppliers are few and highly specialized, raising switching costs and granting pricing power. Vendor certification and multi‑year service contracts (typically 3–7 years) lock in terms and maintenance fees. Major Cineplex, as Thailand’s largest exhibitor with market share above 50%, gains negotiating leverage, but true alternatives for flagship formats remain limited.

Real estate and mall partners

Cinema locations hinge on prime mall anchors and long leases (often 10–20 years), giving landlords leverage via rent hikes, mall revamps and co‑marketing clauses; Major Cineplex, with over 500 screens across 120+ sites as of 2024, mitigates this by spreading risk across a multi‑site portfolio and acting as an anchor traffic driver, while landlord power eases in secondary cities where tenant mix needs boost Major’s negotiating leverage.

F&B and concession inputs

Popcorn, beverage and packaging inputs for Major Cineplex face wide supplier pools, reducing individual supplier leverage as many inputs are commodity-like and can be multi-sourced. Branded beverage deals still carry minimums and co-marketing obligations that restrict flexibility. Inflation spikes in input costs often pass through with a lag, compressing concession margins until pricing and cost recovery align.

- Broad supplier base — low switching cost

- Commoditized inputs — multi-sourcing possible

- Branded drinks — minimums and marketing tie-ins

- Inflation pass-through lag — margin pressure

Utilities and labor

Electricity for HVAC, projection and LED screens plus skilled projection technicians are essential for Major Cineplex; commercial tariffs in Thailand rose to about 5.0 THB/kWh in 2024, constraining margins while utility monopolies limit negotiation. Labor markets are moderately competitive, with certified projection and premium-format training adding incremental wages ~5–8% above base pay. Automation and optimized scheduling have begun reducing technician hours and softening supplier leverage.

- Essential inputs: electricity, skilled technicians

- 2024 tariff: ~5.0 THB/kWh

- Training premium: +5–8% wage cost

- Mitigants: automation, scheduling

Moderate supplier power: exhibitor scale offsets studio/tech leverage, tariffs and wage pressures

Supplier power is moderate: Hollywood studios and tech vendors (IMAX/4DX) exert strong leverage during blockbusters and for premium formats, while Major’s >50% market share, 500+ screens (120+ sites) and in‑house distribution mitigate some risk. Long mall leases (10–20 yrs) and utility tariffs (~5.0 THB/kWh) constrain flexibility; concessions inputs remain low‑power but branded deals and wage premiums (+5–8%) limit pass‑through.

| Factor | 2024 Metric |

|---|---|

| Market share | >50% |

| Screens/sites | 500+/120+ |

| Tariff | ~5.0 THB/kWh |

| Technician wage premium | +5–8% |

What is included in the product

Tailored Porter's Five Forces analysis for Major Cineplex Group uncovering competitive rivalry, buyer and supplier leverage, threats from new entrants and substitutes, and strategic barriers that shape pricing, profitability, and market resilience.

A concise one-sheet Porter's Five Forces for Major Cineplex Group—instantly highlights competitive intensity, supplier and buyer power, and substitute/entry threats to relieve analysis bottlenecks. Clean, slide-ready layout with adjustable pressure levels so teams can tailor scenarios and make faster strategic decisions.

Customers Bargaining Power

Price sensitivity and elasticity

Thai moviegoers are value conscious, especially outside Bangkok, where urban concentration and a 2024 population of about 71 million shape demand sensitivity; Major Cineplex, Thailand's largest operator, sees ticket volumes react to price, promotions and content quality. Premium formats (VIP/IMAX) sustain a notable willingness to pay, while standard screens face discount pressure; family bundles and off‑peak pricing cut churn.

Abundant entertainment choices

Customers can switch to streaming, gaming, or dining with minimal friction as global SVoD subscriptions topped 1 billion by 2024 and gaming revenues exceeded $200 billion in 2023, raising buyer power for casual visits. Low switching costs push price sensitivity; experiential differentiation — premium seating, F&B, IMAX — is key to avoid price-based comparison. Event cinema, theatrical exclusives and limited windows reduce substitutability and strengthen retention.

Loyalty and membership programs

Major Cineplex's memberships, points and tiered benefits lock in repeat visits by creating switching costs and raising lifetime value; data-driven personalized offers in 2024 have reduced effective buyer power through targeted discounts and upsells. Corporate and student segments are fenced with tailored pricing and bulk packages, while weak engagement or low redemption rates would increase churn and shift bargaining leverage back to customers.

Group and corporate buyers

In 2024 group and corporate buyers leveraged bulk bookings and private-screening demand to secure notable discounts and bundled add-ons, using volume and repeat contracts to push pricing down; their lead-time and exclusivity requirements intensified capacity planning across Major Cineplex venues, while a wider corporate client mix reduced dependence on any single buyer.

- Bulk bookings: discount leverage

- Volume grants pricing/add-ons power

- Lead time/exclusivity strains capacity

- Diversified clients lower concentration risk

Geographic convenience

Proximity of Major Cineplex locations in Bangkok cores (metro population ~10.8 million in 2024) reduces customer bargaining power as malls and transit lower switching costs, though single‑multiplex towns leave patrons with limited choice. In central Bangkok multiple complexes drive cross‑shopping, raising price sensitivity. Parking, safety and onsite amenities often decide venue choice beyond ticket price.

- Convenience lowers bargaining power

- Single‑multiplex areas = limited choice

- Bangkok cores = higher cross‑shopping

- Amenities (parking, safety, F&B) sway selection

Outside Bangkok price sensitivity vs premium formats and memberships shaping buyer power

Customers are price sensitive outside Bangkok (Thailand pop ~71m in 2024) while premium formats sustain willingness to pay; low switching costs to SVoD (1bn subs by 2024) and gaming (>$200bn 2023) boost buyer power. Memberships and corporate bulk bookings reduce elasticity; Bangkok metro (~10.8m 2024) convenience lowers bargaining leverage.

| Metric | 2023–24 |

|---|---|

| Thailand pop | ~71m (2024) |

| Bangkok metro | ~10.8m (2024) |

| SVoD subs | ~1bn (2024) |

| Gaming revenue | >$200bn (2023) |

Preview Before You Purchase

Major Cineplex Group Porter's Five Forces Analysis

This Porter’s Five Forces analysis of Major Cineplex Group is the full, professionally formatted document you’re previewing and the exact file the customer will receive after purchase. It lays out competitive rivalry, supplier and buyer power, threats of entry and substitutes, and strategic implications in ready-to-use form. No placeholders or samples—instant download upon payment.