Making Science Porter's Five Forces Analysis

From Overview to Strategy Blueprint

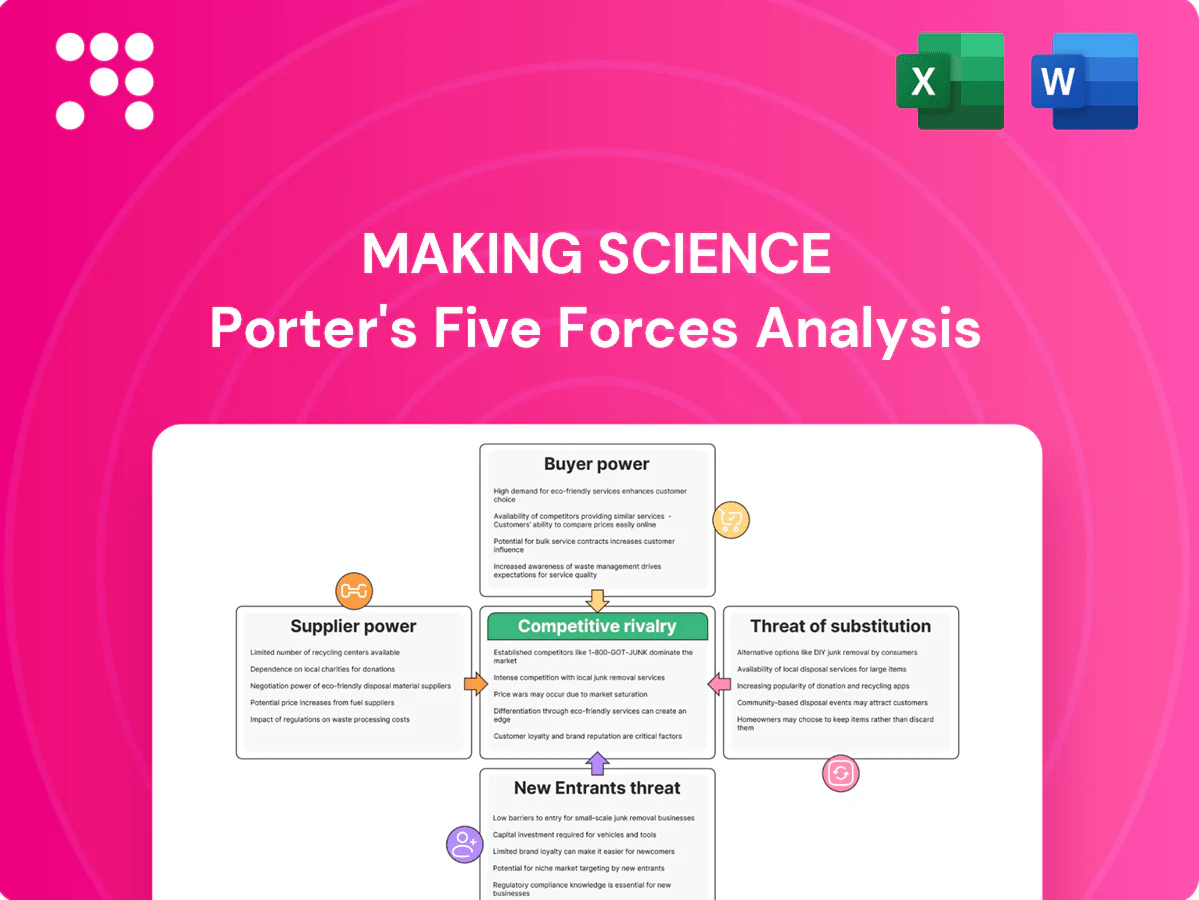

Making Science faces varying buyer power, evolving tech threats, and supplier dynamics that shape its market positioning; this snapshot highlights key pressures and strategic levers. The full Porter's Five Forces Analysis drills into each force with ratings, visuals, and implications. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Reliance on hyperscalers

Cloud platforms concentrate supplier power: AWS (~32% global IaaS market), Azure (~23%) and GCP (~11%) in 2024 control pricing, certification and partner tiers. Contractual SLAs commonly promise 99.95–99.99% uptime while egress fees (≈0.09 USD/GB first 10 TB on major providers) raise switching costs. Bundled credits and co‑selling offsets reduce near‑term rates but deepen dependency. 92% of enterprises report multi‑cloud use, which can rebalance leverage.

Ad & martech platform gatekeepers

Ad and martech gatekeepers—Google, Meta and TikTok—plus leading DSP/CDP vendors control inventory, APIs and measurement; eMarketer estimated Google and Meta held roughly 60% of global digital ad spend in 2024. Policy shifts and signal loss (privacy, cookies) can change performance economics overnight, as seen after ATT. Preferred partner status grants access and support but ties roadmaps to platform priorities. Building proprietary analytics layers and first‑party measurement helps buffer policy shocks.

Specialized talent as a supplier

Senior cloud engineers, data scientists and performance marketers act as scarce suppliers for Making Science, with tech attrition running around 20% in 2023–24 and wage inflation pressuring margins by roughly 10–15% in the same period. Upskilling pipelines and nearshore/offshore delivery lower dependency on expensive local hires and can cut delivery costs. Strengthening employer brand and clear career paths improve negotiation leverage and reduce churn.

Data providers and identity graphs

Audience data, consent tools and ID solutions are critical for activation; privacy shifts and third-party cookie deprecation (Google delay to 2025) plus Apple ATT driving IDFA opt-in near 25% increase reliance on consented, high-quality sources. Volume commitments can secure discounts but create contractual lock-ins; robust first-party data strategies cut external supplier leverage and cost pressure.

- Consented data premiums: higher activation rates, up to 2x CPMs

- IDFA opt-in ~25% (post-ATT)

- Google cookie phase-out moved to 2025

- Volume commitments = price relief vs. contractual risk

Software stack fragmentation

Multiple point solutions (attribution, CMS, testing, CDP) increase integration complexity and give vendors leverage via proprietary connectors and usage‑based fees; the martech landscape exceeded 10,000 solutions by 2024 (ChiefMartec), amplifying fragmentation. Standardizing on interoperable architectures and rationalizing vendors strengthens Making Science’s negotiation stance and limits lock‑in.

- Fragmentation: >10,000 martech vendors (2024)

- Supplier power: proprietary connectors, usage fees

- Defense: interoperable architectures

- Action: strategic vendor rationalization

Supplier power: Cloud 32/23/11% | Ads ~60% | Attrition ~20%

Supplier power is high: cloud platforms (AWS 32%, Azure 23%, GCP 11% in 2024) set pricing and egress fees; ad gatekeepers (Google+Meta ~60% ad spend) control inventory; talent attrition ~20% with 10–15% wage pressure; martech fragmentation >10,000 vendors raises integration lock‑in.

| Supplier | Key metric | Impact |

|---|---|---|

| Cloud | AWS 32% / Azure 23% / GCP 11% (2024) | High pricing power |

| Ad | Google+Meta ~60% (2024) | Inventory/control risk |

| Talent | Attrition ~20% | Cost pressure |

| Martech | >10,000 vendors (2024) | Integration lock‑in |

What is included in the product

Tailored Porter's Five Forces analysis for Making Science that uncovers competitive drivers, buyer and supplier power, threat of new entrants and substitutes, and identifies disruptive trends and strategic levers to protect market share and inform investor or internal strategy materials.

A concise one-sheet Porter's Five Forces for Making Science that visualizes competitive pressure with an editable radar chart, customizable inputs for evolving market conditions, and a clean layout ready for pitch decks or boardroom use—no macros or finance expertise required.

Customers Bargaining Power

Enterprise multi-homing

Enterprise multi-homing is widespread: 65% of enterprise marketers used three or more agencies in 2024, intensifying price competition and driving down margins.

RFP-driven procurement with comparable scopes and transparent rate-cards increases commoditization, while differentiation through measurable outcomes, proprietary IP and certifications lowers direct price-only comparisons.

Adopting performance-based pricing — now present in roughly 20% of digital marketing contracts in 2024 — helps align incentives and reduces client switching.

Switching costs via integration

Deep cloud, data and media integrations raise replacement friction for Making Science, as global public cloud spending reached about $600 billion in 2024, increasing platform lock-in and partner dependency. Documented architectures and reusable assets facilitate buyer onboarding while protecting incumbency. Long-term MSAs with milestones and clear ROI attribution cement retention and stabilize revenue.

Price sensitivity in marketing spend

Marketing and transformation budgets cycle with macro conditions, averaging about 10% of company revenue in 2024 per the CMO Survey, driving procurement caution. Buyers push for efficiency and consolidate vendors to capture scale benefits, compressing rates. Packaging managed services into productized solutions blunts rate pressure while benchmarking and case studies support value-based pricing.

Global-local delivery expectations

International clients demand consistent global standards with local-market nuance; in 2024, 65% of enterprise buyers prioritized regional compliance when selecting vendors. Buyers use footprint requirements to negotiate rates or split awards by region, increasing bargaining power. Hybrid delivery (onshore strategy, nearshore build) boosts responsiveness and cuts cost; local certifications and language capabilities reduce buyer leverage.

- footprint-leverage: regional sourcing used to lower fees

- hybrid-model: onshore+nearshore improves speed/cost

- local-cert+language: lowers buyer negotiating power

Demand for measurable outcomes

Clients now demand clear KPI lifts across CAC, LTV, ROAS and time-to-value, with industry benchmarks (digital ROAS ~4x) used to validate performance; transparent dashboards and MMM/MTA increase trust but make underperformance visible. Shared OKRs and test-and-learn roadmaps keep engagement sticky, while well-scoped contractual outcome clauses protect margins and align incentives.

- Demand: measurable KPI lift

- Visibility: dashboards + MMM/MTA

- Engagement: shared OKRs, test-and-learn

- Risk mgmt: scoped outcome clauses

65% multi-homing squeezes margins while $600B cloud spend raises switching costs

Customers exert high bargaining power: 65% multi-home in 2024, driving price pressure and margin compression.

Transparent RFPs and benchmarks (digital ROAS ~4x) commoditize services, though 20% of contracts use performance pricing to align incentives.

Cloud integration ($600B public cloud spend 2024) and long MSAs raise switching costs, while 65% of buyers demand regional compliance.

| Metric | 2024 |

|---|---|

| Multi-homing | 65% |

| Performance pricing | 20% |

| Public cloud spend | $600B |

| Marketing budget (% rev) | ~10% |

| Regional compliance focus | 65% |

What You See Is What You Get

Making Science Porter's Five Forces Analysis

This preview shows the complete Making Science Porter's Five Forces Analysis — the exact, fully formatted document you will receive immediately after purchase. No placeholders, no samples: what you see is the final deliverable, ready for download and use. Instant access upon payment, with professional analysis and actionable insights included.

From Overview to Strategy Blueprint

Making Science faces varying buyer power, evolving tech threats, and supplier dynamics that shape its market positioning; this snapshot highlights key pressures and strategic levers. The full Porter's Five Forces Analysis drills into each force with ratings, visuals, and implications. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Reliance on hyperscalers

Cloud platforms concentrate supplier power: AWS (~32% global IaaS market), Azure (~23%) and GCP (~11%) in 2024 control pricing, certification and partner tiers. Contractual SLAs commonly promise 99.95–99.99% uptime while egress fees (≈0.09 USD/GB first 10 TB on major providers) raise switching costs. Bundled credits and co‑selling offsets reduce near‑term rates but deepen dependency. 92% of enterprises report multi‑cloud use, which can rebalance leverage.

Ad & martech platform gatekeepers

Ad and martech gatekeepers—Google, Meta and TikTok—plus leading DSP/CDP vendors control inventory, APIs and measurement; eMarketer estimated Google and Meta held roughly 60% of global digital ad spend in 2024. Policy shifts and signal loss (privacy, cookies) can change performance economics overnight, as seen after ATT. Preferred partner status grants access and support but ties roadmaps to platform priorities. Building proprietary analytics layers and first‑party measurement helps buffer policy shocks.

Specialized talent as a supplier

Senior cloud engineers, data scientists and performance marketers act as scarce suppliers for Making Science, with tech attrition running around 20% in 2023–24 and wage inflation pressuring margins by roughly 10–15% in the same period. Upskilling pipelines and nearshore/offshore delivery lower dependency on expensive local hires and can cut delivery costs. Strengthening employer brand and clear career paths improve negotiation leverage and reduce churn.

Data providers and identity graphs

Audience data, consent tools and ID solutions are critical for activation; privacy shifts and third-party cookie deprecation (Google delay to 2025) plus Apple ATT driving IDFA opt-in near 25% increase reliance on consented, high-quality sources. Volume commitments can secure discounts but create contractual lock-ins; robust first-party data strategies cut external supplier leverage and cost pressure.

- Consented data premiums: higher activation rates, up to 2x CPMs

- IDFA opt-in ~25% (post-ATT)

- Google cookie phase-out moved to 2025

- Volume commitments = price relief vs. contractual risk

Software stack fragmentation

Multiple point solutions (attribution, CMS, testing, CDP) increase integration complexity and give vendors leverage via proprietary connectors and usage‑based fees; the martech landscape exceeded 10,000 solutions by 2024 (ChiefMartec), amplifying fragmentation. Standardizing on interoperable architectures and rationalizing vendors strengthens Making Science’s negotiation stance and limits lock‑in.

- Fragmentation: >10,000 martech vendors (2024)

- Supplier power: proprietary connectors, usage fees

- Defense: interoperable architectures

- Action: strategic vendor rationalization

Supplier power: Cloud 32/23/11% | Ads ~60% | Attrition ~20%

Supplier power is high: cloud platforms (AWS 32%, Azure 23%, GCP 11% in 2024) set pricing and egress fees; ad gatekeepers (Google+Meta ~60% ad spend) control inventory; talent attrition ~20% with 10–15% wage pressure; martech fragmentation >10,000 vendors raises integration lock‑in.

| Supplier | Key metric | Impact |

|---|---|---|

| Cloud | AWS 32% / Azure 23% / GCP 11% (2024) | High pricing power |

| Ad | Google+Meta ~60% (2024) | Inventory/control risk |

| Talent | Attrition ~20% | Cost pressure |

| Martech | >10,000 vendors (2024) | Integration lock‑in |

What is included in the product

Tailored Porter's Five Forces analysis for Making Science that uncovers competitive drivers, buyer and supplier power, threat of new entrants and substitutes, and identifies disruptive trends and strategic levers to protect market share and inform investor or internal strategy materials.

A concise one-sheet Porter's Five Forces for Making Science that visualizes competitive pressure with an editable radar chart, customizable inputs for evolving market conditions, and a clean layout ready for pitch decks or boardroom use—no macros or finance expertise required.

Customers Bargaining Power

Enterprise multi-homing

Enterprise multi-homing is widespread: 65% of enterprise marketers used three or more agencies in 2024, intensifying price competition and driving down margins.

RFP-driven procurement with comparable scopes and transparent rate-cards increases commoditization, while differentiation through measurable outcomes, proprietary IP and certifications lowers direct price-only comparisons.

Adopting performance-based pricing — now present in roughly 20% of digital marketing contracts in 2024 — helps align incentives and reduces client switching.

Switching costs via integration

Deep cloud, data and media integrations raise replacement friction for Making Science, as global public cloud spending reached about $600 billion in 2024, increasing platform lock-in and partner dependency. Documented architectures and reusable assets facilitate buyer onboarding while protecting incumbency. Long-term MSAs with milestones and clear ROI attribution cement retention and stabilize revenue.

Price sensitivity in marketing spend

Marketing and transformation budgets cycle with macro conditions, averaging about 10% of company revenue in 2024 per the CMO Survey, driving procurement caution. Buyers push for efficiency and consolidate vendors to capture scale benefits, compressing rates. Packaging managed services into productized solutions blunts rate pressure while benchmarking and case studies support value-based pricing.

Global-local delivery expectations

International clients demand consistent global standards with local-market nuance; in 2024, 65% of enterprise buyers prioritized regional compliance when selecting vendors. Buyers use footprint requirements to negotiate rates or split awards by region, increasing bargaining power. Hybrid delivery (onshore strategy, nearshore build) boosts responsiveness and cuts cost; local certifications and language capabilities reduce buyer leverage.

- footprint-leverage: regional sourcing used to lower fees

- hybrid-model: onshore+nearshore improves speed/cost

- local-cert+language: lowers buyer negotiating power

Demand for measurable outcomes

Clients now demand clear KPI lifts across CAC, LTV, ROAS and time-to-value, with industry benchmarks (digital ROAS ~4x) used to validate performance; transparent dashboards and MMM/MTA increase trust but make underperformance visible. Shared OKRs and test-and-learn roadmaps keep engagement sticky, while well-scoped contractual outcome clauses protect margins and align incentives.

- Demand: measurable KPI lift

- Visibility: dashboards + MMM/MTA

- Engagement: shared OKRs, test-and-learn

- Risk mgmt: scoped outcome clauses

65% multi-homing squeezes margins while $600B cloud spend raises switching costs

Customers exert high bargaining power: 65% multi-home in 2024, driving price pressure and margin compression.

Transparent RFPs and benchmarks (digital ROAS ~4x) commoditize services, though 20% of contracts use performance pricing to align incentives.

Cloud integration ($600B public cloud spend 2024) and long MSAs raise switching costs, while 65% of buyers demand regional compliance.

| Metric | 2024 |

|---|---|

| Multi-homing | 65% |

| Performance pricing | 20% |

| Public cloud spend | $600B |

| Marketing budget (% rev) | ~10% |

| Regional compliance focus | 65% |

What You See Is What You Get

Making Science Porter's Five Forces Analysis

This preview shows the complete Making Science Porter's Five Forces Analysis — the exact, fully formatted document you will receive immediately after purchase. No placeholders, no samples: what you see is the final deliverable, ready for download and use. Instant access upon payment, with professional analysis and actionable insights included.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Making Science faces varying buyer power, evolving tech threats, and supplier dynamics that shape its market positioning; this snapshot highlights key pressures and strategic levers. The full Porter's Five Forces Analysis drills into each force with ratings, visuals, and implications. Unlock the complete report to inform investment or strategic decisions.

Suppliers Bargaining Power

Reliance on hyperscalers

Cloud platforms concentrate supplier power: AWS (~32% global IaaS market), Azure (~23%) and GCP (~11%) in 2024 control pricing, certification and partner tiers. Contractual SLAs commonly promise 99.95–99.99% uptime while egress fees (≈0.09 USD/GB first 10 TB on major providers) raise switching costs. Bundled credits and co‑selling offsets reduce near‑term rates but deepen dependency. 92% of enterprises report multi‑cloud use, which can rebalance leverage.

Ad & martech platform gatekeepers

Ad and martech gatekeepers—Google, Meta and TikTok—plus leading DSP/CDP vendors control inventory, APIs and measurement; eMarketer estimated Google and Meta held roughly 60% of global digital ad spend in 2024. Policy shifts and signal loss (privacy, cookies) can change performance economics overnight, as seen after ATT. Preferred partner status grants access and support but ties roadmaps to platform priorities. Building proprietary analytics layers and first‑party measurement helps buffer policy shocks.

Specialized talent as a supplier

Senior cloud engineers, data scientists and performance marketers act as scarce suppliers for Making Science, with tech attrition running around 20% in 2023–24 and wage inflation pressuring margins by roughly 10–15% in the same period. Upskilling pipelines and nearshore/offshore delivery lower dependency on expensive local hires and can cut delivery costs. Strengthening employer brand and clear career paths improve negotiation leverage and reduce churn.

Data providers and identity graphs

Audience data, consent tools and ID solutions are critical for activation; privacy shifts and third-party cookie deprecation (Google delay to 2025) plus Apple ATT driving IDFA opt-in near 25% increase reliance on consented, high-quality sources. Volume commitments can secure discounts but create contractual lock-ins; robust first-party data strategies cut external supplier leverage and cost pressure.

- Consented data premiums: higher activation rates, up to 2x CPMs

- IDFA opt-in ~25% (post-ATT)

- Google cookie phase-out moved to 2025

- Volume commitments = price relief vs. contractual risk

Software stack fragmentation

Multiple point solutions (attribution, CMS, testing, CDP) increase integration complexity and give vendors leverage via proprietary connectors and usage‑based fees; the martech landscape exceeded 10,000 solutions by 2024 (ChiefMartec), amplifying fragmentation. Standardizing on interoperable architectures and rationalizing vendors strengthens Making Science’s negotiation stance and limits lock‑in.

- Fragmentation: >10,000 martech vendors (2024)

- Supplier power: proprietary connectors, usage fees

- Defense: interoperable architectures

- Action: strategic vendor rationalization

Supplier power: Cloud 32/23/11% | Ads ~60% | Attrition ~20%

Supplier power is high: cloud platforms (AWS 32%, Azure 23%, GCP 11% in 2024) set pricing and egress fees; ad gatekeepers (Google+Meta ~60% ad spend) control inventory; talent attrition ~20% with 10–15% wage pressure; martech fragmentation >10,000 vendors raises integration lock‑in.

| Supplier | Key metric | Impact |

|---|---|---|

| Cloud | AWS 32% / Azure 23% / GCP 11% (2024) | High pricing power |

| Ad | Google+Meta ~60% (2024) | Inventory/control risk |

| Talent | Attrition ~20% | Cost pressure |

| Martech | >10,000 vendors (2024) | Integration lock‑in |

What is included in the product

Tailored Porter's Five Forces analysis for Making Science that uncovers competitive drivers, buyer and supplier power, threat of new entrants and substitutes, and identifies disruptive trends and strategic levers to protect market share and inform investor or internal strategy materials.

A concise one-sheet Porter's Five Forces for Making Science that visualizes competitive pressure with an editable radar chart, customizable inputs for evolving market conditions, and a clean layout ready for pitch decks or boardroom use—no macros or finance expertise required.

Customers Bargaining Power

Enterprise multi-homing

Enterprise multi-homing is widespread: 65% of enterprise marketers used three or more agencies in 2024, intensifying price competition and driving down margins.

RFP-driven procurement with comparable scopes and transparent rate-cards increases commoditization, while differentiation through measurable outcomes, proprietary IP and certifications lowers direct price-only comparisons.

Adopting performance-based pricing — now present in roughly 20% of digital marketing contracts in 2024 — helps align incentives and reduces client switching.

Switching costs via integration

Deep cloud, data and media integrations raise replacement friction for Making Science, as global public cloud spending reached about $600 billion in 2024, increasing platform lock-in and partner dependency. Documented architectures and reusable assets facilitate buyer onboarding while protecting incumbency. Long-term MSAs with milestones and clear ROI attribution cement retention and stabilize revenue.

Price sensitivity in marketing spend

Marketing and transformation budgets cycle with macro conditions, averaging about 10% of company revenue in 2024 per the CMO Survey, driving procurement caution. Buyers push for efficiency and consolidate vendors to capture scale benefits, compressing rates. Packaging managed services into productized solutions blunts rate pressure while benchmarking and case studies support value-based pricing.

Global-local delivery expectations

International clients demand consistent global standards with local-market nuance; in 2024, 65% of enterprise buyers prioritized regional compliance when selecting vendors. Buyers use footprint requirements to negotiate rates or split awards by region, increasing bargaining power. Hybrid delivery (onshore strategy, nearshore build) boosts responsiveness and cuts cost; local certifications and language capabilities reduce buyer leverage.

- footprint-leverage: regional sourcing used to lower fees

- hybrid-model: onshore+nearshore improves speed/cost

- local-cert+language: lowers buyer negotiating power

Demand for measurable outcomes

Clients now demand clear KPI lifts across CAC, LTV, ROAS and time-to-value, with industry benchmarks (digital ROAS ~4x) used to validate performance; transparent dashboards and MMM/MTA increase trust but make underperformance visible. Shared OKRs and test-and-learn roadmaps keep engagement sticky, while well-scoped contractual outcome clauses protect margins and align incentives.

- Demand: measurable KPI lift

- Visibility: dashboards + MMM/MTA

- Engagement: shared OKRs, test-and-learn

- Risk mgmt: scoped outcome clauses

65% multi-homing squeezes margins while $600B cloud spend raises switching costs

Customers exert high bargaining power: 65% multi-home in 2024, driving price pressure and margin compression.

Transparent RFPs and benchmarks (digital ROAS ~4x) commoditize services, though 20% of contracts use performance pricing to align incentives.

Cloud integration ($600B public cloud spend 2024) and long MSAs raise switching costs, while 65% of buyers demand regional compliance.

| Metric | 2024 |

|---|---|

| Multi-homing | 65% |

| Performance pricing | 20% |

| Public cloud spend | $600B |

| Marketing budget (% rev) | ~10% |

| Regional compliance focus | 65% |

What You See Is What You Get

Making Science Porter's Five Forces Analysis

This preview shows the complete Making Science Porter's Five Forces Analysis — the exact, fully formatted document you will receive immediately after purchase. No placeholders, no samples: what you see is the final deliverable, ready for download and use. Instant access upon payment, with professional analysis and actionable insights included.