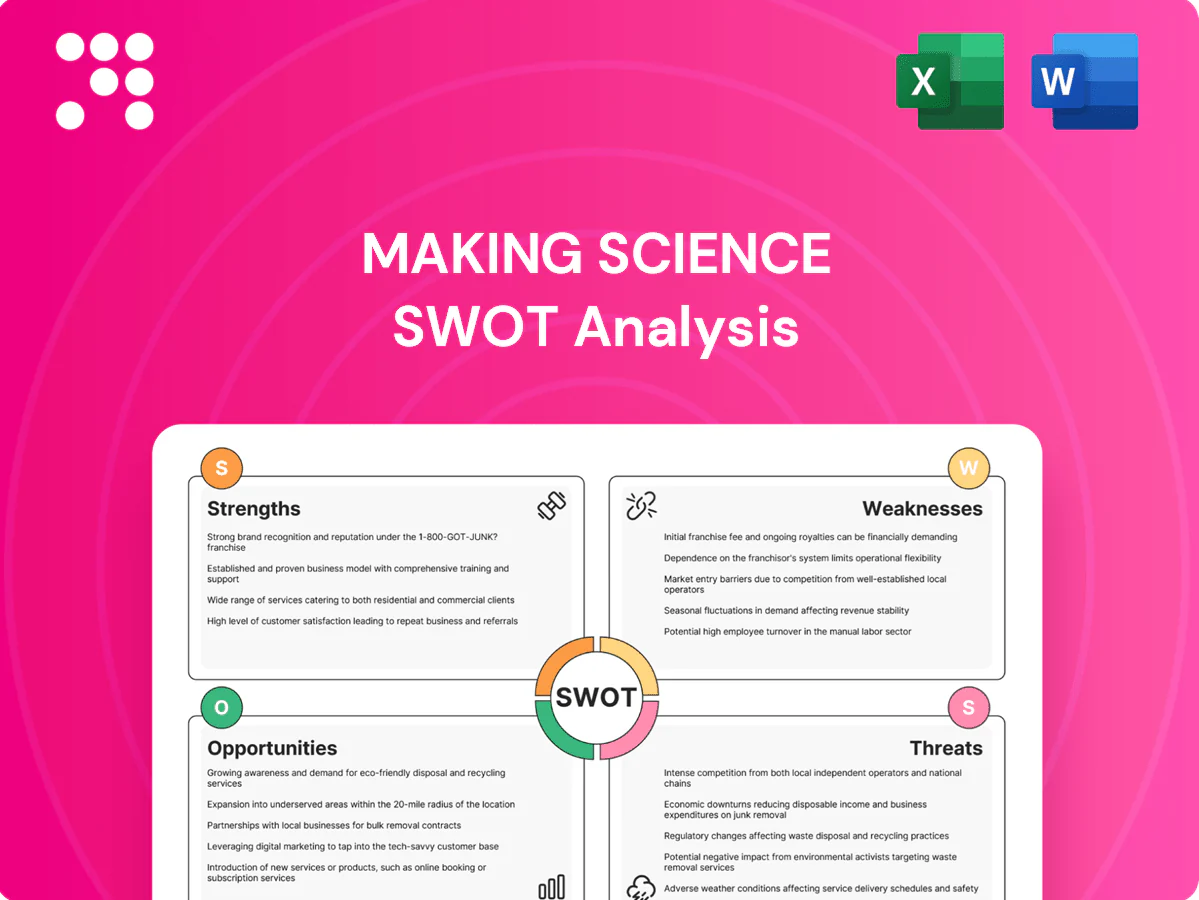

Making Science SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Discover the strategic forces shaping Making Science with our concise SWOT preview—strengths in data-driven services, market expansion opportunities, and digital transformation risks. Purchase the full SWOT to get a detailed, editable Word + Excel report with actionable insights for investors, consultants, and managers.

Strengths

Integrated tech + marketing suite

Integrated cloud, data, ads and ecommerce capabilities cut vendor sprawl in an ecosystem of ~10,000 martech vendors, speeding execution and reducing integration costs. Cross-functional teams align media, martech and data architecture to deliver unified KPIs. Forrester notes unified measurement can boost marketing ROI by up to 30%, and clients value a single accountable partner from strategy through activation.

Data-driven execution

Deep analytics, attribution, and an experimentation culture deliver measurable growth through rigorous A/B testing and multichannel attribution models. First-party data strategies combined with AI-driven insights refine targeting and personalization at scale. Closed-loop reporting ties outcomes to spend, enhancing decision quality and reinforcing performance credibility with enterprise clients.

Digital transformation expertise

Making Science’s digital transformation expertise modernizes stacks, workflows and channels to shorten clients’ time-to-value, with deployments often completed up to 30% faster than legacy programs. Proven playbooks lower cloud migration and commerce enablement risk and cut migration timelines by ~25%. Structured change management and training drive adoption increases of 40–60%. Industry templates enable repeatable scaling across verticals.

Global reach, local depth

Global footprint combined with local market know-how enhances campaign relevance across diverse regions; regulatory and cultural fluency improves targeting and conversion rates. Follow-the-sun delivery model raises responsiveness and reduces time-to-action for clients. Multilingual teams simplify complex rollouts and stakeholder coordination.

- Local regulatory fluency

- Follow-the-sun responsiveness

- Multilingual rollout capability

Partnership ecosystem

Alliances with hyperscalers, ad platforms and SaaS vendors broaden Making Science’s technical scope and market credibility. Preferred partner status unlocks beta features and co-marketing, speeding GTM. Certified talent shortens implementation cycles and ecosystem positioning boosts deal flow; hyperscaler market share: AWS 33%, Azure 23%, GCP 11% (2023); global digital ad spend ≈$650B (2024).

- Hyperscaler alliances: expanded capabilities

- Preferred partner: betas + co-marketing

- Certified talent: faster deployments

- Ecosystem: increased inbound deal flow

Unified cloud, data & commerce cut vendor sprawl, boost marketing ROI +30%

Integrated cloud, ads, data and commerce capabilities cut vendor sprawl, deliver unified KPIs and can boost marketing ROI by up to 30% (Forrester). Rigorous analytics, A/B testing and first-party/AI insights drive measurable growth and closed-loop reporting ties outcomes to spend. Global delivery, hyperscaler alliances and certified talent shorten deployments (time-to-value ~30% faster; migrations ~25% faster) and raise adoption 40–60%.

| Metric | Value |

|---|---|

| Marketing ROI (unified measurement) | +30% (Forrester) |

| Time-to-value | -30% |

| Migration timelines | -25% |

| Adoption uplift | +40–60% |

| Global digital ad spend | $650B (2024) |

| Hyperscaler market share | AWS 33% / Azure 23% / GCP 11% (2023) |

What is included in the product

Provides a concise strategic overview of Making Science’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise, visual SWOT matrix tailored to Making Science for rapid identification of strategic gaps and pain points. Enables quick edits and stakeholder-ready summaries to streamline prioritization and decision-making.

Weaknesses

Scale vs. hyperscaler consultancies

Compared with global mega-consultancies that serve a $360bn management consulting market in 2024, Making Science’s delivery capacity and geographic depth are thinner, limiting eligibility for $10m+ mega-program bids and multi-year transformation scopes. Clients may therefore perceive higher execution risk, and rapid hiring surges to meet demand can strain quality control and program governance.

Margin pressure from media

Heavy media activation compresses margins as platform take rates commonly range 10-30%, and commoditization drives downward pricing pressure on programmatic buys.

Procurement-driven RFPs and benchmarking frequently squeeze retainers, often forcing agencies to cut fees by ~20-30% to win deals.

Dependence on performance fees increases revenue volatility quarter-to-quarter, prompting a strategic shift toward higher-value IP and SaaS offerings to stabilize margins.

Execution complexity

Operating across cloud, data, ads and commerce raises coordination overhead and aligns with McKinsey's finding that about 70% of large-scale digital transformations fail, driven often by execution complexity. Cross-practice handoffs create delays and scope creep; Standish's CHAOS Report notes only ~31% of IT projects are delivered on time, on budget, and with required features. Robust governance and standardized delivery kits are required to prevent misalignment that can erode client satisfaction and increase churn risk.

Client concentration risk

Client concentration risk: if revenue depends on a few enterprise accounts, a single churn event can cut material revenue and margins; renewals and upsells therefore become critical to stabilize cash flow and ARR. Diversifying across sectors and geographies reduces exposure to vertical or regional shocks. Robust customer success and demonstrable ROI are mandatory to protect renewal rates.

- focus on renewals

- upsell programs

- sector/geography diversification

- strengthen CS and value proof

IP and productization gaps

Services-led model scales roughly linearly with headcount, constraining operating leverage; limited proprietary accelerators/SaaS keep margins low — services peers show ~10–15% EBITDA vs SaaS peers 20–30% in 2024 benchmarks. Reusable frameworks must convert to billable efficiency; investment in repeatable IP is needed for margin expansion.

- Headcount-driven revenue

- Low proprietary IP

- Frameworks not fully billable

- Needs repeatable IP investment

Services-led firm: compressed margins from 10–30% take, ~20–30% fee cuts, client concentration risk

Making Science lacks mega-consultancy scale, limiting $10m+ deal eligibility and raising execution risk; rapid hiring can erode quality. Heavy media activation and platform take rates (10–30%) plus procurement pressure force fee cuts of ~20–30%, compressing margins. Services-led model yields ~10–15% EBITDA vs SaaS 20–30% (2024), constraining operating leverage. Client concentration can cause material revenue shocks on churn.

| Metric | 2024 Value | Impact |

|---|---|---|

| Platform take rates | 10–30% | Compress margins |

| Fee concessions | ~20–30% | Lower ASP |

| EBITDA (services) | 10–15% | Low leverage |

What You See Is What You Get

Making Science SWOT Analysis

This is the actual Making Science SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the structured, editable file included in your download. Purchase unlocks the complete, in-depth version immediately after checkout.

Go Beyond the Preview—Access the Full Strategic Report

Discover the strategic forces shaping Making Science with our concise SWOT preview—strengths in data-driven services, market expansion opportunities, and digital transformation risks. Purchase the full SWOT to get a detailed, editable Word + Excel report with actionable insights for investors, consultants, and managers.

Strengths

Integrated tech + marketing suite

Integrated cloud, data, ads and ecommerce capabilities cut vendor sprawl in an ecosystem of ~10,000 martech vendors, speeding execution and reducing integration costs. Cross-functional teams align media, martech and data architecture to deliver unified KPIs. Forrester notes unified measurement can boost marketing ROI by up to 30%, and clients value a single accountable partner from strategy through activation.

Data-driven execution

Deep analytics, attribution, and an experimentation culture deliver measurable growth through rigorous A/B testing and multichannel attribution models. First-party data strategies combined with AI-driven insights refine targeting and personalization at scale. Closed-loop reporting ties outcomes to spend, enhancing decision quality and reinforcing performance credibility with enterprise clients.

Digital transformation expertise

Making Science’s digital transformation expertise modernizes stacks, workflows and channels to shorten clients’ time-to-value, with deployments often completed up to 30% faster than legacy programs. Proven playbooks lower cloud migration and commerce enablement risk and cut migration timelines by ~25%. Structured change management and training drive adoption increases of 40–60%. Industry templates enable repeatable scaling across verticals.

Global reach, local depth

Global footprint combined with local market know-how enhances campaign relevance across diverse regions; regulatory and cultural fluency improves targeting and conversion rates. Follow-the-sun delivery model raises responsiveness and reduces time-to-action for clients. Multilingual teams simplify complex rollouts and stakeholder coordination.

- Local regulatory fluency

- Follow-the-sun responsiveness

- Multilingual rollout capability

Partnership ecosystem

Alliances with hyperscalers, ad platforms and SaaS vendors broaden Making Science’s technical scope and market credibility. Preferred partner status unlocks beta features and co-marketing, speeding GTM. Certified talent shortens implementation cycles and ecosystem positioning boosts deal flow; hyperscaler market share: AWS 33%, Azure 23%, GCP 11% (2023); global digital ad spend ≈$650B (2024).

- Hyperscaler alliances: expanded capabilities

- Preferred partner: betas + co-marketing

- Certified talent: faster deployments

- Ecosystem: increased inbound deal flow

Unified cloud, data & commerce cut vendor sprawl, boost marketing ROI +30%

Integrated cloud, ads, data and commerce capabilities cut vendor sprawl, deliver unified KPIs and can boost marketing ROI by up to 30% (Forrester). Rigorous analytics, A/B testing and first-party/AI insights drive measurable growth and closed-loop reporting ties outcomes to spend. Global delivery, hyperscaler alliances and certified talent shorten deployments (time-to-value ~30% faster; migrations ~25% faster) and raise adoption 40–60%.

| Metric | Value |

|---|---|

| Marketing ROI (unified measurement) | +30% (Forrester) |

| Time-to-value | -30% |

| Migration timelines | -25% |

| Adoption uplift | +40–60% |

| Global digital ad spend | $650B (2024) |

| Hyperscaler market share | AWS 33% / Azure 23% / GCP 11% (2023) |

What is included in the product

Provides a concise strategic overview of Making Science’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise, visual SWOT matrix tailored to Making Science for rapid identification of strategic gaps and pain points. Enables quick edits and stakeholder-ready summaries to streamline prioritization and decision-making.

Weaknesses

Scale vs. hyperscaler consultancies

Compared with global mega-consultancies that serve a $360bn management consulting market in 2024, Making Science’s delivery capacity and geographic depth are thinner, limiting eligibility for $10m+ mega-program bids and multi-year transformation scopes. Clients may therefore perceive higher execution risk, and rapid hiring surges to meet demand can strain quality control and program governance.

Margin pressure from media

Heavy media activation compresses margins as platform take rates commonly range 10-30%, and commoditization drives downward pricing pressure on programmatic buys.

Procurement-driven RFPs and benchmarking frequently squeeze retainers, often forcing agencies to cut fees by ~20-30% to win deals.

Dependence on performance fees increases revenue volatility quarter-to-quarter, prompting a strategic shift toward higher-value IP and SaaS offerings to stabilize margins.

Execution complexity

Operating across cloud, data, ads and commerce raises coordination overhead and aligns with McKinsey's finding that about 70% of large-scale digital transformations fail, driven often by execution complexity. Cross-practice handoffs create delays and scope creep; Standish's CHAOS Report notes only ~31% of IT projects are delivered on time, on budget, and with required features. Robust governance and standardized delivery kits are required to prevent misalignment that can erode client satisfaction and increase churn risk.

Client concentration risk

Client concentration risk: if revenue depends on a few enterprise accounts, a single churn event can cut material revenue and margins; renewals and upsells therefore become critical to stabilize cash flow and ARR. Diversifying across sectors and geographies reduces exposure to vertical or regional shocks. Robust customer success and demonstrable ROI are mandatory to protect renewal rates.

- focus on renewals

- upsell programs

- sector/geography diversification

- strengthen CS and value proof

IP and productization gaps

Services-led model scales roughly linearly with headcount, constraining operating leverage; limited proprietary accelerators/SaaS keep margins low — services peers show ~10–15% EBITDA vs SaaS peers 20–30% in 2024 benchmarks. Reusable frameworks must convert to billable efficiency; investment in repeatable IP is needed for margin expansion.

- Headcount-driven revenue

- Low proprietary IP

- Frameworks not fully billable

- Needs repeatable IP investment

Services-led firm: compressed margins from 10–30% take, ~20–30% fee cuts, client concentration risk

Making Science lacks mega-consultancy scale, limiting $10m+ deal eligibility and raising execution risk; rapid hiring can erode quality. Heavy media activation and platform take rates (10–30%) plus procurement pressure force fee cuts of ~20–30%, compressing margins. Services-led model yields ~10–15% EBITDA vs SaaS 20–30% (2024), constraining operating leverage. Client concentration can cause material revenue shocks on churn.

| Metric | 2024 Value | Impact |

|---|---|---|

| Platform take rates | 10–30% | Compress margins |

| Fee concessions | ~20–30% | Lower ASP |

| EBITDA (services) | 10–15% | Low leverage |

What You See Is What You Get

Making Science SWOT Analysis

This is the actual Making Science SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the structured, editable file included in your download. Purchase unlocks the complete, in-depth version immediately after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Discover the strategic forces shaping Making Science with our concise SWOT preview—strengths in data-driven services, market expansion opportunities, and digital transformation risks. Purchase the full SWOT to get a detailed, editable Word + Excel report with actionable insights for investors, consultants, and managers.

Strengths

Integrated tech + marketing suite

Integrated cloud, data, ads and ecommerce capabilities cut vendor sprawl in an ecosystem of ~10,000 martech vendors, speeding execution and reducing integration costs. Cross-functional teams align media, martech and data architecture to deliver unified KPIs. Forrester notes unified measurement can boost marketing ROI by up to 30%, and clients value a single accountable partner from strategy through activation.

Data-driven execution

Deep analytics, attribution, and an experimentation culture deliver measurable growth through rigorous A/B testing and multichannel attribution models. First-party data strategies combined with AI-driven insights refine targeting and personalization at scale. Closed-loop reporting ties outcomes to spend, enhancing decision quality and reinforcing performance credibility with enterprise clients.

Digital transformation expertise

Making Science’s digital transformation expertise modernizes stacks, workflows and channels to shorten clients’ time-to-value, with deployments often completed up to 30% faster than legacy programs. Proven playbooks lower cloud migration and commerce enablement risk and cut migration timelines by ~25%. Structured change management and training drive adoption increases of 40–60%. Industry templates enable repeatable scaling across verticals.

Global reach, local depth

Global footprint combined with local market know-how enhances campaign relevance across diverse regions; regulatory and cultural fluency improves targeting and conversion rates. Follow-the-sun delivery model raises responsiveness and reduces time-to-action for clients. Multilingual teams simplify complex rollouts and stakeholder coordination.

- Local regulatory fluency

- Follow-the-sun responsiveness

- Multilingual rollout capability

Partnership ecosystem

Alliances with hyperscalers, ad platforms and SaaS vendors broaden Making Science’s technical scope and market credibility. Preferred partner status unlocks beta features and co-marketing, speeding GTM. Certified talent shortens implementation cycles and ecosystem positioning boosts deal flow; hyperscaler market share: AWS 33%, Azure 23%, GCP 11% (2023); global digital ad spend ≈$650B (2024).

- Hyperscaler alliances: expanded capabilities

- Preferred partner: betas + co-marketing

- Certified talent: faster deployments

- Ecosystem: increased inbound deal flow

Unified cloud, data & commerce cut vendor sprawl, boost marketing ROI +30%

Integrated cloud, ads, data and commerce capabilities cut vendor sprawl, deliver unified KPIs and can boost marketing ROI by up to 30% (Forrester). Rigorous analytics, A/B testing and first-party/AI insights drive measurable growth and closed-loop reporting ties outcomes to spend. Global delivery, hyperscaler alliances and certified talent shorten deployments (time-to-value ~30% faster; migrations ~25% faster) and raise adoption 40–60%.

| Metric | Value |

|---|---|

| Marketing ROI (unified measurement) | +30% (Forrester) |

| Time-to-value | -30% |

| Migration timelines | -25% |

| Adoption uplift | +40–60% |

| Global digital ad spend | $650B (2024) |

| Hyperscaler market share | AWS 33% / Azure 23% / GCP 11% (2023) |

What is included in the product

Provides a concise strategic overview of Making Science’s internal strengths and weaknesses and external opportunities and threats, mapping competitive position, growth drivers, operational gaps, and market risks to inform strategic decisions.

Provides a concise, visual SWOT matrix tailored to Making Science for rapid identification of strategic gaps and pain points. Enables quick edits and stakeholder-ready summaries to streamline prioritization and decision-making.

Weaknesses

Scale vs. hyperscaler consultancies

Compared with global mega-consultancies that serve a $360bn management consulting market in 2024, Making Science’s delivery capacity and geographic depth are thinner, limiting eligibility for $10m+ mega-program bids and multi-year transformation scopes. Clients may therefore perceive higher execution risk, and rapid hiring surges to meet demand can strain quality control and program governance.

Margin pressure from media

Heavy media activation compresses margins as platform take rates commonly range 10-30%, and commoditization drives downward pricing pressure on programmatic buys.

Procurement-driven RFPs and benchmarking frequently squeeze retainers, often forcing agencies to cut fees by ~20-30% to win deals.

Dependence on performance fees increases revenue volatility quarter-to-quarter, prompting a strategic shift toward higher-value IP and SaaS offerings to stabilize margins.

Execution complexity

Operating across cloud, data, ads and commerce raises coordination overhead and aligns with McKinsey's finding that about 70% of large-scale digital transformations fail, driven often by execution complexity. Cross-practice handoffs create delays and scope creep; Standish's CHAOS Report notes only ~31% of IT projects are delivered on time, on budget, and with required features. Robust governance and standardized delivery kits are required to prevent misalignment that can erode client satisfaction and increase churn risk.

Client concentration risk

Client concentration risk: if revenue depends on a few enterprise accounts, a single churn event can cut material revenue and margins; renewals and upsells therefore become critical to stabilize cash flow and ARR. Diversifying across sectors and geographies reduces exposure to vertical or regional shocks. Robust customer success and demonstrable ROI are mandatory to protect renewal rates.

- focus on renewals

- upsell programs

- sector/geography diversification

- strengthen CS and value proof

IP and productization gaps

Services-led model scales roughly linearly with headcount, constraining operating leverage; limited proprietary accelerators/SaaS keep margins low — services peers show ~10–15% EBITDA vs SaaS peers 20–30% in 2024 benchmarks. Reusable frameworks must convert to billable efficiency; investment in repeatable IP is needed for margin expansion.

- Headcount-driven revenue

- Low proprietary IP

- Frameworks not fully billable

- Needs repeatable IP investment

Services-led firm: compressed margins from 10–30% take, ~20–30% fee cuts, client concentration risk

Making Science lacks mega-consultancy scale, limiting $10m+ deal eligibility and raising execution risk; rapid hiring can erode quality. Heavy media activation and platform take rates (10–30%) plus procurement pressure force fee cuts of ~20–30%, compressing margins. Services-led model yields ~10–15% EBITDA vs SaaS 20–30% (2024), constraining operating leverage. Client concentration can cause material revenue shocks on churn.

| Metric | 2024 Value | Impact |

|---|---|---|

| Platform take rates | 10–30% | Compress margins |

| Fee concessions | ~20–30% | Lower ASP |

| EBITDA (services) | 10–15% | Low leverage |

What You See Is What You Get

Making Science SWOT Analysis

This is the actual Making Science SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the structured, editable file included in your download. Purchase unlocks the complete, in-depth version immediately after checkout.