Manpower Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Manpower faces moderate buyer power and intense rivalry as global staffing markets compress margins, while supplier dependence on specialized talent and regulatory hurdles heighten barriers. Substitutes from automation and gig platforms pose growing threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Manpower’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Scarce skilled talent

High-demand specialists in IT, healthcare and engineering can dictate rates and terms; BLS projects software developers’ employment to grow 22% 2022–32, intensifying demand. Talent scarcity forces higher pay packages, compressing ManpowerGroup’s margin capture. Candidates with rare certifications increasingly accept direct offers or premium agencies, amplifying supplier power in tight 2024 labor markets.

Candidate multihoming

Candidate multihoming is rising as workers list on multiple platforms and agencies, reducing ManpowerGroup’s exclusivity on placements; ManpowerGroup’s 2024 Talent Shortage Survey noted 54% of employers still face hiring difficulties, intensifying competition for talent. Faster response times and better offers are required to secure commitment, since switching costs for candidates are minimal.

Recruiter and sourcer expertise

Experienced recruiters act as pivotal internal suppliers of placement capacity; 2024 surveys show recruiter scarcity contributes to roughly 45% of hiring delays, pushing compensation and retention costs up as firms chase talent. High mobility means losing star recruiters can reduce fill speed by up to 30% and lower client win rates, concentrating bargaining power within specialist teams and inflating agency margins.

Third‑party tech and data

Reliance on ATS/CRM vendors, major job boards and assessment providers raises costs and exposure; LinkedIn had 930M+ members in 2024, granting platform owners outsized leverage. API access or pricing changes by these platforms can materially worsen unit economics for recruiters and staffing firms. Preferred placement and pay-to-play algorithms give vendors negotiating power, and ongoing consolidation among HR tech firms tightens terms.

- ATS/CRM dependence: higher switching costs

- Platform scale: LinkedIn 930M+ (2024)

- API/pricing shocks: hit unit economics

- Consolidation: fewer vendor alternatives

Training and credential bodies

Training and credential bodies shape candidate readiness; WEF estimates 50% of workers need reskilling by 2025, increasing reliance on credentialing partners. Access to in-demand pathways restricts supply breadth while average US coding bootcamp tuition (~13,500 in 2024) feeds directly into talent costs. Exclusive programs narrow alternative sourcing and can raise hiring premiums.

- Certifiers affect placement readiness

- Reskilling need: 50% by 2025 (WEF)

- Avg bootcamp tuition ~13,500 (2024)

- Exclusive programs limit sourcing

Dev 22%, recruiter delays ≈45% squeeze staffing margins

High-demand specialists (software devs 22% projected growth 2022–32) and scarce recruiters (≈45% of hiring delays) drive up pay and contract leverage, compressing ManpowerGroup margins.

Candidate multihoming and low switching costs (54% of employers report shortages in 2024) reduce exclusivity and force faster, costlier offers.

Dependence on platforms (LinkedIn 930M+ users 2024), ATS vendors and credentialing bodies (WEF: 50% need reskilling by 2025) increases supplier bargaining power and unit-cost exposure.

| Metric | Value |

|---|---|

| Software dev growth | 22% (2022–32, BLS) |

| Employers facing shortages | 54% (2024) |

| Recruiter-related delays | ≈45% (2024) |

| LinkedIn users | 930M+ (2024) |

| Reskilling need | 50% by 2025 (WEF) |

What is included in the product

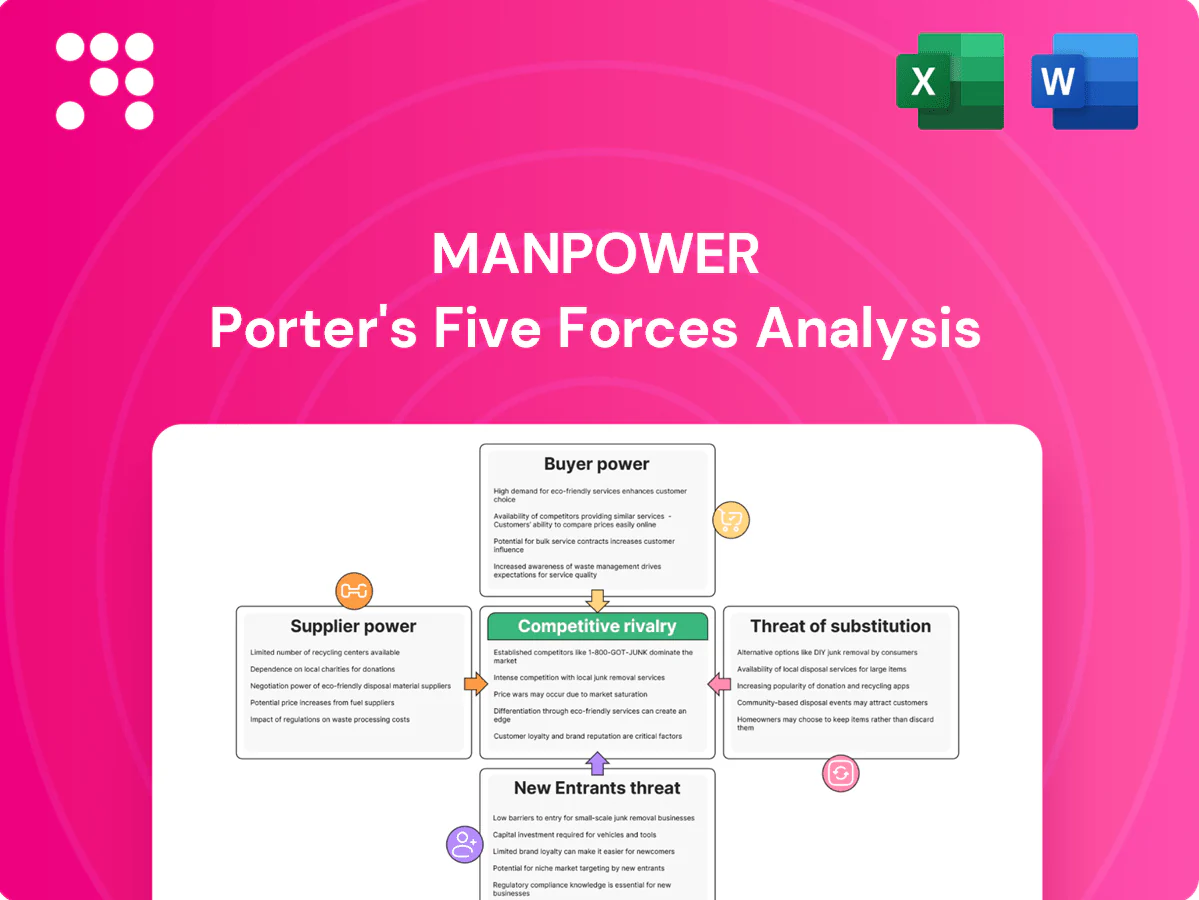

Tailored analysis of Manpower's competitive landscape, detailing each of Porter's five forces and evaluating supplier/buyer power, entry barriers, substitutes, and rival rivalry to identify strategic risks and opportunities.

A concise one-sheet Porter's Five Forces for manpower—visualizes supplier, buyer, entrant, substitute and rivalry pressures to pinpoint hiring and retention risks quickly, customizable for evolving labor market trends and ready to drop into decks.

Customers Bargaining Power

Enterprise procurement clout

Large clients run RFPs and MSP/VMS programs that compress fees; MSPs manage roughly 40% of contingent labor spend (industry reports, 2024), forcing suppliers into tighter margins. Volume commitments tie suppliers to rate cards and SLAs that favor buyers, while buyer consolidation to fewer suppliers amplifies price pressure. ManpowerGroup must therefore differentiate on speed, quality, and compliance to protect margins.

Low switching costs

Low switching costs: clients can onboard alternative agencies or platforms quickly; the global staffing market topped $560 billion in 2023, with many enterprises using multiple suppliers. Non-exclusive short-term contracts and performance KPIs let clients reallocate requisitions within days, keeping pricing and service under constant scrutiny.

Price transparency

In 2024 VMS dashboards and benchmarking data made fee spreads highly visible, with many large buyers (≈60% of enterprises) tracking fill rates, time-to-fill and markup variance in real time. That transparency enables mid-contract renegotiations as clients spot 10–25% spread differentials, making margin expansion difficult absent measurable value-add.

Insourcing options

Large firms increasingly insource TA, with the global HR outsourcing market valued at about 40 billion USD in 2024, enabling internal RPO-like teams and reducing agency spend. Investments in employer branding and referral programs cut agency dependence and create a credible alternative that raises buyer leverage during fee and SLA negotiations. Agencies must therefore justify their use by offering niche expertise, speed, or measurable ROI.

- Insourcing trend: market ~40B USD (2024)

- Employer branding/referrals lower agency reliance

- Raises buyer leverage in fee/SLA talks

- Agencies must prove niche value or faster delivery

Outcome-based demands

Buyers increasingly demand outcome-based fees, pushing providers into performance-linked rebates and SLA penalties that shift attrition risk; by 2024 the global staffing market approached $600B, amplifying buyer leverage on large contracts. Custom compliance and integration raise delivery costs, and negotiating power rises markedly with contract scale and duration.

- Performance fees and rebates

- Penalties shift risk to providers

- Compliance/integration increase costs

- Scale and duration boost buyer leverage

Buyers Rule: MSPs Control 40% of Contingent Spend as Staffing Nears $600B

Buyers hold strong leverage: MSPs manage ~40% of contingent spend and the global staffing market neared $600B in 2024, compressing supplier fees and margins. Low switching costs and multi-supplier strategies mean clients reallocate requisitions within days, with ≈60% of enterprises monitoring real‑time KPIs. Insourcing and a ~$40B HR outsourcing market further reduce agency dependence, forcing agencies to prove measurable value.

| Metric | 2024 Value |

|---|---|

| MSP share of contingent spend | ~40% |

| Global staffing market | ~$600B |

| HR outsourcing market | ~$40B |

| Enterprises tracking KPIs | ~60% |

Preview Before You Purchase

Manpower Porter's Five Forces Analysis

This preview shows the exact Manpower Porter's Five Forces analysis you'll receive immediately after purchase—complete, professionally formatted, and ready to download. It delivers the full assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with clear, actionable insights you can use at once.

A Must-Have Tool for Decision-Makers

Manpower faces moderate buyer power and intense rivalry as global staffing markets compress margins, while supplier dependence on specialized talent and regulatory hurdles heighten barriers. Substitutes from automation and gig platforms pose growing threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Manpower’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Scarce skilled talent

High-demand specialists in IT, healthcare and engineering can dictate rates and terms; BLS projects software developers’ employment to grow 22% 2022–32, intensifying demand. Talent scarcity forces higher pay packages, compressing ManpowerGroup’s margin capture. Candidates with rare certifications increasingly accept direct offers or premium agencies, amplifying supplier power in tight 2024 labor markets.

Candidate multihoming

Candidate multihoming is rising as workers list on multiple platforms and agencies, reducing ManpowerGroup’s exclusivity on placements; ManpowerGroup’s 2024 Talent Shortage Survey noted 54% of employers still face hiring difficulties, intensifying competition for talent. Faster response times and better offers are required to secure commitment, since switching costs for candidates are minimal.

Recruiter and sourcer expertise

Experienced recruiters act as pivotal internal suppliers of placement capacity; 2024 surveys show recruiter scarcity contributes to roughly 45% of hiring delays, pushing compensation and retention costs up as firms chase talent. High mobility means losing star recruiters can reduce fill speed by up to 30% and lower client win rates, concentrating bargaining power within specialist teams and inflating agency margins.

Third‑party tech and data

Reliance on ATS/CRM vendors, major job boards and assessment providers raises costs and exposure; LinkedIn had 930M+ members in 2024, granting platform owners outsized leverage. API access or pricing changes by these platforms can materially worsen unit economics for recruiters and staffing firms. Preferred placement and pay-to-play algorithms give vendors negotiating power, and ongoing consolidation among HR tech firms tightens terms.

- ATS/CRM dependence: higher switching costs

- Platform scale: LinkedIn 930M+ (2024)

- API/pricing shocks: hit unit economics

- Consolidation: fewer vendor alternatives

Training and credential bodies

Training and credential bodies shape candidate readiness; WEF estimates 50% of workers need reskilling by 2025, increasing reliance on credentialing partners. Access to in-demand pathways restricts supply breadth while average US coding bootcamp tuition (~13,500 in 2024) feeds directly into talent costs. Exclusive programs narrow alternative sourcing and can raise hiring premiums.

- Certifiers affect placement readiness

- Reskilling need: 50% by 2025 (WEF)

- Avg bootcamp tuition ~13,500 (2024)

- Exclusive programs limit sourcing

Dev 22%, recruiter delays ≈45% squeeze staffing margins

High-demand specialists (software devs 22% projected growth 2022–32) and scarce recruiters (≈45% of hiring delays) drive up pay and contract leverage, compressing ManpowerGroup margins.

Candidate multihoming and low switching costs (54% of employers report shortages in 2024) reduce exclusivity and force faster, costlier offers.

Dependence on platforms (LinkedIn 930M+ users 2024), ATS vendors and credentialing bodies (WEF: 50% need reskilling by 2025) increases supplier bargaining power and unit-cost exposure.

| Metric | Value |

|---|---|

| Software dev growth | 22% (2022–32, BLS) |

| Employers facing shortages | 54% (2024) |

| Recruiter-related delays | ≈45% (2024) |

| LinkedIn users | 930M+ (2024) |

| Reskilling need | 50% by 2025 (WEF) |

What is included in the product

Tailored analysis of Manpower's competitive landscape, detailing each of Porter's five forces and evaluating supplier/buyer power, entry barriers, substitutes, and rival rivalry to identify strategic risks and opportunities.

A concise one-sheet Porter's Five Forces for manpower—visualizes supplier, buyer, entrant, substitute and rivalry pressures to pinpoint hiring and retention risks quickly, customizable for evolving labor market trends and ready to drop into decks.

Customers Bargaining Power

Enterprise procurement clout

Large clients run RFPs and MSP/VMS programs that compress fees; MSPs manage roughly 40% of contingent labor spend (industry reports, 2024), forcing suppliers into tighter margins. Volume commitments tie suppliers to rate cards and SLAs that favor buyers, while buyer consolidation to fewer suppliers amplifies price pressure. ManpowerGroup must therefore differentiate on speed, quality, and compliance to protect margins.

Low switching costs

Low switching costs: clients can onboard alternative agencies or platforms quickly; the global staffing market topped $560 billion in 2023, with many enterprises using multiple suppliers. Non-exclusive short-term contracts and performance KPIs let clients reallocate requisitions within days, keeping pricing and service under constant scrutiny.

Price transparency

In 2024 VMS dashboards and benchmarking data made fee spreads highly visible, with many large buyers (≈60% of enterprises) tracking fill rates, time-to-fill and markup variance in real time. That transparency enables mid-contract renegotiations as clients spot 10–25% spread differentials, making margin expansion difficult absent measurable value-add.

Insourcing options

Large firms increasingly insource TA, with the global HR outsourcing market valued at about 40 billion USD in 2024, enabling internal RPO-like teams and reducing agency spend. Investments in employer branding and referral programs cut agency dependence and create a credible alternative that raises buyer leverage during fee and SLA negotiations. Agencies must therefore justify their use by offering niche expertise, speed, or measurable ROI.

- Insourcing trend: market ~40B USD (2024)

- Employer branding/referrals lower agency reliance

- Raises buyer leverage in fee/SLA talks

- Agencies must prove niche value or faster delivery

Outcome-based demands

Buyers increasingly demand outcome-based fees, pushing providers into performance-linked rebates and SLA penalties that shift attrition risk; by 2024 the global staffing market approached $600B, amplifying buyer leverage on large contracts. Custom compliance and integration raise delivery costs, and negotiating power rises markedly with contract scale and duration.

- Performance fees and rebates

- Penalties shift risk to providers

- Compliance/integration increase costs

- Scale and duration boost buyer leverage

Buyers Rule: MSPs Control 40% of Contingent Spend as Staffing Nears $600B

Buyers hold strong leverage: MSPs manage ~40% of contingent spend and the global staffing market neared $600B in 2024, compressing supplier fees and margins. Low switching costs and multi-supplier strategies mean clients reallocate requisitions within days, with ≈60% of enterprises monitoring real‑time KPIs. Insourcing and a ~$40B HR outsourcing market further reduce agency dependence, forcing agencies to prove measurable value.

| Metric | 2024 Value |

|---|---|

| MSP share of contingent spend | ~40% |

| Global staffing market | ~$600B |

| HR outsourcing market | ~$40B |

| Enterprises tracking KPIs | ~60% |

Preview Before You Purchase

Manpower Porter's Five Forces Analysis

This preview shows the exact Manpower Porter's Five Forces analysis you'll receive immediately after purchase—complete, professionally formatted, and ready to download. It delivers the full assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with clear, actionable insights you can use at once.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Manpower faces moderate buyer power and intense rivalry as global staffing markets compress margins, while supplier dependence on specialized talent and regulatory hurdles heighten barriers. Substitutes from automation and gig platforms pose growing threats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Manpower’s competitive dynamics and strategic implications in detail.

Suppliers Bargaining Power

Scarce skilled talent

High-demand specialists in IT, healthcare and engineering can dictate rates and terms; BLS projects software developers’ employment to grow 22% 2022–32, intensifying demand. Talent scarcity forces higher pay packages, compressing ManpowerGroup’s margin capture. Candidates with rare certifications increasingly accept direct offers or premium agencies, amplifying supplier power in tight 2024 labor markets.

Candidate multihoming

Candidate multihoming is rising as workers list on multiple platforms and agencies, reducing ManpowerGroup’s exclusivity on placements; ManpowerGroup’s 2024 Talent Shortage Survey noted 54% of employers still face hiring difficulties, intensifying competition for talent. Faster response times and better offers are required to secure commitment, since switching costs for candidates are minimal.

Recruiter and sourcer expertise

Experienced recruiters act as pivotal internal suppliers of placement capacity; 2024 surveys show recruiter scarcity contributes to roughly 45% of hiring delays, pushing compensation and retention costs up as firms chase talent. High mobility means losing star recruiters can reduce fill speed by up to 30% and lower client win rates, concentrating bargaining power within specialist teams and inflating agency margins.

Third‑party tech and data

Reliance on ATS/CRM vendors, major job boards and assessment providers raises costs and exposure; LinkedIn had 930M+ members in 2024, granting platform owners outsized leverage. API access or pricing changes by these platforms can materially worsen unit economics for recruiters and staffing firms. Preferred placement and pay-to-play algorithms give vendors negotiating power, and ongoing consolidation among HR tech firms tightens terms.

- ATS/CRM dependence: higher switching costs

- Platform scale: LinkedIn 930M+ (2024)

- API/pricing shocks: hit unit economics

- Consolidation: fewer vendor alternatives

Training and credential bodies

Training and credential bodies shape candidate readiness; WEF estimates 50% of workers need reskilling by 2025, increasing reliance on credentialing partners. Access to in-demand pathways restricts supply breadth while average US coding bootcamp tuition (~13,500 in 2024) feeds directly into talent costs. Exclusive programs narrow alternative sourcing and can raise hiring premiums.

- Certifiers affect placement readiness

- Reskilling need: 50% by 2025 (WEF)

- Avg bootcamp tuition ~13,500 (2024)

- Exclusive programs limit sourcing

Dev 22%, recruiter delays ≈45% squeeze staffing margins

High-demand specialists (software devs 22% projected growth 2022–32) and scarce recruiters (≈45% of hiring delays) drive up pay and contract leverage, compressing ManpowerGroup margins.

Candidate multihoming and low switching costs (54% of employers report shortages in 2024) reduce exclusivity and force faster, costlier offers.

Dependence on platforms (LinkedIn 930M+ users 2024), ATS vendors and credentialing bodies (WEF: 50% need reskilling by 2025) increases supplier bargaining power and unit-cost exposure.

| Metric | Value |

|---|---|

| Software dev growth | 22% (2022–32, BLS) |

| Employers facing shortages | 54% (2024) |

| Recruiter-related delays | ≈45% (2024) |

| LinkedIn users | 930M+ (2024) |

| Reskilling need | 50% by 2025 (WEF) |

What is included in the product

Tailored analysis of Manpower's competitive landscape, detailing each of Porter's five forces and evaluating supplier/buyer power, entry barriers, substitutes, and rival rivalry to identify strategic risks and opportunities.

A concise one-sheet Porter's Five Forces for manpower—visualizes supplier, buyer, entrant, substitute and rivalry pressures to pinpoint hiring and retention risks quickly, customizable for evolving labor market trends and ready to drop into decks.

Customers Bargaining Power

Enterprise procurement clout

Large clients run RFPs and MSP/VMS programs that compress fees; MSPs manage roughly 40% of contingent labor spend (industry reports, 2024), forcing suppliers into tighter margins. Volume commitments tie suppliers to rate cards and SLAs that favor buyers, while buyer consolidation to fewer suppliers amplifies price pressure. ManpowerGroup must therefore differentiate on speed, quality, and compliance to protect margins.

Low switching costs

Low switching costs: clients can onboard alternative agencies or platforms quickly; the global staffing market topped $560 billion in 2023, with many enterprises using multiple suppliers. Non-exclusive short-term contracts and performance KPIs let clients reallocate requisitions within days, keeping pricing and service under constant scrutiny.

Price transparency

In 2024 VMS dashboards and benchmarking data made fee spreads highly visible, with many large buyers (≈60% of enterprises) tracking fill rates, time-to-fill and markup variance in real time. That transparency enables mid-contract renegotiations as clients spot 10–25% spread differentials, making margin expansion difficult absent measurable value-add.

Insourcing options

Large firms increasingly insource TA, with the global HR outsourcing market valued at about 40 billion USD in 2024, enabling internal RPO-like teams and reducing agency spend. Investments in employer branding and referral programs cut agency dependence and create a credible alternative that raises buyer leverage during fee and SLA negotiations. Agencies must therefore justify their use by offering niche expertise, speed, or measurable ROI.

- Insourcing trend: market ~40B USD (2024)

- Employer branding/referrals lower agency reliance

- Raises buyer leverage in fee/SLA talks

- Agencies must prove niche value or faster delivery

Outcome-based demands

Buyers increasingly demand outcome-based fees, pushing providers into performance-linked rebates and SLA penalties that shift attrition risk; by 2024 the global staffing market approached $600B, amplifying buyer leverage on large contracts. Custom compliance and integration raise delivery costs, and negotiating power rises markedly with contract scale and duration.

- Performance fees and rebates

- Penalties shift risk to providers

- Compliance/integration increase costs

- Scale and duration boost buyer leverage

Buyers Rule: MSPs Control 40% of Contingent Spend as Staffing Nears $600B

Buyers hold strong leverage: MSPs manage ~40% of contingent spend and the global staffing market neared $600B in 2024, compressing supplier fees and margins. Low switching costs and multi-supplier strategies mean clients reallocate requisitions within days, with ≈60% of enterprises monitoring real‑time KPIs. Insourcing and a ~$40B HR outsourcing market further reduce agency dependence, forcing agencies to prove measurable value.

| Metric | 2024 Value |

|---|---|

| MSP share of contingent spend | ~40% |

| Global staffing market | ~$600B |

| HR outsourcing market | ~$40B |

| Enterprises tracking KPIs | ~60% |

Preview Before You Purchase

Manpower Porter's Five Forces Analysis

This preview shows the exact Manpower Porter's Five Forces analysis you'll receive immediately after purchase—complete, professionally formatted, and ready to download. It delivers the full assessment of competitive rivalry, supplier and buyer power, threat of substitutes, and barriers to entry, with clear, actionable insights you can use at once.