Maped SAS Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

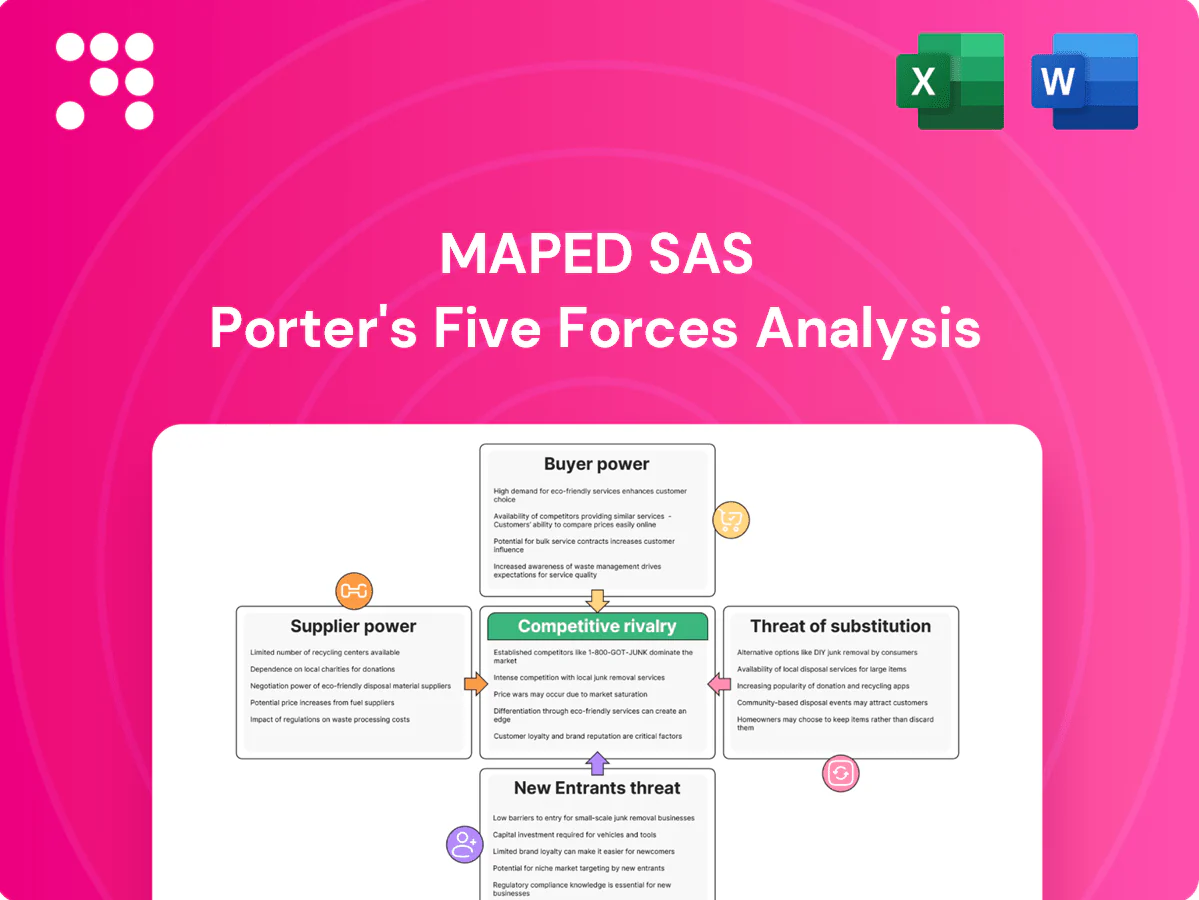

Maped SAS faces mixed pressures from global suppliers, private-label competitors, and shifting school & office demand; this snapshot highlights key tensions but omits depth. The full Porter's Five Forces Analysis quantifies force strengths, maps competitor moves, and identifies strategic gaps. Unlock the complete report for visuals, force-by-force ratings, and actionable recommendations tailored to Maped SAS.

Suppliers Bargaining Power

Commodity inputs: plastics, metals, pigments

Maped relies on polymers, steel, rubber and pigments that are widely available, keeping individual supplier power moderate; 2024 Brent crude averaged about $86/bbl, driving occasional resin price spikes that can squeeze margins. Long-term contracts and commodity hedges partially mitigate swings, while specification flexibility and dual-sourcing reduce dependence on any single supplier.

Specialized tooling and injection molding

Precision molds and tooling vendors exert high leverage due to customization and typical European injection-mold lead times of 12–20 weeks, raising switching costs when designs embed a toolmaker’s proprietary know-how. Preventive maintenance and in-house tooling can cut downtime by ~30–40% and lower dependency. Framework agreements and clear IP ownership over tool designs limit supplier hold-up and price volatility by an estimated 10–20%.

OEM/contract manufacturing footprint

If Maped outsources components or finished goods, concentrated OEM partners can exert negotiating power, especially for specialty tooling or long-lead items. In 2024 China remained the largest contract-manufacturing hub and Asia plus Eastern Europe continue to offer abundant capacity, supporting competitive bidding. Strict quality and compliance (CE/REACH) narrow qualified suppliers, while vendor scorecards and phased onboarding maintain sustained performance pressure.

Logistics, energy, and packaging

Logistics carriers and energy providers indirectly pushed input costs for Maped in 2024, with freight-rate and port-congestion episodes trimming margins on low-price SKUs and raising landed costs. Packaging (paperboard, recycled plastics) remains competitive but is increasingly shaped by 2024 sustainability mandates and higher recycled-content premiums. Multi-modal logistics and regionalized sourcing limited supplier leverage.

- Freight volatility hit margins

- Energy costs pressured COGS

- Sustainable packaging raises premiums

- Regional sourcing reduces supplier power

Sustainability and compliance constraints

REACH now covers over 22,000 registered substances and EN 71 is mandatory for EU toys, while eco-certifications further shrink the supplier pool, increasing supplier bargaining power; Maped’s recycled-content and non-toxic-ink targets narrow eligible suppliers further. Long-term contracts with compliant suppliers stabilize volumes and pricing, and transparency programs shift talks from price-only to total value and risk reduction.

- REACH: 22,000+ substances

- EN 71: mandatory EU toy safety

- Eco-cert limits: fewer qualified suppliers

- Mitigation: long-term contracts, transparency

Plastic supply shocks and long tool lead times squeeze margins; compliance limits suppliers

Maped depends on widely available polymers, steel and pigments; 2024 Brent averaged $86/bbl, driving resin-price spikes that squeeze margins. Precision tooling (EU injection-mold lead times 12–20 weeks) raises switching costs; in‑house tooling and preventive maintenance cut downtime ~30–40%. REACH covers 22,000+ substances and CE/EN71 narrow qualified suppliers, while regional sourcing and long-term contracts limit supplier leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Brent | $86/bbl | resin cost spikes |

| Tooling lead time | 12–20 weeks | high switching cost |

| Maintenance benefit | 30–40% downtime↓ | reduces dependency |

| REACH scope | 22,000+ substances | fewer compliant suppliers |

What is included in the product

Tailored Porter's Five Forces analysis for Maped SAS that uncovers key drivers of competition, buyer and supplier power, and substitution risks impacting pricing and profitability. Provides strategic insights on entry barriers, disruptive threats, and defensive levers to protect market share and guide investor or management decisions.

Relieve competitive-analysis bottlenecks with a concise one-sheet Porter's Five Forces for Maped SAS that visualizes pressure via an editable spider chart, allows scenario comparisons (pre/post changes), and is ready to paste into pitch decks—no macros required.

Customers Bargaining Power

Concentrated retail channels

Large chains and hypermarkets concentrate volume in France (Kantar 2024: Leclerc ~21.8%, Carrefour ~18.7%, Intermarché ~14.6%, Lidl ~8.9%), giving them strong bargaining power. They routinely demand slotting fees (varying by format), promotional funding often 5–20% of COGS and OTIF targets of ~95%+. Failure to meet KPIs can prompt seasonal delisting; joint business planning secures shelf space while protecting margin.

Private label and price sensitivity

Retailers’ private labels intensify price comparisons and push down branded pricing; private-label penetration in EU retail rose to 38% in 2024. Commodity stationery like rulers and erasers have very low switching costs, forcing Maped to justify premiums through ergonomics, durability and distinctive design. Strategic pack architecture and value bundles reinforce price points and increase perceived value.

Online marketplaces and transparency

E-commerce transparency (global online sales ~6.3 trillion USD in 2024) amplifies buyer leverage as price comparisons are instant; customer reviews influence purchase decisions (over 90% consult reviews), shifting power toward demands for quality at low cost. Maped can use D2C channels to A/B test assortments and capture first-party data, while MAP and authorized-seller programs limit grey-market erosion.

Institutional and education tenders

Institutional and education tenders push buyers toward compliance and unit-cost focus; public procurement represents about 14% of EU GDP (Eurostat), making contracts sizable but often cyclical and intensely competitive. Custom safety specs and certifications raise entry barriers yet squeeze margins, while service levels and ESG credentials frequently decide award outcomes.

- High compliance / low unit price

- Sizable but cyclical contracts

- Custom specs increase entry hurdles

- ESG & service can be tie-breakers

Brand preference and switching costs

End-user affinity for ergonomics and safety features reduces buyer power in Maped’s premium niches, as artists and professionals treat performance as a non-negotiable, raising perceived switching costs and lowering price sensitivity. Students’ standardized back-to-school lists concentrate SKU demand seasonally, while loyalty programs and refill options boost lifetime value and cut churn; Maped sells in about 125 countries (2024 presence).

- Premium ergonomics = lower buyer power

- Professionals raise switching costs

- Back-to-school standardizes SKU demand

- Loyalty/refills increase LTV, reduce churn

Retail concentration squeezes margins: promos 5–20%, private-label 38%

Large French retailers (Leclerc 21.8%, Carrefour 18.7%, Intermarché 14.6%, Lidl 8.9% in 2024) concentrate volume and demand slotting/promos (5–20% COGS), squeezing margins. EU private-label share 38% (2024) and e-commerce transparency raise price pressure; premium ergonomics and institutional tenders mitigate but do not remove buyer power.

| Metric | 2024 |

|---|---|

| Leclerc share | 21.8% |

| Carrefour share | 18.7% |

| Private-label EU | 38% |

| Promo funding | 5–20% COGS |

Preview Before You Purchase

Maped SAS Porter's Five Forces Analysis

This preview shows the exact Maped SAS Porter's Five Forces analysis you'll receive after purchase—fully written, formatted and ready to use. No mockups or placeholders; the file available for download is identical to this view. Instant access upon payment.

Go Beyond the Preview—Access the Full Strategic Report

Maped SAS faces mixed pressures from global suppliers, private-label competitors, and shifting school & office demand; this snapshot highlights key tensions but omits depth. The full Porter's Five Forces Analysis quantifies force strengths, maps competitor moves, and identifies strategic gaps. Unlock the complete report for visuals, force-by-force ratings, and actionable recommendations tailored to Maped SAS.

Suppliers Bargaining Power

Commodity inputs: plastics, metals, pigments

Maped relies on polymers, steel, rubber and pigments that are widely available, keeping individual supplier power moderate; 2024 Brent crude averaged about $86/bbl, driving occasional resin price spikes that can squeeze margins. Long-term contracts and commodity hedges partially mitigate swings, while specification flexibility and dual-sourcing reduce dependence on any single supplier.

Specialized tooling and injection molding

Precision molds and tooling vendors exert high leverage due to customization and typical European injection-mold lead times of 12–20 weeks, raising switching costs when designs embed a toolmaker’s proprietary know-how. Preventive maintenance and in-house tooling can cut downtime by ~30–40% and lower dependency. Framework agreements and clear IP ownership over tool designs limit supplier hold-up and price volatility by an estimated 10–20%.

OEM/contract manufacturing footprint

If Maped outsources components or finished goods, concentrated OEM partners can exert negotiating power, especially for specialty tooling or long-lead items. In 2024 China remained the largest contract-manufacturing hub and Asia plus Eastern Europe continue to offer abundant capacity, supporting competitive bidding. Strict quality and compliance (CE/REACH) narrow qualified suppliers, while vendor scorecards and phased onboarding maintain sustained performance pressure.

Logistics, energy, and packaging

Logistics carriers and energy providers indirectly pushed input costs for Maped in 2024, with freight-rate and port-congestion episodes trimming margins on low-price SKUs and raising landed costs. Packaging (paperboard, recycled plastics) remains competitive but is increasingly shaped by 2024 sustainability mandates and higher recycled-content premiums. Multi-modal logistics and regionalized sourcing limited supplier leverage.

- Freight volatility hit margins

- Energy costs pressured COGS

- Sustainable packaging raises premiums

- Regional sourcing reduces supplier power

Sustainability and compliance constraints

REACH now covers over 22,000 registered substances and EN 71 is mandatory for EU toys, while eco-certifications further shrink the supplier pool, increasing supplier bargaining power; Maped’s recycled-content and non-toxic-ink targets narrow eligible suppliers further. Long-term contracts with compliant suppliers stabilize volumes and pricing, and transparency programs shift talks from price-only to total value and risk reduction.

- REACH: 22,000+ substances

- EN 71: mandatory EU toy safety

- Eco-cert limits: fewer qualified suppliers

- Mitigation: long-term contracts, transparency

Plastic supply shocks and long tool lead times squeeze margins; compliance limits suppliers

Maped depends on widely available polymers, steel and pigments; 2024 Brent averaged $86/bbl, driving resin-price spikes that squeeze margins. Precision tooling (EU injection-mold lead times 12–20 weeks) raises switching costs; in‑house tooling and preventive maintenance cut downtime ~30–40%. REACH covers 22,000+ substances and CE/EN71 narrow qualified suppliers, while regional sourcing and long-term contracts limit supplier leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Brent | $86/bbl | resin cost spikes |

| Tooling lead time | 12–20 weeks | high switching cost |

| Maintenance benefit | 30–40% downtime↓ | reduces dependency |

| REACH scope | 22,000+ substances | fewer compliant suppliers |

What is included in the product

Tailored Porter's Five Forces analysis for Maped SAS that uncovers key drivers of competition, buyer and supplier power, and substitution risks impacting pricing and profitability. Provides strategic insights on entry barriers, disruptive threats, and defensive levers to protect market share and guide investor or management decisions.

Relieve competitive-analysis bottlenecks with a concise one-sheet Porter's Five Forces for Maped SAS that visualizes pressure via an editable spider chart, allows scenario comparisons (pre/post changes), and is ready to paste into pitch decks—no macros required.

Customers Bargaining Power

Concentrated retail channels

Large chains and hypermarkets concentrate volume in France (Kantar 2024: Leclerc ~21.8%, Carrefour ~18.7%, Intermarché ~14.6%, Lidl ~8.9%), giving them strong bargaining power. They routinely demand slotting fees (varying by format), promotional funding often 5–20% of COGS and OTIF targets of ~95%+. Failure to meet KPIs can prompt seasonal delisting; joint business planning secures shelf space while protecting margin.

Private label and price sensitivity

Retailers’ private labels intensify price comparisons and push down branded pricing; private-label penetration in EU retail rose to 38% in 2024. Commodity stationery like rulers and erasers have very low switching costs, forcing Maped to justify premiums through ergonomics, durability and distinctive design. Strategic pack architecture and value bundles reinforce price points and increase perceived value.

Online marketplaces and transparency

E-commerce transparency (global online sales ~6.3 trillion USD in 2024) amplifies buyer leverage as price comparisons are instant; customer reviews influence purchase decisions (over 90% consult reviews), shifting power toward demands for quality at low cost. Maped can use D2C channels to A/B test assortments and capture first-party data, while MAP and authorized-seller programs limit grey-market erosion.

Institutional and education tenders

Institutional and education tenders push buyers toward compliance and unit-cost focus; public procurement represents about 14% of EU GDP (Eurostat), making contracts sizable but often cyclical and intensely competitive. Custom safety specs and certifications raise entry barriers yet squeeze margins, while service levels and ESG credentials frequently decide award outcomes.

- High compliance / low unit price

- Sizable but cyclical contracts

- Custom specs increase entry hurdles

- ESG & service can be tie-breakers

Brand preference and switching costs

End-user affinity for ergonomics and safety features reduces buyer power in Maped’s premium niches, as artists and professionals treat performance as a non-negotiable, raising perceived switching costs and lowering price sensitivity. Students’ standardized back-to-school lists concentrate SKU demand seasonally, while loyalty programs and refill options boost lifetime value and cut churn; Maped sells in about 125 countries (2024 presence).

- Premium ergonomics = lower buyer power

- Professionals raise switching costs

- Back-to-school standardizes SKU demand

- Loyalty/refills increase LTV, reduce churn

Retail concentration squeezes margins: promos 5–20%, private-label 38%

Large French retailers (Leclerc 21.8%, Carrefour 18.7%, Intermarché 14.6%, Lidl 8.9% in 2024) concentrate volume and demand slotting/promos (5–20% COGS), squeezing margins. EU private-label share 38% (2024) and e-commerce transparency raise price pressure; premium ergonomics and institutional tenders mitigate but do not remove buyer power.

| Metric | 2024 |

|---|---|

| Leclerc share | 21.8% |

| Carrefour share | 18.7% |

| Private-label EU | 38% |

| Promo funding | 5–20% COGS |

Preview Before You Purchase

Maped SAS Porter's Five Forces Analysis

This preview shows the exact Maped SAS Porter's Five Forces analysis you'll receive after purchase—fully written, formatted and ready to use. No mockups or placeholders; the file available for download is identical to this view. Instant access upon payment.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Maped SAS faces mixed pressures from global suppliers, private-label competitors, and shifting school & office demand; this snapshot highlights key tensions but omits depth. The full Porter's Five Forces Analysis quantifies force strengths, maps competitor moves, and identifies strategic gaps. Unlock the complete report for visuals, force-by-force ratings, and actionable recommendations tailored to Maped SAS.

Suppliers Bargaining Power

Commodity inputs: plastics, metals, pigments

Maped relies on polymers, steel, rubber and pigments that are widely available, keeping individual supplier power moderate; 2024 Brent crude averaged about $86/bbl, driving occasional resin price spikes that can squeeze margins. Long-term contracts and commodity hedges partially mitigate swings, while specification flexibility and dual-sourcing reduce dependence on any single supplier.

Specialized tooling and injection molding

Precision molds and tooling vendors exert high leverage due to customization and typical European injection-mold lead times of 12–20 weeks, raising switching costs when designs embed a toolmaker’s proprietary know-how. Preventive maintenance and in-house tooling can cut downtime by ~30–40% and lower dependency. Framework agreements and clear IP ownership over tool designs limit supplier hold-up and price volatility by an estimated 10–20%.

OEM/contract manufacturing footprint

If Maped outsources components or finished goods, concentrated OEM partners can exert negotiating power, especially for specialty tooling or long-lead items. In 2024 China remained the largest contract-manufacturing hub and Asia plus Eastern Europe continue to offer abundant capacity, supporting competitive bidding. Strict quality and compliance (CE/REACH) narrow qualified suppliers, while vendor scorecards and phased onboarding maintain sustained performance pressure.

Logistics, energy, and packaging

Logistics carriers and energy providers indirectly pushed input costs for Maped in 2024, with freight-rate and port-congestion episodes trimming margins on low-price SKUs and raising landed costs. Packaging (paperboard, recycled plastics) remains competitive but is increasingly shaped by 2024 sustainability mandates and higher recycled-content premiums. Multi-modal logistics and regionalized sourcing limited supplier leverage.

- Freight volatility hit margins

- Energy costs pressured COGS

- Sustainable packaging raises premiums

- Regional sourcing reduces supplier power

Sustainability and compliance constraints

REACH now covers over 22,000 registered substances and EN 71 is mandatory for EU toys, while eco-certifications further shrink the supplier pool, increasing supplier bargaining power; Maped’s recycled-content and non-toxic-ink targets narrow eligible suppliers further. Long-term contracts with compliant suppliers stabilize volumes and pricing, and transparency programs shift talks from price-only to total value and risk reduction.

- REACH: 22,000+ substances

- EN 71: mandatory EU toy safety

- Eco-cert limits: fewer qualified suppliers

- Mitigation: long-term contracts, transparency

Plastic supply shocks and long tool lead times squeeze margins; compliance limits suppliers

Maped depends on widely available polymers, steel and pigments; 2024 Brent averaged $86/bbl, driving resin-price spikes that squeeze margins. Precision tooling (EU injection-mold lead times 12–20 weeks) raises switching costs; in‑house tooling and preventive maintenance cut downtime ~30–40%. REACH covers 22,000+ substances and CE/EN71 narrow qualified suppliers, while regional sourcing and long-term contracts limit supplier leverage.

| Metric | 2024 | Impact |

|---|---|---|

| Brent | $86/bbl | resin cost spikes |

| Tooling lead time | 12–20 weeks | high switching cost |

| Maintenance benefit | 30–40% downtime↓ | reduces dependency |

| REACH scope | 22,000+ substances | fewer compliant suppliers |

What is included in the product

Tailored Porter's Five Forces analysis for Maped SAS that uncovers key drivers of competition, buyer and supplier power, and substitution risks impacting pricing and profitability. Provides strategic insights on entry barriers, disruptive threats, and defensive levers to protect market share and guide investor or management decisions.

Relieve competitive-analysis bottlenecks with a concise one-sheet Porter's Five Forces for Maped SAS that visualizes pressure via an editable spider chart, allows scenario comparisons (pre/post changes), and is ready to paste into pitch decks—no macros required.

Customers Bargaining Power

Concentrated retail channels

Large chains and hypermarkets concentrate volume in France (Kantar 2024: Leclerc ~21.8%, Carrefour ~18.7%, Intermarché ~14.6%, Lidl ~8.9%), giving them strong bargaining power. They routinely demand slotting fees (varying by format), promotional funding often 5–20% of COGS and OTIF targets of ~95%+. Failure to meet KPIs can prompt seasonal delisting; joint business planning secures shelf space while protecting margin.

Private label and price sensitivity

Retailers’ private labels intensify price comparisons and push down branded pricing; private-label penetration in EU retail rose to 38% in 2024. Commodity stationery like rulers and erasers have very low switching costs, forcing Maped to justify premiums through ergonomics, durability and distinctive design. Strategic pack architecture and value bundles reinforce price points and increase perceived value.

Online marketplaces and transparency

E-commerce transparency (global online sales ~6.3 trillion USD in 2024) amplifies buyer leverage as price comparisons are instant; customer reviews influence purchase decisions (over 90% consult reviews), shifting power toward demands for quality at low cost. Maped can use D2C channels to A/B test assortments and capture first-party data, while MAP and authorized-seller programs limit grey-market erosion.

Institutional and education tenders

Institutional and education tenders push buyers toward compliance and unit-cost focus; public procurement represents about 14% of EU GDP (Eurostat), making contracts sizable but often cyclical and intensely competitive. Custom safety specs and certifications raise entry barriers yet squeeze margins, while service levels and ESG credentials frequently decide award outcomes.

- High compliance / low unit price

- Sizable but cyclical contracts

- Custom specs increase entry hurdles

- ESG & service can be tie-breakers

Brand preference and switching costs

End-user affinity for ergonomics and safety features reduces buyer power in Maped’s premium niches, as artists and professionals treat performance as a non-negotiable, raising perceived switching costs and lowering price sensitivity. Students’ standardized back-to-school lists concentrate SKU demand seasonally, while loyalty programs and refill options boost lifetime value and cut churn; Maped sells in about 125 countries (2024 presence).

- Premium ergonomics = lower buyer power

- Professionals raise switching costs

- Back-to-school standardizes SKU demand

- Loyalty/refills increase LTV, reduce churn

Retail concentration squeezes margins: promos 5–20%, private-label 38%

Large French retailers (Leclerc 21.8%, Carrefour 18.7%, Intermarché 14.6%, Lidl 8.9% in 2024) concentrate volume and demand slotting/promos (5–20% COGS), squeezing margins. EU private-label share 38% (2024) and e-commerce transparency raise price pressure; premium ergonomics and institutional tenders mitigate but do not remove buyer power.

| Metric | 2024 |

|---|---|

| Leclerc share | 21.8% |

| Carrefour share | 18.7% |

| Private-label EU | 38% |

| Promo funding | 5–20% COGS |

Preview Before You Purchase

Maped SAS Porter's Five Forces Analysis

This preview shows the exact Maped SAS Porter's Five Forces analysis you'll receive after purchase—fully written, formatted and ready to use. No mockups or placeholders; the file available for download is identical to this view. Instant access upon payment.