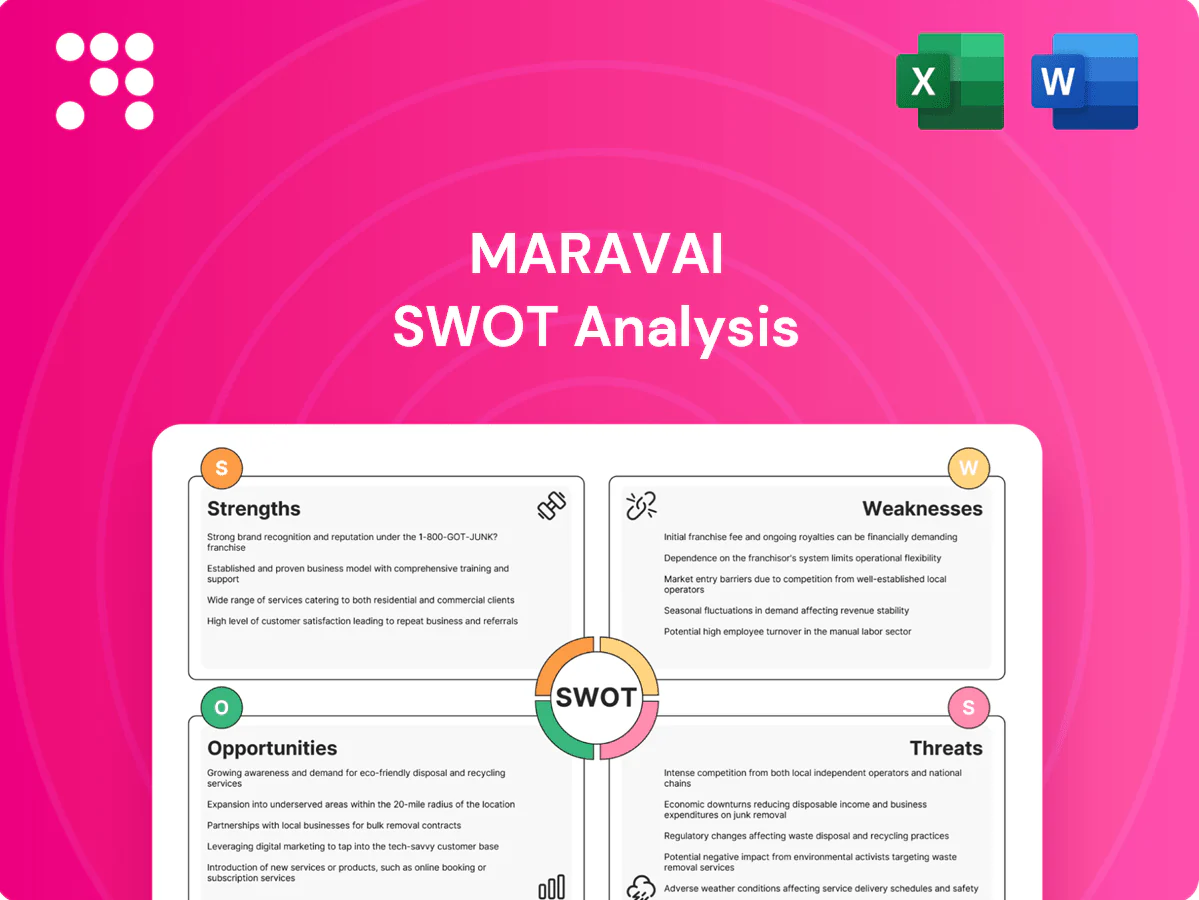

Maravai SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Explore Maravai's strategic position with our concise SWOT snapshot—highlighting proprietary reagent strengths, biotech market tailwinds, and risks from competition and regulatory shifts. Want deeper, actionable insight? Purchase the full SWOT for a research-backed, editable Word + Excel package to inform investment or strategy decisions.

Strengths

Mission-critical nucleic acid reagents

Maravai supplies mission-critical nucleic acid reagents used in therapies, vaccines and diagnostics where quality and reliability are non-negotiable, making it a preferred partner across R&D and GMP stages. That mission-critical status creates pricing power and customer stickiness, as validated workflows limit substitution. Reduced substitution risk supports long-term recurring revenue and higher margin sustainability.

Two-segment portfolio synergy

Maravai LifeSciences (ticker MRVI) aligns Nucleic Acid Production and Biologics Safety Testing to serve adjacent biopharma lifecycle needs. Cross-segment insights boost customer intimacy and enable bundled solutions and cross-selling, supporting diversified revenues across the same end markets. In 2024 Maravai reported about $402 million in revenue, underscoring portfolio-driven resilience. This enhances recurring revenue potential and go-to-market efficiency.

High switching costs and qualification barriers

Customers validate suppliers for regulated programs, creating onboarding and requalification hurdles that commonly take 6–12 months and involve extensive documentation and audits. Once reagents and services are specified they are difficult to replace mid-program, driving multi-year revenue durability. This dynamic supports long-term partnerships with leading pharma and biotech, where programs often span 3–5 years.

Exposure to fast-growing modalities

Demand for Maravai’s reagents and safety-testing services is tightly tied to mRNA, oligonucleotide, and advanced biologics growth; the nucleic-acid reagents market is forecast to grow at about 12% CAGR from 2024–2030, and over 10 oligonucleotide therapies had regulatory approval by 2024. Rising modality complexity increases demand for specialized providers and supports Maravai’s premium positioning versus generic suppliers.

- Market tag: ~12% CAGR (2024–2030)

- Regulatory tag: >10 oligo approvals by 2024

- Strategic tag: premium vs generic

Regulatory and quality credibility

Maravai (NASDAQ: MRVI) sustains regulatory and quality credibility through robust QMS, detailed documentation, and consistent compliance that support regulated applications and ease customer audits and tech transfers.

This demonstrated track record accelerates adoption in late-stage programs and underpins expansion into additional regulated offerings, reinforcing customer confidence and reducing time-to-market.

- Regulatory-ready QMS

- Audit-friendly documentation

- Speeds late-stage adoption

- Enables regulated portfolio expansion

Nucleic-acid reagents: regulatory-ready, sticky contracts, $402M 2024 revenue

Maravai supplies mission-critical nucleic-acid reagents with strong pricing power and customer stickiness; 2024 revenue ~$402M. Regulatory-ready QMS and audit-friendly documentation accelerate late-stage adoption and cross-segment sales. Long onboarding/requalification (6–12 months) creates multi-year contract durability while a ~12% nucleic-acid market CAGR (2024–2030) supports sustained demand.

| Metric | Value |

|---|---|

| 2024 Revenue | $402M |

| Market CAGR (2024–2030) | ~12% |

| Oligo approvals by 2024 | >10 |

| Onboarding time | 6–12 months |

| Ticker | MRVI |

What is included in the product

Provides a focused SWOT analysis of Maravai, highlighting internal strengths and weaknesses and external opportunities and threats shaping its biotech reagents and services growth outlook.

Provides a clear, Maravai-specific SWOT matrix for rapid strategic alignment and decision-making, enabling stakeholders to quickly identify risks, opportunities and prioritize action.

Weaknesses

End-market concentration in biotech

End-market concentration in biotech makes Maravai revenue highly sensitive to biotech funding cycles and program progress, so slowdowns in venture funding or IPO activity can quickly dampen orders. This cyclicality complicates forecasting and capacity planning and increases the likelihood of underutilized production. To retain volumes during downturns the company may need to offer pricing or terms concessions, squeezing margins and cash flow.

Product and modality concentration

Maravai’s reliance on nucleic acid reagents and synthetic DNA/RNA ties its performance to modality-specific demand; COVID-19 vaccine volumes peaked in 2021–2022, exposing the company to post-peak volatility. Limited diversification beyond core chemistries heightens exposure to competitive and pricing pressure, which can magnify revenue swings.

Customer concentration risk

Maravai’s revenue is driven by a small number of large programs, so loss or delay of one marquee account can materially affect quarterly and annual results. Public disclosures note concentration risk and that a few customers hold negotiating leverage, which can compress margins or extend payment terms. This customer mix amplifies cash‑flow and margin volatility for the company.

Regulatory and compliance burden

Maintaining GMP and audit readiness requires significant recurring investment in facilities, personnel and validation, increasing OPEX and diverting capital from R&D; quality deviations can trigger production holds, recalls and reputational harm that disrupt revenue streams.

Expanding compliance into new geographies adds regulatory complexity and local approvals, often lengthening time-to-market for new offerings and raising launch costs.

- GMP/audit cost burden

- Holds/recalls risk

- Geographic compliance complexity

- Longer time-to-market

Scale disadvantage versus giants

Global incumbents with broader catalogs can bundle and discount aggressively; Thermo Fisher and Danaher, which each reported roughly $40–50B in 2024 revenue, can outspend Maravai on automation, distribution, and R&D, compressing win rates in price-sensitive segments and raising barriers to adjacent categories.

- Bundling pressure

- R&D & capex scale

- Price-sensitive losses

- Adjacency barriers

End-market concentration and reagent reliance drive revenue volatility and OPEX pressure

End-market concentration in biotech makes Maravai revenue highly sensitive to funding and program timing, driving forecast and capacity risk. Reliance on nucleic acid reagents and post‑COVID modality demand raises volatility and limited product diversification. A few large customers create material concentration and margin pressure while GMP/audit and geographic compliance raise OPEX and slow launches.

| Metric | Value/Note |

|---|---|

| Competitor revenue (2024) | Thermo Fisher, Danaher ≈$40–50B |

| Customer concentration | Material; few large programs |

| Operational burden | High GMP/audit OPEX |

What You See Is What You Get

Maravai SWOT Analysis

This is the actual Maravai SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete, editable structure ready for download after payment. Buy now to unlock the entire in-depth version and begin using the full report immediately.

Elevate Your Analysis with the Complete SWOT Report

Explore Maravai's strategic position with our concise SWOT snapshot—highlighting proprietary reagent strengths, biotech market tailwinds, and risks from competition and regulatory shifts. Want deeper, actionable insight? Purchase the full SWOT for a research-backed, editable Word + Excel package to inform investment or strategy decisions.

Strengths

Mission-critical nucleic acid reagents

Maravai supplies mission-critical nucleic acid reagents used in therapies, vaccines and diagnostics where quality and reliability are non-negotiable, making it a preferred partner across R&D and GMP stages. That mission-critical status creates pricing power and customer stickiness, as validated workflows limit substitution. Reduced substitution risk supports long-term recurring revenue and higher margin sustainability.

Two-segment portfolio synergy

Maravai LifeSciences (ticker MRVI) aligns Nucleic Acid Production and Biologics Safety Testing to serve adjacent biopharma lifecycle needs. Cross-segment insights boost customer intimacy and enable bundled solutions and cross-selling, supporting diversified revenues across the same end markets. In 2024 Maravai reported about $402 million in revenue, underscoring portfolio-driven resilience. This enhances recurring revenue potential and go-to-market efficiency.

High switching costs and qualification barriers

Customers validate suppliers for regulated programs, creating onboarding and requalification hurdles that commonly take 6–12 months and involve extensive documentation and audits. Once reagents and services are specified they are difficult to replace mid-program, driving multi-year revenue durability. This dynamic supports long-term partnerships with leading pharma and biotech, where programs often span 3–5 years.

Exposure to fast-growing modalities

Demand for Maravai’s reagents and safety-testing services is tightly tied to mRNA, oligonucleotide, and advanced biologics growth; the nucleic-acid reagents market is forecast to grow at about 12% CAGR from 2024–2030, and over 10 oligonucleotide therapies had regulatory approval by 2024. Rising modality complexity increases demand for specialized providers and supports Maravai’s premium positioning versus generic suppliers.

- Market tag: ~12% CAGR (2024–2030)

- Regulatory tag: >10 oligo approvals by 2024

- Strategic tag: premium vs generic

Regulatory and quality credibility

Maravai (NASDAQ: MRVI) sustains regulatory and quality credibility through robust QMS, detailed documentation, and consistent compliance that support regulated applications and ease customer audits and tech transfers.

This demonstrated track record accelerates adoption in late-stage programs and underpins expansion into additional regulated offerings, reinforcing customer confidence and reducing time-to-market.

- Regulatory-ready QMS

- Audit-friendly documentation

- Speeds late-stage adoption

- Enables regulated portfolio expansion

Nucleic-acid reagents: regulatory-ready, sticky contracts, $402M 2024 revenue

Maravai supplies mission-critical nucleic-acid reagents with strong pricing power and customer stickiness; 2024 revenue ~$402M. Regulatory-ready QMS and audit-friendly documentation accelerate late-stage adoption and cross-segment sales. Long onboarding/requalification (6–12 months) creates multi-year contract durability while a ~12% nucleic-acid market CAGR (2024–2030) supports sustained demand.

| Metric | Value |

|---|---|

| 2024 Revenue | $402M |

| Market CAGR (2024–2030) | ~12% |

| Oligo approvals by 2024 | >10 |

| Onboarding time | 6–12 months |

| Ticker | MRVI |

What is included in the product

Provides a focused SWOT analysis of Maravai, highlighting internal strengths and weaknesses and external opportunities and threats shaping its biotech reagents and services growth outlook.

Provides a clear, Maravai-specific SWOT matrix for rapid strategic alignment and decision-making, enabling stakeholders to quickly identify risks, opportunities and prioritize action.

Weaknesses

End-market concentration in biotech

End-market concentration in biotech makes Maravai revenue highly sensitive to biotech funding cycles and program progress, so slowdowns in venture funding or IPO activity can quickly dampen orders. This cyclicality complicates forecasting and capacity planning and increases the likelihood of underutilized production. To retain volumes during downturns the company may need to offer pricing or terms concessions, squeezing margins and cash flow.

Product and modality concentration

Maravai’s reliance on nucleic acid reagents and synthetic DNA/RNA ties its performance to modality-specific demand; COVID-19 vaccine volumes peaked in 2021–2022, exposing the company to post-peak volatility. Limited diversification beyond core chemistries heightens exposure to competitive and pricing pressure, which can magnify revenue swings.

Customer concentration risk

Maravai’s revenue is driven by a small number of large programs, so loss or delay of one marquee account can materially affect quarterly and annual results. Public disclosures note concentration risk and that a few customers hold negotiating leverage, which can compress margins or extend payment terms. This customer mix amplifies cash‑flow and margin volatility for the company.

Regulatory and compliance burden

Maintaining GMP and audit readiness requires significant recurring investment in facilities, personnel and validation, increasing OPEX and diverting capital from R&D; quality deviations can trigger production holds, recalls and reputational harm that disrupt revenue streams.

Expanding compliance into new geographies adds regulatory complexity and local approvals, often lengthening time-to-market for new offerings and raising launch costs.

- GMP/audit cost burden

- Holds/recalls risk

- Geographic compliance complexity

- Longer time-to-market

Scale disadvantage versus giants

Global incumbents with broader catalogs can bundle and discount aggressively; Thermo Fisher and Danaher, which each reported roughly $40–50B in 2024 revenue, can outspend Maravai on automation, distribution, and R&D, compressing win rates in price-sensitive segments and raising barriers to adjacent categories.

- Bundling pressure

- R&D & capex scale

- Price-sensitive losses

- Adjacency barriers

End-market concentration and reagent reliance drive revenue volatility and OPEX pressure

End-market concentration in biotech makes Maravai revenue highly sensitive to funding and program timing, driving forecast and capacity risk. Reliance on nucleic acid reagents and post‑COVID modality demand raises volatility and limited product diversification. A few large customers create material concentration and margin pressure while GMP/audit and geographic compliance raise OPEX and slow launches.

| Metric | Value/Note |

|---|---|

| Competitor revenue (2024) | Thermo Fisher, Danaher ≈$40–50B |

| Customer concentration | Material; few large programs |

| Operational burden | High GMP/audit OPEX |

What You See Is What You Get

Maravai SWOT Analysis

This is the actual Maravai SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete, editable structure ready for download after payment. Buy now to unlock the entire in-depth version and begin using the full report immediately.

Description

Elevate Your Analysis with the Complete SWOT Report

Explore Maravai's strategic position with our concise SWOT snapshot—highlighting proprietary reagent strengths, biotech market tailwinds, and risks from competition and regulatory shifts. Want deeper, actionable insight? Purchase the full SWOT for a research-backed, editable Word + Excel package to inform investment or strategy decisions.

Strengths

Mission-critical nucleic acid reagents

Maravai supplies mission-critical nucleic acid reagents used in therapies, vaccines and diagnostics where quality and reliability are non-negotiable, making it a preferred partner across R&D and GMP stages. That mission-critical status creates pricing power and customer stickiness, as validated workflows limit substitution. Reduced substitution risk supports long-term recurring revenue and higher margin sustainability.

Two-segment portfolio synergy

Maravai LifeSciences (ticker MRVI) aligns Nucleic Acid Production and Biologics Safety Testing to serve adjacent biopharma lifecycle needs. Cross-segment insights boost customer intimacy and enable bundled solutions and cross-selling, supporting diversified revenues across the same end markets. In 2024 Maravai reported about $402 million in revenue, underscoring portfolio-driven resilience. This enhances recurring revenue potential and go-to-market efficiency.

High switching costs and qualification barriers

Customers validate suppliers for regulated programs, creating onboarding and requalification hurdles that commonly take 6–12 months and involve extensive documentation and audits. Once reagents and services are specified they are difficult to replace mid-program, driving multi-year revenue durability. This dynamic supports long-term partnerships with leading pharma and biotech, where programs often span 3–5 years.

Exposure to fast-growing modalities

Demand for Maravai’s reagents and safety-testing services is tightly tied to mRNA, oligonucleotide, and advanced biologics growth; the nucleic-acid reagents market is forecast to grow at about 12% CAGR from 2024–2030, and over 10 oligonucleotide therapies had regulatory approval by 2024. Rising modality complexity increases demand for specialized providers and supports Maravai’s premium positioning versus generic suppliers.

- Market tag: ~12% CAGR (2024–2030)

- Regulatory tag: >10 oligo approvals by 2024

- Strategic tag: premium vs generic

Regulatory and quality credibility

Maravai (NASDAQ: MRVI) sustains regulatory and quality credibility through robust QMS, detailed documentation, and consistent compliance that support regulated applications and ease customer audits and tech transfers.

This demonstrated track record accelerates adoption in late-stage programs and underpins expansion into additional regulated offerings, reinforcing customer confidence and reducing time-to-market.

- Regulatory-ready QMS

- Audit-friendly documentation

- Speeds late-stage adoption

- Enables regulated portfolio expansion

Nucleic-acid reagents: regulatory-ready, sticky contracts, $402M 2024 revenue

Maravai supplies mission-critical nucleic-acid reagents with strong pricing power and customer stickiness; 2024 revenue ~$402M. Regulatory-ready QMS and audit-friendly documentation accelerate late-stage adoption and cross-segment sales. Long onboarding/requalification (6–12 months) creates multi-year contract durability while a ~12% nucleic-acid market CAGR (2024–2030) supports sustained demand.

| Metric | Value |

|---|---|

| 2024 Revenue | $402M |

| Market CAGR (2024–2030) | ~12% |

| Oligo approvals by 2024 | >10 |

| Onboarding time | 6–12 months |

| Ticker | MRVI |

What is included in the product

Provides a focused SWOT analysis of Maravai, highlighting internal strengths and weaknesses and external opportunities and threats shaping its biotech reagents and services growth outlook.

Provides a clear, Maravai-specific SWOT matrix for rapid strategic alignment and decision-making, enabling stakeholders to quickly identify risks, opportunities and prioritize action.

Weaknesses

End-market concentration in biotech

End-market concentration in biotech makes Maravai revenue highly sensitive to biotech funding cycles and program progress, so slowdowns in venture funding or IPO activity can quickly dampen orders. This cyclicality complicates forecasting and capacity planning and increases the likelihood of underutilized production. To retain volumes during downturns the company may need to offer pricing or terms concessions, squeezing margins and cash flow.

Product and modality concentration

Maravai’s reliance on nucleic acid reagents and synthetic DNA/RNA ties its performance to modality-specific demand; COVID-19 vaccine volumes peaked in 2021–2022, exposing the company to post-peak volatility. Limited diversification beyond core chemistries heightens exposure to competitive and pricing pressure, which can magnify revenue swings.

Customer concentration risk

Maravai’s revenue is driven by a small number of large programs, so loss or delay of one marquee account can materially affect quarterly and annual results. Public disclosures note concentration risk and that a few customers hold negotiating leverage, which can compress margins or extend payment terms. This customer mix amplifies cash‑flow and margin volatility for the company.

Regulatory and compliance burden

Maintaining GMP and audit readiness requires significant recurring investment in facilities, personnel and validation, increasing OPEX and diverting capital from R&D; quality deviations can trigger production holds, recalls and reputational harm that disrupt revenue streams.

Expanding compliance into new geographies adds regulatory complexity and local approvals, often lengthening time-to-market for new offerings and raising launch costs.

- GMP/audit cost burden

- Holds/recalls risk

- Geographic compliance complexity

- Longer time-to-market

Scale disadvantage versus giants

Global incumbents with broader catalogs can bundle and discount aggressively; Thermo Fisher and Danaher, which each reported roughly $40–50B in 2024 revenue, can outspend Maravai on automation, distribution, and R&D, compressing win rates in price-sensitive segments and raising barriers to adjacent categories.

- Bundling pressure

- R&D & capex scale

- Price-sensitive losses

- Adjacency barriers

End-market concentration and reagent reliance drive revenue volatility and OPEX pressure

End-market concentration in biotech makes Maravai revenue highly sensitive to funding and program timing, driving forecast and capacity risk. Reliance on nucleic acid reagents and post‑COVID modality demand raises volatility and limited product diversification. A few large customers create material concentration and margin pressure while GMP/audit and geographic compliance raise OPEX and slow launches.

| Metric | Value/Note |

|---|---|

| Competitor revenue (2024) | Thermo Fisher, Danaher ≈$40–50B |

| Customer concentration | Material; few large programs |

| Operational burden | High GMP/audit OPEX |

What You See Is What You Get

Maravai SWOT Analysis

This is the actual Maravai SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the complete, editable structure ready for download after payment. Buy now to unlock the entire in-depth version and begin using the full report immediately.