Marel Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

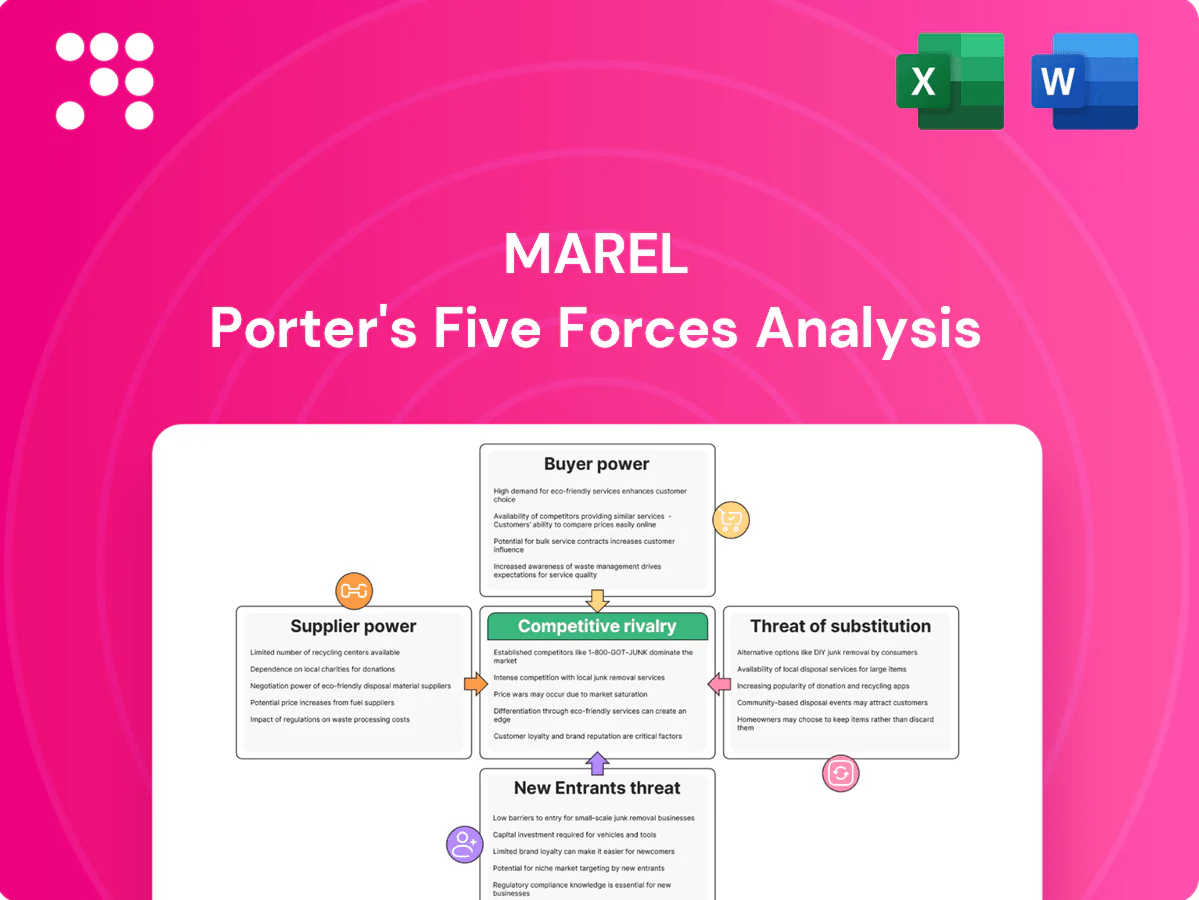

Marel’s Porter's Five Forces offers a concise look at supplier leverage, buyer power, competitive rivalry, substitution risk, and barriers to entry shaping its market — revealing strategic pressures that affect margins and growth. This snapshot highlights key tensions and competitive strengths but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Marel.

Suppliers Bargaining Power

Specialized component dependence

Marel depends on precision mechatronics, food‑grade stainless steel, sensors and vision systems with few qualified suppliers, raising switching costs and lead times; in 2024 Marel reported revenue of about EUR 1.5bn, amplifying supplier leverage on margins. Vendors with hygienic‑design know‑how and IP ratings can command price premiums, while dual‑sourcing and supplier qualification programs partly mitigate this concentration risk.

Commodity inputs with volatility

Commodity inputs such as steel, electronics and plastics saw renewed volatility in 2024 as tight global supply pushed costs upward and suppliers retained near‑term pricing power in constrained segments. Marel mitigates exposure through hedging and product redesign to lower material intensity, while long contracts signed in 2024 helped stabilize portions of input cost. Scale purchasing provides Marel bargaining leverage versus smaller buyers.

Critical software and controls

Controls, PLCs, robotics and embedded software are concentrated among a few OEMs, and firmware compatibility plus certifications create strong vendor lock‑in that raises supplier power over lifecycle updates and spares. This dynamic pressures service margins and capex timing for integrators. Marel offsets dependency by developing proprietary software layers for line control and data integration. Marel reported EUR 1.06bn revenue in 2023, underscoring scale for in‑house R&D.

Aftermarket parts and uptime

High uptime requirements (commonly 99.9% SLA in 2024) make certain aftermarket parts time‑critical; suppliers of bespoke subassemblies can directly affect delivery and service SLAs, often charging expedited fees that add 10–30% to part cost and using priority allocations as leverage.

Global logistics and compliance

Food safety, traceability and regional electrical standards constrain supplier choice, as many vendors fail to meet EHEDG/3‑A or local codes, narrowing sourcing options and raising switching costs. Compliance burdens—documentation, audits and certification—raise supplier bargaining power by creating lock‑in through approved‑vendor lists that slow substitution. Logistics constraints and cross‑border compliance amplify lead times and price sensitivity.

- Food safety limits vendor pool

- EHEDG/3‑A noncompliance narrows options

- Approved‑vendor lists reduce substitution speed

- Compliance audits increase supplier leverage

Few suppliers power hygienic mechatronics: EUR 1.5bn revenue, 99.9% uptime, 10–30% expedite premium

Marel relies on few qualified suppliers for hygienic mechatronics and controls, raising switching costs; 2024 revenue ~EUR 1.5bn increases supplier leverage. Commodity volatility in 2024 pushed input costs; long contracts and hedges mitigate. High uptime (99.9% SLA) and expedited parts (10–30% premium) boost aftermarket supplier power.

| Metric | 2024 |

|---|---|

| Revenue | EUR 1.5bn |

| Uptime SLA | 99.9% |

| Expedite premium | 10–30% |

What is included in the product

Concise Porter's Five Forces assessment tailored to Marel, uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlighting disruptive trends and barriers that shape its pricing power and long-term profitability.

A concise Marel Porter's Five Forces one-sheet that maps supplier, buyer, rivalry, new-entrant and substitute pressures at a glance—ideal for rapid strategic decisions and slide-ready summaries to relieve analysis bottlenecks.

Customers Bargaining Power

Consolidated processors

Large poultry, meat and fish processors purchase at scale and run competitive tenders, using multi-plant footprints and volume commitments to extract multi-year discounts and bundled service agreements, strengthening their negotiating leverage. Marel offsets this by offering performance guarantees, uptime SLAs and integrated end-to-end solutions that tie efficiency improvements to payment models. These contracts shift competition from price to total cost of ownership and demonstrated throughput gains.

High switching costs

Lines are deeply integrated from intake to packing, so switching is risky and often adds 2–8 weeks of downtime for validation and operator retraining, materially disrupting output. Downtime and retraining costs commonly run into multiple percent of production value, which dampens pure price pressure on suppliers. Proven ROI—often targeted within 24 months—and system compatibility remain decisive in renewal decisions.

Performance and TCO focus

Buyers prioritize yield, throughput, labor savings and waste reduction; industry 2024 studies show automation can raise throughput 15–20%, cut labor 20–30%, improve yield 1–3% and lower waste 5–10%. Demonstrable TCO improvements of 10–25% frequently outweigh headline price. Embedded data and analytics anchor value by proving gains in real time. Outcome‑based contracts increasingly shift negotiations from price to performance metrics.

Aftermarket leverage

Aftermarket leverage is strong: spare parts, maintenance, and upgrades are recurring and highly visible to buyers, driving predictable service revenue and retention.

Multi-year service agreements commonly offer bundle discounts, increasing customer stickiness while OEM-specific parts restrict third-party substitutes and preserve margins.

Uptime SLAs and predictive maintenance solutions introduced in 2024 justify premium pricing by reducing customer downtime and total cost of ownership.

- Recurring parts & service revenue

- Bundle discounts in multi-year contracts

- OEM parts limit third-party options

- Uptime SLAs enable premium pricing

Regulatory and ESG demands

Processors face stricter food safety, traceability, and sustainability targets—notably the EU Farm to Fork goal to cut pesticide use and antimicrobial use by 50% by 2030—driving them to demand energy, water, and waste reductions from suppliers and creating specification power over features and materials. Marel’s sustainability credentials can convert these demands into value-add through certified, low-energy processing solutions.

- Regulatory pressure: EU Farm to Fork 50% targets

- Specification power: processors demand energy/water/waste cuts

- Marel edge: sustainability-certified equipment = premium value

Automation raises throughput 15-20%, cuts labor 20-30%, and lowers waste 5-10%

Buyers exert strong price and specification pressure via large tenders, but switching costs, uptime SLAs and outcome‑based contracts shift negotiation toward TCO and performance; 2024 studies show automation raises throughput 15–20%, cuts labor 20–30%, improves yield 1–3% and lowers waste 5–10%.

| Metric | 2024 Impact |

|---|---|

| Throughput | +15–20% |

| Labor | -20–30% |

| Yield | +1–3% |

| Waste | -5–10% |

Preview Before You Purchase

Marel Porter's Five Forces Analysis

This preview shows the exact Marel Porter’s Five Forces Analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the final deliverable; once payment is complete you’ll get instant access to this same file.

Go Beyond the Preview—Access the Full Strategic Report

Marel’s Porter's Five Forces offers a concise look at supplier leverage, buyer power, competitive rivalry, substitution risk, and barriers to entry shaping its market — revealing strategic pressures that affect margins and growth. This snapshot highlights key tensions and competitive strengths but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Marel.

Suppliers Bargaining Power

Specialized component dependence

Marel depends on precision mechatronics, food‑grade stainless steel, sensors and vision systems with few qualified suppliers, raising switching costs and lead times; in 2024 Marel reported revenue of about EUR 1.5bn, amplifying supplier leverage on margins. Vendors with hygienic‑design know‑how and IP ratings can command price premiums, while dual‑sourcing and supplier qualification programs partly mitigate this concentration risk.

Commodity inputs with volatility

Commodity inputs such as steel, electronics and plastics saw renewed volatility in 2024 as tight global supply pushed costs upward and suppliers retained near‑term pricing power in constrained segments. Marel mitigates exposure through hedging and product redesign to lower material intensity, while long contracts signed in 2024 helped stabilize portions of input cost. Scale purchasing provides Marel bargaining leverage versus smaller buyers.

Critical software and controls

Controls, PLCs, robotics and embedded software are concentrated among a few OEMs, and firmware compatibility plus certifications create strong vendor lock‑in that raises supplier power over lifecycle updates and spares. This dynamic pressures service margins and capex timing for integrators. Marel offsets dependency by developing proprietary software layers for line control and data integration. Marel reported EUR 1.06bn revenue in 2023, underscoring scale for in‑house R&D.

Aftermarket parts and uptime

High uptime requirements (commonly 99.9% SLA in 2024) make certain aftermarket parts time‑critical; suppliers of bespoke subassemblies can directly affect delivery and service SLAs, often charging expedited fees that add 10–30% to part cost and using priority allocations as leverage.

Global logistics and compliance

Food safety, traceability and regional electrical standards constrain supplier choice, as many vendors fail to meet EHEDG/3‑A or local codes, narrowing sourcing options and raising switching costs. Compliance burdens—documentation, audits and certification—raise supplier bargaining power by creating lock‑in through approved‑vendor lists that slow substitution. Logistics constraints and cross‑border compliance amplify lead times and price sensitivity.

- Food safety limits vendor pool

- EHEDG/3‑A noncompliance narrows options

- Approved‑vendor lists reduce substitution speed

- Compliance audits increase supplier leverage

Few suppliers power hygienic mechatronics: EUR 1.5bn revenue, 99.9% uptime, 10–30% expedite premium

Marel relies on few qualified suppliers for hygienic mechatronics and controls, raising switching costs; 2024 revenue ~EUR 1.5bn increases supplier leverage. Commodity volatility in 2024 pushed input costs; long contracts and hedges mitigate. High uptime (99.9% SLA) and expedited parts (10–30% premium) boost aftermarket supplier power.

| Metric | 2024 |

|---|---|

| Revenue | EUR 1.5bn |

| Uptime SLA | 99.9% |

| Expedite premium | 10–30% |

What is included in the product

Concise Porter's Five Forces assessment tailored to Marel, uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlighting disruptive trends and barriers that shape its pricing power and long-term profitability.

A concise Marel Porter's Five Forces one-sheet that maps supplier, buyer, rivalry, new-entrant and substitute pressures at a glance—ideal for rapid strategic decisions and slide-ready summaries to relieve analysis bottlenecks.

Customers Bargaining Power

Consolidated processors

Large poultry, meat and fish processors purchase at scale and run competitive tenders, using multi-plant footprints and volume commitments to extract multi-year discounts and bundled service agreements, strengthening their negotiating leverage. Marel offsets this by offering performance guarantees, uptime SLAs and integrated end-to-end solutions that tie efficiency improvements to payment models. These contracts shift competition from price to total cost of ownership and demonstrated throughput gains.

High switching costs

Lines are deeply integrated from intake to packing, so switching is risky and often adds 2–8 weeks of downtime for validation and operator retraining, materially disrupting output. Downtime and retraining costs commonly run into multiple percent of production value, which dampens pure price pressure on suppliers. Proven ROI—often targeted within 24 months—and system compatibility remain decisive in renewal decisions.

Performance and TCO focus

Buyers prioritize yield, throughput, labor savings and waste reduction; industry 2024 studies show automation can raise throughput 15–20%, cut labor 20–30%, improve yield 1–3% and lower waste 5–10%. Demonstrable TCO improvements of 10–25% frequently outweigh headline price. Embedded data and analytics anchor value by proving gains in real time. Outcome‑based contracts increasingly shift negotiations from price to performance metrics.

Aftermarket leverage

Aftermarket leverage is strong: spare parts, maintenance, and upgrades are recurring and highly visible to buyers, driving predictable service revenue and retention.

Multi-year service agreements commonly offer bundle discounts, increasing customer stickiness while OEM-specific parts restrict third-party substitutes and preserve margins.

Uptime SLAs and predictive maintenance solutions introduced in 2024 justify premium pricing by reducing customer downtime and total cost of ownership.

- Recurring parts & service revenue

- Bundle discounts in multi-year contracts

- OEM parts limit third-party options

- Uptime SLAs enable premium pricing

Regulatory and ESG demands

Processors face stricter food safety, traceability, and sustainability targets—notably the EU Farm to Fork goal to cut pesticide use and antimicrobial use by 50% by 2030—driving them to demand energy, water, and waste reductions from suppliers and creating specification power over features and materials. Marel’s sustainability credentials can convert these demands into value-add through certified, low-energy processing solutions.

- Regulatory pressure: EU Farm to Fork 50% targets

- Specification power: processors demand energy/water/waste cuts

- Marel edge: sustainability-certified equipment = premium value

Automation raises throughput 15-20%, cuts labor 20-30%, and lowers waste 5-10%

Buyers exert strong price and specification pressure via large tenders, but switching costs, uptime SLAs and outcome‑based contracts shift negotiation toward TCO and performance; 2024 studies show automation raises throughput 15–20%, cuts labor 20–30%, improves yield 1–3% and lowers waste 5–10%.

| Metric | 2024 Impact |

|---|---|

| Throughput | +15–20% |

| Labor | -20–30% |

| Yield | +1–3% |

| Waste | -5–10% |

Preview Before You Purchase

Marel Porter's Five Forces Analysis

This preview shows the exact Marel Porter’s Five Forces Analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the final deliverable; once payment is complete you’ll get instant access to this same file.

Description

Go Beyond the Preview—Access the Full Strategic Report

Marel’s Porter's Five Forces offers a concise look at supplier leverage, buyer power, competitive rivalry, substitution risk, and barriers to entry shaping its market — revealing strategic pressures that affect margins and growth. This snapshot highlights key tensions and competitive strengths but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations tailored to Marel.

Suppliers Bargaining Power

Specialized component dependence

Marel depends on precision mechatronics, food‑grade stainless steel, sensors and vision systems with few qualified suppliers, raising switching costs and lead times; in 2024 Marel reported revenue of about EUR 1.5bn, amplifying supplier leverage on margins. Vendors with hygienic‑design know‑how and IP ratings can command price premiums, while dual‑sourcing and supplier qualification programs partly mitigate this concentration risk.

Commodity inputs with volatility

Commodity inputs such as steel, electronics and plastics saw renewed volatility in 2024 as tight global supply pushed costs upward and suppliers retained near‑term pricing power in constrained segments. Marel mitigates exposure through hedging and product redesign to lower material intensity, while long contracts signed in 2024 helped stabilize portions of input cost. Scale purchasing provides Marel bargaining leverage versus smaller buyers.

Critical software and controls

Controls, PLCs, robotics and embedded software are concentrated among a few OEMs, and firmware compatibility plus certifications create strong vendor lock‑in that raises supplier power over lifecycle updates and spares. This dynamic pressures service margins and capex timing for integrators. Marel offsets dependency by developing proprietary software layers for line control and data integration. Marel reported EUR 1.06bn revenue in 2023, underscoring scale for in‑house R&D.

Aftermarket parts and uptime

High uptime requirements (commonly 99.9% SLA in 2024) make certain aftermarket parts time‑critical; suppliers of bespoke subassemblies can directly affect delivery and service SLAs, often charging expedited fees that add 10–30% to part cost and using priority allocations as leverage.

Global logistics and compliance

Food safety, traceability and regional electrical standards constrain supplier choice, as many vendors fail to meet EHEDG/3‑A or local codes, narrowing sourcing options and raising switching costs. Compliance burdens—documentation, audits and certification—raise supplier bargaining power by creating lock‑in through approved‑vendor lists that slow substitution. Logistics constraints and cross‑border compliance amplify lead times and price sensitivity.

- Food safety limits vendor pool

- EHEDG/3‑A noncompliance narrows options

- Approved‑vendor lists reduce substitution speed

- Compliance audits increase supplier leverage

Few suppliers power hygienic mechatronics: EUR 1.5bn revenue, 99.9% uptime, 10–30% expedite premium

Marel relies on few qualified suppliers for hygienic mechatronics and controls, raising switching costs; 2024 revenue ~EUR 1.5bn increases supplier leverage. Commodity volatility in 2024 pushed input costs; long contracts and hedges mitigate. High uptime (99.9% SLA) and expedited parts (10–30% premium) boost aftermarket supplier power.

| Metric | 2024 |

|---|---|

| Revenue | EUR 1.5bn |

| Uptime SLA | 99.9% |

| Expedite premium | 10–30% |

What is included in the product

Concise Porter's Five Forces assessment tailored to Marel, uncovering competitive rivalry, supplier and buyer power, threat of new entrants and substitutes, and highlighting disruptive trends and barriers that shape its pricing power and long-term profitability.

A concise Marel Porter's Five Forces one-sheet that maps supplier, buyer, rivalry, new-entrant and substitute pressures at a glance—ideal for rapid strategic decisions and slide-ready summaries to relieve analysis bottlenecks.

Customers Bargaining Power

Consolidated processors

Large poultry, meat and fish processors purchase at scale and run competitive tenders, using multi-plant footprints and volume commitments to extract multi-year discounts and bundled service agreements, strengthening their negotiating leverage. Marel offsets this by offering performance guarantees, uptime SLAs and integrated end-to-end solutions that tie efficiency improvements to payment models. These contracts shift competition from price to total cost of ownership and demonstrated throughput gains.

High switching costs

Lines are deeply integrated from intake to packing, so switching is risky and often adds 2–8 weeks of downtime for validation and operator retraining, materially disrupting output. Downtime and retraining costs commonly run into multiple percent of production value, which dampens pure price pressure on suppliers. Proven ROI—often targeted within 24 months—and system compatibility remain decisive in renewal decisions.

Performance and TCO focus

Buyers prioritize yield, throughput, labor savings and waste reduction; industry 2024 studies show automation can raise throughput 15–20%, cut labor 20–30%, improve yield 1–3% and lower waste 5–10%. Demonstrable TCO improvements of 10–25% frequently outweigh headline price. Embedded data and analytics anchor value by proving gains in real time. Outcome‑based contracts increasingly shift negotiations from price to performance metrics.

Aftermarket leverage

Aftermarket leverage is strong: spare parts, maintenance, and upgrades are recurring and highly visible to buyers, driving predictable service revenue and retention.

Multi-year service agreements commonly offer bundle discounts, increasing customer stickiness while OEM-specific parts restrict third-party substitutes and preserve margins.

Uptime SLAs and predictive maintenance solutions introduced in 2024 justify premium pricing by reducing customer downtime and total cost of ownership.

- Recurring parts & service revenue

- Bundle discounts in multi-year contracts

- OEM parts limit third-party options

- Uptime SLAs enable premium pricing

Regulatory and ESG demands

Processors face stricter food safety, traceability, and sustainability targets—notably the EU Farm to Fork goal to cut pesticide use and antimicrobial use by 50% by 2030—driving them to demand energy, water, and waste reductions from suppliers and creating specification power over features and materials. Marel’s sustainability credentials can convert these demands into value-add through certified, low-energy processing solutions.

- Regulatory pressure: EU Farm to Fork 50% targets

- Specification power: processors demand energy/water/waste cuts

- Marel edge: sustainability-certified equipment = premium value

Automation raises throughput 15-20%, cuts labor 20-30%, and lowers waste 5-10%

Buyers exert strong price and specification pressure via large tenders, but switching costs, uptime SLAs and outcome‑based contracts shift negotiation toward TCO and performance; 2024 studies show automation raises throughput 15–20%, cuts labor 20–30%, improves yield 1–3% and lowers waste 5–10%.

| Metric | 2024 Impact |

|---|---|

| Throughput | +15–20% |

| Labor | -20–30% |

| Yield | +1–3% |

| Waste | -5–10% |

Preview Before You Purchase

Marel Porter's Five Forces Analysis

This preview shows the exact Marel Porter’s Five Forces Analysis you’ll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You’re viewing the final deliverable; once payment is complete you’ll get instant access to this same file.