Martin Marietta Materials PESTLE Analysis

Skip the Research. Get the Strategy.

Our PESTLE analysis reveals how political regulation, infrastructure cycles, and environmental pressure shape Martin Marietta Materials' outlook. We map economic demand drivers, technological adoption, social trends, and legal risks to show clear strategic implications. Ideal for investors and strategists, the full editable report delivers actionable insights—purchase now to get the complete analysis instantly.

Political factors

Federal infrastructure funding cycles

Federal appropriations for highways, bridges and water projects drive Martin Marietta's aggregates and cement demand; multi‑year bills like the IIJA (1.2 trillion USD overall, about 550 billion USD in new spending) provide multi‑year visibility for capital planning. Shifts in administration priorities can reallocate funds between roads and transit, changing product mix, while continuing resolutions and budget gridlock—with roughly 60 billion USD annual federal highway apportionments—can delay lettings and revenue timing.

State & local capital budgets

Most aggregates demand is local and tied to state DOTs and municipal bond-funded projects; the IIJA committed roughly $110 billion for roads and bridges while US municipal bond outstanding was about $4.2 trillion in 2024. Tax receipts, ballot measures and public-private partnerships shape regional pipelines and timing. Regional fiscal health drives uneven geographic performance, and rising resilience and flood-control priorities lift heavy-construction volumes.

Trade and tariff policies

Import duties on cement/clinker and fuel-related sanctions tighten input availability and raise costs for Martin Marietta, while Buy America provisions tied to the $1.2 trillion Infrastructure Investment and Jobs Act steer sourcing and bidding toward domestic suppliers. Cross-border dynamics in Texas and Southeast markets can quickly constrain regional supply, and sudden policy shifts can reset competitive positions across cement and terminal operations.

Permitting and land-use politics

Transportation and logistics policy

- Truck weight: 80,000 lb federal baseline

- HOS: 11/14/70/80 hr + 34‑hr restart

- Ports: IIJA ~17B; PIP awards >3B by 2024

- Costs: tolls/road fees alter per‑load margins

- Incentives: federal/state ZEV grants influence capex

IIJA boost $550B, muni debt $4.2T, FY2024 sales $7.5B

Federal funding (IIJA $1.2T; ~$550B new) and state/muni fiscal health (US muni debt ≈ $4.2T in 2024) drive aggregates/cement demand and timing; permitting delays (12–36 months) and pre‑dev costs ($1–5M) constrain growth. Buy America, tariffs and Buy America steer sourcing; ports/IIJA grants (~$17B; PIP >$3B) ease logistics. FY2024 net sales ≈ $7.5B.

| Metric | Value |

|---|---|

| IIJA | $1.2T ($550B new) |

| Municipal debt (2024) | $4.2T |

| Permitting delay | 12–36 months |

| FY2024 sales | $7.5B |

What is included in the product

Explores how macro-environmental forces uniquely affect Martin Marietta Materials across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven examples tied to construction aggregates and regional markets. Designed for executives and investors, it highlights risks, opportunities, and forward-looking implications to inform strategy, compliance and capital allocation.

A concise, visually segmented PESTLE summary of Martin Marietta Materials that frees teams from digging through reports—ready to drop into presentations, share across departments, and support planning discussions on external risks and market positioning.

Economic factors

Construction cycle sensitivity

Aggregates and ready‑mix volumes move closely with nonresidential, residential and infrastructure cycles, so downturns in private building hit demand while public work from federal and state programs helps offset softness and smooth earnings. Project backlogs give near‑term revenue cushion but roll off in recessions, exposing margins. Shifts toward lower‑value mixes reduce pricing latitude and compress margins.

Interest rates and housing starts

Mortgage rates near 7% in mid‑2025 (Freddie Mac) have pressured single‑family starts and local ready‑mix demand, with single‑family starts down roughly 8–12% year‑over‑year as developers delay projects; higher rates also slow private commercial builds and curb developer activity. Rate cuts historically revive volumes with a 6–12 month lag. Regional affordability shifts amplify impacts in Sunbelt states, which account for about 40% of single‑family starts.

Energy, fuel, and freight costs

Diesel (U.S. average ~$3.98/gal in 2024), electricity and petcoke/natural gas (Henry Hub ~$2.96/MMBtu in 2024) plus rail tariffs materially drive Martin Marietta Materials unit costs, with rail rates rising mid-single digits in 2024; surcharges and dynamic pricing allow partial pass-through but timing gaps create working-capital exposure. Fuel hedging programs and site-level efficiency initiatives reduced volatility impact in 2023–24, yet prolonged fuel or freight spikes compress margins and can shift regional competitive positions.

Pricing power and market structure

Aggregates markets are local oligopolies where high haul costs—often comprising >50% of delivered cost—support disciplined pricing; Martin Marietta leverages tight local supply to protect margins. Cement tightness in fast‑growing regions has enabled list price realization and higher spreads. Contract structures with escalation clauses and targeted M&A to increase quarry density reinforce capture of these pricing gains.

- Local oligopoly: haul >50% of delivered cost

- Cement tightness: supports list price realization

- Contracts: escalation clauses boost capture

- M&A: density/synergies reinforce pricing

Labor availability and wage inflation

Labor shortages for skilled operators and drivers have tightened throughput and raised wages at Martin Marietta; U.S. unemployment averaged about 3.7% in 2024 and average hourly earnings rose roughly 4% year-over-year, increasing operating cost pressure. Overtime and outsourcing widen cost variance and can delay project schedules and deliveries. Apprenticeships and automation investments provide gradual relief to capacity constraints.

- Skilled shortages reduce throughput

- Wage inflation ~4% (2024) raises costs

- Overtime/outsourcing increase cost variance

- Apprenticeships & automation mitigate long-term pressure

IIJA boost $550B, muni debt $4.2T, FY2024 sales $7.5B

Demand tracks nonresidential, residential and infrastructure cycles; project backlogs smooth near‑term revenue but roll off in recessions, exposing margins. Mortgage rates ~7% mid‑2025 cut single‑family starts ~8–12% y/y; rate cuts revive volumes with 6–12 month lag. Fuel (diesel $3.98/gal 2024), freight, labor (+~4% avg hourly earnings 2024) and haul (>50% delivered cost) drive unit costs.

| Metric | Value (2024/2025) |

|---|---|

| Mortgage rate (mid‑2025) | ~7% |

| Single‑family starts y/y | -8–12% |

| Diesel (U.S. avg) | $3.98/gal (2024) |

| Wage inflation | ~4% (2024) |

| Haul share | >50% of delivered cost |

Preview Before You Purchase

Martin Marietta Materials PESTLE Analysis

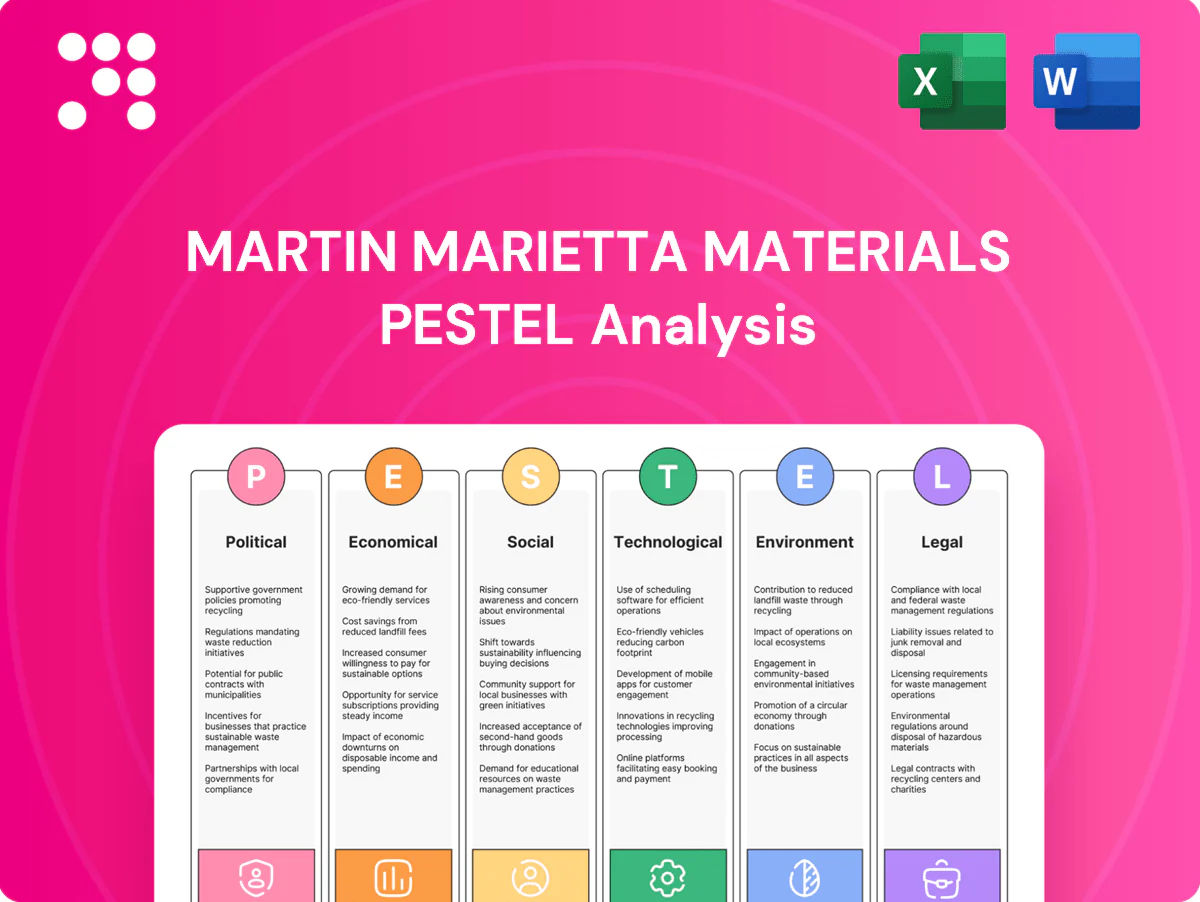

The preview shown here is the exact Martin Marietta Materials PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors in professional structure. No placeholders or edits required; download the same final file upon checkout.

Skip the Research. Get the Strategy.

Our PESTLE analysis reveals how political regulation, infrastructure cycles, and environmental pressure shape Martin Marietta Materials' outlook. We map economic demand drivers, technological adoption, social trends, and legal risks to show clear strategic implications. Ideal for investors and strategists, the full editable report delivers actionable insights—purchase now to get the complete analysis instantly.

Political factors

Federal infrastructure funding cycles

Federal appropriations for highways, bridges and water projects drive Martin Marietta's aggregates and cement demand; multi‑year bills like the IIJA (1.2 trillion USD overall, about 550 billion USD in new spending) provide multi‑year visibility for capital planning. Shifts in administration priorities can reallocate funds between roads and transit, changing product mix, while continuing resolutions and budget gridlock—with roughly 60 billion USD annual federal highway apportionments—can delay lettings and revenue timing.

State & local capital budgets

Most aggregates demand is local and tied to state DOTs and municipal bond-funded projects; the IIJA committed roughly $110 billion for roads and bridges while US municipal bond outstanding was about $4.2 trillion in 2024. Tax receipts, ballot measures and public-private partnerships shape regional pipelines and timing. Regional fiscal health drives uneven geographic performance, and rising resilience and flood-control priorities lift heavy-construction volumes.

Trade and tariff policies

Import duties on cement/clinker and fuel-related sanctions tighten input availability and raise costs for Martin Marietta, while Buy America provisions tied to the $1.2 trillion Infrastructure Investment and Jobs Act steer sourcing and bidding toward domestic suppliers. Cross-border dynamics in Texas and Southeast markets can quickly constrain regional supply, and sudden policy shifts can reset competitive positions across cement and terminal operations.

Permitting and land-use politics

Transportation and logistics policy

- Truck weight: 80,000 lb federal baseline

- HOS: 11/14/70/80 hr + 34‑hr restart

- Ports: IIJA ~17B; PIP awards >3B by 2024

- Costs: tolls/road fees alter per‑load margins

- Incentives: federal/state ZEV grants influence capex

IIJA boost $550B, muni debt $4.2T, FY2024 sales $7.5B

Federal funding (IIJA $1.2T; ~$550B new) and state/muni fiscal health (US muni debt ≈ $4.2T in 2024) drive aggregates/cement demand and timing; permitting delays (12–36 months) and pre‑dev costs ($1–5M) constrain growth. Buy America, tariffs and Buy America steer sourcing; ports/IIJA grants (~$17B; PIP >$3B) ease logistics. FY2024 net sales ≈ $7.5B.

| Metric | Value |

|---|---|

| IIJA | $1.2T ($550B new) |

| Municipal debt (2024) | $4.2T |

| Permitting delay | 12–36 months |

| FY2024 sales | $7.5B |

What is included in the product

Explores how macro-environmental forces uniquely affect Martin Marietta Materials across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven examples tied to construction aggregates and regional markets. Designed for executives and investors, it highlights risks, opportunities, and forward-looking implications to inform strategy, compliance and capital allocation.

A concise, visually segmented PESTLE summary of Martin Marietta Materials that frees teams from digging through reports—ready to drop into presentations, share across departments, and support planning discussions on external risks and market positioning.

Economic factors

Construction cycle sensitivity

Aggregates and ready‑mix volumes move closely with nonresidential, residential and infrastructure cycles, so downturns in private building hit demand while public work from federal and state programs helps offset softness and smooth earnings. Project backlogs give near‑term revenue cushion but roll off in recessions, exposing margins. Shifts toward lower‑value mixes reduce pricing latitude and compress margins.

Interest rates and housing starts

Mortgage rates near 7% in mid‑2025 (Freddie Mac) have pressured single‑family starts and local ready‑mix demand, with single‑family starts down roughly 8–12% year‑over‑year as developers delay projects; higher rates also slow private commercial builds and curb developer activity. Rate cuts historically revive volumes with a 6–12 month lag. Regional affordability shifts amplify impacts in Sunbelt states, which account for about 40% of single‑family starts.

Energy, fuel, and freight costs

Diesel (U.S. average ~$3.98/gal in 2024), electricity and petcoke/natural gas (Henry Hub ~$2.96/MMBtu in 2024) plus rail tariffs materially drive Martin Marietta Materials unit costs, with rail rates rising mid-single digits in 2024; surcharges and dynamic pricing allow partial pass-through but timing gaps create working-capital exposure. Fuel hedging programs and site-level efficiency initiatives reduced volatility impact in 2023–24, yet prolonged fuel or freight spikes compress margins and can shift regional competitive positions.

Pricing power and market structure

Aggregates markets are local oligopolies where high haul costs—often comprising >50% of delivered cost—support disciplined pricing; Martin Marietta leverages tight local supply to protect margins. Cement tightness in fast‑growing regions has enabled list price realization and higher spreads. Contract structures with escalation clauses and targeted M&A to increase quarry density reinforce capture of these pricing gains.

- Local oligopoly: haul >50% of delivered cost

- Cement tightness: supports list price realization

- Contracts: escalation clauses boost capture

- M&A: density/synergies reinforce pricing

Labor availability and wage inflation

Labor shortages for skilled operators and drivers have tightened throughput and raised wages at Martin Marietta; U.S. unemployment averaged about 3.7% in 2024 and average hourly earnings rose roughly 4% year-over-year, increasing operating cost pressure. Overtime and outsourcing widen cost variance and can delay project schedules and deliveries. Apprenticeships and automation investments provide gradual relief to capacity constraints.

- Skilled shortages reduce throughput

- Wage inflation ~4% (2024) raises costs

- Overtime/outsourcing increase cost variance

- Apprenticeships & automation mitigate long-term pressure

IIJA boost $550B, muni debt $4.2T, FY2024 sales $7.5B

Demand tracks nonresidential, residential and infrastructure cycles; project backlogs smooth near‑term revenue but roll off in recessions, exposing margins. Mortgage rates ~7% mid‑2025 cut single‑family starts ~8–12% y/y; rate cuts revive volumes with 6–12 month lag. Fuel (diesel $3.98/gal 2024), freight, labor (+~4% avg hourly earnings 2024) and haul (>50% delivered cost) drive unit costs.

| Metric | Value (2024/2025) |

|---|---|

| Mortgage rate (mid‑2025) | ~7% |

| Single‑family starts y/y | -8–12% |

| Diesel (U.S. avg) | $3.98/gal (2024) |

| Wage inflation | ~4% (2024) |

| Haul share | >50% of delivered cost |

Preview Before You Purchase

Martin Marietta Materials PESTLE Analysis

The preview shown here is the exact Martin Marietta Materials PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors in professional structure. No placeholders or edits required; download the same final file upon checkout.

Original: $10.00

-65%$10.00

$3.50Description

Skip the Research. Get the Strategy.

Our PESTLE analysis reveals how political regulation, infrastructure cycles, and environmental pressure shape Martin Marietta Materials' outlook. We map economic demand drivers, technological adoption, social trends, and legal risks to show clear strategic implications. Ideal for investors and strategists, the full editable report delivers actionable insights—purchase now to get the complete analysis instantly.

Political factors

Federal infrastructure funding cycles

Federal appropriations for highways, bridges and water projects drive Martin Marietta's aggregates and cement demand; multi‑year bills like the IIJA (1.2 trillion USD overall, about 550 billion USD in new spending) provide multi‑year visibility for capital planning. Shifts in administration priorities can reallocate funds between roads and transit, changing product mix, while continuing resolutions and budget gridlock—with roughly 60 billion USD annual federal highway apportionments—can delay lettings and revenue timing.

State & local capital budgets

Most aggregates demand is local and tied to state DOTs and municipal bond-funded projects; the IIJA committed roughly $110 billion for roads and bridges while US municipal bond outstanding was about $4.2 trillion in 2024. Tax receipts, ballot measures and public-private partnerships shape regional pipelines and timing. Regional fiscal health drives uneven geographic performance, and rising resilience and flood-control priorities lift heavy-construction volumes.

Trade and tariff policies

Import duties on cement/clinker and fuel-related sanctions tighten input availability and raise costs for Martin Marietta, while Buy America provisions tied to the $1.2 trillion Infrastructure Investment and Jobs Act steer sourcing and bidding toward domestic suppliers. Cross-border dynamics in Texas and Southeast markets can quickly constrain regional supply, and sudden policy shifts can reset competitive positions across cement and terminal operations.

Permitting and land-use politics

Transportation and logistics policy

- Truck weight: 80,000 lb federal baseline

- HOS: 11/14/70/80 hr + 34‑hr restart

- Ports: IIJA ~17B; PIP awards >3B by 2024

- Costs: tolls/road fees alter per‑load margins

- Incentives: federal/state ZEV grants influence capex

IIJA boost $550B, muni debt $4.2T, FY2024 sales $7.5B

Federal funding (IIJA $1.2T; ~$550B new) and state/muni fiscal health (US muni debt ≈ $4.2T in 2024) drive aggregates/cement demand and timing; permitting delays (12–36 months) and pre‑dev costs ($1–5M) constrain growth. Buy America, tariffs and Buy America steer sourcing; ports/IIJA grants (~$17B; PIP >$3B) ease logistics. FY2024 net sales ≈ $7.5B.

| Metric | Value |

|---|---|

| IIJA | $1.2T ($550B new) |

| Municipal debt (2024) | $4.2T |

| Permitting delay | 12–36 months |

| FY2024 sales | $7.5B |

What is included in the product

Explores how macro-environmental forces uniquely affect Martin Marietta Materials across Political, Economic, Social, Technological, Environmental and Legal dimensions, with data-driven examples tied to construction aggregates and regional markets. Designed for executives and investors, it highlights risks, opportunities, and forward-looking implications to inform strategy, compliance and capital allocation.

A concise, visually segmented PESTLE summary of Martin Marietta Materials that frees teams from digging through reports—ready to drop into presentations, share across departments, and support planning discussions on external risks and market positioning.

Economic factors

Construction cycle sensitivity

Aggregates and ready‑mix volumes move closely with nonresidential, residential and infrastructure cycles, so downturns in private building hit demand while public work from federal and state programs helps offset softness and smooth earnings. Project backlogs give near‑term revenue cushion but roll off in recessions, exposing margins. Shifts toward lower‑value mixes reduce pricing latitude and compress margins.

Interest rates and housing starts

Mortgage rates near 7% in mid‑2025 (Freddie Mac) have pressured single‑family starts and local ready‑mix demand, with single‑family starts down roughly 8–12% year‑over‑year as developers delay projects; higher rates also slow private commercial builds and curb developer activity. Rate cuts historically revive volumes with a 6–12 month lag. Regional affordability shifts amplify impacts in Sunbelt states, which account for about 40% of single‑family starts.

Energy, fuel, and freight costs

Diesel (U.S. average ~$3.98/gal in 2024), electricity and petcoke/natural gas (Henry Hub ~$2.96/MMBtu in 2024) plus rail tariffs materially drive Martin Marietta Materials unit costs, with rail rates rising mid-single digits in 2024; surcharges and dynamic pricing allow partial pass-through but timing gaps create working-capital exposure. Fuel hedging programs and site-level efficiency initiatives reduced volatility impact in 2023–24, yet prolonged fuel or freight spikes compress margins and can shift regional competitive positions.

Pricing power and market structure

Aggregates markets are local oligopolies where high haul costs—often comprising >50% of delivered cost—support disciplined pricing; Martin Marietta leverages tight local supply to protect margins. Cement tightness in fast‑growing regions has enabled list price realization and higher spreads. Contract structures with escalation clauses and targeted M&A to increase quarry density reinforce capture of these pricing gains.

- Local oligopoly: haul >50% of delivered cost

- Cement tightness: supports list price realization

- Contracts: escalation clauses boost capture

- M&A: density/synergies reinforce pricing

Labor availability and wage inflation

Labor shortages for skilled operators and drivers have tightened throughput and raised wages at Martin Marietta; U.S. unemployment averaged about 3.7% in 2024 and average hourly earnings rose roughly 4% year-over-year, increasing operating cost pressure. Overtime and outsourcing widen cost variance and can delay project schedules and deliveries. Apprenticeships and automation investments provide gradual relief to capacity constraints.

- Skilled shortages reduce throughput

- Wage inflation ~4% (2024) raises costs

- Overtime/outsourcing increase cost variance

- Apprenticeships & automation mitigate long-term pressure

IIJA boost $550B, muni debt $4.2T, FY2024 sales $7.5B

Demand tracks nonresidential, residential and infrastructure cycles; project backlogs smooth near‑term revenue but roll off in recessions, exposing margins. Mortgage rates ~7% mid‑2025 cut single‑family starts ~8–12% y/y; rate cuts revive volumes with 6–12 month lag. Fuel (diesel $3.98/gal 2024), freight, labor (+~4% avg hourly earnings 2024) and haul (>50% delivered cost) drive unit costs.

| Metric | Value (2024/2025) |

|---|---|

| Mortgage rate (mid‑2025) | ~7% |

| Single‑family starts y/y | -8–12% |

| Diesel (U.S. avg) | $3.98/gal (2024) |

| Wage inflation | ~4% (2024) |

| Haul share | >50% of delivered cost |

Preview Before You Purchase

Martin Marietta Materials PESTLE Analysis

The preview shown here is the exact Martin Marietta Materials PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It covers Political, Economic, Social, Technological, Legal and Environmental factors in professional structure. No placeholders or edits required; download the same final file upon checkout.