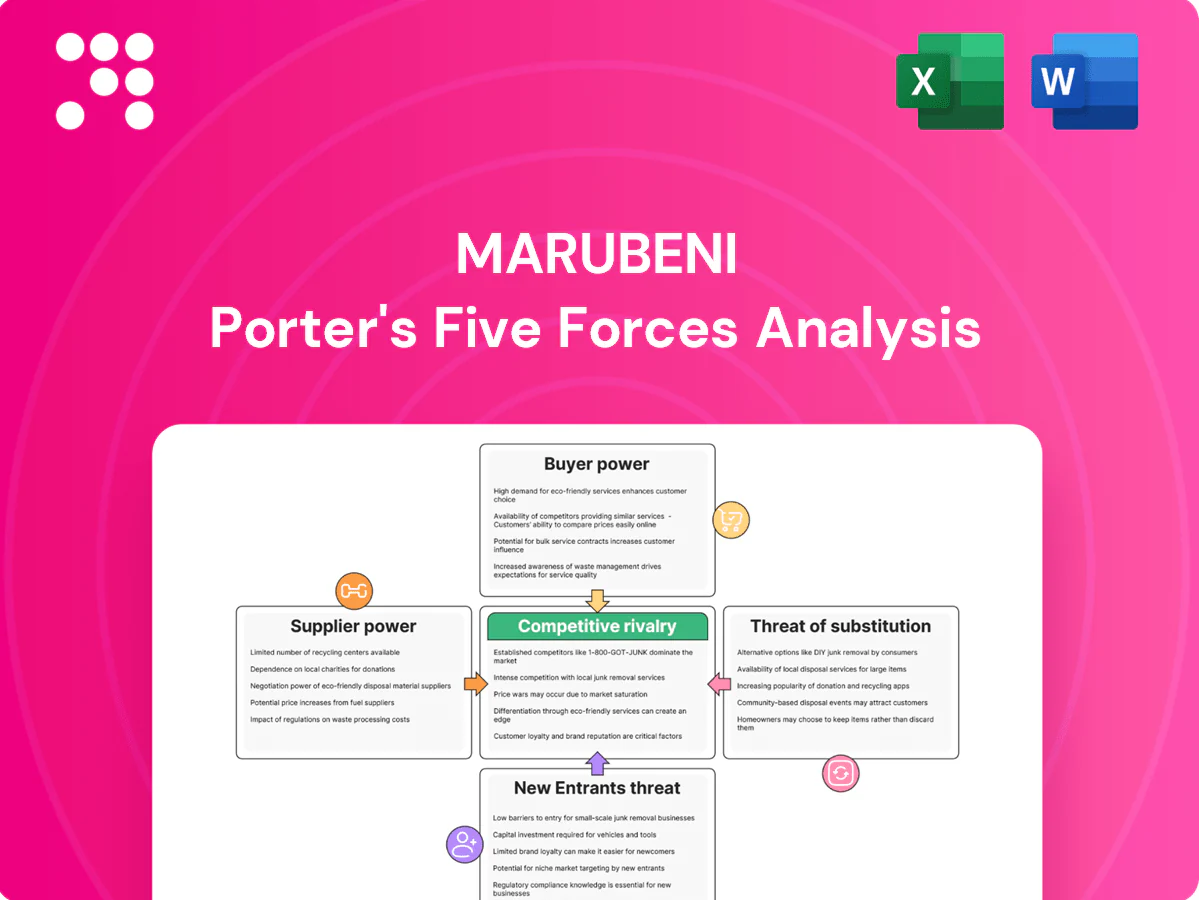

Marubeni Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

Marubeni operates across diversified energy, commodities and infrastructure markets, where supplier leverage, regulatory shifts and integrated competitors shape margins and growth prospects. This snapshot highlights key competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Marubeni’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated resource owners

Many upstream resources Marubeni trades—oil/LNG/copper/grains—are controlled by concentrated players: NOCs hold ~80% of proven oil reserves, the top 4 grain traders handle ~70% of trade, and the five largest copper producers account for roughly 40% of output, raising switching costs and supplier pricing power. Marubeni mitigates via equity stakes, JVs and multi-source portfolios, yet geopolitical shocks can quickly shift leverage back to suppliers.

Logistics and infrastructure dependencies

Port capacity, rail, shipping and storage providers can become chokepoints that raise supplier bargaining power; over 80% of global trade by volume moves by sea (UNCTAD). In tight freight or container markets vendors pass through higher rates and stricter terms. Marubeni’s scale and owned/leased logistics assets improve negotiating leverage, yet port or rail disruptions still expose it to elevated supplier power.

Specialized equipment and technology

Power projects, heavy machinery and specialty chemicals depend on proprietary OEMs and licensors, creating limited alternatives and certification barriers that elevate supplier bargaining power. In 2024 Marubeni reinforced risk mitigation via framework agreements and expanded multi-OEM sourcing across key portfolios. Despite these steps, technical lock-in in certain verticals maintains above-average supplier leverage. Supplier influence remains a material project risk for Marubeni in 2024.

Agricultural origination networks

Farm cooperatives and local aggregators can wield significant leverage in tight harvests; 2023/24 El Niño disruptions and policy shifts (export curbs) amplified that pricing power during regional shortages. Marubeni counters with long-term origination contracts and advisory programs to secure volumes and manage risk. Still, seasonal scarcity episodes can quickly swing bargaining power to suppliers, pressuring margins.

- FAO 2023 cereals production ~2.8 billion tonnes — supply shocks raise supplier leverage

- Long-term contracts and advisory services reduce but do not eliminate origination risk

- Export policy shifts and seasonal scarcity are primary short-term bargaining drivers

ESG and compliance constraints

Stricter ESG standards shrink Marubeni's pool of acceptable suppliers, increasing supplier leverage as certification requirements (e.g., RSPO, FSC) and due diligence commonly add switching frictions and certification timelines often exceeding 12 months. Marubeni invests in supplier development programs to expand compliant capacity, but in the interim compliant suppliers command favorable commercial terms.

- Fewer qualified suppliers → higher bargaining power

- Certification/due diligence >12 months → switching costs

- Supplier development reduces long-term risk, short-term premium pricing

Supplier Power Surges: Commodity Concentration and Sea Chokepoints Heighten 2024 Risk

Supplier power is elevated: NOCs hold ~80% of proven oil reserves, top-4 grain traders ~70% of trade and five largest copper producers ~40% of output, raising pricing and switching costs. Logistics chokepoints matter—>80% trade by sea (UNCTAD). Marubeni offsets with JVs, long-term contracts, supplier development and multi-OEM sourcing, but geopolitical/seasonal shocks keep supplier leverage material in 2024.

| Metric | 2023/24 |

|---|---|

| Oil reserves (NOCs) | ~80% |

| Top-4 grain traders | ~70% |

| Top-5 copper producers | ~40% |

| Trade by sea | >80% (UNCTAD) |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry risks, substitutes, and industry rivalry specific to Marubeni, offering data-backed strategic commentary and highlighting disruptive threats and protective barriers to inform investors and corporate strategy.

A concise one-sheet Marubeni Porter’s Five Forces analysis that visualizes and customizes competitive pressures, helping teams quickly identify and relieve strategic pain points with copy-ready visuals for pitch decks and boardroom slides.

Customers Bargaining Power

Large industrial and utility buyers

Utilities, steelmakers, and refiners buy in bulk and run competitive tenders, enhancing bargaining power; global crude steel output was about 1.878 billion tonnes in 2023, underscoring the scale of off‑takers.

Long‑dated contracts can lock in margins for sellers but also anchor prices close to market benchmarks, limiting upside in tight markets.

Marubeni leverages portfolio optionality to meet specifications and delivery windows, yet buyers’ scale keeps pricing pressure persistent.

Retail and foodservice chains

Downstream retail and foodservice clients demand price stability, high quality and full traceability, increasingly enforced through digital audits; in many markets the top five grocery chains account for over 40% of national grocery sales, concentrating buyer power and strict SLAs. Marubeni leverages supply assurance and private-label solutions to lock in volume and margin, but margin compression in commoditized categories remains a material risk to profitability.

Financial sophistication and transparency

By 2024 many buyers benchmark to LME, Platts and ICE and deploy hedging, narrowing trading spreads and raising switching pressure; transparency and indexation have compressed commodity margins. Marubeni, with FY2023 revenue about ¥7.9 trillion, offsets this by offering risk‑management and structured hedging that create client stickiness beyond price, but market transparency caps outsized margins.

Multi-sourcing and tendering

Buyers routinely multi-source across trading houses to de-risk supply, and frequent tendering in 2024 has intensified price competition, eroding seller leverage; deep relationship reliability still wins tie-breaks but rigorous processes keep buyers advantaged on contract terms.

- Dual-sourcing common

- Tendering raises price pressure

- Relationships can secure awards

- Procurement rigor preserves leverage

Sustainability and provenance demands

Rising ESG and provenance demands are shifting compliance costs upstream, and in 2024 Marubeni scaled sustainability investments (≈JPY 30bn) to bolster traceability and certification for commodity and consumer supply chains.

- Buyers can delist non-compliant SKUs, increasing buyer power

- Marubeni offers traceability/certification services to meet buyer standards

- Compliance costs often borne by suppliers without clear price premia

Buyers, top grocers (>40%) squeeze margins despite ¥7.9tn revenue

Large industrial buyers and top grocery chains (top 5 >40% national sales) drive strong bargaining power through bulk tenders, dual‑sourcing and index benchmarking (LME/Platts/ICE). Marubeni FY2023 revenue ≈¥7.9tn and JPY30bn 2024 sustainability spend mitigate but do not eliminate margin pressure.

| Metric | Value |

|---|---|

| Top5 grocery share | >40% |

| Global steel output 2023 | 1.878bn t |

| Marubeni FY2023 rev | ¥7.9tn |

What You See Is What You Get

Marubeni Porter's Five Forces Analysis

This preview displays the exact Marubeni Porter's Five Forces analysis you'll receive after purchase: a concise, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. No samples or placeholders—this is the full, ready-to-use document. Complete your purchase and get immediate access to this same file for download and use.

A Must-Have Tool for Decision-Makers

Marubeni operates across diversified energy, commodities and infrastructure markets, where supplier leverage, regulatory shifts and integrated competitors shape margins and growth prospects. This snapshot highlights key competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Marubeni’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated resource owners

Many upstream resources Marubeni trades—oil/LNG/copper/grains—are controlled by concentrated players: NOCs hold ~80% of proven oil reserves, the top 4 grain traders handle ~70% of trade, and the five largest copper producers account for roughly 40% of output, raising switching costs and supplier pricing power. Marubeni mitigates via equity stakes, JVs and multi-source portfolios, yet geopolitical shocks can quickly shift leverage back to suppliers.

Logistics and infrastructure dependencies

Port capacity, rail, shipping and storage providers can become chokepoints that raise supplier bargaining power; over 80% of global trade by volume moves by sea (UNCTAD). In tight freight or container markets vendors pass through higher rates and stricter terms. Marubeni’s scale and owned/leased logistics assets improve negotiating leverage, yet port or rail disruptions still expose it to elevated supplier power.

Specialized equipment and technology

Power projects, heavy machinery and specialty chemicals depend on proprietary OEMs and licensors, creating limited alternatives and certification barriers that elevate supplier bargaining power. In 2024 Marubeni reinforced risk mitigation via framework agreements and expanded multi-OEM sourcing across key portfolios. Despite these steps, technical lock-in in certain verticals maintains above-average supplier leverage. Supplier influence remains a material project risk for Marubeni in 2024.

Agricultural origination networks

Farm cooperatives and local aggregators can wield significant leverage in tight harvests; 2023/24 El Niño disruptions and policy shifts (export curbs) amplified that pricing power during regional shortages. Marubeni counters with long-term origination contracts and advisory programs to secure volumes and manage risk. Still, seasonal scarcity episodes can quickly swing bargaining power to suppliers, pressuring margins.

- FAO 2023 cereals production ~2.8 billion tonnes — supply shocks raise supplier leverage

- Long-term contracts and advisory services reduce but do not eliminate origination risk

- Export policy shifts and seasonal scarcity are primary short-term bargaining drivers

ESG and compliance constraints

Stricter ESG standards shrink Marubeni's pool of acceptable suppliers, increasing supplier leverage as certification requirements (e.g., RSPO, FSC) and due diligence commonly add switching frictions and certification timelines often exceeding 12 months. Marubeni invests in supplier development programs to expand compliant capacity, but in the interim compliant suppliers command favorable commercial terms.

- Fewer qualified suppliers → higher bargaining power

- Certification/due diligence >12 months → switching costs

- Supplier development reduces long-term risk, short-term premium pricing

Supplier Power Surges: Commodity Concentration and Sea Chokepoints Heighten 2024 Risk

Supplier power is elevated: NOCs hold ~80% of proven oil reserves, top-4 grain traders ~70% of trade and five largest copper producers ~40% of output, raising pricing and switching costs. Logistics chokepoints matter—>80% trade by sea (UNCTAD). Marubeni offsets with JVs, long-term contracts, supplier development and multi-OEM sourcing, but geopolitical/seasonal shocks keep supplier leverage material in 2024.

| Metric | 2023/24 |

|---|---|

| Oil reserves (NOCs) | ~80% |

| Top-4 grain traders | ~70% |

| Top-5 copper producers | ~40% |

| Trade by sea | >80% (UNCTAD) |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry risks, substitutes, and industry rivalry specific to Marubeni, offering data-backed strategic commentary and highlighting disruptive threats and protective barriers to inform investors and corporate strategy.

A concise one-sheet Marubeni Porter’s Five Forces analysis that visualizes and customizes competitive pressures, helping teams quickly identify and relieve strategic pain points with copy-ready visuals for pitch decks and boardroom slides.

Customers Bargaining Power

Large industrial and utility buyers

Utilities, steelmakers, and refiners buy in bulk and run competitive tenders, enhancing bargaining power; global crude steel output was about 1.878 billion tonnes in 2023, underscoring the scale of off‑takers.

Long‑dated contracts can lock in margins for sellers but also anchor prices close to market benchmarks, limiting upside in tight markets.

Marubeni leverages portfolio optionality to meet specifications and delivery windows, yet buyers’ scale keeps pricing pressure persistent.

Retail and foodservice chains

Downstream retail and foodservice clients demand price stability, high quality and full traceability, increasingly enforced through digital audits; in many markets the top five grocery chains account for over 40% of national grocery sales, concentrating buyer power and strict SLAs. Marubeni leverages supply assurance and private-label solutions to lock in volume and margin, but margin compression in commoditized categories remains a material risk to profitability.

Financial sophistication and transparency

By 2024 many buyers benchmark to LME, Platts and ICE and deploy hedging, narrowing trading spreads and raising switching pressure; transparency and indexation have compressed commodity margins. Marubeni, with FY2023 revenue about ¥7.9 trillion, offsets this by offering risk‑management and structured hedging that create client stickiness beyond price, but market transparency caps outsized margins.

Multi-sourcing and tendering

Buyers routinely multi-source across trading houses to de-risk supply, and frequent tendering in 2024 has intensified price competition, eroding seller leverage; deep relationship reliability still wins tie-breaks but rigorous processes keep buyers advantaged on contract terms.

- Dual-sourcing common

- Tendering raises price pressure

- Relationships can secure awards

- Procurement rigor preserves leverage

Sustainability and provenance demands

Rising ESG and provenance demands are shifting compliance costs upstream, and in 2024 Marubeni scaled sustainability investments (≈JPY 30bn) to bolster traceability and certification for commodity and consumer supply chains.

- Buyers can delist non-compliant SKUs, increasing buyer power

- Marubeni offers traceability/certification services to meet buyer standards

- Compliance costs often borne by suppliers without clear price premia

Buyers, top grocers (>40%) squeeze margins despite ¥7.9tn revenue

Large industrial buyers and top grocery chains (top 5 >40% national sales) drive strong bargaining power through bulk tenders, dual‑sourcing and index benchmarking (LME/Platts/ICE). Marubeni FY2023 revenue ≈¥7.9tn and JPY30bn 2024 sustainability spend mitigate but do not eliminate margin pressure.

| Metric | Value |

|---|---|

| Top5 grocery share | >40% |

| Global steel output 2023 | 1.878bn t |

| Marubeni FY2023 rev | ¥7.9tn |

What You See Is What You Get

Marubeni Porter's Five Forces Analysis

This preview displays the exact Marubeni Porter's Five Forces analysis you'll receive after purchase: a concise, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. No samples or placeholders—this is the full, ready-to-use document. Complete your purchase and get immediate access to this same file for download and use.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Marubeni operates across diversified energy, commodities and infrastructure markets, where supplier leverage, regulatory shifts and integrated competitors shape margins and growth prospects. This snapshot highlights key competitive tensions but only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Marubeni’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated resource owners

Many upstream resources Marubeni trades—oil/LNG/copper/grains—are controlled by concentrated players: NOCs hold ~80% of proven oil reserves, the top 4 grain traders handle ~70% of trade, and the five largest copper producers account for roughly 40% of output, raising switching costs and supplier pricing power. Marubeni mitigates via equity stakes, JVs and multi-source portfolios, yet geopolitical shocks can quickly shift leverage back to suppliers.

Logistics and infrastructure dependencies

Port capacity, rail, shipping and storage providers can become chokepoints that raise supplier bargaining power; over 80% of global trade by volume moves by sea (UNCTAD). In tight freight or container markets vendors pass through higher rates and stricter terms. Marubeni’s scale and owned/leased logistics assets improve negotiating leverage, yet port or rail disruptions still expose it to elevated supplier power.

Specialized equipment and technology

Power projects, heavy machinery and specialty chemicals depend on proprietary OEMs and licensors, creating limited alternatives and certification barriers that elevate supplier bargaining power. In 2024 Marubeni reinforced risk mitigation via framework agreements and expanded multi-OEM sourcing across key portfolios. Despite these steps, technical lock-in in certain verticals maintains above-average supplier leverage. Supplier influence remains a material project risk for Marubeni in 2024.

Agricultural origination networks

Farm cooperatives and local aggregators can wield significant leverage in tight harvests; 2023/24 El Niño disruptions and policy shifts (export curbs) amplified that pricing power during regional shortages. Marubeni counters with long-term origination contracts and advisory programs to secure volumes and manage risk. Still, seasonal scarcity episodes can quickly swing bargaining power to suppliers, pressuring margins.

- FAO 2023 cereals production ~2.8 billion tonnes — supply shocks raise supplier leverage

- Long-term contracts and advisory services reduce but do not eliminate origination risk

- Export policy shifts and seasonal scarcity are primary short-term bargaining drivers

ESG and compliance constraints

Stricter ESG standards shrink Marubeni's pool of acceptable suppliers, increasing supplier leverage as certification requirements (e.g., RSPO, FSC) and due diligence commonly add switching frictions and certification timelines often exceeding 12 months. Marubeni invests in supplier development programs to expand compliant capacity, but in the interim compliant suppliers command favorable commercial terms.

- Fewer qualified suppliers → higher bargaining power

- Certification/due diligence >12 months → switching costs

- Supplier development reduces long-term risk, short-term premium pricing

Supplier Power Surges: Commodity Concentration and Sea Chokepoints Heighten 2024 Risk

Supplier power is elevated: NOCs hold ~80% of proven oil reserves, top-4 grain traders ~70% of trade and five largest copper producers ~40% of output, raising pricing and switching costs. Logistics chokepoints matter—>80% trade by sea (UNCTAD). Marubeni offsets with JVs, long-term contracts, supplier development and multi-OEM sourcing, but geopolitical/seasonal shocks keep supplier leverage material in 2024.

| Metric | 2023/24 |

|---|---|

| Oil reserves (NOCs) | ~80% |

| Top-4 grain traders | ~70% |

| Top-5 copper producers | ~40% |

| Trade by sea | >80% (UNCTAD) |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, entry risks, substitutes, and industry rivalry specific to Marubeni, offering data-backed strategic commentary and highlighting disruptive threats and protective barriers to inform investors and corporate strategy.

A concise one-sheet Marubeni Porter’s Five Forces analysis that visualizes and customizes competitive pressures, helping teams quickly identify and relieve strategic pain points with copy-ready visuals for pitch decks and boardroom slides.

Customers Bargaining Power

Large industrial and utility buyers

Utilities, steelmakers, and refiners buy in bulk and run competitive tenders, enhancing bargaining power; global crude steel output was about 1.878 billion tonnes in 2023, underscoring the scale of off‑takers.

Long‑dated contracts can lock in margins for sellers but also anchor prices close to market benchmarks, limiting upside in tight markets.

Marubeni leverages portfolio optionality to meet specifications and delivery windows, yet buyers’ scale keeps pricing pressure persistent.

Retail and foodservice chains

Downstream retail and foodservice clients demand price stability, high quality and full traceability, increasingly enforced through digital audits; in many markets the top five grocery chains account for over 40% of national grocery sales, concentrating buyer power and strict SLAs. Marubeni leverages supply assurance and private-label solutions to lock in volume and margin, but margin compression in commoditized categories remains a material risk to profitability.

Financial sophistication and transparency

By 2024 many buyers benchmark to LME, Platts and ICE and deploy hedging, narrowing trading spreads and raising switching pressure; transparency and indexation have compressed commodity margins. Marubeni, with FY2023 revenue about ¥7.9 trillion, offsets this by offering risk‑management and structured hedging that create client stickiness beyond price, but market transparency caps outsized margins.

Multi-sourcing and tendering

Buyers routinely multi-source across trading houses to de-risk supply, and frequent tendering in 2024 has intensified price competition, eroding seller leverage; deep relationship reliability still wins tie-breaks but rigorous processes keep buyers advantaged on contract terms.

- Dual-sourcing common

- Tendering raises price pressure

- Relationships can secure awards

- Procurement rigor preserves leverage

Sustainability and provenance demands

Rising ESG and provenance demands are shifting compliance costs upstream, and in 2024 Marubeni scaled sustainability investments (≈JPY 30bn) to bolster traceability and certification for commodity and consumer supply chains.

- Buyers can delist non-compliant SKUs, increasing buyer power

- Marubeni offers traceability/certification services to meet buyer standards

- Compliance costs often borne by suppliers without clear price premia

Buyers, top grocers (>40%) squeeze margins despite ¥7.9tn revenue

Large industrial buyers and top grocery chains (top 5 >40% national sales) drive strong bargaining power through bulk tenders, dual‑sourcing and index benchmarking (LME/Platts/ICE). Marubeni FY2023 revenue ≈¥7.9tn and JPY30bn 2024 sustainability spend mitigate but do not eliminate margin pressure.

| Metric | Value |

|---|---|

| Top5 grocery share | >40% |

| Global steel output 2023 | 1.878bn t |

| Marubeni FY2023 rev | ¥7.9tn |

What You See Is What You Get

Marubeni Porter's Five Forces Analysis

This preview displays the exact Marubeni Porter's Five Forces analysis you'll receive after purchase: a concise, professionally formatted assessment of competitive rivalry, supplier and buyer power, threats of entry and substitution. No samples or placeholders—this is the full, ready-to-use document. Complete your purchase and get immediate access to this same file for download and use.