Guangdong Marubi Biotechnology Porter's Five Forces Analysis

A Must-Have Tool for Decision-Makers

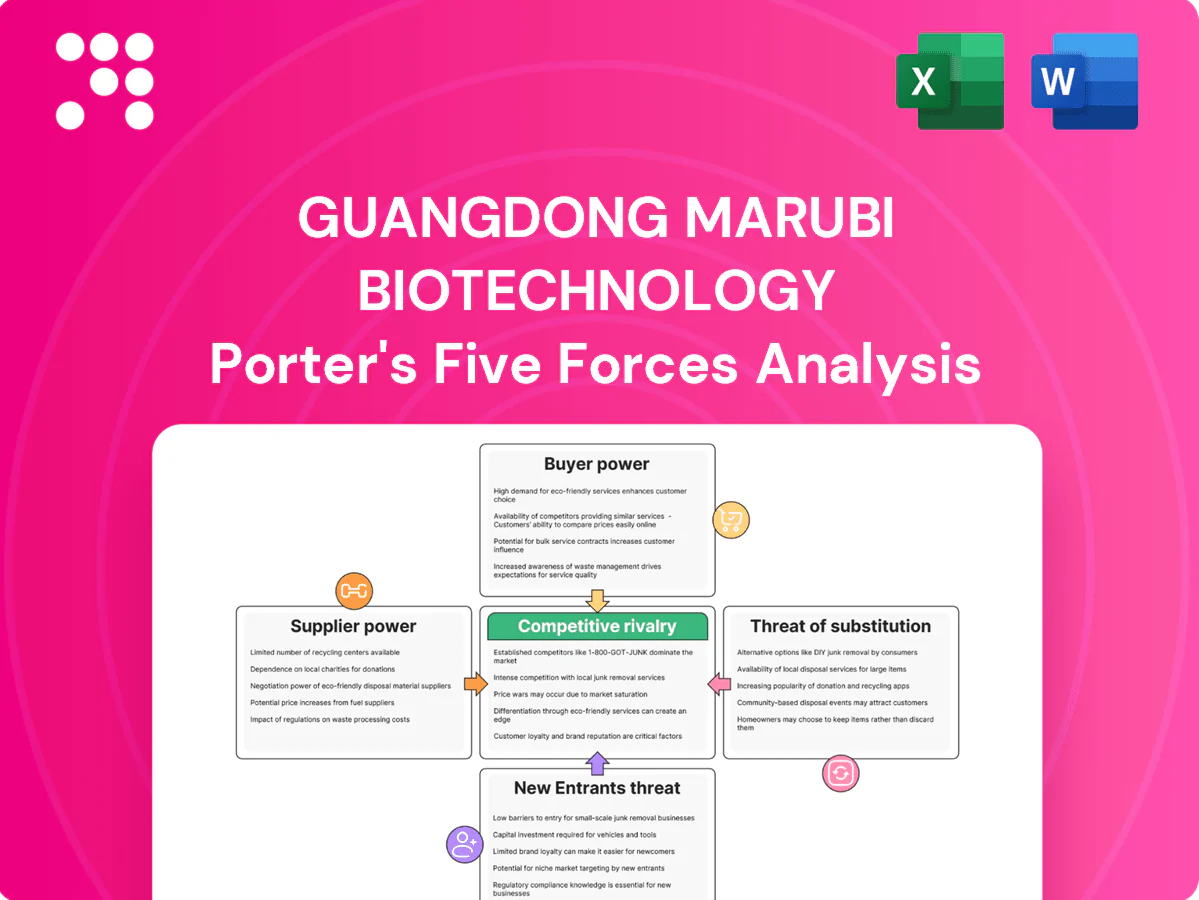

Guangdong Marubi Biotechnology faces intense rivalry from established domestic biotech firms, moderate supplier power due to specialized inputs, and rising buyer leverage as customers demand cost-effective therapies; threats from new entrants and substitutes are tangible given low regulatory barriers for some product lines. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Guangdong Marubi Biotechnology’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Differentiated actives concentration

High-performance inputs such as peptides, hyaluronic acid and advanced encapsulation technologies are concentrated among a few specialty suppliers, notably Bloomage BioTechnology as a leading domestic HA producer in 2024, giving suppliers leverage on pricing and minimum order quantities. Domestic HA leaders can command premiums and priority allocation during tight cycles. Reliance on proprietary actives tightens supply risk at product launches. Dual-sourcing and in-house formulation know‑how partially offset supplier power.

Packaging and component availability

Primary packaging like airless pumps and droppers is widely available in China, which supplies over 60% of global cosmetic packaging (2024), keeping supplier power moderate to low. Custom molds, sustainability specs and premium finishes add 8–12 week lead times and 10–20% setup/cost premiums. Volume commitments (eg >100k units) yield 10–30% discounts but reduce flexibility. Design IP and strict quality controls raise switching costs via 3–6 month requalification and 5–15% extra expense.

OEM/ODM reliance

OEM/ODM reliance gives Guangdong Marubi capex-light scaling—2024 industry data indicate outsourced scale-ups can cut capital needs by roughly 30–60% and compress time-to-market to under 12 months; however, top-tier ODMs with proprietary pipelines command stronger bargaining power. Queue times and line-allocation often prioritize larger clients, sometimes capturing the majority of available slots. Knowledge spillover risk increases dependence on select partners, so internal R&D, partial insourcing or strategic alliances are common levers to rebalance terms.

Imported inputs and FX exposure

Imported fragrances, specialty actives and some machinery expose Guangdong Marubi to FX and logistics risk, with USD/CNY averaging about 7.27 in 2024, enabling suppliers to pass through currency moves and surcharges during tight global supply cycles.

- Longer lead times: higher supplier leverage

- Regulatory docs raise switching costs

- Forward hedging and local sourcing reduce exposure

Digital and media gatekeepers

Traffic, data, and ad inventory on major platforms act as quasi-suppliers, with top platforms capturing over 70% of China digital ad spend in 2024 and concentrating demand generation; auction-based pricing and peak-campaign congestion can raise CPM/CPC by 2–3x, increasing acquisition costs. KOL/MCN agencies with top creators often command >¥1m per campaign and exert fee and scheduling power, so diversifying channels and building owned media reduces dependency.

- Platforms: >70% share of digital ad spend (2024)

- Peak CPM/CPC: +2–3x

- KOL fees: >¥1m/top campaign

- Mitigation: diversify channels; grow owned media

Concentrated actives boost leverage; China packaging >60%; dual-source

High-performance actives concentrated among few suppliers (eg Bloomage BioTechnology leading HA in 2024) give supplier pricing and allocation leverage. Packaging is widely available (China >60% global share, 2024) so supplier power is moderate except for custom specs with 8–12wk leads and 10–20% premiums. ODMs, platforms (>70% digital ad spend) and KOLs (>¥1m/campaign) add bargaining pressure; hedging, dual-sourcing and partial insourcing mitigate.

| Metric | 2024 Data |

|---|---|

| China cosmetic packaging share | >60% |

| USD/CNY avg | 7.27 |

| Platforms ad spend share | >70% |

| Top KOL fee | >¥1m/campaign |

What is included in the product

Tailored Porter's Five Forces analysis for Guangdong Marubi Biotechnology that uncovers competitive intensity, buyer and supplier power, barriers to entry, and substitute threats, highlighting disruptive forces, pricing pressure, and strategic protections to inform investor materials and internal strategy.

A concise one-sheet Porter's Five Forces for Guangdong Marubi Biotechnology that pinpoints competitive pain points—supplier/buyer power, substitutes, new entrants, and industry rivalry—so leadership can quickly triage strategic risks, update for regulatory shifts, and drop the visual into pitch decks or boardroom slides.

Customers Bargaining Power

Low switching costs

Consumers can easily trial rival brands across price tiers, squeezing margins as China’s cosmetics market growth slowed to 6.5% in 2024 and price-driven entrants proliferate.

Small trial sizes and frequent promotions—with online events accounting for an estimated 45% of peak-period sales in 2024—amplify churn and raise acquisition costs.

Loyalty in cosmetics is often campaign-driven rather than structural, so differentiated efficacy claims and sustained community programs are needed to lower price elasticity and improve retention.

Channel intermediaries’ take rates

E-commerce platforms (eg Alibaba/Tmall commission ranges historically 0.5–5%) and offline chains negotiate commissions, marketing slots and returns policies, raising take rates. High traffic costs and platform ad fees—brands report peak-period promo spends reaching 20–30% of GMV during 11.11—compress unit economics. Retailers insist on promotional support and exclusive SKUs; strong sell-through and SKU-level sell-through data materially improve negotiating leverage.

Information transparency

Reviews, ingredient analyzers and social content make pricing and performance highly comparable for Guangdong Marubi; BrightLocal 2024 found about 77% of consumers consult reviews before purchase, heightening price sensitivity. Negative sentiment can spread rapidly across Weibo and Xiaohongshu, often forcing reactive discounts and short-term promos. Claims substantiation via CNAS-accredited third-party testing and clear labeling, plus credible KOL endorsements, help sustain premium pricing.

Price sensitivity in mass segments

Guangdong Marubi faces high price sensitivity in mass segments: in 2024 its core domestic customers remain value-oriented with over half of sales concentrated in entry-to-mid price bands, driven by shopping festivals that anchor reference prices and spike traffic during 11.11 and 6.18 campaigns.

Bundling, tiered portfolios and AOV-protection tactics limit churn; trading-up requires clearly demonstrated efficacy and visible design upgrades to overcome price elasticity.

Institutional buyers and gifting

Institutional buyers and gifting clients exert strong bargaining power in 2024, leveraging bulk orders to demand volume discounts and strict fill-rate commitments that trigger penalties or rebates when forecast accuracy falters. Private-label requests have increased, pressuring margins if accepted, while contract terms now more frequently hinge on service-level guarantees and exclusivity clauses tied to delivery performance.

- Bulk orders -> volume discounts

- Forecast accuracy -> fill-rate penalties/rebates

- Private-label requests -> margin pressure

- Contracts -> service levels & exclusivity

Consumers command pricing as online sales and reviews force promotional dependence

Customers hold strong bargaining power: easy brand switching and slowed market growth (6.5% in 2024) compress margins, while online peak sales (≈45% in 2024) and review-driven buying (≈77% consult reviews) increase price sensitivity. Festival anchoring and entry-to-mid concentration (>50% sales) force promotional dependence; institutional bulk buyers demand discounts and service SLAs. Differentiation via CNAS testing and KOLs needed to defend premiums.

| Metric | 2024 |

|---|---|

| China cosmetics growth | 6.5% |

| Online peak sales share | 45% |

| Consumers consulting reviews | 77% |

| Sales in entry–mid bands | >50% |

| Peak promo spend (GMV) | 20–30% |

What You See Is What You Get

Guangdong Marubi Biotechnology Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Guangdong Marubi Biotechnology you'll receive after purchase—fully formatted, sourced, and ready to use. No placeholders or excerpts; the file you see is the complete deliverable. Buy once for instant download and immediate application.

A Must-Have Tool for Decision-Makers

Guangdong Marubi Biotechnology faces intense rivalry from established domestic biotech firms, moderate supplier power due to specialized inputs, and rising buyer leverage as customers demand cost-effective therapies; threats from new entrants and substitutes are tangible given low regulatory barriers for some product lines. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Guangdong Marubi Biotechnology’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Differentiated actives concentration

High-performance inputs such as peptides, hyaluronic acid and advanced encapsulation technologies are concentrated among a few specialty suppliers, notably Bloomage BioTechnology as a leading domestic HA producer in 2024, giving suppliers leverage on pricing and minimum order quantities. Domestic HA leaders can command premiums and priority allocation during tight cycles. Reliance on proprietary actives tightens supply risk at product launches. Dual-sourcing and in-house formulation know‑how partially offset supplier power.

Packaging and component availability

Primary packaging like airless pumps and droppers is widely available in China, which supplies over 60% of global cosmetic packaging (2024), keeping supplier power moderate to low. Custom molds, sustainability specs and premium finishes add 8–12 week lead times and 10–20% setup/cost premiums. Volume commitments (eg >100k units) yield 10–30% discounts but reduce flexibility. Design IP and strict quality controls raise switching costs via 3–6 month requalification and 5–15% extra expense.

OEM/ODM reliance

OEM/ODM reliance gives Guangdong Marubi capex-light scaling—2024 industry data indicate outsourced scale-ups can cut capital needs by roughly 30–60% and compress time-to-market to under 12 months; however, top-tier ODMs with proprietary pipelines command stronger bargaining power. Queue times and line-allocation often prioritize larger clients, sometimes capturing the majority of available slots. Knowledge spillover risk increases dependence on select partners, so internal R&D, partial insourcing or strategic alliances are common levers to rebalance terms.

Imported inputs and FX exposure

Imported fragrances, specialty actives and some machinery expose Guangdong Marubi to FX and logistics risk, with USD/CNY averaging about 7.27 in 2024, enabling suppliers to pass through currency moves and surcharges during tight global supply cycles.

- Longer lead times: higher supplier leverage

- Regulatory docs raise switching costs

- Forward hedging and local sourcing reduce exposure

Digital and media gatekeepers

Traffic, data, and ad inventory on major platforms act as quasi-suppliers, with top platforms capturing over 70% of China digital ad spend in 2024 and concentrating demand generation; auction-based pricing and peak-campaign congestion can raise CPM/CPC by 2–3x, increasing acquisition costs. KOL/MCN agencies with top creators often command >¥1m per campaign and exert fee and scheduling power, so diversifying channels and building owned media reduces dependency.

- Platforms: >70% share of digital ad spend (2024)

- Peak CPM/CPC: +2–3x

- KOL fees: >¥1m/top campaign

- Mitigation: diversify channels; grow owned media

Concentrated actives boost leverage; China packaging >60%; dual-source

High-performance actives concentrated among few suppliers (eg Bloomage BioTechnology leading HA in 2024) give supplier pricing and allocation leverage. Packaging is widely available (China >60% global share, 2024) so supplier power is moderate except for custom specs with 8–12wk leads and 10–20% premiums. ODMs, platforms (>70% digital ad spend) and KOLs (>¥1m/campaign) add bargaining pressure; hedging, dual-sourcing and partial insourcing mitigate.

| Metric | 2024 Data |

|---|---|

| China cosmetic packaging share | >60% |

| USD/CNY avg | 7.27 |

| Platforms ad spend share | >70% |

| Top KOL fee | >¥1m/campaign |

What is included in the product

Tailored Porter's Five Forces analysis for Guangdong Marubi Biotechnology that uncovers competitive intensity, buyer and supplier power, barriers to entry, and substitute threats, highlighting disruptive forces, pricing pressure, and strategic protections to inform investor materials and internal strategy.

A concise one-sheet Porter's Five Forces for Guangdong Marubi Biotechnology that pinpoints competitive pain points—supplier/buyer power, substitutes, new entrants, and industry rivalry—so leadership can quickly triage strategic risks, update for regulatory shifts, and drop the visual into pitch decks or boardroom slides.

Customers Bargaining Power

Low switching costs

Consumers can easily trial rival brands across price tiers, squeezing margins as China’s cosmetics market growth slowed to 6.5% in 2024 and price-driven entrants proliferate.

Small trial sizes and frequent promotions—with online events accounting for an estimated 45% of peak-period sales in 2024—amplify churn and raise acquisition costs.

Loyalty in cosmetics is often campaign-driven rather than structural, so differentiated efficacy claims and sustained community programs are needed to lower price elasticity and improve retention.

Channel intermediaries’ take rates

E-commerce platforms (eg Alibaba/Tmall commission ranges historically 0.5–5%) and offline chains negotiate commissions, marketing slots and returns policies, raising take rates. High traffic costs and platform ad fees—brands report peak-period promo spends reaching 20–30% of GMV during 11.11—compress unit economics. Retailers insist on promotional support and exclusive SKUs; strong sell-through and SKU-level sell-through data materially improve negotiating leverage.

Information transparency

Reviews, ingredient analyzers and social content make pricing and performance highly comparable for Guangdong Marubi; BrightLocal 2024 found about 77% of consumers consult reviews before purchase, heightening price sensitivity. Negative sentiment can spread rapidly across Weibo and Xiaohongshu, often forcing reactive discounts and short-term promos. Claims substantiation via CNAS-accredited third-party testing and clear labeling, plus credible KOL endorsements, help sustain premium pricing.

Price sensitivity in mass segments

Guangdong Marubi faces high price sensitivity in mass segments: in 2024 its core domestic customers remain value-oriented with over half of sales concentrated in entry-to-mid price bands, driven by shopping festivals that anchor reference prices and spike traffic during 11.11 and 6.18 campaigns.

Bundling, tiered portfolios and AOV-protection tactics limit churn; trading-up requires clearly demonstrated efficacy and visible design upgrades to overcome price elasticity.

Institutional buyers and gifting

Institutional buyers and gifting clients exert strong bargaining power in 2024, leveraging bulk orders to demand volume discounts and strict fill-rate commitments that trigger penalties or rebates when forecast accuracy falters. Private-label requests have increased, pressuring margins if accepted, while contract terms now more frequently hinge on service-level guarantees and exclusivity clauses tied to delivery performance.

- Bulk orders -> volume discounts

- Forecast accuracy -> fill-rate penalties/rebates

- Private-label requests -> margin pressure

- Contracts -> service levels & exclusivity

Consumers command pricing as online sales and reviews force promotional dependence

Customers hold strong bargaining power: easy brand switching and slowed market growth (6.5% in 2024) compress margins, while online peak sales (≈45% in 2024) and review-driven buying (≈77% consult reviews) increase price sensitivity. Festival anchoring and entry-to-mid concentration (>50% sales) force promotional dependence; institutional bulk buyers demand discounts and service SLAs. Differentiation via CNAS testing and KOLs needed to defend premiums.

| Metric | 2024 |

|---|---|

| China cosmetics growth | 6.5% |

| Online peak sales share | 45% |

| Consumers consulting reviews | 77% |

| Sales in entry–mid bands | >50% |

| Peak promo spend (GMV) | 20–30% |

What You See Is What You Get

Guangdong Marubi Biotechnology Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Guangdong Marubi Biotechnology you'll receive after purchase—fully formatted, sourced, and ready to use. No placeholders or excerpts; the file you see is the complete deliverable. Buy once for instant download and immediate application.

Original: $10.00

-65%$10.00

$3.50Description

A Must-Have Tool for Decision-Makers

Guangdong Marubi Biotechnology faces intense rivalry from established domestic biotech firms, moderate supplier power due to specialized inputs, and rising buyer leverage as customers demand cost-effective therapies; threats from new entrants and substitutes are tangible given low regulatory barriers for some product lines. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Guangdong Marubi Biotechnology’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Differentiated actives concentration

High-performance inputs such as peptides, hyaluronic acid and advanced encapsulation technologies are concentrated among a few specialty suppliers, notably Bloomage BioTechnology as a leading domestic HA producer in 2024, giving suppliers leverage on pricing and minimum order quantities. Domestic HA leaders can command premiums and priority allocation during tight cycles. Reliance on proprietary actives tightens supply risk at product launches. Dual-sourcing and in-house formulation know‑how partially offset supplier power.

Packaging and component availability

Primary packaging like airless pumps and droppers is widely available in China, which supplies over 60% of global cosmetic packaging (2024), keeping supplier power moderate to low. Custom molds, sustainability specs and premium finishes add 8–12 week lead times and 10–20% setup/cost premiums. Volume commitments (eg >100k units) yield 10–30% discounts but reduce flexibility. Design IP and strict quality controls raise switching costs via 3–6 month requalification and 5–15% extra expense.

OEM/ODM reliance

OEM/ODM reliance gives Guangdong Marubi capex-light scaling—2024 industry data indicate outsourced scale-ups can cut capital needs by roughly 30–60% and compress time-to-market to under 12 months; however, top-tier ODMs with proprietary pipelines command stronger bargaining power. Queue times and line-allocation often prioritize larger clients, sometimes capturing the majority of available slots. Knowledge spillover risk increases dependence on select partners, so internal R&D, partial insourcing or strategic alliances are common levers to rebalance terms.

Imported inputs and FX exposure

Imported fragrances, specialty actives and some machinery expose Guangdong Marubi to FX and logistics risk, with USD/CNY averaging about 7.27 in 2024, enabling suppliers to pass through currency moves and surcharges during tight global supply cycles.

- Longer lead times: higher supplier leverage

- Regulatory docs raise switching costs

- Forward hedging and local sourcing reduce exposure

Digital and media gatekeepers

Traffic, data, and ad inventory on major platforms act as quasi-suppliers, with top platforms capturing over 70% of China digital ad spend in 2024 and concentrating demand generation; auction-based pricing and peak-campaign congestion can raise CPM/CPC by 2–3x, increasing acquisition costs. KOL/MCN agencies with top creators often command >¥1m per campaign and exert fee and scheduling power, so diversifying channels and building owned media reduces dependency.

- Platforms: >70% share of digital ad spend (2024)

- Peak CPM/CPC: +2–3x

- KOL fees: >¥1m/top campaign

- Mitigation: diversify channels; grow owned media

Concentrated actives boost leverage; China packaging >60%; dual-source

High-performance actives concentrated among few suppliers (eg Bloomage BioTechnology leading HA in 2024) give supplier pricing and allocation leverage. Packaging is widely available (China >60% global share, 2024) so supplier power is moderate except for custom specs with 8–12wk leads and 10–20% premiums. ODMs, platforms (>70% digital ad spend) and KOLs (>¥1m/campaign) add bargaining pressure; hedging, dual-sourcing and partial insourcing mitigate.

| Metric | 2024 Data |

|---|---|

| China cosmetic packaging share | >60% |

| USD/CNY avg | 7.27 |

| Platforms ad spend share | >70% |

| Top KOL fee | >¥1m/campaign |

What is included in the product

Tailored Porter's Five Forces analysis for Guangdong Marubi Biotechnology that uncovers competitive intensity, buyer and supplier power, barriers to entry, and substitute threats, highlighting disruptive forces, pricing pressure, and strategic protections to inform investor materials and internal strategy.

A concise one-sheet Porter's Five Forces for Guangdong Marubi Biotechnology that pinpoints competitive pain points—supplier/buyer power, substitutes, new entrants, and industry rivalry—so leadership can quickly triage strategic risks, update for regulatory shifts, and drop the visual into pitch decks or boardroom slides.

Customers Bargaining Power

Low switching costs

Consumers can easily trial rival brands across price tiers, squeezing margins as China’s cosmetics market growth slowed to 6.5% in 2024 and price-driven entrants proliferate.

Small trial sizes and frequent promotions—with online events accounting for an estimated 45% of peak-period sales in 2024—amplify churn and raise acquisition costs.

Loyalty in cosmetics is often campaign-driven rather than structural, so differentiated efficacy claims and sustained community programs are needed to lower price elasticity and improve retention.

Channel intermediaries’ take rates

E-commerce platforms (eg Alibaba/Tmall commission ranges historically 0.5–5%) and offline chains negotiate commissions, marketing slots and returns policies, raising take rates. High traffic costs and platform ad fees—brands report peak-period promo spends reaching 20–30% of GMV during 11.11—compress unit economics. Retailers insist on promotional support and exclusive SKUs; strong sell-through and SKU-level sell-through data materially improve negotiating leverage.

Information transparency

Reviews, ingredient analyzers and social content make pricing and performance highly comparable for Guangdong Marubi; BrightLocal 2024 found about 77% of consumers consult reviews before purchase, heightening price sensitivity. Negative sentiment can spread rapidly across Weibo and Xiaohongshu, often forcing reactive discounts and short-term promos. Claims substantiation via CNAS-accredited third-party testing and clear labeling, plus credible KOL endorsements, help sustain premium pricing.

Price sensitivity in mass segments

Guangdong Marubi faces high price sensitivity in mass segments: in 2024 its core domestic customers remain value-oriented with over half of sales concentrated in entry-to-mid price bands, driven by shopping festivals that anchor reference prices and spike traffic during 11.11 and 6.18 campaigns.

Bundling, tiered portfolios and AOV-protection tactics limit churn; trading-up requires clearly demonstrated efficacy and visible design upgrades to overcome price elasticity.

Institutional buyers and gifting

Institutional buyers and gifting clients exert strong bargaining power in 2024, leveraging bulk orders to demand volume discounts and strict fill-rate commitments that trigger penalties or rebates when forecast accuracy falters. Private-label requests have increased, pressuring margins if accepted, while contract terms now more frequently hinge on service-level guarantees and exclusivity clauses tied to delivery performance.

- Bulk orders -> volume discounts

- Forecast accuracy -> fill-rate penalties/rebates

- Private-label requests -> margin pressure

- Contracts -> service levels & exclusivity

Consumers command pricing as online sales and reviews force promotional dependence

Customers hold strong bargaining power: easy brand switching and slowed market growth (6.5% in 2024) compress margins, while online peak sales (≈45% in 2024) and review-driven buying (≈77% consult reviews) increase price sensitivity. Festival anchoring and entry-to-mid concentration (>50% sales) force promotional dependence; institutional bulk buyers demand discounts and service SLAs. Differentiation via CNAS testing and KOLs needed to defend premiums.

| Metric | 2024 |

|---|---|

| China cosmetics growth | 6.5% |

| Online peak sales share | 45% |

| Consumers consulting reviews | 77% |

| Sales in entry–mid bands | >50% |

| Peak promo spend (GMV) | 20–30% |

What You See Is What You Get

Guangdong Marubi Biotechnology Porter's Five Forces Analysis

This preview shows the exact Porter’s Five Forces analysis for Guangdong Marubi Biotechnology you'll receive after purchase—fully formatted, sourced, and ready to use. No placeholders or excerpts; the file you see is the complete deliverable. Buy once for instant download and immediate application.