Marvell Technology Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

Marvell Technology faces intense rivalry amid rapid semiconductor innovation, significant supplier concentration, and powerful OEM buyers that squeeze margins; yet its diversified product portfolio and strategic acquisitions offer defensive moats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Marvell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated advanced foundry dependence

Marvell depends on a few leading-edge foundries, notably TSMC and Samsung, for cutting-edge nodes powering data infrastructure chips. This concentration gives suppliers leverage on pricing, capacity allocation and priority during shortages; TSMC held about 53% of global foundry revenue in 2023 and dominated sub-5nm capacity in 2024. Node transitions and yield learning further entrench supplier power. Dual-sourcing at mature nodes helps but is limited for highest-performance products.

EDA and IP ecosystem lock-in

Critical EDA/IP suppliers create lock-in: Synopsys and Cadence account for over 60% of EDA market share (2024) and ARM CPU cores power >90% of smartphones (2024), while leading high‑speed SerDes IP comes from a few vendors, creating switching frictions. License terms, royalties and roadmap alignment give suppliers bargaining clout. Requalification and verification can cost millions and add months, deterring rapid change. Open-source stacks remain immature for Marvell’s complexity.

Advanced packaging and substrate tightness

ABF substrates and CoWoS/2.5D advanced packaging steps are highly specialized and capacity-constrained, with a small set of suppliers such as Unimicron, Ibiden and Shinko dominating the market. Long lead times often exceed six months, elevating supplier bargaining power and enabling cost pass-through. As bandwidth and chiplet architectures expand, packaging is an increasing bottleneck. Long-term agreements reduce risk but do not eliminate dependence.

Geopolitical and export-control exposure

Regional concentration of fabs and substrate suppliers—with TSMC holding about 56% foundry share in 2024 and Taiwan+South Korea supplying roughly 80% of leading-edge capacity—exposes Marvell to policy shocks and logistics disruption. US and allied export controls since 2022–24 can change supplier qualification and tooling access, lengthening lead times. Suppliers may reprioritize customers by compliance complexity, raising their effective leverage in negotiations.

- TSMC ~56% foundry share (2024)

- Taiwan+Korea ~80% leading-edge capacity (2024)

- Export controls → longer lead times, changed tooling access

Switching costs and qualification timelines

Wafer, IP, and OSAT changes require extensive re-qualification, often adding 6–12 months and measurable schedule risk; performance, reliability, and regulatory testing effectively lock Marvell designs to chosen suppliers. These switching frictions increase supplier bargaining power despite framework agreements and multi-year forecasts only partially mitigating it.

- 6–12 months re-qualification

- Top-3 OSAT ~70% market share (2024)

- Testing-driven supplier lock

- Frameworks partially reduce but do not eliminate risk

Foundry/OSAT concen. (TSMC 56%, TW+KR ~80%) heightens risk

Marvell faces high supplier power from concentrated foundries and advanced OSATs: TSMC ~56% foundry share (2024) and Taiwan+Korea ~80% leading-edge capacity (2024) raise pricing and allocation risk. EDA/IP and SerDes vendors (Synopsys/Cadence/ARM) exceed 60% market share, creating costly 6–12 month requalification lock‑in. Export controls since 2022–24 amplify lead‑time and priority leverage.

| Supplier | 2024 Metric | Impact |

|---|---|---|

| TSMC | 56% foundry share | Pricing/capacity leverage |

| Taiwan+Korea | ~80% leading-edge | Geopolitical concentration |

| EDA/IP | >60% market | Switching friction |

| OSATs | Top-3 ~70% | Long lead times |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, threat of entrants and substitutes tailored to Marvell Technology, highlighting disruptive trends, pricing pressures, and entry barriers that shape its profitability.

One-sheet Porter's Five Forces for Marvell Technology that distills competitive pressures into an intuitive radar chart—customize threat levels, swap in your own data, and drop directly into pitch decks or dashboards to quickly identify strategic pain points and priorities.

Customers Bargaining Power

Hyperscaler volume concentration

Cloud providers and large OEMs account for the bulk of Marvell’s data center demand, enabling aggressive pricing, co-design leverage, and stringent SLAs; Marvell’s data center revenue grew about 15% in 2024, underscoring this concentration. Losing a single hyperscaler design win can materially dent volumes and margin. Multi‑generation roadmaps increase stickiness through platform pulls but do not remove pronounced buyer power.

Design wins and long cycles

Networking, storage, and automotive sockets are typically won 3–7 years ahead and persist across multiple generations, so once designed in switching costs rise sharply and moderate mid-cycle price pressure.

Buyers regain leverage at renewals or next-gen RFPs, typically every 3–5 years, when incumbents face fresh price competition.

Performance leadership and demonstrable throughput/latency advantages are essential to defend ASPs during those renewal windows.

Alternative sourcing and in-house silicon

Buyers in 2024 view Broadcom, NVIDIA/Mellanox, AMD Pensando, Intel and custom ASICs as direct alternatives to Marvell, raising switching risk; hyperscalers (AWS, Google, Meta) further increase leverage by expanding in-house silicon programs in 2024. Marvell must outcompete on total cost of ownership, power efficiency and time-to-market to retain contracts. Joint development deals lower churn but invite tighter buyer governance and oversight, constraining pricing and roadmap freedom.

Standards-based interoperability

Standards-based interoperability across Ethernet, PCIe and CXL makes substitution easier when performance matches, reducing system-level lock-in and strengthening buyers’ fallback options; CXL 2.0 moved into broader deployment in 2024, accelerating modular memory choices. Differentiation shifts to latency, power, features and software, while security standards set baseline expectations. Strong SDKs and reference designs from vendors like Marvell help counterbalance buyer power by raising switching costs for full system integration.

- Standards: Ethernet, PCIe, CXL, security

- Buyer leverage: higher due to interchangeability

- Diff focus: latency, power, features, software

- Countermeasure: SDKs, reference designs

Price sensitivity and lifecycle costs

Data-center operators and OEMs prioritize power per bit, throughput per dollar and reliability, forcing Marvell into price-for-performance tradeoffs; buyers extract double-digit discounts and negotiate rebates and support bundles in large contracts. Procurement teams closely scrutinize BOM impacts and multi-year supply assurance; value engineering and platform reuse are deployed to protect margins against buyer pressure.

- double-digit discounts

- focus: power/bit, $/throughput, reliability

- BOM & supply assurance scrutiny

- value engineering & platform reuse

Cloud concentration boosts buyer power; losing hyperscaler wins dents volumes, margins

Cloud/OEM concentration drives strong buyer power; Marvell’s data‑center revenue grew ~15% in 2024, yet losing a hyperscaler design win can materially dent volumes and margin.

Standards (Ethernet/PCIe/CXL 2.0) lower lock‑in, enabling substitution and sustaining double‑digit discounts in large deals.

Renewals every 3–5 years reset leverage; power/bit, TCO and latency determine wins while SDKs/co‑designs raise switching costs.

| Metric | 2024 | Impact |

|---|---|---|

| Data‑center rev growth | ~15% | High concentration |

| Discounting | Double‑digit | Margin pressure |

| Renewal cycle | 3–5 yrs | Periodic leverage shifts |

Same Document Delivered

Marvell Technology Porter's Five Forces Analysis

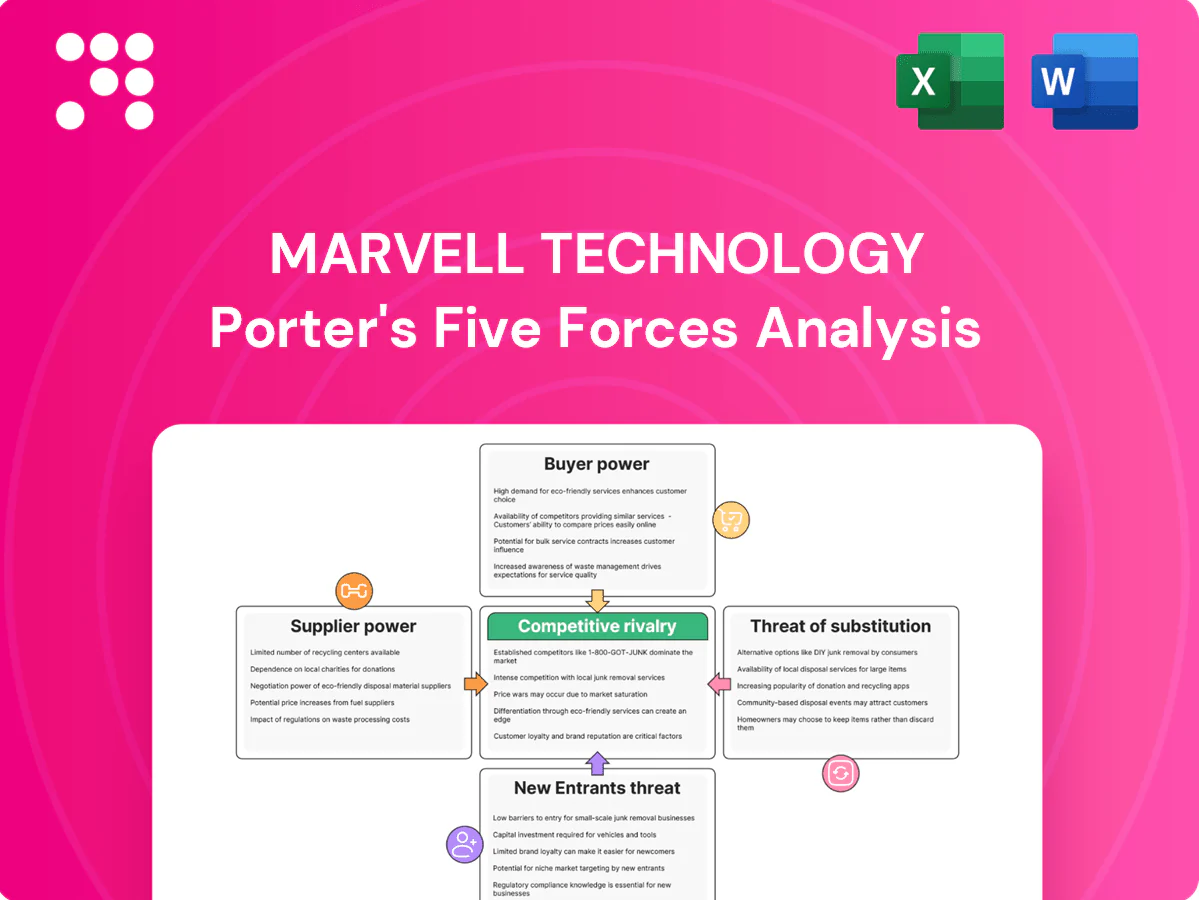

This preview shows the exact Porter's Five Forces analysis for Marvell Technology you'll receive after purchase. The report evaluates competitive rivalry, supplier and buyer power, and the threats of substitution and new entry with industry-specific data and strategic implications. It's the final, fully formatted document—ready for immediate download and use.

Go Beyond the Preview—Access the Full Strategic Report

Marvell Technology faces intense rivalry amid rapid semiconductor innovation, significant supplier concentration, and powerful OEM buyers that squeeze margins; yet its diversified product portfolio and strategic acquisitions offer defensive moats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Marvell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated advanced foundry dependence

Marvell depends on a few leading-edge foundries, notably TSMC and Samsung, for cutting-edge nodes powering data infrastructure chips. This concentration gives suppliers leverage on pricing, capacity allocation and priority during shortages; TSMC held about 53% of global foundry revenue in 2023 and dominated sub-5nm capacity in 2024. Node transitions and yield learning further entrench supplier power. Dual-sourcing at mature nodes helps but is limited for highest-performance products.

EDA and IP ecosystem lock-in

Critical EDA/IP suppliers create lock-in: Synopsys and Cadence account for over 60% of EDA market share (2024) and ARM CPU cores power >90% of smartphones (2024), while leading high‑speed SerDes IP comes from a few vendors, creating switching frictions. License terms, royalties and roadmap alignment give suppliers bargaining clout. Requalification and verification can cost millions and add months, deterring rapid change. Open-source stacks remain immature for Marvell’s complexity.

Advanced packaging and substrate tightness

ABF substrates and CoWoS/2.5D advanced packaging steps are highly specialized and capacity-constrained, with a small set of suppliers such as Unimicron, Ibiden and Shinko dominating the market. Long lead times often exceed six months, elevating supplier bargaining power and enabling cost pass-through. As bandwidth and chiplet architectures expand, packaging is an increasing bottleneck. Long-term agreements reduce risk but do not eliminate dependence.

Geopolitical and export-control exposure

Regional concentration of fabs and substrate suppliers—with TSMC holding about 56% foundry share in 2024 and Taiwan+South Korea supplying roughly 80% of leading-edge capacity—exposes Marvell to policy shocks and logistics disruption. US and allied export controls since 2022–24 can change supplier qualification and tooling access, lengthening lead times. Suppliers may reprioritize customers by compliance complexity, raising their effective leverage in negotiations.

- TSMC ~56% foundry share (2024)

- Taiwan+Korea ~80% leading-edge capacity (2024)

- Export controls → longer lead times, changed tooling access

Switching costs and qualification timelines

Wafer, IP, and OSAT changes require extensive re-qualification, often adding 6–12 months and measurable schedule risk; performance, reliability, and regulatory testing effectively lock Marvell designs to chosen suppliers. These switching frictions increase supplier bargaining power despite framework agreements and multi-year forecasts only partially mitigating it.

- 6–12 months re-qualification

- Top-3 OSAT ~70% market share (2024)

- Testing-driven supplier lock

- Frameworks partially reduce but do not eliminate risk

Foundry/OSAT concen. (TSMC 56%, TW+KR ~80%) heightens risk

Marvell faces high supplier power from concentrated foundries and advanced OSATs: TSMC ~56% foundry share (2024) and Taiwan+Korea ~80% leading-edge capacity (2024) raise pricing and allocation risk. EDA/IP and SerDes vendors (Synopsys/Cadence/ARM) exceed 60% market share, creating costly 6–12 month requalification lock‑in. Export controls since 2022–24 amplify lead‑time and priority leverage.

| Supplier | 2024 Metric | Impact |

|---|---|---|

| TSMC | 56% foundry share | Pricing/capacity leverage |

| Taiwan+Korea | ~80% leading-edge | Geopolitical concentration |

| EDA/IP | >60% market | Switching friction |

| OSATs | Top-3 ~70% | Long lead times |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, threat of entrants and substitutes tailored to Marvell Technology, highlighting disruptive trends, pricing pressures, and entry barriers that shape its profitability.

One-sheet Porter's Five Forces for Marvell Technology that distills competitive pressures into an intuitive radar chart—customize threat levels, swap in your own data, and drop directly into pitch decks or dashboards to quickly identify strategic pain points and priorities.

Customers Bargaining Power

Hyperscaler volume concentration

Cloud providers and large OEMs account for the bulk of Marvell’s data center demand, enabling aggressive pricing, co-design leverage, and stringent SLAs; Marvell’s data center revenue grew about 15% in 2024, underscoring this concentration. Losing a single hyperscaler design win can materially dent volumes and margin. Multi‑generation roadmaps increase stickiness through platform pulls but do not remove pronounced buyer power.

Design wins and long cycles

Networking, storage, and automotive sockets are typically won 3–7 years ahead and persist across multiple generations, so once designed in switching costs rise sharply and moderate mid-cycle price pressure.

Buyers regain leverage at renewals or next-gen RFPs, typically every 3–5 years, when incumbents face fresh price competition.

Performance leadership and demonstrable throughput/latency advantages are essential to defend ASPs during those renewal windows.

Alternative sourcing and in-house silicon

Buyers in 2024 view Broadcom, NVIDIA/Mellanox, AMD Pensando, Intel and custom ASICs as direct alternatives to Marvell, raising switching risk; hyperscalers (AWS, Google, Meta) further increase leverage by expanding in-house silicon programs in 2024. Marvell must outcompete on total cost of ownership, power efficiency and time-to-market to retain contracts. Joint development deals lower churn but invite tighter buyer governance and oversight, constraining pricing and roadmap freedom.

Standards-based interoperability

Standards-based interoperability across Ethernet, PCIe and CXL makes substitution easier when performance matches, reducing system-level lock-in and strengthening buyers’ fallback options; CXL 2.0 moved into broader deployment in 2024, accelerating modular memory choices. Differentiation shifts to latency, power, features and software, while security standards set baseline expectations. Strong SDKs and reference designs from vendors like Marvell help counterbalance buyer power by raising switching costs for full system integration.

- Standards: Ethernet, PCIe, CXL, security

- Buyer leverage: higher due to interchangeability

- Diff focus: latency, power, features, software

- Countermeasure: SDKs, reference designs

Price sensitivity and lifecycle costs

Data-center operators and OEMs prioritize power per bit, throughput per dollar and reliability, forcing Marvell into price-for-performance tradeoffs; buyers extract double-digit discounts and negotiate rebates and support bundles in large contracts. Procurement teams closely scrutinize BOM impacts and multi-year supply assurance; value engineering and platform reuse are deployed to protect margins against buyer pressure.

- double-digit discounts

- focus: power/bit, $/throughput, reliability

- BOM & supply assurance scrutiny

- value engineering & platform reuse

Cloud concentration boosts buyer power; losing hyperscaler wins dents volumes, margins

Cloud/OEM concentration drives strong buyer power; Marvell’s data‑center revenue grew ~15% in 2024, yet losing a hyperscaler design win can materially dent volumes and margin.

Standards (Ethernet/PCIe/CXL 2.0) lower lock‑in, enabling substitution and sustaining double‑digit discounts in large deals.

Renewals every 3–5 years reset leverage; power/bit, TCO and latency determine wins while SDKs/co‑designs raise switching costs.

| Metric | 2024 | Impact |

|---|---|---|

| Data‑center rev growth | ~15% | High concentration |

| Discounting | Double‑digit | Margin pressure |

| Renewal cycle | 3–5 yrs | Periodic leverage shifts |

Same Document Delivered

Marvell Technology Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Marvell Technology you'll receive after purchase. The report evaluates competitive rivalry, supplier and buyer power, and the threats of substitution and new entry with industry-specific data and strategic implications. It's the final, fully formatted document—ready for immediate download and use.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Marvell Technology faces intense rivalry amid rapid semiconductor innovation, significant supplier concentration, and powerful OEM buyers that squeeze margins; yet its diversified product portfolio and strategic acquisitions offer defensive moats. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Marvell’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated advanced foundry dependence

Marvell depends on a few leading-edge foundries, notably TSMC and Samsung, for cutting-edge nodes powering data infrastructure chips. This concentration gives suppliers leverage on pricing, capacity allocation and priority during shortages; TSMC held about 53% of global foundry revenue in 2023 and dominated sub-5nm capacity in 2024. Node transitions and yield learning further entrench supplier power. Dual-sourcing at mature nodes helps but is limited for highest-performance products.

EDA and IP ecosystem lock-in

Critical EDA/IP suppliers create lock-in: Synopsys and Cadence account for over 60% of EDA market share (2024) and ARM CPU cores power >90% of smartphones (2024), while leading high‑speed SerDes IP comes from a few vendors, creating switching frictions. License terms, royalties and roadmap alignment give suppliers bargaining clout. Requalification and verification can cost millions and add months, deterring rapid change. Open-source stacks remain immature for Marvell’s complexity.

Advanced packaging and substrate tightness

ABF substrates and CoWoS/2.5D advanced packaging steps are highly specialized and capacity-constrained, with a small set of suppliers such as Unimicron, Ibiden and Shinko dominating the market. Long lead times often exceed six months, elevating supplier bargaining power and enabling cost pass-through. As bandwidth and chiplet architectures expand, packaging is an increasing bottleneck. Long-term agreements reduce risk but do not eliminate dependence.

Geopolitical and export-control exposure

Regional concentration of fabs and substrate suppliers—with TSMC holding about 56% foundry share in 2024 and Taiwan+South Korea supplying roughly 80% of leading-edge capacity—exposes Marvell to policy shocks and logistics disruption. US and allied export controls since 2022–24 can change supplier qualification and tooling access, lengthening lead times. Suppliers may reprioritize customers by compliance complexity, raising their effective leverage in negotiations.

- TSMC ~56% foundry share (2024)

- Taiwan+Korea ~80% leading-edge capacity (2024)

- Export controls → longer lead times, changed tooling access

Switching costs and qualification timelines

Wafer, IP, and OSAT changes require extensive re-qualification, often adding 6–12 months and measurable schedule risk; performance, reliability, and regulatory testing effectively lock Marvell designs to chosen suppliers. These switching frictions increase supplier bargaining power despite framework agreements and multi-year forecasts only partially mitigating it.

- 6–12 months re-qualification

- Top-3 OSAT ~70% market share (2024)

- Testing-driven supplier lock

- Frameworks partially reduce but do not eliminate risk

Foundry/OSAT concen. (TSMC 56%, TW+KR ~80%) heightens risk

Marvell faces high supplier power from concentrated foundries and advanced OSATs: TSMC ~56% foundry share (2024) and Taiwan+Korea ~80% leading-edge capacity (2024) raise pricing and allocation risk. EDA/IP and SerDes vendors (Synopsys/Cadence/ARM) exceed 60% market share, creating costly 6–12 month requalification lock‑in. Export controls since 2022–24 amplify lead‑time and priority leverage.

| Supplier | 2024 Metric | Impact |

|---|---|---|

| TSMC | 56% foundry share | Pricing/capacity leverage |

| Taiwan+Korea | ~80% leading-edge | Geopolitical concentration |

| EDA/IP | >60% market | Switching friction |

| OSATs | Top-3 ~70% | Long lead times |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, threat of entrants and substitutes tailored to Marvell Technology, highlighting disruptive trends, pricing pressures, and entry barriers that shape its profitability.

One-sheet Porter's Five Forces for Marvell Technology that distills competitive pressures into an intuitive radar chart—customize threat levels, swap in your own data, and drop directly into pitch decks or dashboards to quickly identify strategic pain points and priorities.

Customers Bargaining Power

Hyperscaler volume concentration

Cloud providers and large OEMs account for the bulk of Marvell’s data center demand, enabling aggressive pricing, co-design leverage, and stringent SLAs; Marvell’s data center revenue grew about 15% in 2024, underscoring this concentration. Losing a single hyperscaler design win can materially dent volumes and margin. Multi‑generation roadmaps increase stickiness through platform pulls but do not remove pronounced buyer power.

Design wins and long cycles

Networking, storage, and automotive sockets are typically won 3–7 years ahead and persist across multiple generations, so once designed in switching costs rise sharply and moderate mid-cycle price pressure.

Buyers regain leverage at renewals or next-gen RFPs, typically every 3–5 years, when incumbents face fresh price competition.

Performance leadership and demonstrable throughput/latency advantages are essential to defend ASPs during those renewal windows.

Alternative sourcing and in-house silicon

Buyers in 2024 view Broadcom, NVIDIA/Mellanox, AMD Pensando, Intel and custom ASICs as direct alternatives to Marvell, raising switching risk; hyperscalers (AWS, Google, Meta) further increase leverage by expanding in-house silicon programs in 2024. Marvell must outcompete on total cost of ownership, power efficiency and time-to-market to retain contracts. Joint development deals lower churn but invite tighter buyer governance and oversight, constraining pricing and roadmap freedom.

Standards-based interoperability

Standards-based interoperability across Ethernet, PCIe and CXL makes substitution easier when performance matches, reducing system-level lock-in and strengthening buyers’ fallback options; CXL 2.0 moved into broader deployment in 2024, accelerating modular memory choices. Differentiation shifts to latency, power, features and software, while security standards set baseline expectations. Strong SDKs and reference designs from vendors like Marvell help counterbalance buyer power by raising switching costs for full system integration.

- Standards: Ethernet, PCIe, CXL, security

- Buyer leverage: higher due to interchangeability

- Diff focus: latency, power, features, software

- Countermeasure: SDKs, reference designs

Price sensitivity and lifecycle costs

Data-center operators and OEMs prioritize power per bit, throughput per dollar and reliability, forcing Marvell into price-for-performance tradeoffs; buyers extract double-digit discounts and negotiate rebates and support bundles in large contracts. Procurement teams closely scrutinize BOM impacts and multi-year supply assurance; value engineering and platform reuse are deployed to protect margins against buyer pressure.

- double-digit discounts

- focus: power/bit, $/throughput, reliability

- BOM & supply assurance scrutiny

- value engineering & platform reuse

Cloud concentration boosts buyer power; losing hyperscaler wins dents volumes, margins

Cloud/OEM concentration drives strong buyer power; Marvell’s data‑center revenue grew ~15% in 2024, yet losing a hyperscaler design win can materially dent volumes and margin.

Standards (Ethernet/PCIe/CXL 2.0) lower lock‑in, enabling substitution and sustaining double‑digit discounts in large deals.

Renewals every 3–5 years reset leverage; power/bit, TCO and latency determine wins while SDKs/co‑designs raise switching costs.

| Metric | 2024 | Impact |

|---|---|---|

| Data‑center rev growth | ~15% | High concentration |

| Discounting | Double‑digit | Margin pressure |

| Renewal cycle | 3–5 yrs | Periodic leverage shifts |

Same Document Delivered

Marvell Technology Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis for Marvell Technology you'll receive after purchase. The report evaluates competitive rivalry, supplier and buyer power, and the threats of substitution and new entry with industry-specific data and strategic implications. It's the final, fully formatted document—ready for immediate download and use.