Masimo Porter's Five Forces Analysis

From Overview to Strategy Blueprint

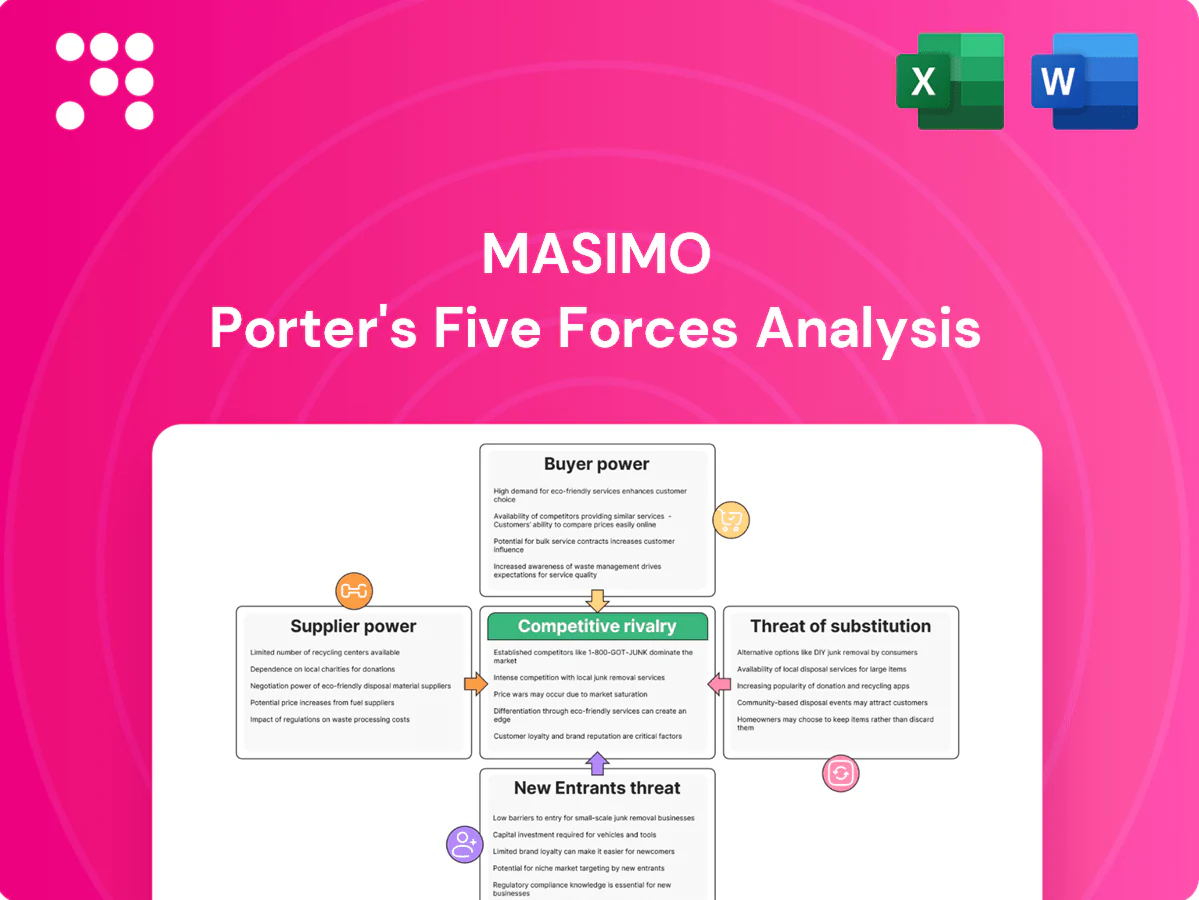

Masimo faces intense competitive rivalry from established medtech firms, moderate supplier power, and growing buyer sophistication as hospitals push for cost-effective monitoring; regulatory hurdles and emerging wearable substitutes add strategic complexity. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Masimo’s competitive dynamics in detail.

Suppliers Bargaining Power

Supplier Power 1

Masimo depends on specialized LEDs, photodiodes, MEMS and medical-grade adhesives with a relatively limited supplier pool, increasing supplier leverage; as of 2024 Masimo’s trailing twelve-month revenue was about $1.5 billion, amplifying the impact of supply disruptions. Dual-sourcing and qualification programs reduce single-vendor risk but raise procurement and validation costs. Any supplier quality lapse can halt FDA-compliant production and trigger costly recalls and revenue loss.

Supplier Power 2

Regulatory and quality requirements under FDA and EU MDR raise switching costs for Masimo, as revalidation, audits and documentation typically add 3–9 months and tens to hundreds of thousands USD in expense, empowering compliant vendors in negotiations; long-term supply agreements further dampen price volatility, often stabilizing input costs and margins by reducing short-term price swings for critical components.

Supplier Power 3

Upstream inputs such as semiconductors and optoelectronics remain cyclical, with advanced-node capacity concentrated among a few foundries (major vendors account for the majority of capacity), driving lead times often into double-digit weeks and periodic price spikes. Tight capacity in 2024 elevated component costs and vendor leverage. Strategic inventory buffers and improved demand forecasting mitigate risk but cannot fully offset supply shocks. Supply continuity therefore stays a persistent management focus.

Supplier Power 4

Masimo’s proprietary algorithms and sensor designs reduce commoditization of inputs and supported over 1,500 patents as of 2024, raising switching costs for suppliers. Custom specifications limit supplier alternatives while embedding supplier know-how into final products, creating performance differentiation but increasing vendor dependence. Long-term co-development agreements further increase mutual lock-in and bargaining asymmetry.

- Proprietary IP: high

- Supplier alternatives: limited

- Vendor dependence: elevated

Supplier Power 5

Supplier Power 5: Contract manufacturers deliver scale and cost advantages but volume concentration increases their leverage; geographic diversification mitigates geopolitical and supply-chain risk; transfer of tooling and processes is non-trivial, creating supplier stickiness; renewals hinge on price, yield, and regulatory compliance metrics.

- Scale vs leverage: contract manufacturing concentration

- Geographic diversification: reduces geopolitical exposure

- Tooling stickiness: high switching costs

- KPIs: price, yield, compliance govern renewals

Supplier concentration and proprietary sensors threaten $1.5B revenue

Masimo faces elevated supplier power due to limited optoelectronics/MEMS vendors, proprietary sensor specs (1,500+ patents in 2024) and concentrated contract manufacturing; 2024 trailing twelve-month revenue ≈ $1.5B magnifies disruption impact. Revalidation typically 3–9 months; lead times often 10–16 weeks. Dual-sourcing reduces but raises costs.

| Metric | 2024 |

|---|---|

| Revenue (TTM) | $1.5B |

| Patents | 1,500+ |

| Lead time | 10–16 weeks |

| Revalidation | 3–9 months |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and entry risks tailored to Masimo’s medical-device and monitoring market. Identifies disruptive technologies, substitutes, and strategic barriers that shape pricing, profitability, and Masimo’s competitive positioning.

Clean, one-sheet Porter's Five Forces for Masimo—instantly visualizes competitive pressure and supplier/buyer dynamics for rapid decision-making and investor briefings.

Customers Bargaining Power

Buyer Power 1

Primary buyers for Masimo are hospitals, IDNs and GPOs that negotiate aggressively; GPOs represent purchasing for over 95% of U.S. hospitals (Healthcare Supply Chain Association, 2024), aggregating demand and pressuring pricing. Competitive tender processes pit vendors head-to-head on specifications and total cost, while multi-year contracts hinge on robust clinical and economic evidence to secure adoption.

Buyer Power 2

Masimo integration with EMR/IT and staff workflows raises switching costs as over 95% of US hospitals use certified EHRs (ONC 2023), making replacement costly and complex. Training, clinical validation and interoperability testing—switching costs often exceed $1M and take months—reduce willingness to change suppliers. Downtime and retraining risks deter churn despite price gaps, while deeper connectivity and automation further entrench vendor lock-in.

Buyer Power 3

Clinically differentiated accuracy in low perfusion or motion allows Masimo to command ASP premiums typically in the 10–20% range, as buyers prioritize outcomes and alarm reliability over price.

When alarm reliability affects patient safety, purchasers accept higher ASPs; hospitals model ROI using length-of-stay savings averaging $2,500–$4,000 per bed-day and reduced adverse-event costs.

Robust peer-reviewed validation (dozens of clinical studies by 2024) weakens price-only negotiations, shifting procurement toward value-based purchasing and total-cost-of-care analyses.

Buyer Power 4

Consumable sensors create recurring spend and vendor dependence, and in 2024 standardization committees intensified efforts to push cross-compatibility to curb costs. Proprietary interfaces continue to limit substitution at the sensor level, while large purchasers frequently demand volume rebates and service-level guarantees to manage total cost of ownership.

- Recurring sensors drive lock-in

- 2024 standardization pressures favor cross-compatibility

- Proprietary interfaces reduce substitution

- Buyers seek volume rebates and SLAs

Buyer Power 5

Buyer Power 5: emerging home and ambulatory monitoring buyers in 2024 are markedly more price-sensitive as reimbursement scrutiny intensifies and payers push aggressive cost containment, forcing vendors to defend margins with robust evidence dossiers and health-economic models.

- 2024: payers tightening reimbursement

- International tenders prioritize lowest compliant bid

- Evidence dossiers/HEOR essential to preserve pricing

GPO power and >$1M switching costs enable 10-20% ASP premiums despite tightening reimbursement

Hospitals/IDNs/GPOs (>95% of US hospitals via GPOs, 2024) exert strong price pressure, using tenders and volume rebates. High switching costs (often >$1M, months) plus integration and consumable sensors sustain lock-in, supporting 10–20% ASP premiums for clinical accuracy. Payer reimbursement tightening in 2024 and home-monitoring price sensitivity constrain pricing despite HEOR evidence.

| Metric | Value | Source |

|---|---|---|

| GPO coverage | >95% | HSCA 2024 |

| Switching cost | >$1M | Market studies 2024 |

| ASP premium | 10–20% | Commercial data 2024 |

| LOS savings | $2,500–$4,000 | Hospital ROI models 2024 |

Full Version Awaits

Masimo Porter's Five Forces Analysis

This preview shows the exact Masimo Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're previewing the final deliverable; once your purchase is complete you'll have instant access to this same file.

From Overview to Strategy Blueprint

Masimo faces intense competitive rivalry from established medtech firms, moderate supplier power, and growing buyer sophistication as hospitals push for cost-effective monitoring; regulatory hurdles and emerging wearable substitutes add strategic complexity. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Masimo’s competitive dynamics in detail.

Suppliers Bargaining Power

Supplier Power 1

Masimo depends on specialized LEDs, photodiodes, MEMS and medical-grade adhesives with a relatively limited supplier pool, increasing supplier leverage; as of 2024 Masimo’s trailing twelve-month revenue was about $1.5 billion, amplifying the impact of supply disruptions. Dual-sourcing and qualification programs reduce single-vendor risk but raise procurement and validation costs. Any supplier quality lapse can halt FDA-compliant production and trigger costly recalls and revenue loss.

Supplier Power 2

Regulatory and quality requirements under FDA and EU MDR raise switching costs for Masimo, as revalidation, audits and documentation typically add 3–9 months and tens to hundreds of thousands USD in expense, empowering compliant vendors in negotiations; long-term supply agreements further dampen price volatility, often stabilizing input costs and margins by reducing short-term price swings for critical components.

Supplier Power 3

Upstream inputs such as semiconductors and optoelectronics remain cyclical, with advanced-node capacity concentrated among a few foundries (major vendors account for the majority of capacity), driving lead times often into double-digit weeks and periodic price spikes. Tight capacity in 2024 elevated component costs and vendor leverage. Strategic inventory buffers and improved demand forecasting mitigate risk but cannot fully offset supply shocks. Supply continuity therefore stays a persistent management focus.

Supplier Power 4

Masimo’s proprietary algorithms and sensor designs reduce commoditization of inputs and supported over 1,500 patents as of 2024, raising switching costs for suppliers. Custom specifications limit supplier alternatives while embedding supplier know-how into final products, creating performance differentiation but increasing vendor dependence. Long-term co-development agreements further increase mutual lock-in and bargaining asymmetry.

- Proprietary IP: high

- Supplier alternatives: limited

- Vendor dependence: elevated

Supplier Power 5

Supplier Power 5: Contract manufacturers deliver scale and cost advantages but volume concentration increases their leverage; geographic diversification mitigates geopolitical and supply-chain risk; transfer of tooling and processes is non-trivial, creating supplier stickiness; renewals hinge on price, yield, and regulatory compliance metrics.

- Scale vs leverage: contract manufacturing concentration

- Geographic diversification: reduces geopolitical exposure

- Tooling stickiness: high switching costs

- KPIs: price, yield, compliance govern renewals

Supplier concentration and proprietary sensors threaten $1.5B revenue

Masimo faces elevated supplier power due to limited optoelectronics/MEMS vendors, proprietary sensor specs (1,500+ patents in 2024) and concentrated contract manufacturing; 2024 trailing twelve-month revenue ≈ $1.5B magnifies disruption impact. Revalidation typically 3–9 months; lead times often 10–16 weeks. Dual-sourcing reduces but raises costs.

| Metric | 2024 |

|---|---|

| Revenue (TTM) | $1.5B |

| Patents | 1,500+ |

| Lead time | 10–16 weeks |

| Revalidation | 3–9 months |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and entry risks tailored to Masimo’s medical-device and monitoring market. Identifies disruptive technologies, substitutes, and strategic barriers that shape pricing, profitability, and Masimo’s competitive positioning.

Clean, one-sheet Porter's Five Forces for Masimo—instantly visualizes competitive pressure and supplier/buyer dynamics for rapid decision-making and investor briefings.

Customers Bargaining Power

Buyer Power 1

Primary buyers for Masimo are hospitals, IDNs and GPOs that negotiate aggressively; GPOs represent purchasing for over 95% of U.S. hospitals (Healthcare Supply Chain Association, 2024), aggregating demand and pressuring pricing. Competitive tender processes pit vendors head-to-head on specifications and total cost, while multi-year contracts hinge on robust clinical and economic evidence to secure adoption.

Buyer Power 2

Masimo integration with EMR/IT and staff workflows raises switching costs as over 95% of US hospitals use certified EHRs (ONC 2023), making replacement costly and complex. Training, clinical validation and interoperability testing—switching costs often exceed $1M and take months—reduce willingness to change suppliers. Downtime and retraining risks deter churn despite price gaps, while deeper connectivity and automation further entrench vendor lock-in.

Buyer Power 3

Clinically differentiated accuracy in low perfusion or motion allows Masimo to command ASP premiums typically in the 10–20% range, as buyers prioritize outcomes and alarm reliability over price.

When alarm reliability affects patient safety, purchasers accept higher ASPs; hospitals model ROI using length-of-stay savings averaging $2,500–$4,000 per bed-day and reduced adverse-event costs.

Robust peer-reviewed validation (dozens of clinical studies by 2024) weakens price-only negotiations, shifting procurement toward value-based purchasing and total-cost-of-care analyses.

Buyer Power 4

Consumable sensors create recurring spend and vendor dependence, and in 2024 standardization committees intensified efforts to push cross-compatibility to curb costs. Proprietary interfaces continue to limit substitution at the sensor level, while large purchasers frequently demand volume rebates and service-level guarantees to manage total cost of ownership.

- Recurring sensors drive lock-in

- 2024 standardization pressures favor cross-compatibility

- Proprietary interfaces reduce substitution

- Buyers seek volume rebates and SLAs

Buyer Power 5

Buyer Power 5: emerging home and ambulatory monitoring buyers in 2024 are markedly more price-sensitive as reimbursement scrutiny intensifies and payers push aggressive cost containment, forcing vendors to defend margins with robust evidence dossiers and health-economic models.

- 2024: payers tightening reimbursement

- International tenders prioritize lowest compliant bid

- Evidence dossiers/HEOR essential to preserve pricing

GPO power and >$1M switching costs enable 10-20% ASP premiums despite tightening reimbursement

Hospitals/IDNs/GPOs (>95% of US hospitals via GPOs, 2024) exert strong price pressure, using tenders and volume rebates. High switching costs (often >$1M, months) plus integration and consumable sensors sustain lock-in, supporting 10–20% ASP premiums for clinical accuracy. Payer reimbursement tightening in 2024 and home-monitoring price sensitivity constrain pricing despite HEOR evidence.

| Metric | Value | Source |

|---|---|---|

| GPO coverage | >95% | HSCA 2024 |

| Switching cost | >$1M | Market studies 2024 |

| ASP premium | 10–20% | Commercial data 2024 |

| LOS savings | $2,500–$4,000 | Hospital ROI models 2024 |

Full Version Awaits

Masimo Porter's Five Forces Analysis

This preview shows the exact Masimo Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're previewing the final deliverable; once your purchase is complete you'll have instant access to this same file.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Masimo faces intense competitive rivalry from established medtech firms, moderate supplier power, and growing buyer sophistication as hospitals push for cost-effective monitoring; regulatory hurdles and emerging wearable substitutes add strategic complexity. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Masimo’s competitive dynamics in detail.

Suppliers Bargaining Power

Supplier Power 1

Masimo depends on specialized LEDs, photodiodes, MEMS and medical-grade adhesives with a relatively limited supplier pool, increasing supplier leverage; as of 2024 Masimo’s trailing twelve-month revenue was about $1.5 billion, amplifying the impact of supply disruptions. Dual-sourcing and qualification programs reduce single-vendor risk but raise procurement and validation costs. Any supplier quality lapse can halt FDA-compliant production and trigger costly recalls and revenue loss.

Supplier Power 2

Regulatory and quality requirements under FDA and EU MDR raise switching costs for Masimo, as revalidation, audits and documentation typically add 3–9 months and tens to hundreds of thousands USD in expense, empowering compliant vendors in negotiations; long-term supply agreements further dampen price volatility, often stabilizing input costs and margins by reducing short-term price swings for critical components.

Supplier Power 3

Upstream inputs such as semiconductors and optoelectronics remain cyclical, with advanced-node capacity concentrated among a few foundries (major vendors account for the majority of capacity), driving lead times often into double-digit weeks and periodic price spikes. Tight capacity in 2024 elevated component costs and vendor leverage. Strategic inventory buffers and improved demand forecasting mitigate risk but cannot fully offset supply shocks. Supply continuity therefore stays a persistent management focus.

Supplier Power 4

Masimo’s proprietary algorithms and sensor designs reduce commoditization of inputs and supported over 1,500 patents as of 2024, raising switching costs for suppliers. Custom specifications limit supplier alternatives while embedding supplier know-how into final products, creating performance differentiation but increasing vendor dependence. Long-term co-development agreements further increase mutual lock-in and bargaining asymmetry.

- Proprietary IP: high

- Supplier alternatives: limited

- Vendor dependence: elevated

Supplier Power 5

Supplier Power 5: Contract manufacturers deliver scale and cost advantages but volume concentration increases their leverage; geographic diversification mitigates geopolitical and supply-chain risk; transfer of tooling and processes is non-trivial, creating supplier stickiness; renewals hinge on price, yield, and regulatory compliance metrics.

- Scale vs leverage: contract manufacturing concentration

- Geographic diversification: reduces geopolitical exposure

- Tooling stickiness: high switching costs

- KPIs: price, yield, compliance govern renewals

Supplier concentration and proprietary sensors threaten $1.5B revenue

Masimo faces elevated supplier power due to limited optoelectronics/MEMS vendors, proprietary sensor specs (1,500+ patents in 2024) and concentrated contract manufacturing; 2024 trailing twelve-month revenue ≈ $1.5B magnifies disruption impact. Revalidation typically 3–9 months; lead times often 10–16 weeks. Dual-sourcing reduces but raises costs.

| Metric | 2024 |

|---|---|

| Revenue (TTM) | $1.5B |

| Patents | 1,500+ |

| Lead time | 10–16 weeks |

| Revalidation | 3–9 months |

What is included in the product

Uncovers key drivers of competition, customer influence, supplier power, and entry risks tailored to Masimo’s medical-device and monitoring market. Identifies disruptive technologies, substitutes, and strategic barriers that shape pricing, profitability, and Masimo’s competitive positioning.

Clean, one-sheet Porter's Five Forces for Masimo—instantly visualizes competitive pressure and supplier/buyer dynamics for rapid decision-making and investor briefings.

Customers Bargaining Power

Buyer Power 1

Primary buyers for Masimo are hospitals, IDNs and GPOs that negotiate aggressively; GPOs represent purchasing for over 95% of U.S. hospitals (Healthcare Supply Chain Association, 2024), aggregating demand and pressuring pricing. Competitive tender processes pit vendors head-to-head on specifications and total cost, while multi-year contracts hinge on robust clinical and economic evidence to secure adoption.

Buyer Power 2

Masimo integration with EMR/IT and staff workflows raises switching costs as over 95% of US hospitals use certified EHRs (ONC 2023), making replacement costly and complex. Training, clinical validation and interoperability testing—switching costs often exceed $1M and take months—reduce willingness to change suppliers. Downtime and retraining risks deter churn despite price gaps, while deeper connectivity and automation further entrench vendor lock-in.

Buyer Power 3

Clinically differentiated accuracy in low perfusion or motion allows Masimo to command ASP premiums typically in the 10–20% range, as buyers prioritize outcomes and alarm reliability over price.

When alarm reliability affects patient safety, purchasers accept higher ASPs; hospitals model ROI using length-of-stay savings averaging $2,500–$4,000 per bed-day and reduced adverse-event costs.

Robust peer-reviewed validation (dozens of clinical studies by 2024) weakens price-only negotiations, shifting procurement toward value-based purchasing and total-cost-of-care analyses.

Buyer Power 4

Consumable sensors create recurring spend and vendor dependence, and in 2024 standardization committees intensified efforts to push cross-compatibility to curb costs. Proprietary interfaces continue to limit substitution at the sensor level, while large purchasers frequently demand volume rebates and service-level guarantees to manage total cost of ownership.

- Recurring sensors drive lock-in

- 2024 standardization pressures favor cross-compatibility

- Proprietary interfaces reduce substitution

- Buyers seek volume rebates and SLAs

Buyer Power 5

Buyer Power 5: emerging home and ambulatory monitoring buyers in 2024 are markedly more price-sensitive as reimbursement scrutiny intensifies and payers push aggressive cost containment, forcing vendors to defend margins with robust evidence dossiers and health-economic models.

- 2024: payers tightening reimbursement

- International tenders prioritize lowest compliant bid

- Evidence dossiers/HEOR essential to preserve pricing

GPO power and >$1M switching costs enable 10-20% ASP premiums despite tightening reimbursement

Hospitals/IDNs/GPOs (>95% of US hospitals via GPOs, 2024) exert strong price pressure, using tenders and volume rebates. High switching costs (often >$1M, months) plus integration and consumable sensors sustain lock-in, supporting 10–20% ASP premiums for clinical accuracy. Payer reimbursement tightening in 2024 and home-monitoring price sensitivity constrain pricing despite HEOR evidence.

| Metric | Value | Source |

|---|---|---|

| GPO coverage | >95% | HSCA 2024 |

| Switching cost | >$1M | Market studies 2024 |

| ASP premium | 10–20% | Commercial data 2024 |

| LOS savings | $2,500–$4,000 | Hospital ROI models 2024 |

Full Version Awaits

Masimo Porter's Five Forces Analysis

This preview shows the exact Masimo Porter's Five Forces analysis you'll receive immediately after purchase—no surprises, no placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're previewing the final deliverable; once your purchase is complete you'll have instant access to this same file.