Masimo SWOT Analysis

Go Beyond the Preview—Access the Full Strategic Report

Masimo's blend of medical-device innovation, recurring revenue, and regulatory footholds creates clear strengths, while supply-chain pressures, patent disputes, and competitive incumbents pose material risks. Growth hinges on telehealth and wearable expansion. Want deeper, actionable insights? Purchase the full SWOT for a downloadable Word and Excel analysis.

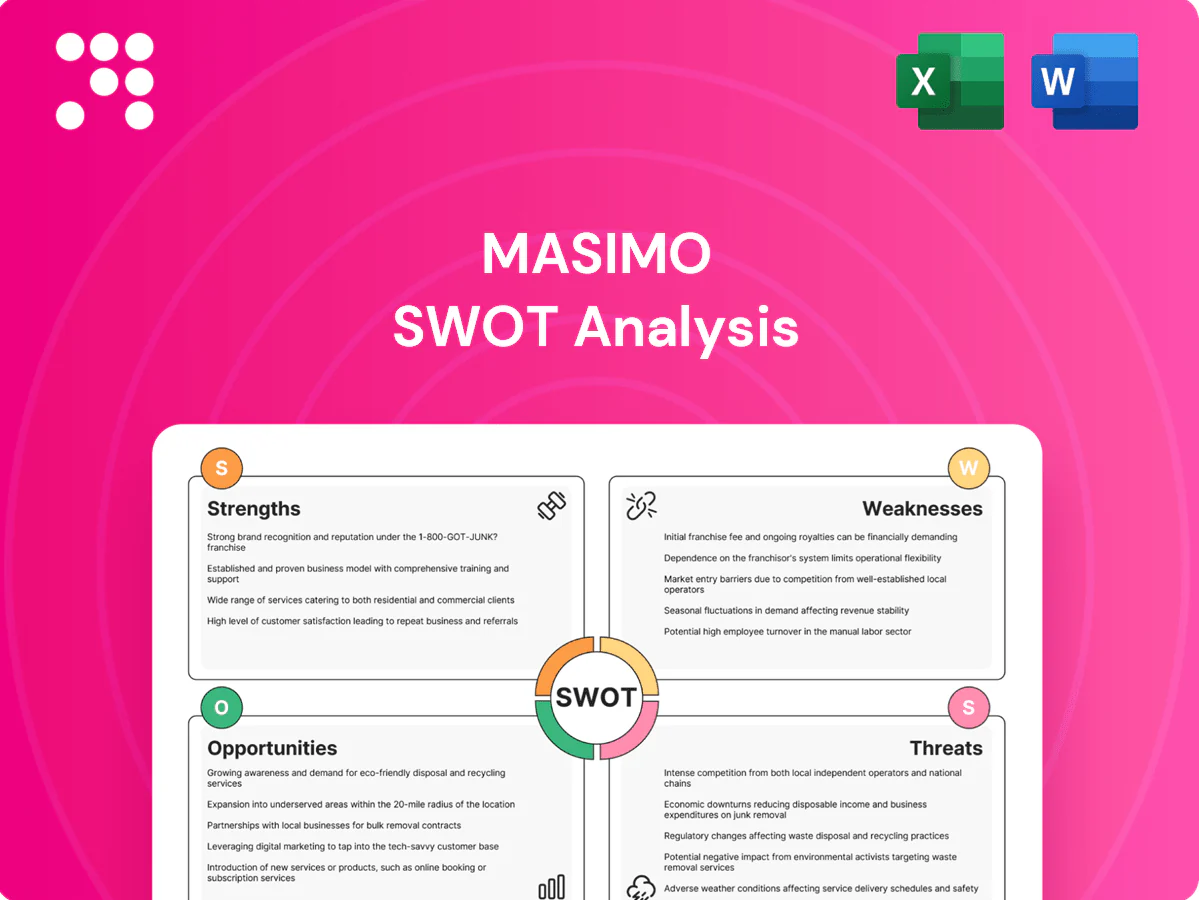

Strengths

Clinically proven monitoring accuracy

Masimo’s pulse oximetry and capnography are FDA-cleared and backed by multiple clinical trials reporting SpO2 accuracy with root-mean-square error ≤3% under motion and low perfusion, supporting clinician trust and procurement decisions. Robust validation correlates with fewer missed desaturations and contributes to value-based care by lowering adverse events and potential length-of-stay. This clinical performance differentiates Masimo from commoditized sensors and strengthens purchase justification.

Broad noninvasive monitoring portfolio

Masimo’s broad noninvasive portfolio spans SpO2, CO2, brain function and advanced parameters, covering OR, ICU and wards and deployed in 100+ countries; this breadth enables bundled hospital deals and clinical standardization, mitigates single-product risk by diversifying revenue streams across departments, and supports scalable use cases from spot-checks to continuous monitoring.

Integration and connectivity ecosystem

Masimo’s automation and connectivity solutions integrate with hospital IT, EHRs, and alarm-management workflows, supporting enterprise visibility, compliance, and analytics. Interoperability increases customer stickiness and switching costs, helping software and services contribute to recurring revenue. Masimo reported fiscal 2024 revenue of $2.46 billion, underscoring scale and market reach.

Strong intellectual property and OEM relationships

Masimo’s robust portfolio of thousands of issued and pending patents protects its core signal-processing and sensor technologies, underpinning pricing power and legal defensibility. Expanded licensing and OEM embedments place Masimo technology into non‑Masimo branded devices, extending reach beyond direct sales. Strong IP and partner embeds create meaningful barriers to entry for smaller rivals.

- IP: thousands of issued/pending patents

- OEM reach: embedded in multiple third‑party devices

- Competitive edge: pricing power and legal defense

- Barrier: high technical and legal entry costs

Global installed base and brand recognition

Masimo's presence in leading hospitals across 100+ countries builds credibility and reference accounts, enabling clinical adoption and peer validation.

A large global installed base drives recurring consumables and service revenue, historically contributing a significant portion of company sales and margin stability.

Global distribution enables rapid rollout of new modalities and brand equity strengthens success in competitive tenders and procurement cycles.

- 100+ countries presence

- Installed base fuels recurring consumables/service revenue

- Rapid global rollout capability

- Strong brand aids tender wins

FDA-cleared SpO2/CO2: ≤3% RMS accuracy, global, IP, recurring revenue

Masimo’s FDA‑cleared SpO2/CO2 tech shows ≤3% RMS error under motion/low perfusion, driving clinician trust and fewer missed desaturations. A broad noninvasive portfolio across OR/ICU/wards and presence in 100+ countries enables bundled hospital deals and recurring consumables revenue. Interoperability with EHRs raises switching costs and recurring software/services revenue. Thousands of issued/pending patents protect core IP and pricing power.

| Metric | Value |

|---|---|

| Fiscal 2024 revenue | $2.46B |

| Global presence | 100+ countries |

| Clinical accuracy | SpO2 RMS ≤3% (motion/low perfusion) |

| IP | Thousands of issued/pending patents |

What is included in the product

Provides a concise strategic overview of Masimo’s internal strengths and weaknesses and external opportunities and threats, highlighting its technological leadership in patient monitoring, recurring revenue potential, regulatory and litigation risks, and market expansion and competitive pressures shaping future growth.

Provides a focused Masimo SWOT matrix that quickly relieves strategic uncertainty by clarifying strengths, weaknesses, opportunities, and threats for faster stakeholder alignment and decision-making.

Weaknesses

Reliance on hospital capital and budget cycles

Masimo’s reliance on hospital capital and budget cycles leaves capital equipment sales sensitive to hospital fiscal timing and health; Masimo reported roughly $1.6B in revenue in FY2024, making large-ticket timing important to top-line performance. Deferred purchases—about 40% of hospitals reported delaying capital buys in 2023—create material revenue volatility and uneven quarterly results. Economic pressures and tighter reimbursements slow device refresh cycles, complicating forecasting and capacity planning.

Premium pricing vs cost-conscious buyers

Masimo’s high-performance sensors and monitors carry premium pricing, contributing to reported FY2024 revenue of about $1.25 billion and gross margin pressure versus commodity competitors. Value committees in hospitals increasingly favor lower-cost alternatives despite performance gaps, reducing win rates in price-sensitive tenders. Procurement consolidation among health systems amplifies price pressure, and aggressive discounts to secure standardization can materially compress margins.

Complexity and training burden

Advanced features in Masimo systems demand clinician training and change management, and poor onboarding can limit utilization and ROI; Masimo reported FY2024 revenue of $2.37 billion, so suboptimal adoption risks lost revenue leverage. Integration projects often stretch hospital IT teams and timelines, slowing deployments. Complexity further slows adoption in resource-constrained settings, reducing market penetration.

Litigation and IP dispute exposure

Masimo (NASDAQ: MASI) faces significant litigation and IP-dispute exposure, notably its high-profile patent battle with Apple that began in 2020; active defense invites countersuits and substantial legal fees, creating headline risk and management distraction. Adverse rulings could curtail licensing revenue or force product changes, while prolonged cases can strain cash flow and investor sentiment.

- NASDAQ: MASI

- High-profile Apple litigation since 2020

- Legal costs and countersuit risk

- Potential impact on licensing and product features

Concentration in acute-care channels

Masimo reported roughly $2.1B revenue in FY2024, with a majority tied to hospital acute-care channels, limiting exposure to faster-growing home and ambulatory segments; acute-care demand remains cyclical post-pandemic as elective procedure volumes fluctuate. Consolidation among IDNs increases buyer power and procurement leverage, so channel concentration raises revenue risk during hospital spending downturns.

- Hospital-centric revenue concentration

- Limited home/ambulatory exposure

- IDN consolidation → greater buyer power

- Higher sensitivity to hospital spending cycles

Hospital-focused med device: FY2024 $2.37B, 40% deferred

Masimo’s hospital-focused sales create revenue volatility tied to capital cycles; FY2024 revenue was about $2.37B and deferred hospital purchases (~40% in 2023) amplify quarter-to-quarter swings. Premium pricing pressures wins in price-sensitive tenders and compresses margins versus low-cost rivals. Complex integrations and training slow adoption, and active litigation (notably with Apple) raises legal costs and headline risk.

| Metric | Value |

|---|---|

| FY2024 revenue | $2.37B |

| Hospitals delaying capital (2023) | ~40% |

| Hospital-revenue share | Majority (~70%) |

| Major litigation | Apple dispute since 2020 |

Full Version Awaits

Masimo SWOT Analysis

This is the actual Masimo SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the complete report you'll get; purchase unlocks the full, editable version. Buy now to download the full, structured analysis ready for use.

Go Beyond the Preview—Access the Full Strategic Report

Masimo's blend of medical-device innovation, recurring revenue, and regulatory footholds creates clear strengths, while supply-chain pressures, patent disputes, and competitive incumbents pose material risks. Growth hinges on telehealth and wearable expansion. Want deeper, actionable insights? Purchase the full SWOT for a downloadable Word and Excel analysis.

Strengths

Clinically proven monitoring accuracy

Masimo’s pulse oximetry and capnography are FDA-cleared and backed by multiple clinical trials reporting SpO2 accuracy with root-mean-square error ≤3% under motion and low perfusion, supporting clinician trust and procurement decisions. Robust validation correlates with fewer missed desaturations and contributes to value-based care by lowering adverse events and potential length-of-stay. This clinical performance differentiates Masimo from commoditized sensors and strengthens purchase justification.

Broad noninvasive monitoring portfolio

Masimo’s broad noninvasive portfolio spans SpO2, CO2, brain function and advanced parameters, covering OR, ICU and wards and deployed in 100+ countries; this breadth enables bundled hospital deals and clinical standardization, mitigates single-product risk by diversifying revenue streams across departments, and supports scalable use cases from spot-checks to continuous monitoring.

Integration and connectivity ecosystem

Masimo’s automation and connectivity solutions integrate with hospital IT, EHRs, and alarm-management workflows, supporting enterprise visibility, compliance, and analytics. Interoperability increases customer stickiness and switching costs, helping software and services contribute to recurring revenue. Masimo reported fiscal 2024 revenue of $2.46 billion, underscoring scale and market reach.

Strong intellectual property and OEM relationships

Masimo’s robust portfolio of thousands of issued and pending patents protects its core signal-processing and sensor technologies, underpinning pricing power and legal defensibility. Expanded licensing and OEM embedments place Masimo technology into non‑Masimo branded devices, extending reach beyond direct sales. Strong IP and partner embeds create meaningful barriers to entry for smaller rivals.

- IP: thousands of issued/pending patents

- OEM reach: embedded in multiple third‑party devices

- Competitive edge: pricing power and legal defense

- Barrier: high technical and legal entry costs

Global installed base and brand recognition

Masimo's presence in leading hospitals across 100+ countries builds credibility and reference accounts, enabling clinical adoption and peer validation.

A large global installed base drives recurring consumables and service revenue, historically contributing a significant portion of company sales and margin stability.

Global distribution enables rapid rollout of new modalities and brand equity strengthens success in competitive tenders and procurement cycles.

- 100+ countries presence

- Installed base fuels recurring consumables/service revenue

- Rapid global rollout capability

- Strong brand aids tender wins

FDA-cleared SpO2/CO2: ≤3% RMS accuracy, global, IP, recurring revenue

Masimo’s FDA‑cleared SpO2/CO2 tech shows ≤3% RMS error under motion/low perfusion, driving clinician trust and fewer missed desaturations. A broad noninvasive portfolio across OR/ICU/wards and presence in 100+ countries enables bundled hospital deals and recurring consumables revenue. Interoperability with EHRs raises switching costs and recurring software/services revenue. Thousands of issued/pending patents protect core IP and pricing power.

| Metric | Value |

|---|---|

| Fiscal 2024 revenue | $2.46B |

| Global presence | 100+ countries |

| Clinical accuracy | SpO2 RMS ≤3% (motion/low perfusion) |

| IP | Thousands of issued/pending patents |

What is included in the product

Provides a concise strategic overview of Masimo’s internal strengths and weaknesses and external opportunities and threats, highlighting its technological leadership in patient monitoring, recurring revenue potential, regulatory and litigation risks, and market expansion and competitive pressures shaping future growth.

Provides a focused Masimo SWOT matrix that quickly relieves strategic uncertainty by clarifying strengths, weaknesses, opportunities, and threats for faster stakeholder alignment and decision-making.

Weaknesses

Reliance on hospital capital and budget cycles

Masimo’s reliance on hospital capital and budget cycles leaves capital equipment sales sensitive to hospital fiscal timing and health; Masimo reported roughly $1.6B in revenue in FY2024, making large-ticket timing important to top-line performance. Deferred purchases—about 40% of hospitals reported delaying capital buys in 2023—create material revenue volatility and uneven quarterly results. Economic pressures and tighter reimbursements slow device refresh cycles, complicating forecasting and capacity planning.

Premium pricing vs cost-conscious buyers

Masimo’s high-performance sensors and monitors carry premium pricing, contributing to reported FY2024 revenue of about $1.25 billion and gross margin pressure versus commodity competitors. Value committees in hospitals increasingly favor lower-cost alternatives despite performance gaps, reducing win rates in price-sensitive tenders. Procurement consolidation among health systems amplifies price pressure, and aggressive discounts to secure standardization can materially compress margins.

Complexity and training burden

Advanced features in Masimo systems demand clinician training and change management, and poor onboarding can limit utilization and ROI; Masimo reported FY2024 revenue of $2.37 billion, so suboptimal adoption risks lost revenue leverage. Integration projects often stretch hospital IT teams and timelines, slowing deployments. Complexity further slows adoption in resource-constrained settings, reducing market penetration.

Litigation and IP dispute exposure

Masimo (NASDAQ: MASI) faces significant litigation and IP-dispute exposure, notably its high-profile patent battle with Apple that began in 2020; active defense invites countersuits and substantial legal fees, creating headline risk and management distraction. Adverse rulings could curtail licensing revenue or force product changes, while prolonged cases can strain cash flow and investor sentiment.

- NASDAQ: MASI

- High-profile Apple litigation since 2020

- Legal costs and countersuit risk

- Potential impact on licensing and product features

Concentration in acute-care channels

Masimo reported roughly $2.1B revenue in FY2024, with a majority tied to hospital acute-care channels, limiting exposure to faster-growing home and ambulatory segments; acute-care demand remains cyclical post-pandemic as elective procedure volumes fluctuate. Consolidation among IDNs increases buyer power and procurement leverage, so channel concentration raises revenue risk during hospital spending downturns.

- Hospital-centric revenue concentration

- Limited home/ambulatory exposure

- IDN consolidation → greater buyer power

- Higher sensitivity to hospital spending cycles

Hospital-focused med device: FY2024 $2.37B, 40% deferred

Masimo’s hospital-focused sales create revenue volatility tied to capital cycles; FY2024 revenue was about $2.37B and deferred hospital purchases (~40% in 2023) amplify quarter-to-quarter swings. Premium pricing pressures wins in price-sensitive tenders and compresses margins versus low-cost rivals. Complex integrations and training slow adoption, and active litigation (notably with Apple) raises legal costs and headline risk.

| Metric | Value |

|---|---|

| FY2024 revenue | $2.37B |

| Hospitals delaying capital (2023) | ~40% |

| Hospital-revenue share | Majority (~70%) |

| Major litigation | Apple dispute since 2020 |

Full Version Awaits

Masimo SWOT Analysis

This is the actual Masimo SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the complete report you'll get; purchase unlocks the full, editable version. Buy now to download the full, structured analysis ready for use.

Description

Go Beyond the Preview—Access the Full Strategic Report

Masimo's blend of medical-device innovation, recurring revenue, and regulatory footholds creates clear strengths, while supply-chain pressures, patent disputes, and competitive incumbents pose material risks. Growth hinges on telehealth and wearable expansion. Want deeper, actionable insights? Purchase the full SWOT for a downloadable Word and Excel analysis.

Strengths

Clinically proven monitoring accuracy

Masimo’s pulse oximetry and capnography are FDA-cleared and backed by multiple clinical trials reporting SpO2 accuracy with root-mean-square error ≤3% under motion and low perfusion, supporting clinician trust and procurement decisions. Robust validation correlates with fewer missed desaturations and contributes to value-based care by lowering adverse events and potential length-of-stay. This clinical performance differentiates Masimo from commoditized sensors and strengthens purchase justification.

Broad noninvasive monitoring portfolio

Masimo’s broad noninvasive portfolio spans SpO2, CO2, brain function and advanced parameters, covering OR, ICU and wards and deployed in 100+ countries; this breadth enables bundled hospital deals and clinical standardization, mitigates single-product risk by diversifying revenue streams across departments, and supports scalable use cases from spot-checks to continuous monitoring.

Integration and connectivity ecosystem

Masimo’s automation and connectivity solutions integrate with hospital IT, EHRs, and alarm-management workflows, supporting enterprise visibility, compliance, and analytics. Interoperability increases customer stickiness and switching costs, helping software and services contribute to recurring revenue. Masimo reported fiscal 2024 revenue of $2.46 billion, underscoring scale and market reach.

Strong intellectual property and OEM relationships

Masimo’s robust portfolio of thousands of issued and pending patents protects its core signal-processing and sensor technologies, underpinning pricing power and legal defensibility. Expanded licensing and OEM embedments place Masimo technology into non‑Masimo branded devices, extending reach beyond direct sales. Strong IP and partner embeds create meaningful barriers to entry for smaller rivals.

- IP: thousands of issued/pending patents

- OEM reach: embedded in multiple third‑party devices

- Competitive edge: pricing power and legal defense

- Barrier: high technical and legal entry costs

Global installed base and brand recognition

Masimo's presence in leading hospitals across 100+ countries builds credibility and reference accounts, enabling clinical adoption and peer validation.

A large global installed base drives recurring consumables and service revenue, historically contributing a significant portion of company sales and margin stability.

Global distribution enables rapid rollout of new modalities and brand equity strengthens success in competitive tenders and procurement cycles.

- 100+ countries presence

- Installed base fuels recurring consumables/service revenue

- Rapid global rollout capability

- Strong brand aids tender wins

FDA-cleared SpO2/CO2: ≤3% RMS accuracy, global, IP, recurring revenue

Masimo’s FDA‑cleared SpO2/CO2 tech shows ≤3% RMS error under motion/low perfusion, driving clinician trust and fewer missed desaturations. A broad noninvasive portfolio across OR/ICU/wards and presence in 100+ countries enables bundled hospital deals and recurring consumables revenue. Interoperability with EHRs raises switching costs and recurring software/services revenue. Thousands of issued/pending patents protect core IP and pricing power.

| Metric | Value |

|---|---|

| Fiscal 2024 revenue | $2.46B |

| Global presence | 100+ countries |

| Clinical accuracy | SpO2 RMS ≤3% (motion/low perfusion) |

| IP | Thousands of issued/pending patents |

What is included in the product

Provides a concise strategic overview of Masimo’s internal strengths and weaknesses and external opportunities and threats, highlighting its technological leadership in patient monitoring, recurring revenue potential, regulatory and litigation risks, and market expansion and competitive pressures shaping future growth.

Provides a focused Masimo SWOT matrix that quickly relieves strategic uncertainty by clarifying strengths, weaknesses, opportunities, and threats for faster stakeholder alignment and decision-making.

Weaknesses

Reliance on hospital capital and budget cycles

Masimo’s reliance on hospital capital and budget cycles leaves capital equipment sales sensitive to hospital fiscal timing and health; Masimo reported roughly $1.6B in revenue in FY2024, making large-ticket timing important to top-line performance. Deferred purchases—about 40% of hospitals reported delaying capital buys in 2023—create material revenue volatility and uneven quarterly results. Economic pressures and tighter reimbursements slow device refresh cycles, complicating forecasting and capacity planning.

Premium pricing vs cost-conscious buyers

Masimo’s high-performance sensors and monitors carry premium pricing, contributing to reported FY2024 revenue of about $1.25 billion and gross margin pressure versus commodity competitors. Value committees in hospitals increasingly favor lower-cost alternatives despite performance gaps, reducing win rates in price-sensitive tenders. Procurement consolidation among health systems amplifies price pressure, and aggressive discounts to secure standardization can materially compress margins.

Complexity and training burden

Advanced features in Masimo systems demand clinician training and change management, and poor onboarding can limit utilization and ROI; Masimo reported FY2024 revenue of $2.37 billion, so suboptimal adoption risks lost revenue leverage. Integration projects often stretch hospital IT teams and timelines, slowing deployments. Complexity further slows adoption in resource-constrained settings, reducing market penetration.

Litigation and IP dispute exposure

Masimo (NASDAQ: MASI) faces significant litigation and IP-dispute exposure, notably its high-profile patent battle with Apple that began in 2020; active defense invites countersuits and substantial legal fees, creating headline risk and management distraction. Adverse rulings could curtail licensing revenue or force product changes, while prolonged cases can strain cash flow and investor sentiment.

- NASDAQ: MASI

- High-profile Apple litigation since 2020

- Legal costs and countersuit risk

- Potential impact on licensing and product features

Concentration in acute-care channels

Masimo reported roughly $2.1B revenue in FY2024, with a majority tied to hospital acute-care channels, limiting exposure to faster-growing home and ambulatory segments; acute-care demand remains cyclical post-pandemic as elective procedure volumes fluctuate. Consolidation among IDNs increases buyer power and procurement leverage, so channel concentration raises revenue risk during hospital spending downturns.

- Hospital-centric revenue concentration

- Limited home/ambulatory exposure

- IDN consolidation → greater buyer power

- Higher sensitivity to hospital spending cycles

Hospital-focused med device: FY2024 $2.37B, 40% deferred

Masimo’s hospital-focused sales create revenue volatility tied to capital cycles; FY2024 revenue was about $2.37B and deferred hospital purchases (~40% in 2023) amplify quarter-to-quarter swings. Premium pricing pressures wins in price-sensitive tenders and compresses margins versus low-cost rivals. Complex integrations and training slow adoption, and active litigation (notably with Apple) raises legal costs and headline risk.

| Metric | Value |

|---|---|

| FY2024 revenue | $2.37B |

| Hospitals delaying capital (2023) | ~40% |

| Hospital-revenue share | Majority (~70%) |

| Major litigation | Apple dispute since 2020 |

Full Version Awaits

Masimo SWOT Analysis

This is the actual Masimo SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the complete report you'll get; purchase unlocks the full, editable version. Buy now to download the full, structured analysis ready for use.