Mastermyne Porter's Five Forces Analysis

From Overview to Strategy Blueprint

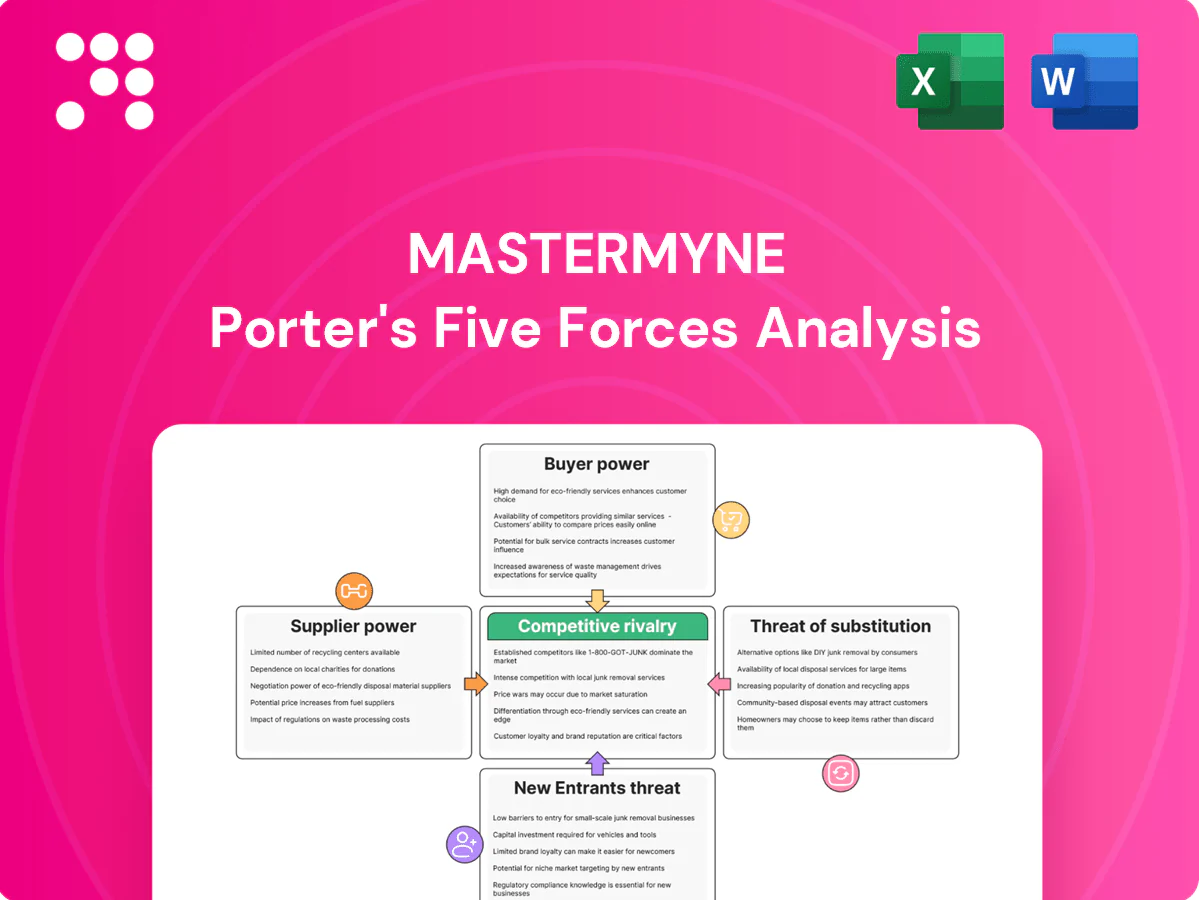

Mastermyne’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, and competitive rivalry shaping its mining-services niche. It teases threats from new entrants and substitutes while flagging strategic levers management can pull. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated OEM equipment base

Mastermyne depends on a small set of global OEMs—notably Sandvik, Epiroc and Komatsu—for longwall and development equipment, parts and maintenance. Limited alternatives give these suppliers leverage on pricing and lead times, with major longwall components often carrying procurement lead times up to 24 months. Such long-lead items can constrain project schedules and working capital. Strategic partnerships and multi-year framework agreements are used to mitigate this supplier power.

Specialist consumables dependence

Strata support, ventilation, hydraulics and gas drainage rely on specialized consumables meeting strict regulatory and safety standards, concentrating supply among a few qualified vendors and raising switching costs. Quality and safety imperatives materially reduce viable substitution, increasing supplier leverage. Bulk-buying and vendor-managed inventory arrangements are common mitigants, lowering disruption risk and stabilizing pricing as of 2024.

Skilled labor scarcity

Experienced underground crews, supervisors and engineers remain scarce across Australia’s coal basins, giving labor-hire firms and training providers notable leverage in 2024; wage inflation and retention bonuses (often ranging A$10,000–A$30,000) have squeezed contractor margins, while Mastermyne’s growing in-house training pipeline helps partially offset supplier power by upskilling staff internally.

Energy and fuel volatility

Diesel and electricity are core inputs for Mastermyne; Brent averaged about 85 USD/bbl in 2024, Australian diesel ran near AUD 1.90/L and industrial power around AUD 0.18/kWh, amplifying cost exposure from price swings and regional constraints. Contractual pass-throughs can mitigate but not eliminate margin impact. Efficiency drives and electrification offer gradual risk reduction.

- Diesel dependence: high — AUD 1.90/L (2024)

- Electricity exposure: industrial ~AUD 0.18/kWh (2024)

- Mitigation: pass-throughs, efficiency, electrification

Compliance-driven supplier lock-in

Compliance-driven supplier lock-in for Mastermyne is reinforced by site-specific approvals, certifications and safety records that narrow acceptable suppliers; audits and changeovers typically cost A$10,000–A$100,000 and take 4–12 weeks, strengthening prequalified vendors’ bargaining power. Prequalified vendors on approved lists capture higher margin work, while multi-sourcing within those lists partially balances supplier power.

- Site approvals limit pool

- Audits: A$10k–A$100k, 4–12 weeks

- Prequalification boosts supplier leverage

- Multi-sourcing mitigates concentration

Supply risk: concentrated OEMs, long lead times 24 months

Mastermyne faces high supplier power from a concentrated set of OEMs (Sandvik, Epiroc, Komatsu) with long-lead items up to 24 months, limiting flexibility and raising costs. Compliance and site approvals (audits A$10k–A$100k, 4–12 weeks) further lock in vendors while scarce skilled labor and wage retention (A$10k–A$30k) add leverage. Fuel and power exposure (diesel ~A$1.90/L, industrial power ~A$0.18/kWh) amplify input risk.

| Metric | 2024 Value |

|---|---|

| Long-lead procurement | Up to 24 months |

| Audit cost/time | A$10k–A$100k; 4–12 weeks |

| Labor retention | A$10k–A$30k bonuses |

| Diesel | A$1.90/L |

| Industrial power | A$0.18/kWh |

What is included in the product

Concise Porter's Five Forces review for Mastermyne, assessing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting strategic levers to protect margins and market share.

A one-sheet Mastermyne Porter's Five Forces that maps competitive pressure with customizable inputs and a radar chart—easy to copy into decks, integrate into Excel dashboards, and use without macros for faster strategic decisions.

Customers Bargaining Power

Few large mining clients

A handful of major coal producers dominate underground longwall work in QLD and NSW, with the top four clients representing over 70% of longwall contracts in 2024. Their scale and formal tender processes exert strong price pressure, compressing margins for contractors like Mastermyne. Losing a single longwall contract can reduce fleet utilization by 20–35% and materially hit revenue. Deep client relationships and a proven performance record are critical hedges.

Competitive tendering and KPIs

Buyers run rigorous RFPs with detailed technical and safety KPIs, forcing contractors into head-to-head comparisons on rate cards and productivity. Penalty and incentive regimes transfer operational and safety risk to the contractor, compressing margins and shifting cash-flow variability. Demonstrated low incident rates and high move efficiency materially improve a contractor’s negotiating stance and ability to win higher-margin scopes.

Ability to insource critical tasks

Larger miners such as BHP and Rio Tinto increasingly internalize development and relocation teams, creating a credible 2024-era threat of insourcing that strengthens buyer leverage over contractors. Contractors must demonstrably deliver clear cost and time advantages to retain scope, while co-sourcing models that embed contractor capability can mitigate buyer power by aligning incentives and reducing the appeal of full insourcing.

Demand cyclicality with coal prices

When coal prices soften buyers defer capex and renegotiate contract rates; during upcycles capacity tightness tempers buyer power. Framework agreements smooth pricing but often include reopeners, and workforce/fleet flexibility helps protect margins. Coal spot swings were c.30% across 2023–24, Newcastle ranging about US$100–200/t, amplifying buyer bargaining dynamics.

- Price volatility: ~30% swing 2023–24

- Newcastle: ~US$100–200/t range

- Frameworks: reopeners common

- Operational flexibility: key margin defense

Multi-year, multi-site leverage

Buyers increasingly bundle multi-site work to extract scale discounts, and by 2024 procurement trends favored 3–5 year bundled contracts that amplify negotiating leverage. Cross-site standardization lowers switching costs, enabling buyers to reassign scope quickly; contractors often accept lower margins in exchange for longer visibility. Consistent outperformance can convert competitive tenders into sole-source extensions, materially reducing buyer power.

Top-4 buyers >70% share; 20–35% fleet risk; ~30% coal volatility

Buyers concentrated: top 4 clients >70% longwall spend (2024), giving strong price leverage and risking 20–35% fleet utilization loss per contract. Rigorous RFPs, penalties and 3–5yr bundled contracts compress margins; insourcing by majors increases buyer power. Coal price swings ~30% (Newcastle US$100–200/t 2023–24) amplify renegotiation risk.

| Metric | Value (2024) |

|---|---|

| Top-4 share | >70% |

| Utilization loss | 20–35% |

| Coal price swing | ~30% (US$100–200/t) |

What You See Is What You Get

Mastermyne Porter's Five Forces Analysis

This preview shows the exact Mastermyne Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file contains a full assessment of industry rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. It is fully formatted and ready for instant download and use.

From Overview to Strategy Blueprint

Mastermyne’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, and competitive rivalry shaping its mining-services niche. It teases threats from new entrants and substitutes while flagging strategic levers management can pull. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated OEM equipment base

Mastermyne depends on a small set of global OEMs—notably Sandvik, Epiroc and Komatsu—for longwall and development equipment, parts and maintenance. Limited alternatives give these suppliers leverage on pricing and lead times, with major longwall components often carrying procurement lead times up to 24 months. Such long-lead items can constrain project schedules and working capital. Strategic partnerships and multi-year framework agreements are used to mitigate this supplier power.

Specialist consumables dependence

Strata support, ventilation, hydraulics and gas drainage rely on specialized consumables meeting strict regulatory and safety standards, concentrating supply among a few qualified vendors and raising switching costs. Quality and safety imperatives materially reduce viable substitution, increasing supplier leverage. Bulk-buying and vendor-managed inventory arrangements are common mitigants, lowering disruption risk and stabilizing pricing as of 2024.

Skilled labor scarcity

Experienced underground crews, supervisors and engineers remain scarce across Australia’s coal basins, giving labor-hire firms and training providers notable leverage in 2024; wage inflation and retention bonuses (often ranging A$10,000–A$30,000) have squeezed contractor margins, while Mastermyne’s growing in-house training pipeline helps partially offset supplier power by upskilling staff internally.

Energy and fuel volatility

Diesel and electricity are core inputs for Mastermyne; Brent averaged about 85 USD/bbl in 2024, Australian diesel ran near AUD 1.90/L and industrial power around AUD 0.18/kWh, amplifying cost exposure from price swings and regional constraints. Contractual pass-throughs can mitigate but not eliminate margin impact. Efficiency drives and electrification offer gradual risk reduction.

- Diesel dependence: high — AUD 1.90/L (2024)

- Electricity exposure: industrial ~AUD 0.18/kWh (2024)

- Mitigation: pass-throughs, efficiency, electrification

Compliance-driven supplier lock-in

Compliance-driven supplier lock-in for Mastermyne is reinforced by site-specific approvals, certifications and safety records that narrow acceptable suppliers; audits and changeovers typically cost A$10,000–A$100,000 and take 4–12 weeks, strengthening prequalified vendors’ bargaining power. Prequalified vendors on approved lists capture higher margin work, while multi-sourcing within those lists partially balances supplier power.

- Site approvals limit pool

- Audits: A$10k–A$100k, 4–12 weeks

- Prequalification boosts supplier leverage

- Multi-sourcing mitigates concentration

Supply risk: concentrated OEMs, long lead times 24 months

Mastermyne faces high supplier power from a concentrated set of OEMs (Sandvik, Epiroc, Komatsu) with long-lead items up to 24 months, limiting flexibility and raising costs. Compliance and site approvals (audits A$10k–A$100k, 4–12 weeks) further lock in vendors while scarce skilled labor and wage retention (A$10k–A$30k) add leverage. Fuel and power exposure (diesel ~A$1.90/L, industrial power ~A$0.18/kWh) amplify input risk.

| Metric | 2024 Value |

|---|---|

| Long-lead procurement | Up to 24 months |

| Audit cost/time | A$10k–A$100k; 4–12 weeks |

| Labor retention | A$10k–A$30k bonuses |

| Diesel | A$1.90/L |

| Industrial power | A$0.18/kWh |

What is included in the product

Concise Porter's Five Forces review for Mastermyne, assessing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting strategic levers to protect margins and market share.

A one-sheet Mastermyne Porter's Five Forces that maps competitive pressure with customizable inputs and a radar chart—easy to copy into decks, integrate into Excel dashboards, and use without macros for faster strategic decisions.

Customers Bargaining Power

Few large mining clients

A handful of major coal producers dominate underground longwall work in QLD and NSW, with the top four clients representing over 70% of longwall contracts in 2024. Their scale and formal tender processes exert strong price pressure, compressing margins for contractors like Mastermyne. Losing a single longwall contract can reduce fleet utilization by 20–35% and materially hit revenue. Deep client relationships and a proven performance record are critical hedges.

Competitive tendering and KPIs

Buyers run rigorous RFPs with detailed technical and safety KPIs, forcing contractors into head-to-head comparisons on rate cards and productivity. Penalty and incentive regimes transfer operational and safety risk to the contractor, compressing margins and shifting cash-flow variability. Demonstrated low incident rates and high move efficiency materially improve a contractor’s negotiating stance and ability to win higher-margin scopes.

Ability to insource critical tasks

Larger miners such as BHP and Rio Tinto increasingly internalize development and relocation teams, creating a credible 2024-era threat of insourcing that strengthens buyer leverage over contractors. Contractors must demonstrably deliver clear cost and time advantages to retain scope, while co-sourcing models that embed contractor capability can mitigate buyer power by aligning incentives and reducing the appeal of full insourcing.

Demand cyclicality with coal prices

When coal prices soften buyers defer capex and renegotiate contract rates; during upcycles capacity tightness tempers buyer power. Framework agreements smooth pricing but often include reopeners, and workforce/fleet flexibility helps protect margins. Coal spot swings were c.30% across 2023–24, Newcastle ranging about US$100–200/t, amplifying buyer bargaining dynamics.

- Price volatility: ~30% swing 2023–24

- Newcastle: ~US$100–200/t range

- Frameworks: reopeners common

- Operational flexibility: key margin defense

Multi-year, multi-site leverage

Buyers increasingly bundle multi-site work to extract scale discounts, and by 2024 procurement trends favored 3–5 year bundled contracts that amplify negotiating leverage. Cross-site standardization lowers switching costs, enabling buyers to reassign scope quickly; contractors often accept lower margins in exchange for longer visibility. Consistent outperformance can convert competitive tenders into sole-source extensions, materially reducing buyer power.

Top-4 buyers >70% share; 20–35% fleet risk; ~30% coal volatility

Buyers concentrated: top 4 clients >70% longwall spend (2024), giving strong price leverage and risking 20–35% fleet utilization loss per contract. Rigorous RFPs, penalties and 3–5yr bundled contracts compress margins; insourcing by majors increases buyer power. Coal price swings ~30% (Newcastle US$100–200/t 2023–24) amplify renegotiation risk.

| Metric | Value (2024) |

|---|---|

| Top-4 share | >70% |

| Utilization loss | 20–35% |

| Coal price swing | ~30% (US$100–200/t) |

What You See Is What You Get

Mastermyne Porter's Five Forces Analysis

This preview shows the exact Mastermyne Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file contains a full assessment of industry rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. It is fully formatted and ready for instant download and use.

Description

From Overview to Strategy Blueprint

Mastermyne’s Porter's Five Forces snapshot highlights supplier leverage, buyer pressure, and competitive rivalry shaping its mining-services niche. It teases threats from new entrants and substitutes while flagging strategic levers management can pull. This brief only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable strategy.

Suppliers Bargaining Power

Concentrated OEM equipment base

Mastermyne depends on a small set of global OEMs—notably Sandvik, Epiroc and Komatsu—for longwall and development equipment, parts and maintenance. Limited alternatives give these suppliers leverage on pricing and lead times, with major longwall components often carrying procurement lead times up to 24 months. Such long-lead items can constrain project schedules and working capital. Strategic partnerships and multi-year framework agreements are used to mitigate this supplier power.

Specialist consumables dependence

Strata support, ventilation, hydraulics and gas drainage rely on specialized consumables meeting strict regulatory and safety standards, concentrating supply among a few qualified vendors and raising switching costs. Quality and safety imperatives materially reduce viable substitution, increasing supplier leverage. Bulk-buying and vendor-managed inventory arrangements are common mitigants, lowering disruption risk and stabilizing pricing as of 2024.

Skilled labor scarcity

Experienced underground crews, supervisors and engineers remain scarce across Australia’s coal basins, giving labor-hire firms and training providers notable leverage in 2024; wage inflation and retention bonuses (often ranging A$10,000–A$30,000) have squeezed contractor margins, while Mastermyne’s growing in-house training pipeline helps partially offset supplier power by upskilling staff internally.

Energy and fuel volatility

Diesel and electricity are core inputs for Mastermyne; Brent averaged about 85 USD/bbl in 2024, Australian diesel ran near AUD 1.90/L and industrial power around AUD 0.18/kWh, amplifying cost exposure from price swings and regional constraints. Contractual pass-throughs can mitigate but not eliminate margin impact. Efficiency drives and electrification offer gradual risk reduction.

- Diesel dependence: high — AUD 1.90/L (2024)

- Electricity exposure: industrial ~AUD 0.18/kWh (2024)

- Mitigation: pass-throughs, efficiency, electrification

Compliance-driven supplier lock-in

Compliance-driven supplier lock-in for Mastermyne is reinforced by site-specific approvals, certifications and safety records that narrow acceptable suppliers; audits and changeovers typically cost A$10,000–A$100,000 and take 4–12 weeks, strengthening prequalified vendors’ bargaining power. Prequalified vendors on approved lists capture higher margin work, while multi-sourcing within those lists partially balances supplier power.

- Site approvals limit pool

- Audits: A$10k–A$100k, 4–12 weeks

- Prequalification boosts supplier leverage

- Multi-sourcing mitigates concentration

Supply risk: concentrated OEMs, long lead times 24 months

Mastermyne faces high supplier power from a concentrated set of OEMs (Sandvik, Epiroc, Komatsu) with long-lead items up to 24 months, limiting flexibility and raising costs. Compliance and site approvals (audits A$10k–A$100k, 4–12 weeks) further lock in vendors while scarce skilled labor and wage retention (A$10k–A$30k) add leverage. Fuel and power exposure (diesel ~A$1.90/L, industrial power ~A$0.18/kWh) amplify input risk.

| Metric | 2024 Value |

|---|---|

| Long-lead procurement | Up to 24 months |

| Audit cost/time | A$10k–A$100k; 4–12 weeks |

| Labor retention | A$10k–A$30k bonuses |

| Diesel | A$1.90/L |

| Industrial power | A$0.18/kWh |

What is included in the product

Concise Porter's Five Forces review for Mastermyne, assessing competitive rivalry, buyer and supplier power, threat of new entrants and substitutes, and highlighting strategic levers to protect margins and market share.

A one-sheet Mastermyne Porter's Five Forces that maps competitive pressure with customizable inputs and a radar chart—easy to copy into decks, integrate into Excel dashboards, and use without macros for faster strategic decisions.

Customers Bargaining Power

Few large mining clients

A handful of major coal producers dominate underground longwall work in QLD and NSW, with the top four clients representing over 70% of longwall contracts in 2024. Their scale and formal tender processes exert strong price pressure, compressing margins for contractors like Mastermyne. Losing a single longwall contract can reduce fleet utilization by 20–35% and materially hit revenue. Deep client relationships and a proven performance record are critical hedges.

Competitive tendering and KPIs

Buyers run rigorous RFPs with detailed technical and safety KPIs, forcing contractors into head-to-head comparisons on rate cards and productivity. Penalty and incentive regimes transfer operational and safety risk to the contractor, compressing margins and shifting cash-flow variability. Demonstrated low incident rates and high move efficiency materially improve a contractor’s negotiating stance and ability to win higher-margin scopes.

Ability to insource critical tasks

Larger miners such as BHP and Rio Tinto increasingly internalize development and relocation teams, creating a credible 2024-era threat of insourcing that strengthens buyer leverage over contractors. Contractors must demonstrably deliver clear cost and time advantages to retain scope, while co-sourcing models that embed contractor capability can mitigate buyer power by aligning incentives and reducing the appeal of full insourcing.

Demand cyclicality with coal prices

When coal prices soften buyers defer capex and renegotiate contract rates; during upcycles capacity tightness tempers buyer power. Framework agreements smooth pricing but often include reopeners, and workforce/fleet flexibility helps protect margins. Coal spot swings were c.30% across 2023–24, Newcastle ranging about US$100–200/t, amplifying buyer bargaining dynamics.

- Price volatility: ~30% swing 2023–24

- Newcastle: ~US$100–200/t range

- Frameworks: reopeners common

- Operational flexibility: key margin defense

Multi-year, multi-site leverage

Buyers increasingly bundle multi-site work to extract scale discounts, and by 2024 procurement trends favored 3–5 year bundled contracts that amplify negotiating leverage. Cross-site standardization lowers switching costs, enabling buyers to reassign scope quickly; contractors often accept lower margins in exchange for longer visibility. Consistent outperformance can convert competitive tenders into sole-source extensions, materially reducing buyer power.

Top-4 buyers >70% share; 20–35% fleet risk; ~30% coal volatility

Buyers concentrated: top 4 clients >70% longwall spend (2024), giving strong price leverage and risking 20–35% fleet utilization loss per contract. Rigorous RFPs, penalties and 3–5yr bundled contracts compress margins; insourcing by majors increases buyer power. Coal price swings ~30% (Newcastle US$100–200/t 2023–24) amplify renegotiation risk.

| Metric | Value (2024) |

|---|---|

| Top-4 share | >70% |

| Utilization loss | 20–35% |

| Coal price swing | ~30% (US$100–200/t) |

What You See Is What You Get

Mastermyne Porter's Five Forces Analysis

This preview shows the exact Mastermyne Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The file contains a full assessment of industry rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. It is fully formatted and ready for instant download and use.