Matahari Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

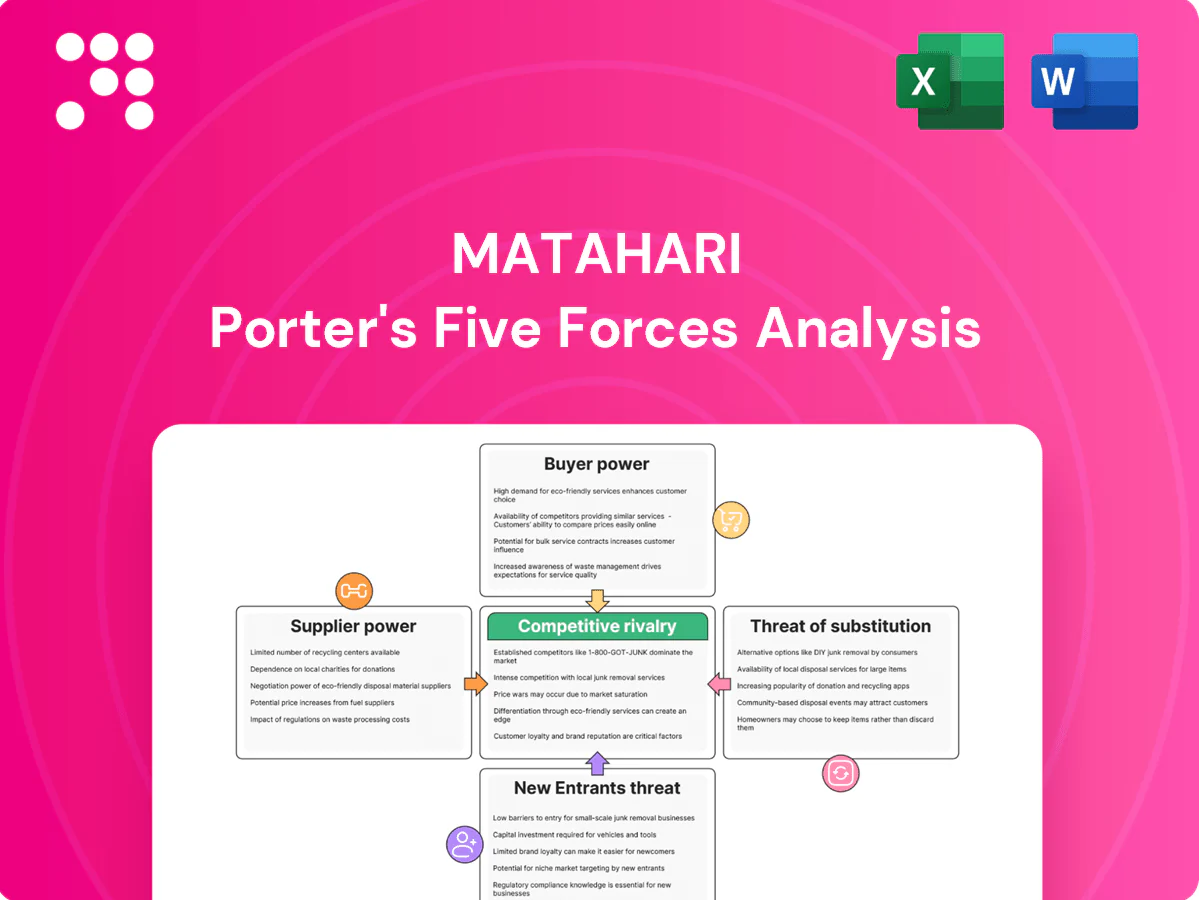

Matahari’s Porter's Five Forces snapshot highlights intense rivalry, moderate supplier leverage, strong buyer sensitivity, and looming substitute threats—key factors shaping retail margins and growth. This brief scratches the surface; unlock the full analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or competitive decisions.

Suppliers Bargaining Power

Diverse vendor base dilutes leverage

Indonesia’s apparel and beauty supply chains remained highly fragmented in 2024 across local manufacturers, importers and global brands, preventing any single supplier from dominating Matahari’s sourcing decisions. Matahari sources similar SKUs from dozens of vendors, enabling periodic re-bidding and vendor rotation to maintain competitive terms. This supplier diversity constrains pricing power and contractual leverage, supporting margin resilience.

Scale buying grants volume discounts

Matahari’s nationwide footprint of over 150 stores enables bulk purchasing and annual volume commitments, prompting suppliers in 2024 to offer better pricing, extended payment terms, and category exclusivity to secure large orders. Aggregated procurement lowers per-unit costs—often improving margins by roughly 5–15%—and enhances negotiating leverage with national suppliers. Scale also supports private-label development that further disciplines vendor margins.

Private labels cap upstream power

House brands substitute for third-party labels, reducing Matahari’s reliance on branded suppliers; in 2024 Matahari scaled private-label assortments to reinforce this channel. By controlling design and sourcing, Matahari can shift volumes to preferred factories, cutting lead times and costs. Private labels increase bargaining power with branded partners by offering credible alternatives, keeping supplier switching feasible and cost-effective.

Import exposure adds FX and lead-time risk

Import exposure raises FX and lead-time risk for Matahari: USD/IDR averaged about 15,200 in 2024, so currency swings squeeze supplier terms and vendors often pass through FX volatility, pressuring gross margins. Extended lead times reduce replenishment flexibility and constrain markdowns, increasing inventory carry and stockouts. Matahari must hedge FX and diversify sourcing to dampen these pressures.

- FX pass-through: vendors shift costs to buyers

- Lead times: limits on replenishment and markdown agility

- Mitigants: hedging and multi-origin sourcing

Exclusive brand ties create pockets of power

Where a supplier controls a high-demand brand with limited alternatives, leverage tilts their way, and exclusivity or limited distribution constrains Matahari’s assortment flexibility and pricing; as of 2024 Matahari operates over 150 stores, so single-brand bottlenecks can impact sales at scale. Matahari counters via broad portfolio and rotating featured brands; balanced category planning reduces overexposure to any one premium label.

- Supplier leverage: exclusive brands limit negotiation

- Matahari scale: >150 stores in 2024 aids assortment reach

- Mitigants: portfolio breadth, rotating features, category balancing

150+ stores and fragmented suppliers enable private-label margin lift of 5-15% amid FX risk

Supplier power is constrained by fragmented 2024 supply chains and Matahari’s >150 stores, enabling re-bidding, vendor rotation and private-label scale that improve margins ~5–15%. Import exposure (USD/IDR ~15,200 in 2024) raises FX pass-through and lead‑time risk, requiring hedging and multi-origin sourcing. Exclusive brands remain the main supplier leverage point, mitigated by portfolio rotation.

| Metric | 2024 |

|---|---|

| Stores | >150 |

| USD/IDR avg | ~15,200 |

| Private-label margin lift | 5–15% |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Matahari, uncovering competitive intensity, buyer and supplier power, threats from new entrants and substitutes, and strategic levers to protect and grow market share.

A concise, one-sheet Matahari Porter's Five Forces analysis that instantly highlights strategic pressures with an editable spider chart, easy-to-customize scores, and a clean layout ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Abundant alternatives heighten choice

Shoppers freely switch among department stores, specialty fast-fashion, marketplaces, and brand-owned stores, with Indonesia internet penetration at 77% and e-commerce accounting for roughly 13% of retail sales in 2024. Low switching costs amplify price sensitivity and shrink brand loyalty. Convenience, promotions and same-day delivery heavily influence channel choice. This breadth elevates buyer power over assortments and pricing.

Price- and promo-driven behavior

Indonesian retail is promotion-intensive—frequent discounts, bundles and seasonal sales push customers to anchor on deal prices, compressing Matahari’s margins. Loyalty programs and vouchers are expected table stakes, raising acquisition costs and lowering price stickiness. Sustained promo cadence trains demand and raises buyer leverage, amplified across a population of about 276 million (2024), increasing bargaining power.

Omnichannel expectations rising

Omnichannel expectations rising: 72% of shoppers in 2024 say seamless online-offline inventory visibility, pickup and returns are must-haves, so inconsistent pricing or fragmented stock drives churn fast. If Matahari lags marketplaces on fulfillment or unified pricing, customers switch quickly, raising their bargaining power. Elevating service standards to match product quality and adding click-and-collect and easy returns increases switching frictions and lowers buyer leverage.

Middle-class growth, but value focus

Indonesia had about 205 million internet users in 2024, and expanding middle-income segments broaden demand while keeping value-for-money central. Shoppers routinely compare prices across apps before visiting stores, and transparent online pricing strengthens customer negotiating power. Curated value tiers and private labels can reframe perceived value and blunt that power.

- Middle-income expansion: broader demand

- 205M internet users (2024): price comparison

- Transparent pricing: stronger customer leverage

- Private labels/value tiers: reduce customer power

Geographic convenience matters

Geographic convenience drives buyer power: Matahari's mall and secondary-city proximity often makes it the nearest full-range apparel option, softening customer bargaining where it is the closest choice, while in dense urban corridors with many rivals customer power strengthens; Indonesia's urbanization reached about 57.8% in 2024, concentrating rivals in metros. Network planning—relocations, format diversification, pop-ups—can rebalance local leverage.

- Nearest-store advantage reduces buyer power

- High-density metros increase customer leverage

- 2024 urbanization 57.8%

- Network adjustments mitigate local bargaining

Shoppers switch channels; price sensitivity and omnichannel gaps drive churn

Shoppers freely switch across channels, with 205M internet users and e-commerce ~13% of retail (2024), raising price sensitivity. Promotion-heavy retail compresses Matahari’s margins and lifts buyer leverage. Rising omnichannel expectations (72% demand unified service) make inconsistent fulfillment a churn driver.

| Metric | 2024 |

|---|---|

| Internet users | 205M |

| E‑commerce share | ~13% |

| Urbanization | 57.8% |

Same Document Delivered

Matahari Porter's Five Forces Analysis

This preview shows the exact Matahari Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, actionable, and ready for download the moment you buy. You're viewing the final deliverable.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Matahari’s Porter's Five Forces snapshot highlights intense rivalry, moderate supplier leverage, strong buyer sensitivity, and looming substitute threats—key factors shaping retail margins and growth. This brief scratches the surface; unlock the full analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or competitive decisions.

Suppliers Bargaining Power

Diverse vendor base dilutes leverage

Indonesia’s apparel and beauty supply chains remained highly fragmented in 2024 across local manufacturers, importers and global brands, preventing any single supplier from dominating Matahari’s sourcing decisions. Matahari sources similar SKUs from dozens of vendors, enabling periodic re-bidding and vendor rotation to maintain competitive terms. This supplier diversity constrains pricing power and contractual leverage, supporting margin resilience.

Scale buying grants volume discounts

Matahari’s nationwide footprint of over 150 stores enables bulk purchasing and annual volume commitments, prompting suppliers in 2024 to offer better pricing, extended payment terms, and category exclusivity to secure large orders. Aggregated procurement lowers per-unit costs—often improving margins by roughly 5–15%—and enhances negotiating leverage with national suppliers. Scale also supports private-label development that further disciplines vendor margins.

Private labels cap upstream power

House brands substitute for third-party labels, reducing Matahari’s reliance on branded suppliers; in 2024 Matahari scaled private-label assortments to reinforce this channel. By controlling design and sourcing, Matahari can shift volumes to preferred factories, cutting lead times and costs. Private labels increase bargaining power with branded partners by offering credible alternatives, keeping supplier switching feasible and cost-effective.

Import exposure adds FX and lead-time risk

Import exposure raises FX and lead-time risk for Matahari: USD/IDR averaged about 15,200 in 2024, so currency swings squeeze supplier terms and vendors often pass through FX volatility, pressuring gross margins. Extended lead times reduce replenishment flexibility and constrain markdowns, increasing inventory carry and stockouts. Matahari must hedge FX and diversify sourcing to dampen these pressures.

- FX pass-through: vendors shift costs to buyers

- Lead times: limits on replenishment and markdown agility

- Mitigants: hedging and multi-origin sourcing

Exclusive brand ties create pockets of power

Where a supplier controls a high-demand brand with limited alternatives, leverage tilts their way, and exclusivity or limited distribution constrains Matahari’s assortment flexibility and pricing; as of 2024 Matahari operates over 150 stores, so single-brand bottlenecks can impact sales at scale. Matahari counters via broad portfolio and rotating featured brands; balanced category planning reduces overexposure to any one premium label.

- Supplier leverage: exclusive brands limit negotiation

- Matahari scale: >150 stores in 2024 aids assortment reach

- Mitigants: portfolio breadth, rotating features, category balancing

150+ stores and fragmented suppliers enable private-label margin lift of 5-15% amid FX risk

Supplier power is constrained by fragmented 2024 supply chains and Matahari’s >150 stores, enabling re-bidding, vendor rotation and private-label scale that improve margins ~5–15%. Import exposure (USD/IDR ~15,200 in 2024) raises FX pass-through and lead‑time risk, requiring hedging and multi-origin sourcing. Exclusive brands remain the main supplier leverage point, mitigated by portfolio rotation.

| Metric | 2024 |

|---|---|

| Stores | >150 |

| USD/IDR avg | ~15,200 |

| Private-label margin lift | 5–15% |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Matahari, uncovering competitive intensity, buyer and supplier power, threats from new entrants and substitutes, and strategic levers to protect and grow market share.

A concise, one-sheet Matahari Porter's Five Forces analysis that instantly highlights strategic pressures with an editable spider chart, easy-to-customize scores, and a clean layout ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Abundant alternatives heighten choice

Shoppers freely switch among department stores, specialty fast-fashion, marketplaces, and brand-owned stores, with Indonesia internet penetration at 77% and e-commerce accounting for roughly 13% of retail sales in 2024. Low switching costs amplify price sensitivity and shrink brand loyalty. Convenience, promotions and same-day delivery heavily influence channel choice. This breadth elevates buyer power over assortments and pricing.

Price- and promo-driven behavior

Indonesian retail is promotion-intensive—frequent discounts, bundles and seasonal sales push customers to anchor on deal prices, compressing Matahari’s margins. Loyalty programs and vouchers are expected table stakes, raising acquisition costs and lowering price stickiness. Sustained promo cadence trains demand and raises buyer leverage, amplified across a population of about 276 million (2024), increasing bargaining power.

Omnichannel expectations rising

Omnichannel expectations rising: 72% of shoppers in 2024 say seamless online-offline inventory visibility, pickup and returns are must-haves, so inconsistent pricing or fragmented stock drives churn fast. If Matahari lags marketplaces on fulfillment or unified pricing, customers switch quickly, raising their bargaining power. Elevating service standards to match product quality and adding click-and-collect and easy returns increases switching frictions and lowers buyer leverage.

Middle-class growth, but value focus

Indonesia had about 205 million internet users in 2024, and expanding middle-income segments broaden demand while keeping value-for-money central. Shoppers routinely compare prices across apps before visiting stores, and transparent online pricing strengthens customer negotiating power. Curated value tiers and private labels can reframe perceived value and blunt that power.

- Middle-income expansion: broader demand

- 205M internet users (2024): price comparison

- Transparent pricing: stronger customer leverage

- Private labels/value tiers: reduce customer power

Geographic convenience matters

Geographic convenience drives buyer power: Matahari's mall and secondary-city proximity often makes it the nearest full-range apparel option, softening customer bargaining where it is the closest choice, while in dense urban corridors with many rivals customer power strengthens; Indonesia's urbanization reached about 57.8% in 2024, concentrating rivals in metros. Network planning—relocations, format diversification, pop-ups—can rebalance local leverage.

- Nearest-store advantage reduces buyer power

- High-density metros increase customer leverage

- 2024 urbanization 57.8%

- Network adjustments mitigate local bargaining

Shoppers switch channels; price sensitivity and omnichannel gaps drive churn

Shoppers freely switch across channels, with 205M internet users and e-commerce ~13% of retail (2024), raising price sensitivity. Promotion-heavy retail compresses Matahari’s margins and lifts buyer leverage. Rising omnichannel expectations (72% demand unified service) make inconsistent fulfillment a churn driver.

| Metric | 2024 |

|---|---|

| Internet users | 205M |

| E‑commerce share | ~13% |

| Urbanization | 57.8% |

Same Document Delivered

Matahari Porter's Five Forces Analysis

This preview shows the exact Matahari Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, actionable, and ready for download the moment you buy. You're viewing the final deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Matahari’s Porter's Five Forces snapshot highlights intense rivalry, moderate supplier leverage, strong buyer sensitivity, and looming substitute threats—key factors shaping retail margins and growth. This brief scratches the surface; unlock the full analysis for force-by-force ratings, visuals, and actionable strategy to inform investment or competitive decisions.

Suppliers Bargaining Power

Diverse vendor base dilutes leverage

Indonesia’s apparel and beauty supply chains remained highly fragmented in 2024 across local manufacturers, importers and global brands, preventing any single supplier from dominating Matahari’s sourcing decisions. Matahari sources similar SKUs from dozens of vendors, enabling periodic re-bidding and vendor rotation to maintain competitive terms. This supplier diversity constrains pricing power and contractual leverage, supporting margin resilience.

Scale buying grants volume discounts

Matahari’s nationwide footprint of over 150 stores enables bulk purchasing and annual volume commitments, prompting suppliers in 2024 to offer better pricing, extended payment terms, and category exclusivity to secure large orders. Aggregated procurement lowers per-unit costs—often improving margins by roughly 5–15%—and enhances negotiating leverage with national suppliers. Scale also supports private-label development that further disciplines vendor margins.

Private labels cap upstream power

House brands substitute for third-party labels, reducing Matahari’s reliance on branded suppliers; in 2024 Matahari scaled private-label assortments to reinforce this channel. By controlling design and sourcing, Matahari can shift volumes to preferred factories, cutting lead times and costs. Private labels increase bargaining power with branded partners by offering credible alternatives, keeping supplier switching feasible and cost-effective.

Import exposure adds FX and lead-time risk

Import exposure raises FX and lead-time risk for Matahari: USD/IDR averaged about 15,200 in 2024, so currency swings squeeze supplier terms and vendors often pass through FX volatility, pressuring gross margins. Extended lead times reduce replenishment flexibility and constrain markdowns, increasing inventory carry and stockouts. Matahari must hedge FX and diversify sourcing to dampen these pressures.

- FX pass-through: vendors shift costs to buyers

- Lead times: limits on replenishment and markdown agility

- Mitigants: hedging and multi-origin sourcing

Exclusive brand ties create pockets of power

Where a supplier controls a high-demand brand with limited alternatives, leverage tilts their way, and exclusivity or limited distribution constrains Matahari’s assortment flexibility and pricing; as of 2024 Matahari operates over 150 stores, so single-brand bottlenecks can impact sales at scale. Matahari counters via broad portfolio and rotating featured brands; balanced category planning reduces overexposure to any one premium label.

- Supplier leverage: exclusive brands limit negotiation

- Matahari scale: >150 stores in 2024 aids assortment reach

- Mitigants: portfolio breadth, rotating features, category balancing

150+ stores and fragmented suppliers enable private-label margin lift of 5-15% amid FX risk

Supplier power is constrained by fragmented 2024 supply chains and Matahari’s >150 stores, enabling re-bidding, vendor rotation and private-label scale that improve margins ~5–15%. Import exposure (USD/IDR ~15,200 in 2024) raises FX pass-through and lead‑time risk, requiring hedging and multi-origin sourcing. Exclusive brands remain the main supplier leverage point, mitigated by portfolio rotation.

| Metric | 2024 |

|---|---|

| Stores | >150 |

| USD/IDR avg | ~15,200 |

| Private-label margin lift | 5–15% |

What is included in the product

Provides a tailored Porter's Five Forces assessment of Matahari, uncovering competitive intensity, buyer and supplier power, threats from new entrants and substitutes, and strategic levers to protect and grow market share.

A concise, one-sheet Matahari Porter's Five Forces analysis that instantly highlights strategic pressures with an editable spider chart, easy-to-customize scores, and a clean layout ready to drop into pitch decks or boardroom slides.

Customers Bargaining Power

Abundant alternatives heighten choice

Shoppers freely switch among department stores, specialty fast-fashion, marketplaces, and brand-owned stores, with Indonesia internet penetration at 77% and e-commerce accounting for roughly 13% of retail sales in 2024. Low switching costs amplify price sensitivity and shrink brand loyalty. Convenience, promotions and same-day delivery heavily influence channel choice. This breadth elevates buyer power over assortments and pricing.

Price- and promo-driven behavior

Indonesian retail is promotion-intensive—frequent discounts, bundles and seasonal sales push customers to anchor on deal prices, compressing Matahari’s margins. Loyalty programs and vouchers are expected table stakes, raising acquisition costs and lowering price stickiness. Sustained promo cadence trains demand and raises buyer leverage, amplified across a population of about 276 million (2024), increasing bargaining power.

Omnichannel expectations rising

Omnichannel expectations rising: 72% of shoppers in 2024 say seamless online-offline inventory visibility, pickup and returns are must-haves, so inconsistent pricing or fragmented stock drives churn fast. If Matahari lags marketplaces on fulfillment or unified pricing, customers switch quickly, raising their bargaining power. Elevating service standards to match product quality and adding click-and-collect and easy returns increases switching frictions and lowers buyer leverage.

Middle-class growth, but value focus

Indonesia had about 205 million internet users in 2024, and expanding middle-income segments broaden demand while keeping value-for-money central. Shoppers routinely compare prices across apps before visiting stores, and transparent online pricing strengthens customer negotiating power. Curated value tiers and private labels can reframe perceived value and blunt that power.

- Middle-income expansion: broader demand

- 205M internet users (2024): price comparison

- Transparent pricing: stronger customer leverage

- Private labels/value tiers: reduce customer power

Geographic convenience matters

Geographic convenience drives buyer power: Matahari's mall and secondary-city proximity often makes it the nearest full-range apparel option, softening customer bargaining where it is the closest choice, while in dense urban corridors with many rivals customer power strengthens; Indonesia's urbanization reached about 57.8% in 2024, concentrating rivals in metros. Network planning—relocations, format diversification, pop-ups—can rebalance local leverage.

- Nearest-store advantage reduces buyer power

- High-density metros increase customer leverage

- 2024 urbanization 57.8%

- Network adjustments mitigate local bargaining

Shoppers switch channels; price sensitivity and omnichannel gaps drive churn

Shoppers freely switch across channels, with 205M internet users and e-commerce ~13% of retail (2024), raising price sensitivity. Promotion-heavy retail compresses Matahari’s margins and lifts buyer leverage. Rising omnichannel expectations (72% demand unified service) make inconsistent fulfillment a churn driver.

| Metric | 2024 |

|---|---|

| Internet users | 205M |

| E‑commerce share | ~13% |

| Urbanization | 57.8% |

Same Document Delivered

Matahari Porter's Five Forces Analysis

This preview shows the exact Matahari Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The document is fully formatted, actionable, and ready for download the moment you buy. You're viewing the final deliverable.