Materion Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Materion faces intense rivalry and moderate buyer power in specialty materials, with supplier influence driven by scarce raw inputs and a growing threat from substitutes and new entrants in advanced alloys and coatings. This snapshot highlights key tensions but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to explore Materion’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce critical inputs

Many of Materion’s feedstocks—beryllium, high‑purity ceramics and noble metals—are scarce and sourced from a handful of countries (US, China, Kazakhstan), concentrating supplier leverage; Materion reported roughly $1.2B revenue in 2024, so input cost swings materially affect margins. Price volatility and allocation risk can ripple through costs, and supply‑assurance programs and hedging only partially mitigate these shocks.

Regulation and compliance burden

Environmental, health and safety rules for toxic and hard-to-handle inputs notably raise supplier leverage for Materion, since compliance costs and permitting shrink the pool of qualified upstream providers; EU REACH covered over 22,000 registered substances by 2024, increasing traceability burdens. Certification audits and chain-of-custody traceability add switching frictions and time-to-source. Any regulatory tightening quickly amplifies supplier power and dependence.

Backward integration offsets

Materion’s upstream capabilities in select materials such as beryllium—central to its engineered materials portfolio—temper supplier power, underpinning a business that reported about $1.1 billion in net sales in fiscal 2024. Internal processing knowledge and in-house refining reduce reliance on external sources for some high-value inputs. Strategic inventories and dual-sourcing arrangements further mitigate supplier leverage. However, key specialty inputs and rare alloys remain difficult or uneconomic to fully integrate.

Long-term, specialty contracts

Long-term, specialty contracts stabilize Materion supply chains but embed supplier terms through technical specs and custom formulations that increase supplier leverage. Vendor-managed quality and proprietary blends create high switching costs and relational lock-in; renegotiation cycles often shift bargaining power to suppliers in tight markets. Index-linked pricing transmits commodity spikes quickly, compressing margins.

- Multi-year terms: lock-in risk

- Vendor-managed quality: high switching cost

- Renegotiation favors suppliers in tight markets

- Index-linked pricing: rapid commodity pass-through

Processing know-how as counterweight

Materion’s proprietary metallurgical and ceramic processes create bespoke input specs that narrow the pool of viable suppliers, but co-development relationships and shared process IP give Materion leverage—in 2024 the company continued investing in process R&D, keeping supplier options concentrated while using collaboration to negotiate terms.

- Limited supplier pool due to unique inputs

- Co-development yields joint IP and bargaining chips

- 2024 R&D-led collaborations strengthened negotiating position

- Dependence remains where substitutes are scarce

Scarce feedstocks in US/China/Kazakhstan boost supplier power;$1.2B revenue margin-sensitive

Materion faces high supplier power: scarce inputs (beryllium, noble metals) are concentrated in US, China, Kazakhstan while $1.2B revenue in 2024 makes input swings margin‑sensitive. EHS and REACH compliance (22,000+ substances by 2024) raise switching costs. In‑house processing and R&D reduce but do not eliminate dependence; long contracts and index pricing preserve supplier leverage.

| Metric | 2024 |

|---|---|

| Revenue | $1.2B |

| Net sales (reported) | $1.1B |

| Critical feedstock concentration | US, China, Kazakhstan |

| REACH registry | 22,000+ substances |

What is included in the product

Tailored Porter's Five Forces analysis for Materion, uncovering key competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats that shape pricing, profitability and strategic positioning in specialty materials markets.

A concise, one-sheet Materion Porter's Five Forces summary that visualizes competitive pressure, suggests strategic levers for suppliers, buyers, rivals, entrants and substitutes, and is ready to drop into decks or scenario tabs without macros.

Customers Bargaining Power

Concentrated blue-chip OEMs

Concentrated blue-chip OEMs in aerospace, semiconductor, automotive, and medical purchase large volumes from Materion and exert strong negotiating leverage, reflecting the global semiconductor market of roughly $600 billion in 2024 and large aerospace OEM procurement scales. They enforce strict quality, delivery, and aggressive cost-down targets, with supplier scorecards and dual-sourcing keeping margin pressure intense. Volume commitments are commonly traded for price concessions and longer payment terms.

High qualification and switching costs

Materials are tightly specified with qualification cycles commonly 12–36 months, making buyer switching difficult and often incurring switching costs frequently above $500,000, which dampens day-to-day price pressure once approved. Buyers, however, can leverage future program awards to extract concessions. End-use regulatory compliance can further delay substitutions by an additional 6–18 months, reinforcing incumbent advantage.

Customization increases stickiness

Co-engineered alloys and ceramics embed Materion into customer designs, creating technical lock-in that raises switching costs. Tailored specifications and application support increase exit barriers and allow for premium pricing on specialized solutions. However, industry-wide design-to-cost programs and supplier consolidation can pressure margins over time. Ongoing collaboration is needed to defend pricing power and margin durability.

Total cost-of-ownership focus

Buyers prioritize total cost of ownership, valuing reliability, performance and yield impact over unit price; materials that improve device performance or reduce scrap materially weaken buyer leverage. Service-level SLAs and technical support create stickiness and premium pricing power, even as procurement continues to benchmark global alternatives; the global semiconductor market (~600 billion in 2024) heightens sourcing scrutiny.

- Reliability > unit price

- Yield reduction reduces buyer power

- SLAs/tech support add value

- Global benchmarking persists

Cyclical demand bargaining

Downcycles in electronics and aerospace MRO elevate buyer leverage as volume drops—Materion saw sales sensitivity in 2024 with group-wide revenue of about $1.19 billion, amplifying consolidated purchasers’ negotiation power; in upcycles, capacity tightness shifts leverage back to Materion. Frame agreements smooth order timing but do not eliminate cyclicality.

- 2024 revenue: $1.19B

- Consolidated buyers: higher leverage in downcycles

- Upcycle capacity tightness restores pricing power

- Frame agreements reduce but do not remove cyclicality

Concentrated OEM demand and 12-36 month qualification create technical lock-in and premium pricing

Large, concentrated OEMs (semiconductor ~$600B 2024) exert strong price and SLA demands while long 12–36 month qualification cycles and switching costs >$500,000 grant Materion technical lock-in. Co‑engineered materials and SLAs support premium pricing, but downcycles amplify buyer leverage; 2024 revenue was $1.19B.

| Metric | Value |

|---|---|

| Materion 2024 revenue | $1.19B |

| Semiconductor market 2024 | $600B |

| Qualification | 12–36 months |

| Switching cost | >$500,000 |

Preview Before You Purchase

Materion Porter's Five Forces Analysis

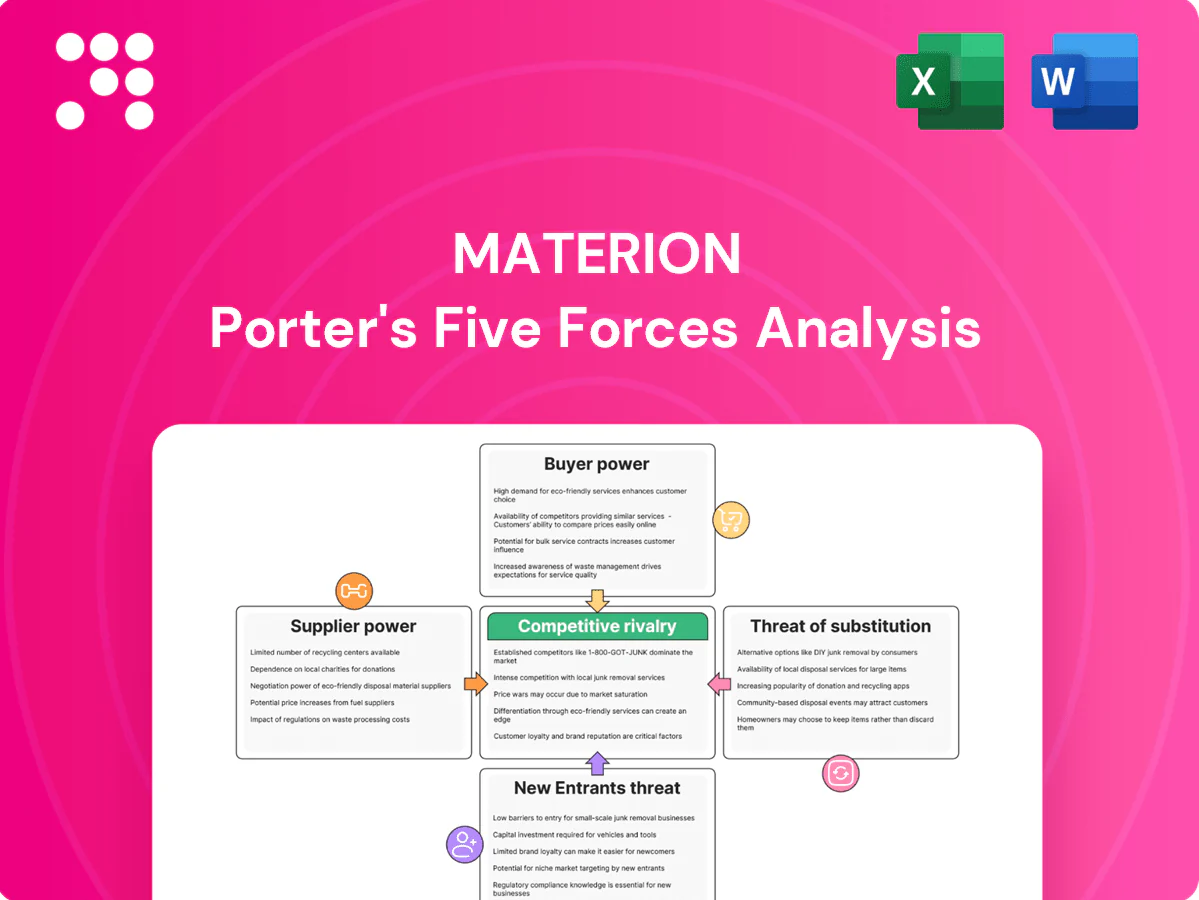

This preview shows the exact Materion Porter's Five Forces analysis you’ll receive after purchase—complete, professionally formatted, and ready to download. It covers supplier power, buyer power, competitive rivalry, threat of substitutes, and threat of new entrants with actionable insights. No placeholders or samples; you get instant access to this exact file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Materion faces intense rivalry and moderate buyer power in specialty materials, with supplier influence driven by scarce raw inputs and a growing threat from substitutes and new entrants in advanced alloys and coatings. This snapshot highlights key tensions but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to explore Materion’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce critical inputs

Many of Materion’s feedstocks—beryllium, high‑purity ceramics and noble metals—are scarce and sourced from a handful of countries (US, China, Kazakhstan), concentrating supplier leverage; Materion reported roughly $1.2B revenue in 2024, so input cost swings materially affect margins. Price volatility and allocation risk can ripple through costs, and supply‑assurance programs and hedging only partially mitigate these shocks.

Regulation and compliance burden

Environmental, health and safety rules for toxic and hard-to-handle inputs notably raise supplier leverage for Materion, since compliance costs and permitting shrink the pool of qualified upstream providers; EU REACH covered over 22,000 registered substances by 2024, increasing traceability burdens. Certification audits and chain-of-custody traceability add switching frictions and time-to-source. Any regulatory tightening quickly amplifies supplier power and dependence.

Backward integration offsets

Materion’s upstream capabilities in select materials such as beryllium—central to its engineered materials portfolio—temper supplier power, underpinning a business that reported about $1.1 billion in net sales in fiscal 2024. Internal processing knowledge and in-house refining reduce reliance on external sources for some high-value inputs. Strategic inventories and dual-sourcing arrangements further mitigate supplier leverage. However, key specialty inputs and rare alloys remain difficult or uneconomic to fully integrate.

Long-term, specialty contracts

Long-term, specialty contracts stabilize Materion supply chains but embed supplier terms through technical specs and custom formulations that increase supplier leverage. Vendor-managed quality and proprietary blends create high switching costs and relational lock-in; renegotiation cycles often shift bargaining power to suppliers in tight markets. Index-linked pricing transmits commodity spikes quickly, compressing margins.

- Multi-year terms: lock-in risk

- Vendor-managed quality: high switching cost

- Renegotiation favors suppliers in tight markets

- Index-linked pricing: rapid commodity pass-through

Processing know-how as counterweight

Materion’s proprietary metallurgical and ceramic processes create bespoke input specs that narrow the pool of viable suppliers, but co-development relationships and shared process IP give Materion leverage—in 2024 the company continued investing in process R&D, keeping supplier options concentrated while using collaboration to negotiate terms.

- Limited supplier pool due to unique inputs

- Co-development yields joint IP and bargaining chips

- 2024 R&D-led collaborations strengthened negotiating position

- Dependence remains where substitutes are scarce

Scarce feedstocks in US/China/Kazakhstan boost supplier power;$1.2B revenue margin-sensitive

Materion faces high supplier power: scarce inputs (beryllium, noble metals) are concentrated in US, China, Kazakhstan while $1.2B revenue in 2024 makes input swings margin‑sensitive. EHS and REACH compliance (22,000+ substances by 2024) raise switching costs. In‑house processing and R&D reduce but do not eliminate dependence; long contracts and index pricing preserve supplier leverage.

| Metric | 2024 |

|---|---|

| Revenue | $1.2B |

| Net sales (reported) | $1.1B |

| Critical feedstock concentration | US, China, Kazakhstan |

| REACH registry | 22,000+ substances |

What is included in the product

Tailored Porter's Five Forces analysis for Materion, uncovering key competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats that shape pricing, profitability and strategic positioning in specialty materials markets.

A concise, one-sheet Materion Porter's Five Forces summary that visualizes competitive pressure, suggests strategic levers for suppliers, buyers, rivals, entrants and substitutes, and is ready to drop into decks or scenario tabs without macros.

Customers Bargaining Power

Concentrated blue-chip OEMs

Concentrated blue-chip OEMs in aerospace, semiconductor, automotive, and medical purchase large volumes from Materion and exert strong negotiating leverage, reflecting the global semiconductor market of roughly $600 billion in 2024 and large aerospace OEM procurement scales. They enforce strict quality, delivery, and aggressive cost-down targets, with supplier scorecards and dual-sourcing keeping margin pressure intense. Volume commitments are commonly traded for price concessions and longer payment terms.

High qualification and switching costs

Materials are tightly specified with qualification cycles commonly 12–36 months, making buyer switching difficult and often incurring switching costs frequently above $500,000, which dampens day-to-day price pressure once approved. Buyers, however, can leverage future program awards to extract concessions. End-use regulatory compliance can further delay substitutions by an additional 6–18 months, reinforcing incumbent advantage.

Customization increases stickiness

Co-engineered alloys and ceramics embed Materion into customer designs, creating technical lock-in that raises switching costs. Tailored specifications and application support increase exit barriers and allow for premium pricing on specialized solutions. However, industry-wide design-to-cost programs and supplier consolidation can pressure margins over time. Ongoing collaboration is needed to defend pricing power and margin durability.

Total cost-of-ownership focus

Buyers prioritize total cost of ownership, valuing reliability, performance and yield impact over unit price; materials that improve device performance or reduce scrap materially weaken buyer leverage. Service-level SLAs and technical support create stickiness and premium pricing power, even as procurement continues to benchmark global alternatives; the global semiconductor market (~600 billion in 2024) heightens sourcing scrutiny.

- Reliability > unit price

- Yield reduction reduces buyer power

- SLAs/tech support add value

- Global benchmarking persists

Cyclical demand bargaining

Downcycles in electronics and aerospace MRO elevate buyer leverage as volume drops—Materion saw sales sensitivity in 2024 with group-wide revenue of about $1.19 billion, amplifying consolidated purchasers’ negotiation power; in upcycles, capacity tightness shifts leverage back to Materion. Frame agreements smooth order timing but do not eliminate cyclicality.

- 2024 revenue: $1.19B

- Consolidated buyers: higher leverage in downcycles

- Upcycle capacity tightness restores pricing power

- Frame agreements reduce but do not remove cyclicality

Concentrated OEM demand and 12-36 month qualification create technical lock-in and premium pricing

Large, concentrated OEMs (semiconductor ~$600B 2024) exert strong price and SLA demands while long 12–36 month qualification cycles and switching costs >$500,000 grant Materion technical lock-in. Co‑engineered materials and SLAs support premium pricing, but downcycles amplify buyer leverage; 2024 revenue was $1.19B.

| Metric | Value |

|---|---|

| Materion 2024 revenue | $1.19B |

| Semiconductor market 2024 | $600B |

| Qualification | 12–36 months |

| Switching cost | >$500,000 |

Preview Before You Purchase

Materion Porter's Five Forces Analysis

This preview shows the exact Materion Porter's Five Forces analysis you’ll receive after purchase—complete, professionally formatted, and ready to download. It covers supplier power, buyer power, competitive rivalry, threat of substitutes, and threat of new entrants with actionable insights. No placeholders or samples; you get instant access to this exact file.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Materion faces intense rivalry and moderate buyer power in specialty materials, with supplier influence driven by scarce raw inputs and a growing threat from substitutes and new entrants in advanced alloys and coatings. This snapshot highlights key tensions but omits force-by-force ratings and strategic implications. Unlock the full Porter's Five Forces Analysis to explore Materion’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Scarce critical inputs

Many of Materion’s feedstocks—beryllium, high‑purity ceramics and noble metals—are scarce and sourced from a handful of countries (US, China, Kazakhstan), concentrating supplier leverage; Materion reported roughly $1.2B revenue in 2024, so input cost swings materially affect margins. Price volatility and allocation risk can ripple through costs, and supply‑assurance programs and hedging only partially mitigate these shocks.

Regulation and compliance burden

Environmental, health and safety rules for toxic and hard-to-handle inputs notably raise supplier leverage for Materion, since compliance costs and permitting shrink the pool of qualified upstream providers; EU REACH covered over 22,000 registered substances by 2024, increasing traceability burdens. Certification audits and chain-of-custody traceability add switching frictions and time-to-source. Any regulatory tightening quickly amplifies supplier power and dependence.

Backward integration offsets

Materion’s upstream capabilities in select materials such as beryllium—central to its engineered materials portfolio—temper supplier power, underpinning a business that reported about $1.1 billion in net sales in fiscal 2024. Internal processing knowledge and in-house refining reduce reliance on external sources for some high-value inputs. Strategic inventories and dual-sourcing arrangements further mitigate supplier leverage. However, key specialty inputs and rare alloys remain difficult or uneconomic to fully integrate.

Long-term, specialty contracts

Long-term, specialty contracts stabilize Materion supply chains but embed supplier terms through technical specs and custom formulations that increase supplier leverage. Vendor-managed quality and proprietary blends create high switching costs and relational lock-in; renegotiation cycles often shift bargaining power to suppliers in tight markets. Index-linked pricing transmits commodity spikes quickly, compressing margins.

- Multi-year terms: lock-in risk

- Vendor-managed quality: high switching cost

- Renegotiation favors suppliers in tight markets

- Index-linked pricing: rapid commodity pass-through

Processing know-how as counterweight

Materion’s proprietary metallurgical and ceramic processes create bespoke input specs that narrow the pool of viable suppliers, but co-development relationships and shared process IP give Materion leverage—in 2024 the company continued investing in process R&D, keeping supplier options concentrated while using collaboration to negotiate terms.

- Limited supplier pool due to unique inputs

- Co-development yields joint IP and bargaining chips

- 2024 R&D-led collaborations strengthened negotiating position

- Dependence remains where substitutes are scarce

Scarce feedstocks in US/China/Kazakhstan boost supplier power;$1.2B revenue margin-sensitive

Materion faces high supplier power: scarce inputs (beryllium, noble metals) are concentrated in US, China, Kazakhstan while $1.2B revenue in 2024 makes input swings margin‑sensitive. EHS and REACH compliance (22,000+ substances by 2024) raise switching costs. In‑house processing and R&D reduce but do not eliminate dependence; long contracts and index pricing preserve supplier leverage.

| Metric | 2024 |

|---|---|

| Revenue | $1.2B |

| Net sales (reported) | $1.1B |

| Critical feedstock concentration | US, China, Kazakhstan |

| REACH registry | 22,000+ substances |

What is included in the product

Tailored Porter's Five Forces analysis for Materion, uncovering key competitive drivers, supplier and buyer power, entry barriers, substitutes and disruptive threats that shape pricing, profitability and strategic positioning in specialty materials markets.

A concise, one-sheet Materion Porter's Five Forces summary that visualizes competitive pressure, suggests strategic levers for suppliers, buyers, rivals, entrants and substitutes, and is ready to drop into decks or scenario tabs without macros.

Customers Bargaining Power

Concentrated blue-chip OEMs

Concentrated blue-chip OEMs in aerospace, semiconductor, automotive, and medical purchase large volumes from Materion and exert strong negotiating leverage, reflecting the global semiconductor market of roughly $600 billion in 2024 and large aerospace OEM procurement scales. They enforce strict quality, delivery, and aggressive cost-down targets, with supplier scorecards and dual-sourcing keeping margin pressure intense. Volume commitments are commonly traded for price concessions and longer payment terms.

High qualification and switching costs

Materials are tightly specified with qualification cycles commonly 12–36 months, making buyer switching difficult and often incurring switching costs frequently above $500,000, which dampens day-to-day price pressure once approved. Buyers, however, can leverage future program awards to extract concessions. End-use regulatory compliance can further delay substitutions by an additional 6–18 months, reinforcing incumbent advantage.

Customization increases stickiness

Co-engineered alloys and ceramics embed Materion into customer designs, creating technical lock-in that raises switching costs. Tailored specifications and application support increase exit barriers and allow for premium pricing on specialized solutions. However, industry-wide design-to-cost programs and supplier consolidation can pressure margins over time. Ongoing collaboration is needed to defend pricing power and margin durability.

Total cost-of-ownership focus

Buyers prioritize total cost of ownership, valuing reliability, performance and yield impact over unit price; materials that improve device performance or reduce scrap materially weaken buyer leverage. Service-level SLAs and technical support create stickiness and premium pricing power, even as procurement continues to benchmark global alternatives; the global semiconductor market (~600 billion in 2024) heightens sourcing scrutiny.

- Reliability > unit price

- Yield reduction reduces buyer power

- SLAs/tech support add value

- Global benchmarking persists

Cyclical demand bargaining

Downcycles in electronics and aerospace MRO elevate buyer leverage as volume drops—Materion saw sales sensitivity in 2024 with group-wide revenue of about $1.19 billion, amplifying consolidated purchasers’ negotiation power; in upcycles, capacity tightness shifts leverage back to Materion. Frame agreements smooth order timing but do not eliminate cyclicality.

- 2024 revenue: $1.19B

- Consolidated buyers: higher leverage in downcycles

- Upcycle capacity tightness restores pricing power

- Frame agreements reduce but do not remove cyclicality

Concentrated OEM demand and 12-36 month qualification create technical lock-in and premium pricing

Large, concentrated OEMs (semiconductor ~$600B 2024) exert strong price and SLA demands while long 12–36 month qualification cycles and switching costs >$500,000 grant Materion technical lock-in. Co‑engineered materials and SLAs support premium pricing, but downcycles amplify buyer leverage; 2024 revenue was $1.19B.

| Metric | Value |

|---|---|

| Materion 2024 revenue | $1.19B |

| Semiconductor market 2024 | $600B |

| Qualification | 12–36 months |

| Switching cost | >$500,000 |

Preview Before You Purchase

Materion Porter's Five Forces Analysis

This preview shows the exact Materion Porter's Five Forces analysis you’ll receive after purchase—complete, professionally formatted, and ready to download. It covers supplier power, buyer power, competitive rivalry, threat of substitutes, and threat of new entrants with actionable insights. No placeholders or samples; you get instant access to this exact file.