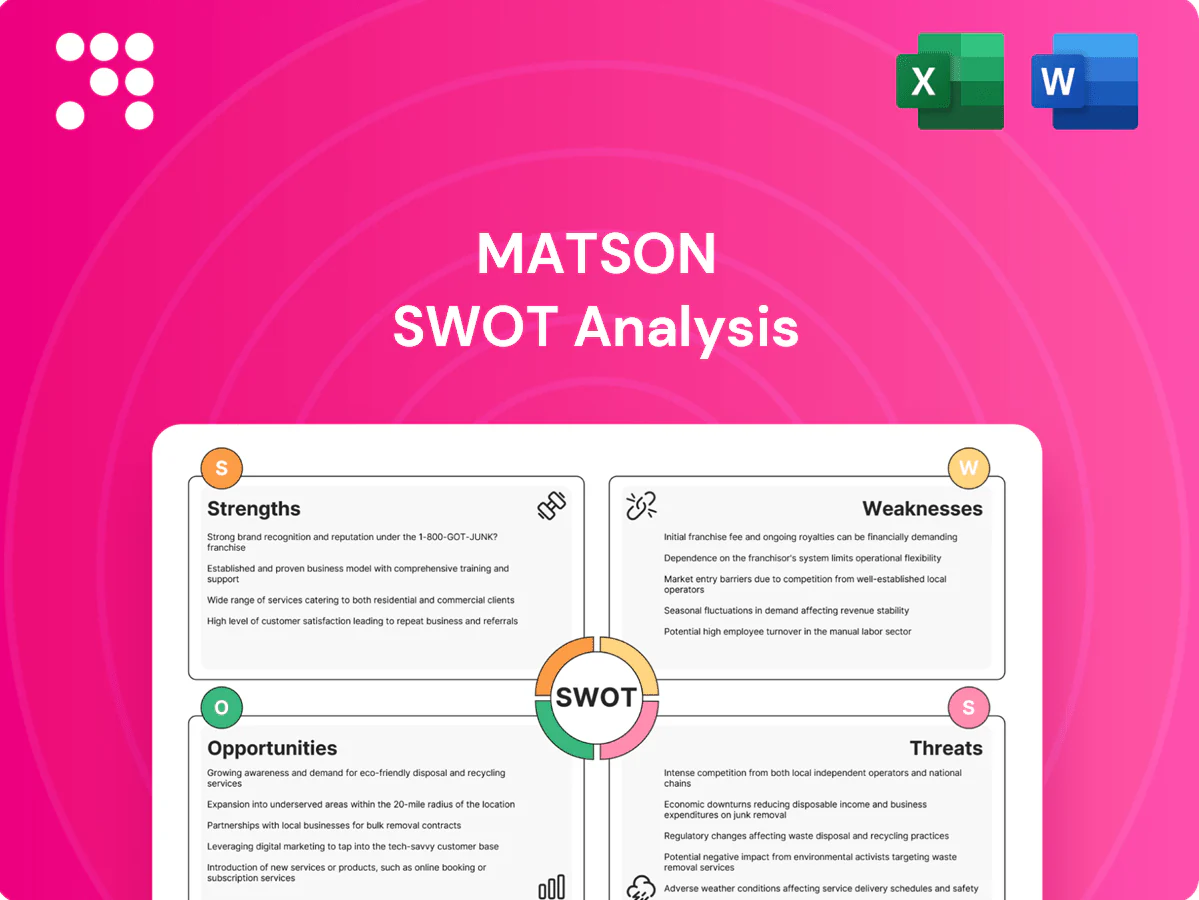

Matson SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Our Matson SWOT Analysis highlights the company’s strengths in niche Pacific routes and integrated logistics, while exposing operational risks, competitive pressures, and growth opportunities in offshore services. This snapshot guides investor and strategist thinking but omits detailed financial context and tactical recommendations. Purchase the full SWOT for a research-backed, editable Word and Excel package with deep analysis and action-ready insights.

Strengths

Jones Act market leadership

Matson is the leading U.S. liner to Hawaii and a major Alaska carrier, leveraging Jones Act protection (1920) to sustain stable demand, pricing power and high service stickiness; its scale—reflected in roughly $2.0B revenue in 2024—cuts unit costs and boosts schedule reliability, deterring new entrants.

Integrated ocean-logistics network

Matson pairs ocean transportation with logistics services to offer end-to-end solutions; in 2023 the company reported $2.6 billion in revenue with logistics and intermodal services contributing roughly 30% of total revenue, enhancing cross-sell opportunities and wallet share. Customers gain single-provider coordination and improved cargo visibility, reducing exceptions and enabling faster problem resolution. This integrated model boosts retention and supports yield management, helping preserve adjusted operating margins amid rate volatility.

Premium, time-definite service

Matson (NYSE: MATX) commands premium, time-definite trans-Pacific service that supports higher yields; 2024 revenue reached about $2.92 billion, underscoring sustained demand for fast sailings. Time-sensitive shippers consistently pay for reliability over lowest cost, keeping Matson less exposed to spot-rate volatility. High service quality differentiates Matson from commoditized carriers and bolsters brand equity and defensible pricing.

Strategic Pacific footprint

Matson operates dedicated routes linking Hawaii, Alaska, Guam and Micronesia to the U.S. mainland and select international ports, underpinning essential freight flows for island economies. The network secures steady U.S. military, consumer and construction cargo, while deep local market know-how improves schedule reliability and on‑ground execution.

- Strategic Pacific coverage

- Essential island freight lifeline

- Stable military and commercial demand

Asset base and operational expertise

Matson's owned and chartered vessels, terminals and equipment provide tight service control, while long-standing port relationships and deep labor experience help minimize disruptions; mature safety and compliance systems (ISM-compliant) and strong operational discipline support on-time sailings and cost management.

- Owned and chartered assets

- Established port/labor ties

- ISM-compliant safety systems

- Operational discipline

Jones Act carrier secures pricing power via Hawaii/Alaska lanes and integrated ocean-logistics model

Matson leverages Jones Act protection and leading Hawaii/Alaska routes to sustain pricing power, stable demand and high service stickiness. Its integrated ocean+logistics model (logistics ~30% of revenue) raises wallet share and supports margins. Premium time-definite trans-Pacific service and owned/chartered assets drive reliability and deterrence to entrants.

| Metric | Value |

|---|---|

| 2024 revenue | $2.92B |

| 2023 revenue | $2.6B |

| Logistics share | ~30% |

What is included in the product

Provides a concise SWOT analysis of Matson, highlighting its operational strengths, financial and fleet advantages, internal weaknesses, and external opportunities and threats shaping its competitive maritime logistics position.

Provides a concise Matson SWOT matrix to quickly surface port strengths, fleet risks, and market opportunities, relieving strategic alignment bottlenecks for faster decision-making.

Weaknesses

Geographic concentration

Matson's revenue is heavily concentrated on Pacific island economies and related U.S. lanes, with the company remaining the largest U.S. carrier to Hawaii; local economic swings can therefore disproportionately reduce container volumes. Demand is cyclical and tied to tourism, construction activity and population trends, making earnings sensitive to those sectors. Regulatory constraints and required network fit limit easy geographic diversification, constraining growth options.

Fuel cost exposure

Matson remains highly exposed to marine fuel volatility, with bunker prices closely tracking Brent (Brent averaged about $85/barrel in 2024), which can squeeze margins between surcharge resets. Hedging and fuel surcharges historically offset only a portion of sudden spikes, leaving short-term margin leakage. Fuel-efficiency gains from vessel upgrades require multi-year timelines and significant capex. Prolonged high fuel costs risk eroding Matson’s price competitiveness on key Pacific trades.

Capital-intensive operations

Matson's fleet, container, and terminal investments require large cash outlays, with the company targeting roughly $500–700 million in annual capex in the 2023–25 period for new ships, containers, and terminal upgrades. Ship replacement cycles create lumpy capex and financing needs as vessels cost hundreds of millions each and multiyear newbuild schedules concentrate spending. Returns hinge on maintaining high utilization—lower utilization quickly erodes margins—and leverage metrics can worsen in downturns, tightening balance-sheet flexibility.

Labor and union dependency

Operations depend on skilled, unionized labor at key West Coast and island ports, making Matson vulnerable to contract negotiations that can raise costs or trigger slowdowns. Labor shortages force higher overtime and training expenses, degrading margin and operational flexibility. Even localized labor disputes can cascade into schedule disruptions and customer-service failures.

- Union dependency

- Higher labor costs

- Overtime & training strain

- Schedule disruption risk

Environmental compliance burden

Stricter emissions and waste regulations raise Matson’s operating costs through higher fuel bills and retrofit expenses, pressuring margins and cash flow. Compliance requires capital investment in newer dual-fuel vessels and alternative fuels, lengthening payback periods. Expanded reporting and audit requirements add administrative complexity and non-compliance risks of fines and reputational damage.

- Higher operating costs

- Capex for cleaner vessels/fuels

- Increased reporting burden

- Fines and reputational risk

Pacific revenue concentration, fuel and capex pressures threaten margins and leverage

High revenue concentration in Pacific/U.S. island lanes leaves volumes sensitive to local demand swings.

Strong exposure to bunker costs; Brent averaged about $85/barrel in 2024, pressuring margins between surcharge resets.

Large, lumpy capex needs—targeting roughly $500–700 million annually in 2023–25—strain cash flow and leverage in downturns.

Unionized labor and tightening emissions rules raise operating costs and operational disruption risk.

| Weakness | Impact | Metric |

|---|---|---|

| Concentration | Volume sensitivity | Pacific lanes share |

| Fuel | Margin pressure | Brent $85/2024 |

| Capex | Cash & leverage | $500–700M/yr (2023–25) |

| Labor/Reg | Cost & disruption | Unionized ports |

Full Version Awaits

Matson SWOT Analysis

This is the actual Matson SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report and reflects the structure and depth of the complete file. Buy now to unlock the full, editable version for immediate download.

Elevate Your Analysis with the Complete SWOT Report

Our Matson SWOT Analysis highlights the company’s strengths in niche Pacific routes and integrated logistics, while exposing operational risks, competitive pressures, and growth opportunities in offshore services. This snapshot guides investor and strategist thinking but omits detailed financial context and tactical recommendations. Purchase the full SWOT for a research-backed, editable Word and Excel package with deep analysis and action-ready insights.

Strengths

Jones Act market leadership

Matson is the leading U.S. liner to Hawaii and a major Alaska carrier, leveraging Jones Act protection (1920) to sustain stable demand, pricing power and high service stickiness; its scale—reflected in roughly $2.0B revenue in 2024—cuts unit costs and boosts schedule reliability, deterring new entrants.

Integrated ocean-logistics network

Matson pairs ocean transportation with logistics services to offer end-to-end solutions; in 2023 the company reported $2.6 billion in revenue with logistics and intermodal services contributing roughly 30% of total revenue, enhancing cross-sell opportunities and wallet share. Customers gain single-provider coordination and improved cargo visibility, reducing exceptions and enabling faster problem resolution. This integrated model boosts retention and supports yield management, helping preserve adjusted operating margins amid rate volatility.

Premium, time-definite service

Matson (NYSE: MATX) commands premium, time-definite trans-Pacific service that supports higher yields; 2024 revenue reached about $2.92 billion, underscoring sustained demand for fast sailings. Time-sensitive shippers consistently pay for reliability over lowest cost, keeping Matson less exposed to spot-rate volatility. High service quality differentiates Matson from commoditized carriers and bolsters brand equity and defensible pricing.

Strategic Pacific footprint

Matson operates dedicated routes linking Hawaii, Alaska, Guam and Micronesia to the U.S. mainland and select international ports, underpinning essential freight flows for island economies. The network secures steady U.S. military, consumer and construction cargo, while deep local market know-how improves schedule reliability and on‑ground execution.

- Strategic Pacific coverage

- Essential island freight lifeline

- Stable military and commercial demand

Asset base and operational expertise

Matson's owned and chartered vessels, terminals and equipment provide tight service control, while long-standing port relationships and deep labor experience help minimize disruptions; mature safety and compliance systems (ISM-compliant) and strong operational discipline support on-time sailings and cost management.

- Owned and chartered assets

- Established port/labor ties

- ISM-compliant safety systems

- Operational discipline

Jones Act carrier secures pricing power via Hawaii/Alaska lanes and integrated ocean-logistics model

Matson leverages Jones Act protection and leading Hawaii/Alaska routes to sustain pricing power, stable demand and high service stickiness. Its integrated ocean+logistics model (logistics ~30% of revenue) raises wallet share and supports margins. Premium time-definite trans-Pacific service and owned/chartered assets drive reliability and deterrence to entrants.

| Metric | Value |

|---|---|

| 2024 revenue | $2.92B |

| 2023 revenue | $2.6B |

| Logistics share | ~30% |

What is included in the product

Provides a concise SWOT analysis of Matson, highlighting its operational strengths, financial and fleet advantages, internal weaknesses, and external opportunities and threats shaping its competitive maritime logistics position.

Provides a concise Matson SWOT matrix to quickly surface port strengths, fleet risks, and market opportunities, relieving strategic alignment bottlenecks for faster decision-making.

Weaknesses

Geographic concentration

Matson's revenue is heavily concentrated on Pacific island economies and related U.S. lanes, with the company remaining the largest U.S. carrier to Hawaii; local economic swings can therefore disproportionately reduce container volumes. Demand is cyclical and tied to tourism, construction activity and population trends, making earnings sensitive to those sectors. Regulatory constraints and required network fit limit easy geographic diversification, constraining growth options.

Fuel cost exposure

Matson remains highly exposed to marine fuel volatility, with bunker prices closely tracking Brent (Brent averaged about $85/barrel in 2024), which can squeeze margins between surcharge resets. Hedging and fuel surcharges historically offset only a portion of sudden spikes, leaving short-term margin leakage. Fuel-efficiency gains from vessel upgrades require multi-year timelines and significant capex. Prolonged high fuel costs risk eroding Matson’s price competitiveness on key Pacific trades.

Capital-intensive operations

Matson's fleet, container, and terminal investments require large cash outlays, with the company targeting roughly $500–700 million in annual capex in the 2023–25 period for new ships, containers, and terminal upgrades. Ship replacement cycles create lumpy capex and financing needs as vessels cost hundreds of millions each and multiyear newbuild schedules concentrate spending. Returns hinge on maintaining high utilization—lower utilization quickly erodes margins—and leverage metrics can worsen in downturns, tightening balance-sheet flexibility.

Labor and union dependency

Operations depend on skilled, unionized labor at key West Coast and island ports, making Matson vulnerable to contract negotiations that can raise costs or trigger slowdowns. Labor shortages force higher overtime and training expenses, degrading margin and operational flexibility. Even localized labor disputes can cascade into schedule disruptions and customer-service failures.

- Union dependency

- Higher labor costs

- Overtime & training strain

- Schedule disruption risk

Environmental compliance burden

Stricter emissions and waste regulations raise Matson’s operating costs through higher fuel bills and retrofit expenses, pressuring margins and cash flow. Compliance requires capital investment in newer dual-fuel vessels and alternative fuels, lengthening payback periods. Expanded reporting and audit requirements add administrative complexity and non-compliance risks of fines and reputational damage.

- Higher operating costs

- Capex for cleaner vessels/fuels

- Increased reporting burden

- Fines and reputational risk

Pacific revenue concentration, fuel and capex pressures threaten margins and leverage

High revenue concentration in Pacific/U.S. island lanes leaves volumes sensitive to local demand swings.

Strong exposure to bunker costs; Brent averaged about $85/barrel in 2024, pressuring margins between surcharge resets.

Large, lumpy capex needs—targeting roughly $500–700 million annually in 2023–25—strain cash flow and leverage in downturns.

Unionized labor and tightening emissions rules raise operating costs and operational disruption risk.

| Weakness | Impact | Metric |

|---|---|---|

| Concentration | Volume sensitivity | Pacific lanes share |

| Fuel | Margin pressure | Brent $85/2024 |

| Capex | Cash & leverage | $500–700M/yr (2023–25) |

| Labor/Reg | Cost & disruption | Unionized ports |

Full Version Awaits

Matson SWOT Analysis

This is the actual Matson SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report and reflects the structure and depth of the complete file. Buy now to unlock the full, editable version for immediate download.

Description

Elevate Your Analysis with the Complete SWOT Report

Our Matson SWOT Analysis highlights the company’s strengths in niche Pacific routes and integrated logistics, while exposing operational risks, competitive pressures, and growth opportunities in offshore services. This snapshot guides investor and strategist thinking but omits detailed financial context and tactical recommendations. Purchase the full SWOT for a research-backed, editable Word and Excel package with deep analysis and action-ready insights.

Strengths

Jones Act market leadership

Matson is the leading U.S. liner to Hawaii and a major Alaska carrier, leveraging Jones Act protection (1920) to sustain stable demand, pricing power and high service stickiness; its scale—reflected in roughly $2.0B revenue in 2024—cuts unit costs and boosts schedule reliability, deterring new entrants.

Integrated ocean-logistics network

Matson pairs ocean transportation with logistics services to offer end-to-end solutions; in 2023 the company reported $2.6 billion in revenue with logistics and intermodal services contributing roughly 30% of total revenue, enhancing cross-sell opportunities and wallet share. Customers gain single-provider coordination and improved cargo visibility, reducing exceptions and enabling faster problem resolution. This integrated model boosts retention and supports yield management, helping preserve adjusted operating margins amid rate volatility.

Premium, time-definite service

Matson (NYSE: MATX) commands premium, time-definite trans-Pacific service that supports higher yields; 2024 revenue reached about $2.92 billion, underscoring sustained demand for fast sailings. Time-sensitive shippers consistently pay for reliability over lowest cost, keeping Matson less exposed to spot-rate volatility. High service quality differentiates Matson from commoditized carriers and bolsters brand equity and defensible pricing.

Strategic Pacific footprint

Matson operates dedicated routes linking Hawaii, Alaska, Guam and Micronesia to the U.S. mainland and select international ports, underpinning essential freight flows for island economies. The network secures steady U.S. military, consumer and construction cargo, while deep local market know-how improves schedule reliability and on‑ground execution.

- Strategic Pacific coverage

- Essential island freight lifeline

- Stable military and commercial demand

Asset base and operational expertise

Matson's owned and chartered vessels, terminals and equipment provide tight service control, while long-standing port relationships and deep labor experience help minimize disruptions; mature safety and compliance systems (ISM-compliant) and strong operational discipline support on-time sailings and cost management.

- Owned and chartered assets

- Established port/labor ties

- ISM-compliant safety systems

- Operational discipline

Jones Act carrier secures pricing power via Hawaii/Alaska lanes and integrated ocean-logistics model

Matson leverages Jones Act protection and leading Hawaii/Alaska routes to sustain pricing power, stable demand and high service stickiness. Its integrated ocean+logistics model (logistics ~30% of revenue) raises wallet share and supports margins. Premium time-definite trans-Pacific service and owned/chartered assets drive reliability and deterrence to entrants.

| Metric | Value |

|---|---|

| 2024 revenue | $2.92B |

| 2023 revenue | $2.6B |

| Logistics share | ~30% |

What is included in the product

Provides a concise SWOT analysis of Matson, highlighting its operational strengths, financial and fleet advantages, internal weaknesses, and external opportunities and threats shaping its competitive maritime logistics position.

Provides a concise Matson SWOT matrix to quickly surface port strengths, fleet risks, and market opportunities, relieving strategic alignment bottlenecks for faster decision-making.

Weaknesses

Geographic concentration

Matson's revenue is heavily concentrated on Pacific island economies and related U.S. lanes, with the company remaining the largest U.S. carrier to Hawaii; local economic swings can therefore disproportionately reduce container volumes. Demand is cyclical and tied to tourism, construction activity and population trends, making earnings sensitive to those sectors. Regulatory constraints and required network fit limit easy geographic diversification, constraining growth options.

Fuel cost exposure

Matson remains highly exposed to marine fuel volatility, with bunker prices closely tracking Brent (Brent averaged about $85/barrel in 2024), which can squeeze margins between surcharge resets. Hedging and fuel surcharges historically offset only a portion of sudden spikes, leaving short-term margin leakage. Fuel-efficiency gains from vessel upgrades require multi-year timelines and significant capex. Prolonged high fuel costs risk eroding Matson’s price competitiveness on key Pacific trades.

Capital-intensive operations

Matson's fleet, container, and terminal investments require large cash outlays, with the company targeting roughly $500–700 million in annual capex in the 2023–25 period for new ships, containers, and terminal upgrades. Ship replacement cycles create lumpy capex and financing needs as vessels cost hundreds of millions each and multiyear newbuild schedules concentrate spending. Returns hinge on maintaining high utilization—lower utilization quickly erodes margins—and leverage metrics can worsen in downturns, tightening balance-sheet flexibility.

Labor and union dependency

Operations depend on skilled, unionized labor at key West Coast and island ports, making Matson vulnerable to contract negotiations that can raise costs or trigger slowdowns. Labor shortages force higher overtime and training expenses, degrading margin and operational flexibility. Even localized labor disputes can cascade into schedule disruptions and customer-service failures.

- Union dependency

- Higher labor costs

- Overtime & training strain

- Schedule disruption risk

Environmental compliance burden

Stricter emissions and waste regulations raise Matson’s operating costs through higher fuel bills and retrofit expenses, pressuring margins and cash flow. Compliance requires capital investment in newer dual-fuel vessels and alternative fuels, lengthening payback periods. Expanded reporting and audit requirements add administrative complexity and non-compliance risks of fines and reputational damage.

- Higher operating costs

- Capex for cleaner vessels/fuels

- Increased reporting burden

- Fines and reputational risk

Pacific revenue concentration, fuel and capex pressures threaten margins and leverage

High revenue concentration in Pacific/U.S. island lanes leaves volumes sensitive to local demand swings.

Strong exposure to bunker costs; Brent averaged about $85/barrel in 2024, pressuring margins between surcharge resets.

Large, lumpy capex needs—targeting roughly $500–700 million annually in 2023–25—strain cash flow and leverage in downturns.

Unionized labor and tightening emissions rules raise operating costs and operational disruption risk.

| Weakness | Impact | Metric |

|---|---|---|

| Concentration | Volume sensitivity | Pacific lanes share |

| Fuel | Margin pressure | Brent $85/2024 |

| Capex | Cash & leverage | $500–700M/yr (2023–25) |

| Labor/Reg | Cost & disruption | Unionized ports |

Full Version Awaits

Matson SWOT Analysis

This is the actual Matson SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is pulled directly from the full report and reflects the structure and depth of the complete file. Buy now to unlock the full, editable version for immediate download.