Mattel Porter's Five Forces Analysis

From Overview to Strategy Blueprint

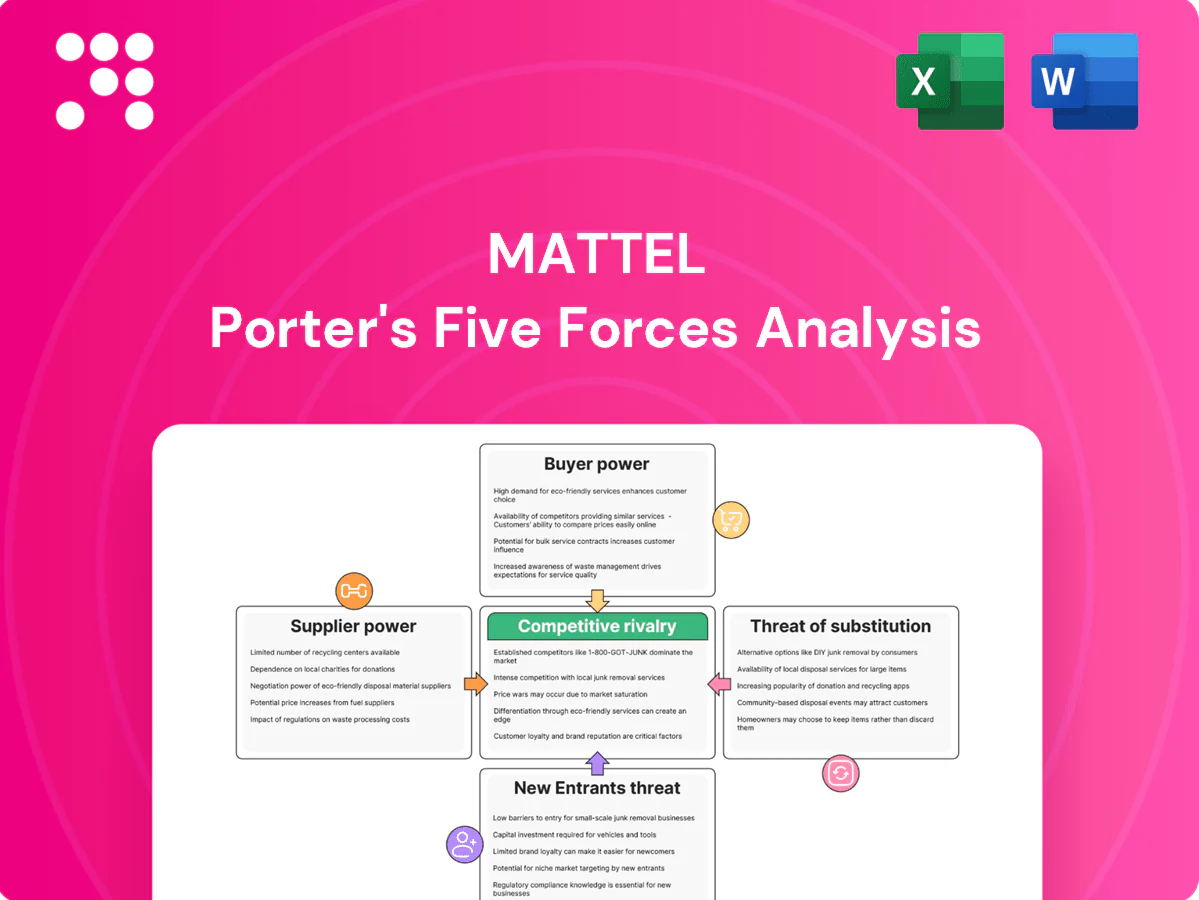

Mattel faces intense rivalry from diversified toy and entertainment players, shifting buyer preferences, rising substitute digital entertainment, moderate supplier leverage, and barriers that moderate new entrants. This snapshot highlights key pressures on margins and growth. The full Porter's Five Forces Analysis delivers force-by-force ratings, visuals, and strategic implications to guide investment or strategy decisions—unlock it now.

Suppliers Bargaining Power

Global plastics and components

Mattel relies on polymers, die-cast metals and electronic modules sourced largely from Asia (≈60–80% of manufacturing footprint), concentrating exposure in Southeast and East Asia. Commodity price volatility for resins and metals can swing margins—price moves of 10–20%+ annually have been observed in recent cycles—if not hedged or under long-term contracts. Mattel’s scale enables multi-sourcing and volume discounts that lower unit costs. Tight specs and rigorous quality controls limit feasible supplier substitutes, moderately elevating supplier power.

Contract manufacturing concentration

Production is concentrated among a limited set of qualified contract manufacturers holding international toy-safety certifications (e.g., ISO, EN71) primarily in Asia, creating moderate supplier leverage. Switching is feasible but costly due to tooling replacement, factory audits, and lead-time risks that can delay seasonal launches. Mattel reduces dependence through dual-sourcing and geographic diversification across China, Vietnam, and Indonesia.

Licensing/content partners as “suppliers”

Mattel treats licensors and content partners as quasi-suppliers of brand equity; hit IP owners can command higher royalties and exclusivity, pressuring margins. Mattel’s owned franchises—Barbie, Hot Wheels, Fisher‑Price—provide countervailing leverage, with branded portfolio strength used to negotiate balanced terms. Negotiating across multiple brands helps normalize royalty rates and exclusivity tradeoffs for 2024 collaborations.

Compliance and ESG requirements

- Compliance limits supplier pool

- Approved vendors leverage investment

- Preferred programs temper pricing

- Audits/traceability cut opportunism

Logistics and geopolitics exposure

Ocean freight capacity swings, port congestion and geopolitical shifts can amplify supplier leverage by creating bottlenecks; container rates fell from pandemic peaks above USD 10,000 per FEU to near pre‑pandemic levels by 2024, but congestion still adds weeks to some lanes.

Suppliers near ports or with flexible logistics gain bargaining power during disruptions; Mattel mitigates risk with diversified lanes, inventory planning and expanding nearshoring options to strengthen negotiation leverage.

Asia sourcing 60–80% concentrates supplier power amid 10–20%+ commodity swings

Mattel sources 60–80% of manufacturing in Asia, concentrating supplier exposure; resin/metal costs have swung 10–20%+ annually in recent cycles, pressuring margins. Certified contract manufacturers and compliance needs raise switching costs, giving approved suppliers moderate leverage, while Mattel’s scale, preferred-vendor agreements and geographic diversification (China, Vietnam, Indonesia) temper supplier power. Ocean freight peaked >USD 10,000/FEU in 2021 and normalized toward 2024, easing logistics pressure.

| Metric | 2024 Value/Note |

|---|---|

| Asia manufacturing footprint | 60–80% |

| Commodity price volatility | 10–20%+ annual swings |

| Container rates peak | >USD 10,000/FEU (2021) → near pre‑pandemic by 2024 |

What is included in the product

Concise Porter's Five Forces analysis for Mattel evaluating competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers that affect pricing, margins, and long-term market positioning.

A concise one-sheet Porter's Five Forces for Mattel that pinpoints supplier, buyer, rivalry, entrant and substitute pressures—ideal for quick strategic decisions; customizable force levels and radar visualization require no macros and drop straight into decks or reports.

Customers Bargaining Power

Retail giants’ negotiating clout

Mass retailers and e-commerce platforms concentrate demand—Amazon held roughly 38% of US e-commerce sales in 2024—so Walmart, Target and Amazon exert strong pressure on pricing, co-op marketing, terms and shelf placement. Failure to meet sell-through targets can trigger delisting or reduced assortment. Mattel counters by leveraging must-have IP (Barbie, Hot Wheels) and retailer-exclusive SKUs to protect shelf space and margins.

Low switching costs for consumers

Parents and gift-givers can easily trade among toy brands and categories, keeping buyer power high as price promotions and trending IP (e.g., movie tie-ins) rapidly shift demand; Mattel reported roughly $6.2 billion in 2024 net sales, underscoring heavy reliance on hit lines. Low switching costs mean deals and trends move volume quickly, though brand affinity and collectibles for Barbie and Hot Wheels raise stickiness for flagship lines.

Seasonality and promotional intensity

Q4 drives a disproportionate share of industry sales, roughly 35–40% of annual toy revenue per NPD (2024), heightening retailer leverage to demand heavy promotions and slotting, which compress margins. Slotting fees and promotional intensity force Mattel to defend pricing, so it uses advanced demand forecasting and tiered assortments to optimize mix. Early orders and pre‑sales data cut last‑minute concessions and lower markdown risk.

Direct-to-consumer and digital channels

Direct-to-consumer and specialty channels give Mattel alternative routes that dilute retailer bargaining by shifting some sales away from big-box partners; global e-commerce reached about 25% of retail sales in 2024 (eMarketer), supporting DTC growth.

First-party data and customization bolster pricing resilience, but DTC volumes remain a minority versus major retailers; omnichannel execution lets Mattel balance reach and margin control.

- Retailer dependence: reduced

- Global e‑commerce 2024: ~25%

- First‑party data: improves pricing

- DTC scale: still smaller than big‑box

- Omnichannel: tradeoff reach vs margin

Licensing and co-branded expectations

Retailers demand fresh content tie-ins and eventized launches; failure to deliver newness weakens Mattel’s negotiation leverage with major chains.

Mattel’s media pipeline and partnerships — highlighted by the Barbie franchise that helped drive a $1.4 billion global box office for the 2023 film — sustain retail excitement and shelf prominence.

Timed exclusives and limited editions increase scarcity and bargaining stance, enabling higher margins and preferential retailer placement.

- Retailer expectations: fresh tie-ins, event launches

- Media leverage: Barbie $1.4B global box office

- Negotiation tools: timed exclusives, limited editions

Mass retailers and Q4 seasonality give buyers leverage; IP, DTC and exclusives defend sales

Mass retailers (Amazon ~38% US e‑commerce 2024) and Q4 seasonality (35–40% of annual toy revenue, NPD 2024) give buyers strong leverage on price, slots and promos. Mattel ($6.2B net sales 2024) defends via must‑have IP (Barbie $1.4B box office 2023), DTC/e‑commerce (~25% global retail 2024) and exclusives.

| Metric | Value |

|---|---|

| Amazon share (US e‑comm) | ~38% (2024) |

| Mattel net sales | $6.2B (2024) |

| Q4 share (toys) | 35–40% (NPD 2024) |

| Global e‑commerce | ~25% (2024) |

Same Document Delivered

Mattel Porter's Five Forces Analysis

This preview shows the exact Mattel Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The final document is professionally formatted and covers competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes. You'll get instant access to this ready-to-use file for analysis and decision-making.

From Overview to Strategy Blueprint

Mattel faces intense rivalry from diversified toy and entertainment players, shifting buyer preferences, rising substitute digital entertainment, moderate supplier leverage, and barriers that moderate new entrants. This snapshot highlights key pressures on margins and growth. The full Porter's Five Forces Analysis delivers force-by-force ratings, visuals, and strategic implications to guide investment or strategy decisions—unlock it now.

Suppliers Bargaining Power

Global plastics and components

Mattel relies on polymers, die-cast metals and electronic modules sourced largely from Asia (≈60–80% of manufacturing footprint), concentrating exposure in Southeast and East Asia. Commodity price volatility for resins and metals can swing margins—price moves of 10–20%+ annually have been observed in recent cycles—if not hedged or under long-term contracts. Mattel’s scale enables multi-sourcing and volume discounts that lower unit costs. Tight specs and rigorous quality controls limit feasible supplier substitutes, moderately elevating supplier power.

Contract manufacturing concentration

Production is concentrated among a limited set of qualified contract manufacturers holding international toy-safety certifications (e.g., ISO, EN71) primarily in Asia, creating moderate supplier leverage. Switching is feasible but costly due to tooling replacement, factory audits, and lead-time risks that can delay seasonal launches. Mattel reduces dependence through dual-sourcing and geographic diversification across China, Vietnam, and Indonesia.

Licensing/content partners as “suppliers”

Mattel treats licensors and content partners as quasi-suppliers of brand equity; hit IP owners can command higher royalties and exclusivity, pressuring margins. Mattel’s owned franchises—Barbie, Hot Wheels, Fisher‑Price—provide countervailing leverage, with branded portfolio strength used to negotiate balanced terms. Negotiating across multiple brands helps normalize royalty rates and exclusivity tradeoffs for 2024 collaborations.

Compliance and ESG requirements

- Compliance limits supplier pool

- Approved vendors leverage investment

- Preferred programs temper pricing

- Audits/traceability cut opportunism

Logistics and geopolitics exposure

Ocean freight capacity swings, port congestion and geopolitical shifts can amplify supplier leverage by creating bottlenecks; container rates fell from pandemic peaks above USD 10,000 per FEU to near pre‑pandemic levels by 2024, but congestion still adds weeks to some lanes.

Suppliers near ports or with flexible logistics gain bargaining power during disruptions; Mattel mitigates risk with diversified lanes, inventory planning and expanding nearshoring options to strengthen negotiation leverage.

Asia sourcing 60–80% concentrates supplier power amid 10–20%+ commodity swings

Mattel sources 60–80% of manufacturing in Asia, concentrating supplier exposure; resin/metal costs have swung 10–20%+ annually in recent cycles, pressuring margins. Certified contract manufacturers and compliance needs raise switching costs, giving approved suppliers moderate leverage, while Mattel’s scale, preferred-vendor agreements and geographic diversification (China, Vietnam, Indonesia) temper supplier power. Ocean freight peaked >USD 10,000/FEU in 2021 and normalized toward 2024, easing logistics pressure.

| Metric | 2024 Value/Note |

|---|---|

| Asia manufacturing footprint | 60–80% |

| Commodity price volatility | 10–20%+ annual swings |

| Container rates peak | >USD 10,000/FEU (2021) → near pre‑pandemic by 2024 |

What is included in the product

Concise Porter's Five Forces analysis for Mattel evaluating competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers that affect pricing, margins, and long-term market positioning.

A concise one-sheet Porter's Five Forces for Mattel that pinpoints supplier, buyer, rivalry, entrant and substitute pressures—ideal for quick strategic decisions; customizable force levels and radar visualization require no macros and drop straight into decks or reports.

Customers Bargaining Power

Retail giants’ negotiating clout

Mass retailers and e-commerce platforms concentrate demand—Amazon held roughly 38% of US e-commerce sales in 2024—so Walmart, Target and Amazon exert strong pressure on pricing, co-op marketing, terms and shelf placement. Failure to meet sell-through targets can trigger delisting or reduced assortment. Mattel counters by leveraging must-have IP (Barbie, Hot Wheels) and retailer-exclusive SKUs to protect shelf space and margins.

Low switching costs for consumers

Parents and gift-givers can easily trade among toy brands and categories, keeping buyer power high as price promotions and trending IP (e.g., movie tie-ins) rapidly shift demand; Mattel reported roughly $6.2 billion in 2024 net sales, underscoring heavy reliance on hit lines. Low switching costs mean deals and trends move volume quickly, though brand affinity and collectibles for Barbie and Hot Wheels raise stickiness for flagship lines.

Seasonality and promotional intensity

Q4 drives a disproportionate share of industry sales, roughly 35–40% of annual toy revenue per NPD (2024), heightening retailer leverage to demand heavy promotions and slotting, which compress margins. Slotting fees and promotional intensity force Mattel to defend pricing, so it uses advanced demand forecasting and tiered assortments to optimize mix. Early orders and pre‑sales data cut last‑minute concessions and lower markdown risk.

Direct-to-consumer and digital channels

Direct-to-consumer and specialty channels give Mattel alternative routes that dilute retailer bargaining by shifting some sales away from big-box partners; global e-commerce reached about 25% of retail sales in 2024 (eMarketer), supporting DTC growth.

First-party data and customization bolster pricing resilience, but DTC volumes remain a minority versus major retailers; omnichannel execution lets Mattel balance reach and margin control.

- Retailer dependence: reduced

- Global e‑commerce 2024: ~25%

- First‑party data: improves pricing

- DTC scale: still smaller than big‑box

- Omnichannel: tradeoff reach vs margin

Licensing and co-branded expectations

Retailers demand fresh content tie-ins and eventized launches; failure to deliver newness weakens Mattel’s negotiation leverage with major chains.

Mattel’s media pipeline and partnerships — highlighted by the Barbie franchise that helped drive a $1.4 billion global box office for the 2023 film — sustain retail excitement and shelf prominence.

Timed exclusives and limited editions increase scarcity and bargaining stance, enabling higher margins and preferential retailer placement.

- Retailer expectations: fresh tie-ins, event launches

- Media leverage: Barbie $1.4B global box office

- Negotiation tools: timed exclusives, limited editions

Mass retailers and Q4 seasonality give buyers leverage; IP, DTC and exclusives defend sales

Mass retailers (Amazon ~38% US e‑commerce 2024) and Q4 seasonality (35–40% of annual toy revenue, NPD 2024) give buyers strong leverage on price, slots and promos. Mattel ($6.2B net sales 2024) defends via must‑have IP (Barbie $1.4B box office 2023), DTC/e‑commerce (~25% global retail 2024) and exclusives.

| Metric | Value |

|---|---|

| Amazon share (US e‑comm) | ~38% (2024) |

| Mattel net sales | $6.2B (2024) |

| Q4 share (toys) | 35–40% (NPD 2024) |

| Global e‑commerce | ~25% (2024) |

Same Document Delivered

Mattel Porter's Five Forces Analysis

This preview shows the exact Mattel Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The final document is professionally formatted and covers competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes. You'll get instant access to this ready-to-use file for analysis and decision-making.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

Mattel faces intense rivalry from diversified toy and entertainment players, shifting buyer preferences, rising substitute digital entertainment, moderate supplier leverage, and barriers that moderate new entrants. This snapshot highlights key pressures on margins and growth. The full Porter's Five Forces Analysis delivers force-by-force ratings, visuals, and strategic implications to guide investment or strategy decisions—unlock it now.

Suppliers Bargaining Power

Global plastics and components

Mattel relies on polymers, die-cast metals and electronic modules sourced largely from Asia (≈60–80% of manufacturing footprint), concentrating exposure in Southeast and East Asia. Commodity price volatility for resins and metals can swing margins—price moves of 10–20%+ annually have been observed in recent cycles—if not hedged or under long-term contracts. Mattel’s scale enables multi-sourcing and volume discounts that lower unit costs. Tight specs and rigorous quality controls limit feasible supplier substitutes, moderately elevating supplier power.

Contract manufacturing concentration

Production is concentrated among a limited set of qualified contract manufacturers holding international toy-safety certifications (e.g., ISO, EN71) primarily in Asia, creating moderate supplier leverage. Switching is feasible but costly due to tooling replacement, factory audits, and lead-time risks that can delay seasonal launches. Mattel reduces dependence through dual-sourcing and geographic diversification across China, Vietnam, and Indonesia.

Licensing/content partners as “suppliers”

Mattel treats licensors and content partners as quasi-suppliers of brand equity; hit IP owners can command higher royalties and exclusivity, pressuring margins. Mattel’s owned franchises—Barbie, Hot Wheels, Fisher‑Price—provide countervailing leverage, with branded portfolio strength used to negotiate balanced terms. Negotiating across multiple brands helps normalize royalty rates and exclusivity tradeoffs for 2024 collaborations.

Compliance and ESG requirements

- Compliance limits supplier pool

- Approved vendors leverage investment

- Preferred programs temper pricing

- Audits/traceability cut opportunism

Logistics and geopolitics exposure

Ocean freight capacity swings, port congestion and geopolitical shifts can amplify supplier leverage by creating bottlenecks; container rates fell from pandemic peaks above USD 10,000 per FEU to near pre‑pandemic levels by 2024, but congestion still adds weeks to some lanes.

Suppliers near ports or with flexible logistics gain bargaining power during disruptions; Mattel mitigates risk with diversified lanes, inventory planning and expanding nearshoring options to strengthen negotiation leverage.

Asia sourcing 60–80% concentrates supplier power amid 10–20%+ commodity swings

Mattel sources 60–80% of manufacturing in Asia, concentrating supplier exposure; resin/metal costs have swung 10–20%+ annually in recent cycles, pressuring margins. Certified contract manufacturers and compliance needs raise switching costs, giving approved suppliers moderate leverage, while Mattel’s scale, preferred-vendor agreements and geographic diversification (China, Vietnam, Indonesia) temper supplier power. Ocean freight peaked >USD 10,000/FEU in 2021 and normalized toward 2024, easing logistics pressure.

| Metric | 2024 Value/Note |

|---|---|

| Asia manufacturing footprint | 60–80% |

| Commodity price volatility | 10–20%+ annual swings |

| Container rates peak | >USD 10,000/FEU (2021) → near pre‑pandemic by 2024 |

What is included in the product

Concise Porter's Five Forces analysis for Mattel evaluating competitive rivalry, supplier and buyer power, threat of substitutes and new entrants, and identifying disruptive trends and strategic levers that affect pricing, margins, and long-term market positioning.

A concise one-sheet Porter's Five Forces for Mattel that pinpoints supplier, buyer, rivalry, entrant and substitute pressures—ideal for quick strategic decisions; customizable force levels and radar visualization require no macros and drop straight into decks or reports.

Customers Bargaining Power

Retail giants’ negotiating clout

Mass retailers and e-commerce platforms concentrate demand—Amazon held roughly 38% of US e-commerce sales in 2024—so Walmart, Target and Amazon exert strong pressure on pricing, co-op marketing, terms and shelf placement. Failure to meet sell-through targets can trigger delisting or reduced assortment. Mattel counters by leveraging must-have IP (Barbie, Hot Wheels) and retailer-exclusive SKUs to protect shelf space and margins.

Low switching costs for consumers

Parents and gift-givers can easily trade among toy brands and categories, keeping buyer power high as price promotions and trending IP (e.g., movie tie-ins) rapidly shift demand; Mattel reported roughly $6.2 billion in 2024 net sales, underscoring heavy reliance on hit lines. Low switching costs mean deals and trends move volume quickly, though brand affinity and collectibles for Barbie and Hot Wheels raise stickiness for flagship lines.

Seasonality and promotional intensity

Q4 drives a disproportionate share of industry sales, roughly 35–40% of annual toy revenue per NPD (2024), heightening retailer leverage to demand heavy promotions and slotting, which compress margins. Slotting fees and promotional intensity force Mattel to defend pricing, so it uses advanced demand forecasting and tiered assortments to optimize mix. Early orders and pre‑sales data cut last‑minute concessions and lower markdown risk.

Direct-to-consumer and digital channels

Direct-to-consumer and specialty channels give Mattel alternative routes that dilute retailer bargaining by shifting some sales away from big-box partners; global e-commerce reached about 25% of retail sales in 2024 (eMarketer), supporting DTC growth.

First-party data and customization bolster pricing resilience, but DTC volumes remain a minority versus major retailers; omnichannel execution lets Mattel balance reach and margin control.

- Retailer dependence: reduced

- Global e‑commerce 2024: ~25%

- First‑party data: improves pricing

- DTC scale: still smaller than big‑box

- Omnichannel: tradeoff reach vs margin

Licensing and co-branded expectations

Retailers demand fresh content tie-ins and eventized launches; failure to deliver newness weakens Mattel’s negotiation leverage with major chains.

Mattel’s media pipeline and partnerships — highlighted by the Barbie franchise that helped drive a $1.4 billion global box office for the 2023 film — sustain retail excitement and shelf prominence.

Timed exclusives and limited editions increase scarcity and bargaining stance, enabling higher margins and preferential retailer placement.

- Retailer expectations: fresh tie-ins, event launches

- Media leverage: Barbie $1.4B global box office

- Negotiation tools: timed exclusives, limited editions

Mass retailers and Q4 seasonality give buyers leverage; IP, DTC and exclusives defend sales

Mass retailers (Amazon ~38% US e‑commerce 2024) and Q4 seasonality (35–40% of annual toy revenue, NPD 2024) give buyers strong leverage on price, slots and promos. Mattel ($6.2B net sales 2024) defends via must‑have IP (Barbie $1.4B box office 2023), DTC/e‑commerce (~25% global retail 2024) and exclusives.

| Metric | Value |

|---|---|

| Amazon share (US e‑comm) | ~38% (2024) |

| Mattel net sales | $6.2B (2024) |

| Q4 share (toys) | 35–40% (NPD 2024) |

| Global e‑commerce | ~25% (2024) |

Same Document Delivered

Mattel Porter's Five Forces Analysis

This preview shows the exact Mattel Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or samples. The final document is professionally formatted and covers competitive rivalry, supplier and buyer power, and threats of new entrants and substitutes. You'll get instant access to this ready-to-use file for analysis and decision-making.