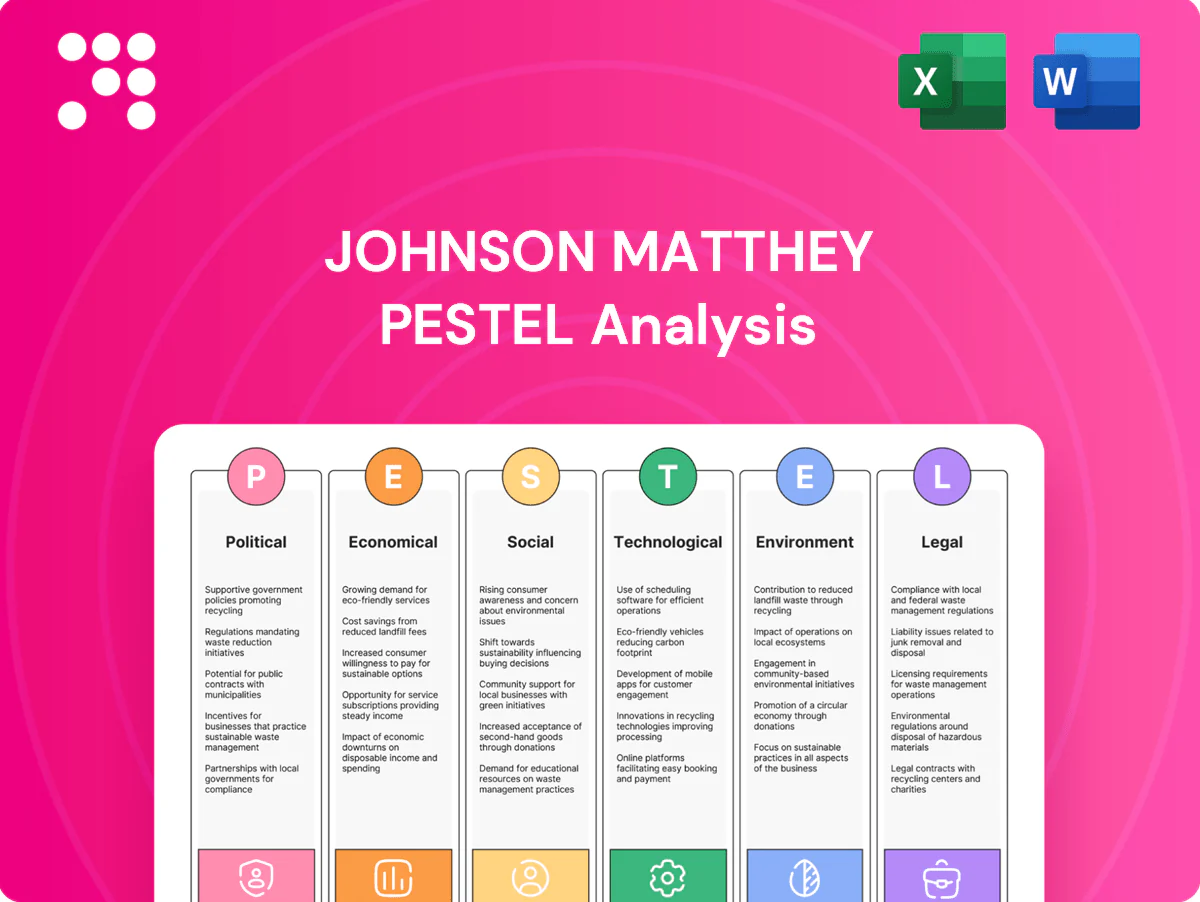

Johnson Matthey PESTLE Analysis

Your Shortcut to Market Insight Starts Here

Unlock how political regulation, shifting energy economics, and rapid clean-tech innovation are shaping Johnson Matthey’s strategic path. This concise PESTLE snapshot highlights risks and growth levers you can act on. Purchase the full, editable analysis to get detailed insights and ready-to-use strategic recommendations.

Political factors

Emissions policy tailwinds

Stricter global emissions standards in transport and industry — EU Euro 7 (timelines around 2025–27), China VI (phased in through 2021–23) and ongoing US EPA tightening through the 2020s — are boosting demand for advanced catalysts as transport accounts for about 24% of energy‑related CO2 (IEA). Policy reversals or delays can shift volumes and mix, so JM must align lobbying and compliance to capture regulatory-led growth.

Hydrogen and green industrial policy

US IRA clean hydrogen tax credit (Section 45V) of up to 3 per kg, the EU Green Deal target of 10 Mt renewable hydrogen by 2030 and the UK 10 GW electrolyser target plus a £240m Net Zero Hydrogen Fund drive demand for fuel cells and electrolysis supply chains that boost Johnson Matthey’s catalysts and components uptake. Subsidies and CfDs can accelerate JM adoption and pricing power, while localization and eligibility rules shape where JM sites capacity. Monitoring tender pipelines across US, EU and UK is critical for order visibility and capacity planning.

Geopolitical supply chain risk

Johnson Matthey faces concentrated PGM sourcing risk with roughly 70% of global platinum group metals originating in South Africa and about 10% from Russia, exposing it to political instability and sanctions. Trade tensions and tariffs have repeatedly distorted flows and pressured processing margins. Expanding diversified mines and recycling — recycling supplies around 20–25% of platinum demand — cuts geopolitical exposure. Government stockpiles and export controls can rapidly swing availability and prices.

Brexit and market access

Brexit created UK REACH (effective 1 January 2021) forcing Johnson Matthey to maintain dual UK REACH and EU REACH registrations, increasing regulatory and testing costs and complicating logistics between UK and EU sites.

Rules-of-origin and customs checks under the UK–EU Trade and Cooperation Agreement add paperwork, tariff risk and lead times, prompting JM to optimise plant footprints and inventory buffers.

Targeted UK government support for strategic manufacturing (eg industrial schemes and grants) can offset some frictional costs and influence investment location decisions.

- UK REACH launched 01-01-2021

- Dual compliance required: UK REACH + EU REACH

- Rules-of-origin/customs add lead time and cost

- Government manufacturing support mitigates some impacts

Public procurement and standards

Government clean-air rules and low-carbon fuel mandates plus public-fleet electrification drive procurement toward emissions-light tech; public procurement equals roughly 12% of GDP and the EU market is about €2 trillion yearly, boosting demand for JM catalysts and battery materials. CSRD/ESRS transparency rules (affecting ~50,000 firms) increase lifecycle scrutiny, while JM’s participation in standards bodies helps align specs with its low-embedded-carbon and recycled-content capabilities.

- Public procurement ≈12% GDP

- EU market ≈€2tn/yr

- CSRD covers ~50,000 firms

- Standards alignment improves market access

EU Euro 7, US IRA hydrogen incentives and PGM supply risks drive catalyst & electrolysis demand

Stricter vehicle/industrial emissions rules (EU Euro 7 timelines 2025–27), US EPA tightening and IRA 45V hydrogen credit (up to $3/kg) plus EU 10 Mt by 2030 and UK 10 GW by 2030 lift demand for JM catalysts and electrolysis components; PGM supply concentration (~70% South Africa, ~10% Russia) and recycling (~20–25% of supply) drive sourcing risk management; UK REACH (01-01-2021) and rules-of-origin add compliance costs; public procurement (~12% GDP) and CSRD (~50,000 firms) raise lifecycle transparency demands.

| Item | Metric/Date | Relevance to JM |

|---|---|---|

| EU Euro 7 | 2025–27 | Higher catalyst demand |

| US IRA 45V | Up to $3/kg | Boosts hydrogen market |

| PGM sourcing | ~70% RSA; ~10% RUS | Geopolitical supply risk |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect Johnson Matthey, with each category expanded into specific sub-points and examples tied to its chemicals, catalysts, and battery materials activities. Backed by current data and forward-looking insights, the analysis supports executives and investors in identifying risks, opportunities, and strategic scenarios.

A concise, visually segmented PESTLE summary of Johnson Matthey that’s easy to drop into slides or reports, editable for specific regions or business lines, and ideal for quickly aligning teams and supporting risk and market-positioning discussions.

Economic factors

Commodity price volatility

Platinum, palladium and rhodium price swings (2024 average: Pt ~$975/oz, Pd ~$1,260/oz, Rh ~$9,000/oz) materially drive Johnson Matthey’s working capital and hedging needs, forcing wider cash buffers. Spread management and recycling — which supplied roughly 25% of JM’s PGM feedstock in 2024 — are critical to margin stability. Substitution between PGMs (e.g., Pd to Pt in autocatalysts) shifts demand balance. Robust hedging and contractual pass-throughs (coverage ~70% in 2024) protect earnings.

Auto cycle and powertrain mix

ICE and hybrid production still drives catalyst volumes as EVs accounted for about 16% of global new car sales in 2024, leaving roughly 84% ICE/hybrid share; rising EV penetration reduces per-vehicle catalyst demand. China NEV share reached ~30% in 2024, the EU ~22% and the US ~8%, shifting regional technology content per unit. Commercial and off-road segments follow different cyclical patterns, impacting timing of orders. Accurate 2024–25 forecasts are critical for capacity loading and inventory management to avoid under- or over-utilisation.

Inflation and energy costs

High electricity (~£0.15–0.20/kWh) and industrial gas (~£0.04–0.06/kWh) prices raise processing costs for metal refining and chemicals, squeezing margins amid 2024 UK CPI around 4%. Energy surcharges and long‑term PPAs have been used to mitigate volatility, stabilising input costs. Aggressive efficiency programmes and electrification lower unit costs, but margin resilience hinges on pricing discipline and contract structures.

FX and interest rate dynamics

Capex, R&D, and scale-up economics

Hydrogen and catalyst capacity require disciplined capex tied to visible offtake; pilot-to-plant scale-up shifts yields and unit costs materially, often changing project IRR during commercialization phases.

Partnerships and customer prepayments can de-risk investments while R&D productivity and time-to-market determine long-term ROCE and asset turnover.

EU Euro 7, US IRA hydrogen incentives and PGM supply risks drive catalyst & electrolysis demand

Platinum/Pd/Rh volatility (2024 avg Pt ~$975, Pd ~$1,260, Rh ~$9,000) drives working capital and hedging; hedge coverage ~70% and recycling supplied ~25% of PGM feed in 2024. EVs ~16% of global car sales in 2024, reducing per‑vehicle catalyst demand as NEV shares: China ~30%, EU ~22%, US ~8%. Energy (£0.15–0.20/kWh) and FX (GBP/USD 1.27, EUR/GBP 0.86 Jul‑2025) plus BOE/Fed ~5.25% raise costs and discount rates.

| Metric | 2024/Jul‑2025 |

|---|---|

| PGM prices | Pt $975, Pd $1,260, Rh $9,000/oz (2024) |

| EV share | 16% global (2024) |

| Energy | £0.15–0.20/kWh (2024) |

| FX/Rates | GBP/USD 1.27, EUR/GBP 0.86; BOE/Fed ~5.25% (Jul‑2025) |

| Hedging/Recycling | Coverage ~70%; recycling ~25% feed (2024) |

Same Document Delivered

Johnson Matthey PESTLE Analysis

This Johnson Matthey PESTLE Analysis gives a concise evaluation of political, economic, social, technological, legal and environmental factors affecting the company. The content and structure shown in the preview is the same document you’ll download after payment. Fully formatted and ready to use, no placeholders or surprises.

Your Shortcut to Market Insight Starts Here

Unlock how political regulation, shifting energy economics, and rapid clean-tech innovation are shaping Johnson Matthey’s strategic path. This concise PESTLE snapshot highlights risks and growth levers you can act on. Purchase the full, editable analysis to get detailed insights and ready-to-use strategic recommendations.

Political factors

Emissions policy tailwinds

Stricter global emissions standards in transport and industry — EU Euro 7 (timelines around 2025–27), China VI (phased in through 2021–23) and ongoing US EPA tightening through the 2020s — are boosting demand for advanced catalysts as transport accounts for about 24% of energy‑related CO2 (IEA). Policy reversals or delays can shift volumes and mix, so JM must align lobbying and compliance to capture regulatory-led growth.

Hydrogen and green industrial policy

US IRA clean hydrogen tax credit (Section 45V) of up to 3 per kg, the EU Green Deal target of 10 Mt renewable hydrogen by 2030 and the UK 10 GW electrolyser target plus a £240m Net Zero Hydrogen Fund drive demand for fuel cells and electrolysis supply chains that boost Johnson Matthey’s catalysts and components uptake. Subsidies and CfDs can accelerate JM adoption and pricing power, while localization and eligibility rules shape where JM sites capacity. Monitoring tender pipelines across US, EU and UK is critical for order visibility and capacity planning.

Geopolitical supply chain risk

Johnson Matthey faces concentrated PGM sourcing risk with roughly 70% of global platinum group metals originating in South Africa and about 10% from Russia, exposing it to political instability and sanctions. Trade tensions and tariffs have repeatedly distorted flows and pressured processing margins. Expanding diversified mines and recycling — recycling supplies around 20–25% of platinum demand — cuts geopolitical exposure. Government stockpiles and export controls can rapidly swing availability and prices.

Brexit and market access

Brexit created UK REACH (effective 1 January 2021) forcing Johnson Matthey to maintain dual UK REACH and EU REACH registrations, increasing regulatory and testing costs and complicating logistics between UK and EU sites.

Rules-of-origin and customs checks under the UK–EU Trade and Cooperation Agreement add paperwork, tariff risk and lead times, prompting JM to optimise plant footprints and inventory buffers.

Targeted UK government support for strategic manufacturing (eg industrial schemes and grants) can offset some frictional costs and influence investment location decisions.

- UK REACH launched 01-01-2021

- Dual compliance required: UK REACH + EU REACH

- Rules-of-origin/customs add lead time and cost

- Government manufacturing support mitigates some impacts

Public procurement and standards

Government clean-air rules and low-carbon fuel mandates plus public-fleet electrification drive procurement toward emissions-light tech; public procurement equals roughly 12% of GDP and the EU market is about €2 trillion yearly, boosting demand for JM catalysts and battery materials. CSRD/ESRS transparency rules (affecting ~50,000 firms) increase lifecycle scrutiny, while JM’s participation in standards bodies helps align specs with its low-embedded-carbon and recycled-content capabilities.

- Public procurement ≈12% GDP

- EU market ≈€2tn/yr

- CSRD covers ~50,000 firms

- Standards alignment improves market access

EU Euro 7, US IRA hydrogen incentives and PGM supply risks drive catalyst & electrolysis demand

Stricter vehicle/industrial emissions rules (EU Euro 7 timelines 2025–27), US EPA tightening and IRA 45V hydrogen credit (up to $3/kg) plus EU 10 Mt by 2030 and UK 10 GW by 2030 lift demand for JM catalysts and electrolysis components; PGM supply concentration (~70% South Africa, ~10% Russia) and recycling (~20–25% of supply) drive sourcing risk management; UK REACH (01-01-2021) and rules-of-origin add compliance costs; public procurement (~12% GDP) and CSRD (~50,000 firms) raise lifecycle transparency demands.

| Item | Metric/Date | Relevance to JM |

|---|---|---|

| EU Euro 7 | 2025–27 | Higher catalyst demand |

| US IRA 45V | Up to $3/kg | Boosts hydrogen market |

| PGM sourcing | ~70% RSA; ~10% RUS | Geopolitical supply risk |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect Johnson Matthey, with each category expanded into specific sub-points and examples tied to its chemicals, catalysts, and battery materials activities. Backed by current data and forward-looking insights, the analysis supports executives and investors in identifying risks, opportunities, and strategic scenarios.

A concise, visually segmented PESTLE summary of Johnson Matthey that’s easy to drop into slides or reports, editable for specific regions or business lines, and ideal for quickly aligning teams and supporting risk and market-positioning discussions.

Economic factors

Commodity price volatility

Platinum, palladium and rhodium price swings (2024 average: Pt ~$975/oz, Pd ~$1,260/oz, Rh ~$9,000/oz) materially drive Johnson Matthey’s working capital and hedging needs, forcing wider cash buffers. Spread management and recycling — which supplied roughly 25% of JM’s PGM feedstock in 2024 — are critical to margin stability. Substitution between PGMs (e.g., Pd to Pt in autocatalysts) shifts demand balance. Robust hedging and contractual pass-throughs (coverage ~70% in 2024) protect earnings.

Auto cycle and powertrain mix

ICE and hybrid production still drives catalyst volumes as EVs accounted for about 16% of global new car sales in 2024, leaving roughly 84% ICE/hybrid share; rising EV penetration reduces per-vehicle catalyst demand. China NEV share reached ~30% in 2024, the EU ~22% and the US ~8%, shifting regional technology content per unit. Commercial and off-road segments follow different cyclical patterns, impacting timing of orders. Accurate 2024–25 forecasts are critical for capacity loading and inventory management to avoid under- or over-utilisation.

Inflation and energy costs

High electricity (~£0.15–0.20/kWh) and industrial gas (~£0.04–0.06/kWh) prices raise processing costs for metal refining and chemicals, squeezing margins amid 2024 UK CPI around 4%. Energy surcharges and long‑term PPAs have been used to mitigate volatility, stabilising input costs. Aggressive efficiency programmes and electrification lower unit costs, but margin resilience hinges on pricing discipline and contract structures.

FX and interest rate dynamics

Capex, R&D, and scale-up economics

Hydrogen and catalyst capacity require disciplined capex tied to visible offtake; pilot-to-plant scale-up shifts yields and unit costs materially, often changing project IRR during commercialization phases.

Partnerships and customer prepayments can de-risk investments while R&D productivity and time-to-market determine long-term ROCE and asset turnover.

EU Euro 7, US IRA hydrogen incentives and PGM supply risks drive catalyst & electrolysis demand

Platinum/Pd/Rh volatility (2024 avg Pt ~$975, Pd ~$1,260, Rh ~$9,000) drives working capital and hedging; hedge coverage ~70% and recycling supplied ~25% of PGM feed in 2024. EVs ~16% of global car sales in 2024, reducing per‑vehicle catalyst demand as NEV shares: China ~30%, EU ~22%, US ~8%. Energy (£0.15–0.20/kWh) and FX (GBP/USD 1.27, EUR/GBP 0.86 Jul‑2025) plus BOE/Fed ~5.25% raise costs and discount rates.

| Metric | 2024/Jul‑2025 |

|---|---|

| PGM prices | Pt $975, Pd $1,260, Rh $9,000/oz (2024) |

| EV share | 16% global (2024) |

| Energy | £0.15–0.20/kWh (2024) |

| FX/Rates | GBP/USD 1.27, EUR/GBP 0.86; BOE/Fed ~5.25% (Jul‑2025) |

| Hedging/Recycling | Coverage ~70%; recycling ~25% feed (2024) |

Same Document Delivered

Johnson Matthey PESTLE Analysis

This Johnson Matthey PESTLE Analysis gives a concise evaluation of political, economic, social, technological, legal and environmental factors affecting the company. The content and structure shown in the preview is the same document you’ll download after payment. Fully formatted and ready to use, no placeholders or surprises.

Description

Your Shortcut to Market Insight Starts Here

Unlock how political regulation, shifting energy economics, and rapid clean-tech innovation are shaping Johnson Matthey’s strategic path. This concise PESTLE snapshot highlights risks and growth levers you can act on. Purchase the full, editable analysis to get detailed insights and ready-to-use strategic recommendations.

Political factors

Emissions policy tailwinds

Stricter global emissions standards in transport and industry — EU Euro 7 (timelines around 2025–27), China VI (phased in through 2021–23) and ongoing US EPA tightening through the 2020s — are boosting demand for advanced catalysts as transport accounts for about 24% of energy‑related CO2 (IEA). Policy reversals or delays can shift volumes and mix, so JM must align lobbying and compliance to capture regulatory-led growth.

Hydrogen and green industrial policy

US IRA clean hydrogen tax credit (Section 45V) of up to 3 per kg, the EU Green Deal target of 10 Mt renewable hydrogen by 2030 and the UK 10 GW electrolyser target plus a £240m Net Zero Hydrogen Fund drive demand for fuel cells and electrolysis supply chains that boost Johnson Matthey’s catalysts and components uptake. Subsidies and CfDs can accelerate JM adoption and pricing power, while localization and eligibility rules shape where JM sites capacity. Monitoring tender pipelines across US, EU and UK is critical for order visibility and capacity planning.

Geopolitical supply chain risk

Johnson Matthey faces concentrated PGM sourcing risk with roughly 70% of global platinum group metals originating in South Africa and about 10% from Russia, exposing it to political instability and sanctions. Trade tensions and tariffs have repeatedly distorted flows and pressured processing margins. Expanding diversified mines and recycling — recycling supplies around 20–25% of platinum demand — cuts geopolitical exposure. Government stockpiles and export controls can rapidly swing availability and prices.

Brexit and market access

Brexit created UK REACH (effective 1 January 2021) forcing Johnson Matthey to maintain dual UK REACH and EU REACH registrations, increasing regulatory and testing costs and complicating logistics between UK and EU sites.

Rules-of-origin and customs checks under the UK–EU Trade and Cooperation Agreement add paperwork, tariff risk and lead times, prompting JM to optimise plant footprints and inventory buffers.

Targeted UK government support for strategic manufacturing (eg industrial schemes and grants) can offset some frictional costs and influence investment location decisions.

- UK REACH launched 01-01-2021

- Dual compliance required: UK REACH + EU REACH

- Rules-of-origin/customs add lead time and cost

- Government manufacturing support mitigates some impacts

Public procurement and standards

Government clean-air rules and low-carbon fuel mandates plus public-fleet electrification drive procurement toward emissions-light tech; public procurement equals roughly 12% of GDP and the EU market is about €2 trillion yearly, boosting demand for JM catalysts and battery materials. CSRD/ESRS transparency rules (affecting ~50,000 firms) increase lifecycle scrutiny, while JM’s participation in standards bodies helps align specs with its low-embedded-carbon and recycled-content capabilities.

- Public procurement ≈12% GDP

- EU market ≈€2tn/yr

- CSRD covers ~50,000 firms

- Standards alignment improves market access

EU Euro 7, US IRA hydrogen incentives and PGM supply risks drive catalyst & electrolysis demand

Stricter vehicle/industrial emissions rules (EU Euro 7 timelines 2025–27), US EPA tightening and IRA 45V hydrogen credit (up to $3/kg) plus EU 10 Mt by 2030 and UK 10 GW by 2030 lift demand for JM catalysts and electrolysis components; PGM supply concentration (~70% South Africa, ~10% Russia) and recycling (~20–25% of supply) drive sourcing risk management; UK REACH (01-01-2021) and rules-of-origin add compliance costs; public procurement (~12% GDP) and CSRD (~50,000 firms) raise lifecycle transparency demands.

| Item | Metric/Date | Relevance to JM |

|---|---|---|

| EU Euro 7 | 2025–27 | Higher catalyst demand |

| US IRA 45V | Up to $3/kg | Boosts hydrogen market |

| PGM sourcing | ~70% RSA; ~10% RUS | Geopolitical supply risk |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental, and Legal factors uniquely affect Johnson Matthey, with each category expanded into specific sub-points and examples tied to its chemicals, catalysts, and battery materials activities. Backed by current data and forward-looking insights, the analysis supports executives and investors in identifying risks, opportunities, and strategic scenarios.

A concise, visually segmented PESTLE summary of Johnson Matthey that’s easy to drop into slides or reports, editable for specific regions or business lines, and ideal for quickly aligning teams and supporting risk and market-positioning discussions.

Economic factors

Commodity price volatility

Platinum, palladium and rhodium price swings (2024 average: Pt ~$975/oz, Pd ~$1,260/oz, Rh ~$9,000/oz) materially drive Johnson Matthey’s working capital and hedging needs, forcing wider cash buffers. Spread management and recycling — which supplied roughly 25% of JM’s PGM feedstock in 2024 — are critical to margin stability. Substitution between PGMs (e.g., Pd to Pt in autocatalysts) shifts demand balance. Robust hedging and contractual pass-throughs (coverage ~70% in 2024) protect earnings.

Auto cycle and powertrain mix

ICE and hybrid production still drives catalyst volumes as EVs accounted for about 16% of global new car sales in 2024, leaving roughly 84% ICE/hybrid share; rising EV penetration reduces per-vehicle catalyst demand. China NEV share reached ~30% in 2024, the EU ~22% and the US ~8%, shifting regional technology content per unit. Commercial and off-road segments follow different cyclical patterns, impacting timing of orders. Accurate 2024–25 forecasts are critical for capacity loading and inventory management to avoid under- or over-utilisation.

Inflation and energy costs

High electricity (~£0.15–0.20/kWh) and industrial gas (~£0.04–0.06/kWh) prices raise processing costs for metal refining and chemicals, squeezing margins amid 2024 UK CPI around 4%. Energy surcharges and long‑term PPAs have been used to mitigate volatility, stabilising input costs. Aggressive efficiency programmes and electrification lower unit costs, but margin resilience hinges on pricing discipline and contract structures.

FX and interest rate dynamics

Capex, R&D, and scale-up economics

Hydrogen and catalyst capacity require disciplined capex tied to visible offtake; pilot-to-plant scale-up shifts yields and unit costs materially, often changing project IRR during commercialization phases.

Partnerships and customer prepayments can de-risk investments while R&D productivity and time-to-market determine long-term ROCE and asset turnover.

EU Euro 7, US IRA hydrogen incentives and PGM supply risks drive catalyst & electrolysis demand

Platinum/Pd/Rh volatility (2024 avg Pt ~$975, Pd ~$1,260, Rh ~$9,000) drives working capital and hedging; hedge coverage ~70% and recycling supplied ~25% of PGM feed in 2024. EVs ~16% of global car sales in 2024, reducing per‑vehicle catalyst demand as NEV shares: China ~30%, EU ~22%, US ~8%. Energy (£0.15–0.20/kWh) and FX (GBP/USD 1.27, EUR/GBP 0.86 Jul‑2025) plus BOE/Fed ~5.25% raise costs and discount rates.

| Metric | 2024/Jul‑2025 |

|---|---|

| PGM prices | Pt $975, Pd $1,260, Rh $9,000/oz (2024) |

| EV share | 16% global (2024) |

| Energy | £0.15–0.20/kWh (2024) |

| FX/Rates | GBP/USD 1.27, EUR/GBP 0.86; BOE/Fed ~5.25% (Jul‑2025) |

| Hedging/Recycling | Coverage ~70%; recycling ~25% feed (2024) |

Same Document Delivered

Johnson Matthey PESTLE Analysis

This Johnson Matthey PESTLE Analysis gives a concise evaluation of political, economic, social, technological, legal and environmental factors affecting the company. The content and structure shown in the preview is the same document you’ll download after payment. Fully formatted and ready to use, no placeholders or surprises.