MAXIMUS Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

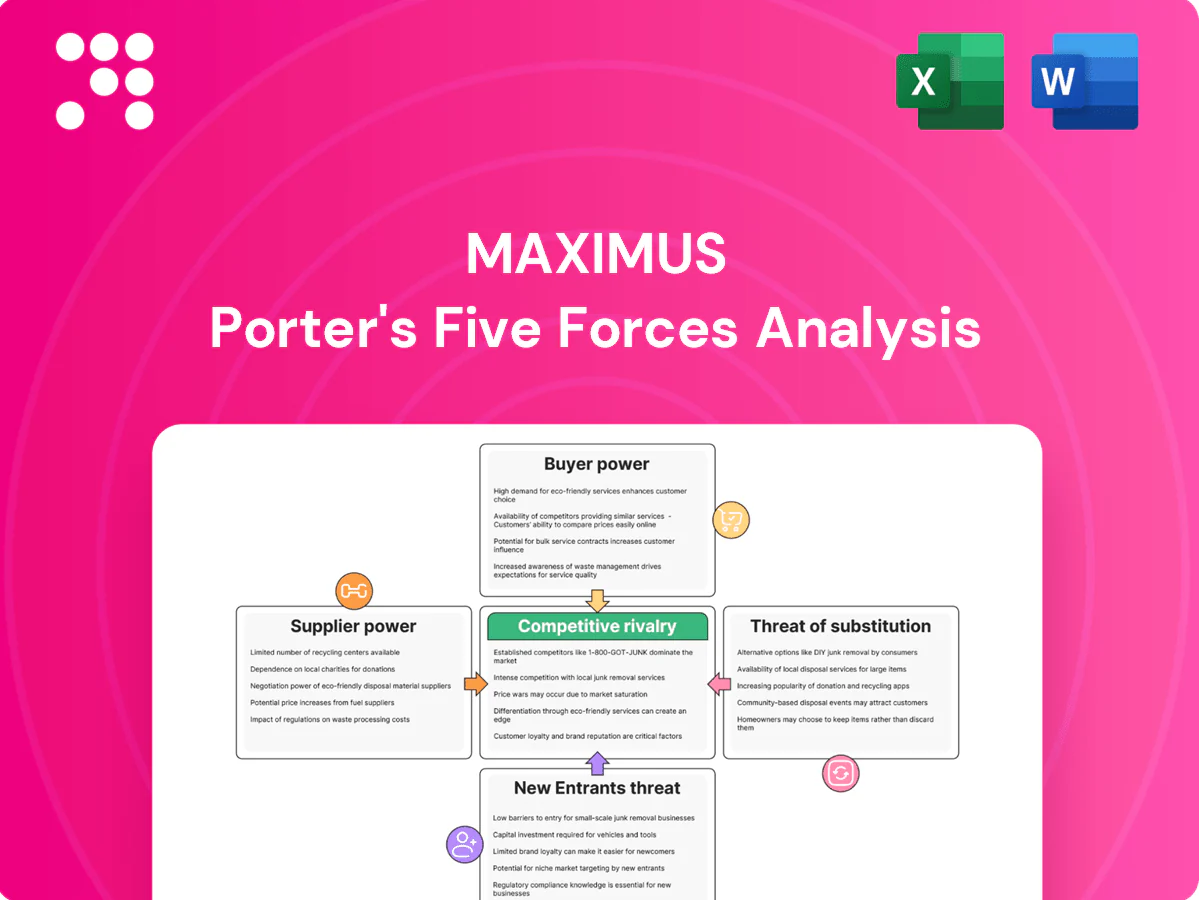

MAXIMUS faces moderate buyer power and regulatory-driven barriers that limit new entrants, while supplier power and substitute threats are low-to-moderate given its specialized government-contract services. Competitive rivalry is intense among established integrators. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MAXIMUS’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized labor dependence

MAXIMUS depends on skilled caseworkers, clinicians and cleared IT staff, drawing from a workforce of approximately 34,000 employees worldwide. Tight labor markets and 2024 wage inflation trends grant this talent moderate bargaining power. Required certifications and role-specific training raise switching costs for buyers. Company retention programs and targeted upskilling partially offset supplier leverage.

Critical IT and cloud vendors

Core MAXIMUS operations rely on major cloud, CRM, IVR and analytics platforms, concentrating dependency on top hyperscalers (2024 market shares: AWS ~32%, Microsoft ~22%, Google ~11%). FedRAMP and other compliance needs amplify supplier leverage for federal contracts. Long-term licenses and deep integrations increase switching costs and lock-in. A deliberate multi-vendor strategy can reduce concentration risk and improve negotiation leverage.

Data and telecom provisioning

Secure networks, call centers and low-latency data feeds are critical inputs; providers often mandate SLAs of 99.99% (≈52.6 minutes downtime/year), creating bargaining levers for suppliers. Regional telecoms are typically concentrated in 2–3 players holding over 60% share, limiting buyer options. Redundancy (multi-carrier paths) raises provisioning costs 10–20% and reduces switching flexibility, while large volume commitments can cut unit bandwidth pricing materially.

Specialist subcontractors

Specialist subcontractors providing local outreach, language services, and niche compliance support fill critical gaps for MAXIMUS, granting them leverage where on-the-ground capabilities are scarce; in geographies with few providers this scarcity raises supplier power. As of 2024 federal flow-down clauses (FAR/DFARS) continue to restrict eligible vendor pools, while master service agreements and rate cards commonly cap subcontract rates.

- Local outreach: localized presence drives premium

- Language services: essential for compliance and access

- Niche compliance partners: limited suppliers increase bargaining power

- FAR/DFARS (2024): flow-downs narrow vendor options

- MSAs: rate caps limit price escalation

Software and compliance tooling

Identity proofing, fraud detection, and audit tools are mandatory for MAXIMUS programs, and the global identity verification market reached about 12.9 billion USD in 2024, concentrating supplier power as certification-heavy solutions (FIPS, SOC2, FedRAMP) narrow options and raise switching costs; integration and validation can add 5–15% of project budgets, increasing dependence.

- Concentration: few certified vendors

- Cost: integration/validation +5–15% of budget

- Leverage: framework contracts enable volume discounts

Supplier power moderate: 34k; hyperscalers 32%/22%/11%

MAXIMUS faces moderate supplier power: 34,000 workforce dependency, 2024 wage inflation elevates labor leverage. Hyperscaler concentration (AWS 32%, Microsoft 22%, Google 11% in 2024) and FedRAMP needs increase cloud supplier bargaining power. Identity verification market ~12.9B USD (2024) and 99.99% SLA demands raise switching costs; multi-vendor strategies mitigate risk.

| Input | 2024 Metric | Impact |

|---|---|---|

| Workforce | 34,000 | Moderate leverage |

| Cloud | AWS32% MSFT22% GCP11% | High concentration |

| ID verification | $12.9B | Certification lock-in |

What is included in the product

Tailored Porter's Five Forces analysis for MAXIMUS, uncovering key drivers of competition, buyer and supplier power, entry barriers, substitutes, and disruptive threats to its market position, with strategic commentary to inform investor and management decisions.

MAXIMUS Porter's Five Forces delivers a single-page, customizable assessment that quickly highlights competitive pressures and strategic opportunities. No complex code—export-ready visuals and a clean layout make it ideal for fast decision-making and seamless integration into decks or dashboards.

Customers Bargaining Power

Concentrated government buyers

Federal and state agencies constitute a small number of very large Maximus accounts, giving buyers outsized leverage; Maximus reported roughly $6.2 billion in FY2024 revenue with government business representing the majority of sales. Their budgetary control and formal procurement rules let agencies dictate service levels, compliance measures and contract terms. Competitive wins hinge on price, regulatory compliance and track record, compressing margins and elevating procurement risk.

Rigorous RFP and rebid cycles

Competitive tenders in government RFPs force transparency and sustained price pressure, compressing margins even for incumbents; MAXIMUS remained exposed to rebid risk despite incumbency in 2024. Performance metrics in contracts tie directly to fee adjustments and penalties, increasing financial volatility. Agencies frequently reset scope at renewal, creating scope-creep or scope-loss risks that materially affect contract value.

High switching costs, exercised leverage

Transitioning vendors is costly and risky for public programs, often disrupting services and incurring remediation expenses, while Maximus reported roughly $5.8B revenue in 2024 highlighting its scale and client dependence. Buyers still extract concessions via rebid threats, with governments using competitive procurement cycles to drive price adjustments. Extensive knowledge transfer reduces vendor stickiness, and SLAs/incentives increasingly tie pricing to measurable outcomes.

Budget constraints and scrutiny

Public budgets and oversight force MAXIMUS to push for lower total cost; FY2024 revenue reported near $6.5 billion heightens client scrutiny of unit economics. Political cycles in 2024 demonstrated contract freezes and reshaping of program scopes, tightening near-term demand. Cost-plus and fixed-fee structures cap margins, so value demonstrations and ROI metrics are mandatory for renewal.

- Budget pressure: drives price competition

- Political risk: contract freezes in 2024

- Fee structure: limits margin upside

- Value proof: required for renewals

Compliance and data control

Agencies enforce strict security, privacy and reporting standards that give buyers leverage over MAXIMUS, with non-compliance triggering price holdbacks or contract termination; in 2024 MAXIMUS reported roughly $5.7 billion in revenue, heavily tied to government contracts where compliance clauses are standard. Custom agency requirements limit vendor pricing power and procurement flexibility, and data ownership remains with the buyer, constraining resale or reuse of client data.

- Strict standards reduce vendor pricing power

- Non-compliance enables holdbacks/termination

- Buyer retains data ownership — limits commercialization

- 2024 revenue concentration increases buyer leverage

Few large government buyers compress pricing despite vendors' $6.5B scale

Federal/state agencies are few, large buyers giving outsized leverage; MAXIMUS reported ~$6.5B revenue in FY2024, majority government. Procurement rules, strict compliance and performance‑based fees compress pricing power and margins. Rebid and scope‑change risks enable agencies to extract concessions despite high vendor transition costs.

| Metric | FY2024 |

|---|---|

| Revenue | $6.5B |

| Govt share | Majority |

Preview the Actual Deliverable

MAXIMUS Porter's Five Forces Analysis

This preview shows the exact MAXIMUS Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use upon payment. What you see is the deliverable.

Go Beyond the Preview—Access the Full Strategic Report

MAXIMUS faces moderate buyer power and regulatory-driven barriers that limit new entrants, while supplier power and substitute threats are low-to-moderate given its specialized government-contract services. Competitive rivalry is intense among established integrators. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MAXIMUS’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized labor dependence

MAXIMUS depends on skilled caseworkers, clinicians and cleared IT staff, drawing from a workforce of approximately 34,000 employees worldwide. Tight labor markets and 2024 wage inflation trends grant this talent moderate bargaining power. Required certifications and role-specific training raise switching costs for buyers. Company retention programs and targeted upskilling partially offset supplier leverage.

Critical IT and cloud vendors

Core MAXIMUS operations rely on major cloud, CRM, IVR and analytics platforms, concentrating dependency on top hyperscalers (2024 market shares: AWS ~32%, Microsoft ~22%, Google ~11%). FedRAMP and other compliance needs amplify supplier leverage for federal contracts. Long-term licenses and deep integrations increase switching costs and lock-in. A deliberate multi-vendor strategy can reduce concentration risk and improve negotiation leverage.

Data and telecom provisioning

Secure networks, call centers and low-latency data feeds are critical inputs; providers often mandate SLAs of 99.99% (≈52.6 minutes downtime/year), creating bargaining levers for suppliers. Regional telecoms are typically concentrated in 2–3 players holding over 60% share, limiting buyer options. Redundancy (multi-carrier paths) raises provisioning costs 10–20% and reduces switching flexibility, while large volume commitments can cut unit bandwidth pricing materially.

Specialist subcontractors

Specialist subcontractors providing local outreach, language services, and niche compliance support fill critical gaps for MAXIMUS, granting them leverage where on-the-ground capabilities are scarce; in geographies with few providers this scarcity raises supplier power. As of 2024 federal flow-down clauses (FAR/DFARS) continue to restrict eligible vendor pools, while master service agreements and rate cards commonly cap subcontract rates.

- Local outreach: localized presence drives premium

- Language services: essential for compliance and access

- Niche compliance partners: limited suppliers increase bargaining power

- FAR/DFARS (2024): flow-downs narrow vendor options

- MSAs: rate caps limit price escalation

Software and compliance tooling

Identity proofing, fraud detection, and audit tools are mandatory for MAXIMUS programs, and the global identity verification market reached about 12.9 billion USD in 2024, concentrating supplier power as certification-heavy solutions (FIPS, SOC2, FedRAMP) narrow options and raise switching costs; integration and validation can add 5–15% of project budgets, increasing dependence.

- Concentration: few certified vendors

- Cost: integration/validation +5–15% of budget

- Leverage: framework contracts enable volume discounts

Supplier power moderate: 34k; hyperscalers 32%/22%/11%

MAXIMUS faces moderate supplier power: 34,000 workforce dependency, 2024 wage inflation elevates labor leverage. Hyperscaler concentration (AWS 32%, Microsoft 22%, Google 11% in 2024) and FedRAMP needs increase cloud supplier bargaining power. Identity verification market ~12.9B USD (2024) and 99.99% SLA demands raise switching costs; multi-vendor strategies mitigate risk.

| Input | 2024 Metric | Impact |

|---|---|---|

| Workforce | 34,000 | Moderate leverage |

| Cloud | AWS32% MSFT22% GCP11% | High concentration |

| ID verification | $12.9B | Certification lock-in |

What is included in the product

Tailored Porter's Five Forces analysis for MAXIMUS, uncovering key drivers of competition, buyer and supplier power, entry barriers, substitutes, and disruptive threats to its market position, with strategic commentary to inform investor and management decisions.

MAXIMUS Porter's Five Forces delivers a single-page, customizable assessment that quickly highlights competitive pressures and strategic opportunities. No complex code—export-ready visuals and a clean layout make it ideal for fast decision-making and seamless integration into decks or dashboards.

Customers Bargaining Power

Concentrated government buyers

Federal and state agencies constitute a small number of very large Maximus accounts, giving buyers outsized leverage; Maximus reported roughly $6.2 billion in FY2024 revenue with government business representing the majority of sales. Their budgetary control and formal procurement rules let agencies dictate service levels, compliance measures and contract terms. Competitive wins hinge on price, regulatory compliance and track record, compressing margins and elevating procurement risk.

Rigorous RFP and rebid cycles

Competitive tenders in government RFPs force transparency and sustained price pressure, compressing margins even for incumbents; MAXIMUS remained exposed to rebid risk despite incumbency in 2024. Performance metrics in contracts tie directly to fee adjustments and penalties, increasing financial volatility. Agencies frequently reset scope at renewal, creating scope-creep or scope-loss risks that materially affect contract value.

High switching costs, exercised leverage

Transitioning vendors is costly and risky for public programs, often disrupting services and incurring remediation expenses, while Maximus reported roughly $5.8B revenue in 2024 highlighting its scale and client dependence. Buyers still extract concessions via rebid threats, with governments using competitive procurement cycles to drive price adjustments. Extensive knowledge transfer reduces vendor stickiness, and SLAs/incentives increasingly tie pricing to measurable outcomes.

Budget constraints and scrutiny

Public budgets and oversight force MAXIMUS to push for lower total cost; FY2024 revenue reported near $6.5 billion heightens client scrutiny of unit economics. Political cycles in 2024 demonstrated contract freezes and reshaping of program scopes, tightening near-term demand. Cost-plus and fixed-fee structures cap margins, so value demonstrations and ROI metrics are mandatory for renewal.

- Budget pressure: drives price competition

- Political risk: contract freezes in 2024

- Fee structure: limits margin upside

- Value proof: required for renewals

Compliance and data control

Agencies enforce strict security, privacy and reporting standards that give buyers leverage over MAXIMUS, with non-compliance triggering price holdbacks or contract termination; in 2024 MAXIMUS reported roughly $5.7 billion in revenue, heavily tied to government contracts where compliance clauses are standard. Custom agency requirements limit vendor pricing power and procurement flexibility, and data ownership remains with the buyer, constraining resale or reuse of client data.

- Strict standards reduce vendor pricing power

- Non-compliance enables holdbacks/termination

- Buyer retains data ownership — limits commercialization

- 2024 revenue concentration increases buyer leverage

Few large government buyers compress pricing despite vendors' $6.5B scale

Federal/state agencies are few, large buyers giving outsized leverage; MAXIMUS reported ~$6.5B revenue in FY2024, majority government. Procurement rules, strict compliance and performance‑based fees compress pricing power and margins. Rebid and scope‑change risks enable agencies to extract concessions despite high vendor transition costs.

| Metric | FY2024 |

|---|---|

| Revenue | $6.5B |

| Govt share | Majority |

Preview the Actual Deliverable

MAXIMUS Porter's Five Forces Analysis

This preview shows the exact MAXIMUS Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use upon payment. What you see is the deliverable.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

MAXIMUS faces moderate buyer power and regulatory-driven barriers that limit new entrants, while supplier power and substitute threats are low-to-moderate given its specialized government-contract services. Competitive rivalry is intense among established integrators. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore MAXIMUS’s competitive dynamics in detail.

Suppliers Bargaining Power

Specialized labor dependence

MAXIMUS depends on skilled caseworkers, clinicians and cleared IT staff, drawing from a workforce of approximately 34,000 employees worldwide. Tight labor markets and 2024 wage inflation trends grant this talent moderate bargaining power. Required certifications and role-specific training raise switching costs for buyers. Company retention programs and targeted upskilling partially offset supplier leverage.

Critical IT and cloud vendors

Core MAXIMUS operations rely on major cloud, CRM, IVR and analytics platforms, concentrating dependency on top hyperscalers (2024 market shares: AWS ~32%, Microsoft ~22%, Google ~11%). FedRAMP and other compliance needs amplify supplier leverage for federal contracts. Long-term licenses and deep integrations increase switching costs and lock-in. A deliberate multi-vendor strategy can reduce concentration risk and improve negotiation leverage.

Data and telecom provisioning

Secure networks, call centers and low-latency data feeds are critical inputs; providers often mandate SLAs of 99.99% (≈52.6 minutes downtime/year), creating bargaining levers for suppliers. Regional telecoms are typically concentrated in 2–3 players holding over 60% share, limiting buyer options. Redundancy (multi-carrier paths) raises provisioning costs 10–20% and reduces switching flexibility, while large volume commitments can cut unit bandwidth pricing materially.

Specialist subcontractors

Specialist subcontractors providing local outreach, language services, and niche compliance support fill critical gaps for MAXIMUS, granting them leverage where on-the-ground capabilities are scarce; in geographies with few providers this scarcity raises supplier power. As of 2024 federal flow-down clauses (FAR/DFARS) continue to restrict eligible vendor pools, while master service agreements and rate cards commonly cap subcontract rates.

- Local outreach: localized presence drives premium

- Language services: essential for compliance and access

- Niche compliance partners: limited suppliers increase bargaining power

- FAR/DFARS (2024): flow-downs narrow vendor options

- MSAs: rate caps limit price escalation

Software and compliance tooling

Identity proofing, fraud detection, and audit tools are mandatory for MAXIMUS programs, and the global identity verification market reached about 12.9 billion USD in 2024, concentrating supplier power as certification-heavy solutions (FIPS, SOC2, FedRAMP) narrow options and raise switching costs; integration and validation can add 5–15% of project budgets, increasing dependence.

- Concentration: few certified vendors

- Cost: integration/validation +5–15% of budget

- Leverage: framework contracts enable volume discounts

Supplier power moderate: 34k; hyperscalers 32%/22%/11%

MAXIMUS faces moderate supplier power: 34,000 workforce dependency, 2024 wage inflation elevates labor leverage. Hyperscaler concentration (AWS 32%, Microsoft 22%, Google 11% in 2024) and FedRAMP needs increase cloud supplier bargaining power. Identity verification market ~12.9B USD (2024) and 99.99% SLA demands raise switching costs; multi-vendor strategies mitigate risk.

| Input | 2024 Metric | Impact |

|---|---|---|

| Workforce | 34,000 | Moderate leverage |

| Cloud | AWS32% MSFT22% GCP11% | High concentration |

| ID verification | $12.9B | Certification lock-in |

What is included in the product

Tailored Porter's Five Forces analysis for MAXIMUS, uncovering key drivers of competition, buyer and supplier power, entry barriers, substitutes, and disruptive threats to its market position, with strategic commentary to inform investor and management decisions.

MAXIMUS Porter's Five Forces delivers a single-page, customizable assessment that quickly highlights competitive pressures and strategic opportunities. No complex code—export-ready visuals and a clean layout make it ideal for fast decision-making and seamless integration into decks or dashboards.

Customers Bargaining Power

Concentrated government buyers

Federal and state agencies constitute a small number of very large Maximus accounts, giving buyers outsized leverage; Maximus reported roughly $6.2 billion in FY2024 revenue with government business representing the majority of sales. Their budgetary control and formal procurement rules let agencies dictate service levels, compliance measures and contract terms. Competitive wins hinge on price, regulatory compliance and track record, compressing margins and elevating procurement risk.

Rigorous RFP and rebid cycles

Competitive tenders in government RFPs force transparency and sustained price pressure, compressing margins even for incumbents; MAXIMUS remained exposed to rebid risk despite incumbency in 2024. Performance metrics in contracts tie directly to fee adjustments and penalties, increasing financial volatility. Agencies frequently reset scope at renewal, creating scope-creep or scope-loss risks that materially affect contract value.

High switching costs, exercised leverage

Transitioning vendors is costly and risky for public programs, often disrupting services and incurring remediation expenses, while Maximus reported roughly $5.8B revenue in 2024 highlighting its scale and client dependence. Buyers still extract concessions via rebid threats, with governments using competitive procurement cycles to drive price adjustments. Extensive knowledge transfer reduces vendor stickiness, and SLAs/incentives increasingly tie pricing to measurable outcomes.

Budget constraints and scrutiny

Public budgets and oversight force MAXIMUS to push for lower total cost; FY2024 revenue reported near $6.5 billion heightens client scrutiny of unit economics. Political cycles in 2024 demonstrated contract freezes and reshaping of program scopes, tightening near-term demand. Cost-plus and fixed-fee structures cap margins, so value demonstrations and ROI metrics are mandatory for renewal.

- Budget pressure: drives price competition

- Political risk: contract freezes in 2024

- Fee structure: limits margin upside

- Value proof: required for renewals

Compliance and data control

Agencies enforce strict security, privacy and reporting standards that give buyers leverage over MAXIMUS, with non-compliance triggering price holdbacks or contract termination; in 2024 MAXIMUS reported roughly $5.7 billion in revenue, heavily tied to government contracts where compliance clauses are standard. Custom agency requirements limit vendor pricing power and procurement flexibility, and data ownership remains with the buyer, constraining resale or reuse of client data.

- Strict standards reduce vendor pricing power

- Non-compliance enables holdbacks/termination

- Buyer retains data ownership — limits commercialization

- 2024 revenue concentration increases buyer leverage

Few large government buyers compress pricing despite vendors' $6.5B scale

Federal/state agencies are few, large buyers giving outsized leverage; MAXIMUS reported ~$6.5B revenue in FY2024, majority government. Procurement rules, strict compliance and performance‑based fees compress pricing power and margins. Rebid and scope‑change risks enable agencies to extract concessions despite high vendor transition costs.

| Metric | FY2024 |

|---|---|

| Revenue | $6.5B |

| Govt share | Majority |

Preview the Actual Deliverable

MAXIMUS Porter's Five Forces Analysis

This preview shows the exact MAXIMUS Porter's Five Forces Analysis you'll receive immediately after purchase—no placeholders or samples. The document is fully formatted, professionally written, and ready for download and use upon payment. What you see is the deliverable.