Mayer Steel Pipe PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape Mayer Steel Pipe’s strategic outlook in our concise PESTLE snapshot. Ideal for investors, consultants, and managers, this brief highlights key external risks and opportunities you can act on immediately. Purchase the full PESTLE analysis to access detailed insights, data tables, and actionable recommendations for confident decision-making.

Political factors

Trade policy and tariffs

Import duties such as the US Section 232 25% steel tariff and other country-level levies materially shape Mayer Steel Pipe price competitiveness across markets. Sudden tariff hikes or anti-dumping measures have repeatedly disrupted sourcing and route-to-market plans, especially given China’s 57% share of global crude steel output (World Steel Association 2023). Proactive hedging of supply sources and localized finishing can mitigate policy shocks, while close monitoring of bilateral trade agreements is essential to protect margins.

Infrastructure spending priorities

Government-funded construction and utilities form Mayer Steel Pipe’s baseline demand, with major programs such as the US Bipartisan Infrastructure Law committing about 550 billion USD of new federal investment driving sustained pipe volumes. Shifts in budgets toward water, energy and transport change product mix and can swing annual volumes by double-digit percentages on large contracts. Public–private partnerships and improved advocacy and tender readiness raise win rates and accelerate project pipelines across regions.

Political stability and security

Political stability directly affects project execution, logistics safety and investor confidence; global FDI fell 12% to about $1.02 trillion in 2023 (UNCTAD), illustrating sensitivity to instability. Elections and policy transitions commonly delay approvals and public works; geopolitical tensions raise freight insurance and rerouting costs. Diversifying end-markets and staging inventory buffers reduce exposure.

Local content and industrial policy

Local content mandates and buy-local rules—often setting thresholds in the 30–60% range—affect Mayer Steel Pipe’s sourcing, certification costs and pricing power while driving demand for domestic inputs.

2024–25 incentives for domestic manufacturing (tax credits, capital subsidies) can justify capex in mills and coating lines; compliance opens preferential tenders but raises audit and reporting burdens.

Strategic JVs or tolling arrangements provide efficient routes to meet content thresholds without full upstream investment.

- Impact: higher sourcing/certification costs

- Incentives: capex support for mills/coating lines

- Access: preferential tenders vs audit burden

- Mitigation: JV/tolling to meet thresholds

Energy policy and subsidies

Power tariffs, fuel taxes and grid reliability materially affect Mayer Steel Pipe mill costs—industrial electricity often drives 15–25% of OPEX and unplanned outages raise per-ton costs; fuel levies (e.g., diesel excise) further squeeze margins. Subsidies for pipeline gas or renewables can cut EAF and heat-treatment energy spend; in 2024 corporate renewable PPAs reached prices as low as $20/MWh (~2 c/kWh). Policy-driven energy transitions will likely force capital expenditure for boiler/electric arc furnace upgrades and grid-interactive controls, while long-term PPAs stabilize cost curves and hedge volatility.

- Tariff exposure: high OPEX share

- Subsidies: lower EAF/heat costs

- Capex: equipment upgrades required

- PPAs: price stability (as low as $20/MWh in 2024)

Tariffs, 57% China steel share and local-content rules reshape pipe pricing

Import tariffs (eg US Section 232 25%) and anti-dumping actions plus China’s 57% share of crude steel (World Steel Association 2023) materially affect Mayer Steel Pipe pricing and sourcing. Government infrastructure spend (US Bipartisan Infrastructure Law ~550 billion USD) and local-content rules (commonly 30–60%) shape demand and bid access. Energy policy, PPAs as low as $20/MWh (2024), and political instability (FDI $1.02T 2023) drive OPEX, capex and route-to-market risk.

| Factor | Key stat | Impact |

|---|---|---|

| Tariffs | US 25% | Price competitiveness |

| Demand | 550B USD | Volume upside |

| Local content | 30–60% | Sourcing/certification |

| Energy | $20/MWh | Lower OPEX |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Mayer Steel Pipe, with data-backed trends and region-specific regulatory insights; designed for executives and investors to identify risks, opportunities and forward-looking scenarios ready for inclusion in plans, decks, or reports.

A clean, visually segmented PESTLE summary of Mayer Steel Pipe that’s easily droppable into presentations and shared across teams, helping stakeholders quickly align on external risks, market positioning and action points during planning sessions.

Economic factors

Raw material price volatility

Hot-rolled coil, billet and scrap dominate Mayer Steel Pipe's COGS, and 2024–25 commodity swings produced double-digit percentage moves that quickly compress or expand spreads. Commodity cycles and supply shocks—notably regional scrap tightness in 2024—drive short-term margin volatility. Indexed contracts, flexible surcharges and multi-sourcing combined with tight inventory discipline have been used to preserve margins and reduce exposure.

Construction and industrial cycles

Pipeline demand closely follows building permits and capex trends: US building permits averaged about 1.4 million units in 2024 while manufacturing PMI dipped around the 50 mark for much of 2024, signaling tepid industrial activity. Slowdowns defer project starts, extending sales cycles and raising receivable and credit risk for Mayer Steel Pipe. Counter-cyclical maintenance and repair work, which rose in spend share during 2023–24 downturns, and product diversification help balance these cyclical swings.

Exchange rates and export competitiveness

FX movements affect Mayer Steel Pipe by changing imported input costs and export pricing; global FX turnover averaged about $7.5 trillion per day in April 2022 (BIS), underscoring market liquidity and volatility. A weaker home currency can boost overseas sales but raise input inflation, so currency-matched sourcing creates natural hedges. Formal hedging programs cut earnings volatility and stabilize margins during swings.

Interest rates and financing

- Working capital cost increase: +200–300 bps vs 2021

- Benchmark rates: Fed 5.25–5.50% (mid‑2025), RBI repo ~6.5% (2025)

- Customer financing tighter → order delays

- Focus: supplier credit terms, receivables insurance, shorter CCC

Logistics and freight economics

Ocean and domestic freight rates—after 2021 peaks above USD 10,000/FEU—normalized to roughly USD 2,000/FEU in 2024 (Drewry), lowering delivered costs but leaving lead-time volatility. Port congestion and US trucking shortages (ATA estimated shortfall ~80,000 drivers in 2022–23) continue to erode service levels. Nearshoring to Mexico and regional hubs has improved reliability, while digital freight-visibility adoption (major providers report >60% carrier/shipper uptake by 2024) optimizes routing and costs.

- Rates: Drewry ~USD 2,000/FEU (2024)

- Trucking shortfall: ~80,000 drivers (ATA, 2022–23)

- Nearshoring: rising Mexico/region volumes (2023–24)

- Visibility: >60% adoption of digital tools (2024)

Tariffs, 57% China steel share and local-content rules reshape pipe pricing

Commodity swings (HRC, billet, scrap) drove double‑digit margin moves in 2024–25; indexed contracts, surcharges and tight inventories limited exposure. Construction permits ~1.4M units (2024) and PMI ~50 tempered pipeline demand, extending sales cycles and credit risk. Higher rates (Fed 5.25–5.50% mid‑2025; RBI ~6.5% 2025) raised working‑capital cost ~+200–300 bps, increasing focus on receivables insurance and shorter CCC.

| Metric | Value |

|---|---|

| Building permits (US, 2024) | ~1.4M units |

| Fed funds (mid‑2025) | 5.25–5.50% |

| RBI repo (2025) | ~6.5% |

| Ocean rates (2024) | ~USD 2,000/FEU |

| WC funding cost vs 2021 | +200–300 bps |

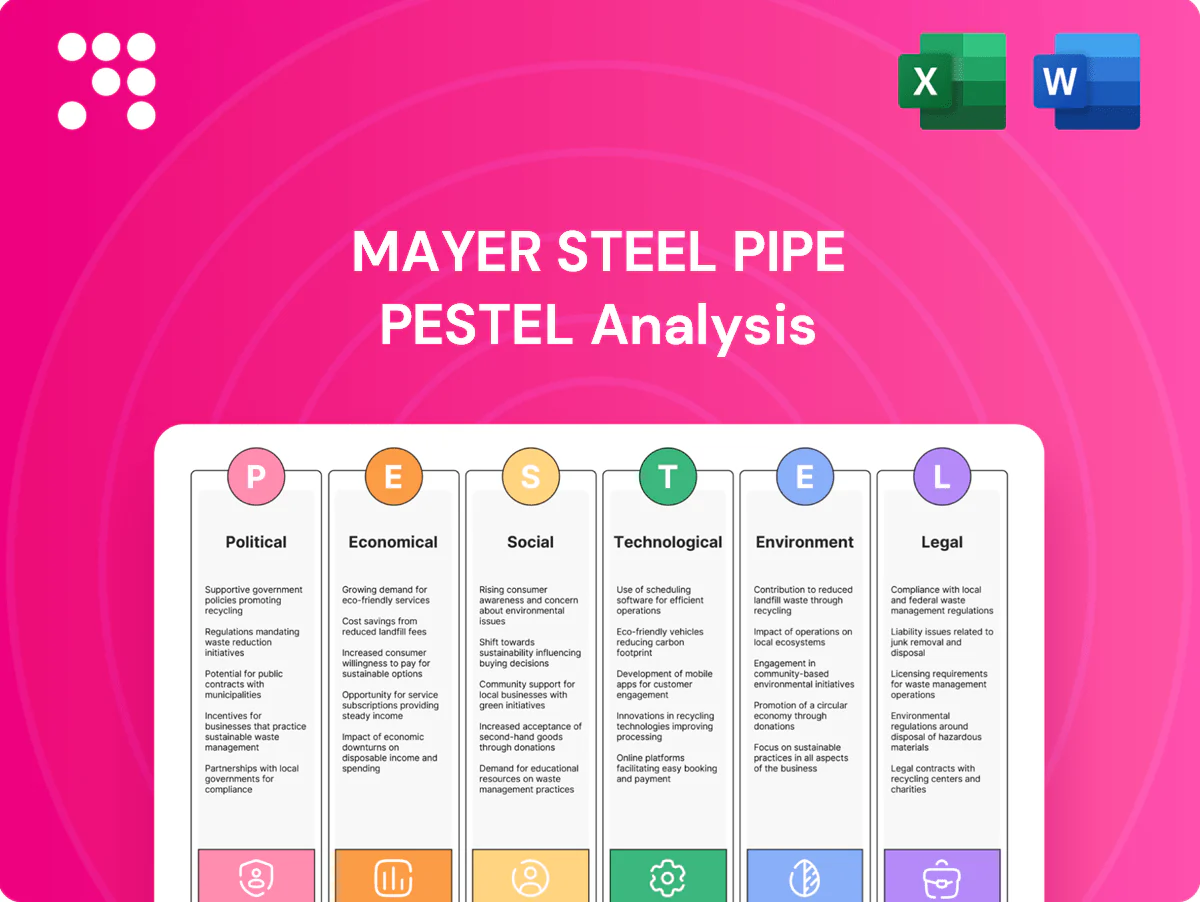

Preview Before You Purchase

Mayer Steel Pipe PESTLE Analysis

The preview shown here is the exact Mayer Steel Pipe PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying and the content, structure, and layout match the downloadable file. No placeholders or teasers: the file is complete and professionally structured. After payment you’ll instantly receive this same final document.

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape Mayer Steel Pipe’s strategic outlook in our concise PESTLE snapshot. Ideal for investors, consultants, and managers, this brief highlights key external risks and opportunities you can act on immediately. Purchase the full PESTLE analysis to access detailed insights, data tables, and actionable recommendations for confident decision-making.

Political factors

Trade policy and tariffs

Import duties such as the US Section 232 25% steel tariff and other country-level levies materially shape Mayer Steel Pipe price competitiveness across markets. Sudden tariff hikes or anti-dumping measures have repeatedly disrupted sourcing and route-to-market plans, especially given China’s 57% share of global crude steel output (World Steel Association 2023). Proactive hedging of supply sources and localized finishing can mitigate policy shocks, while close monitoring of bilateral trade agreements is essential to protect margins.

Infrastructure spending priorities

Government-funded construction and utilities form Mayer Steel Pipe’s baseline demand, with major programs such as the US Bipartisan Infrastructure Law committing about 550 billion USD of new federal investment driving sustained pipe volumes. Shifts in budgets toward water, energy and transport change product mix and can swing annual volumes by double-digit percentages on large contracts. Public–private partnerships and improved advocacy and tender readiness raise win rates and accelerate project pipelines across regions.

Political stability and security

Political stability directly affects project execution, logistics safety and investor confidence; global FDI fell 12% to about $1.02 trillion in 2023 (UNCTAD), illustrating sensitivity to instability. Elections and policy transitions commonly delay approvals and public works; geopolitical tensions raise freight insurance and rerouting costs. Diversifying end-markets and staging inventory buffers reduce exposure.

Local content and industrial policy

Local content mandates and buy-local rules—often setting thresholds in the 30–60% range—affect Mayer Steel Pipe’s sourcing, certification costs and pricing power while driving demand for domestic inputs.

2024–25 incentives for domestic manufacturing (tax credits, capital subsidies) can justify capex in mills and coating lines; compliance opens preferential tenders but raises audit and reporting burdens.

Strategic JVs or tolling arrangements provide efficient routes to meet content thresholds without full upstream investment.

- Impact: higher sourcing/certification costs

- Incentives: capex support for mills/coating lines

- Access: preferential tenders vs audit burden

- Mitigation: JV/tolling to meet thresholds

Energy policy and subsidies

Power tariffs, fuel taxes and grid reliability materially affect Mayer Steel Pipe mill costs—industrial electricity often drives 15–25% of OPEX and unplanned outages raise per-ton costs; fuel levies (e.g., diesel excise) further squeeze margins. Subsidies for pipeline gas or renewables can cut EAF and heat-treatment energy spend; in 2024 corporate renewable PPAs reached prices as low as $20/MWh (~2 c/kWh). Policy-driven energy transitions will likely force capital expenditure for boiler/electric arc furnace upgrades and grid-interactive controls, while long-term PPAs stabilize cost curves and hedge volatility.

- Tariff exposure: high OPEX share

- Subsidies: lower EAF/heat costs

- Capex: equipment upgrades required

- PPAs: price stability (as low as $20/MWh in 2024)

Tariffs, 57% China steel share and local-content rules reshape pipe pricing

Import tariffs (eg US Section 232 25%) and anti-dumping actions plus China’s 57% share of crude steel (World Steel Association 2023) materially affect Mayer Steel Pipe pricing and sourcing. Government infrastructure spend (US Bipartisan Infrastructure Law ~550 billion USD) and local-content rules (commonly 30–60%) shape demand and bid access. Energy policy, PPAs as low as $20/MWh (2024), and political instability (FDI $1.02T 2023) drive OPEX, capex and route-to-market risk.

| Factor | Key stat | Impact |

|---|---|---|

| Tariffs | US 25% | Price competitiveness |

| Demand | 550B USD | Volume upside |

| Local content | 30–60% | Sourcing/certification |

| Energy | $20/MWh | Lower OPEX |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Mayer Steel Pipe, with data-backed trends and region-specific regulatory insights; designed for executives and investors to identify risks, opportunities and forward-looking scenarios ready for inclusion in plans, decks, or reports.

A clean, visually segmented PESTLE summary of Mayer Steel Pipe that’s easily droppable into presentations and shared across teams, helping stakeholders quickly align on external risks, market positioning and action points during planning sessions.

Economic factors

Raw material price volatility

Hot-rolled coil, billet and scrap dominate Mayer Steel Pipe's COGS, and 2024–25 commodity swings produced double-digit percentage moves that quickly compress or expand spreads. Commodity cycles and supply shocks—notably regional scrap tightness in 2024—drive short-term margin volatility. Indexed contracts, flexible surcharges and multi-sourcing combined with tight inventory discipline have been used to preserve margins and reduce exposure.

Construction and industrial cycles

Pipeline demand closely follows building permits and capex trends: US building permits averaged about 1.4 million units in 2024 while manufacturing PMI dipped around the 50 mark for much of 2024, signaling tepid industrial activity. Slowdowns defer project starts, extending sales cycles and raising receivable and credit risk for Mayer Steel Pipe. Counter-cyclical maintenance and repair work, which rose in spend share during 2023–24 downturns, and product diversification help balance these cyclical swings.

Exchange rates and export competitiveness

FX movements affect Mayer Steel Pipe by changing imported input costs and export pricing; global FX turnover averaged about $7.5 trillion per day in April 2022 (BIS), underscoring market liquidity and volatility. A weaker home currency can boost overseas sales but raise input inflation, so currency-matched sourcing creates natural hedges. Formal hedging programs cut earnings volatility and stabilize margins during swings.

Interest rates and financing

- Working capital cost increase: +200–300 bps vs 2021

- Benchmark rates: Fed 5.25–5.50% (mid‑2025), RBI repo ~6.5% (2025)

- Customer financing tighter → order delays

- Focus: supplier credit terms, receivables insurance, shorter CCC

Logistics and freight economics

Ocean and domestic freight rates—after 2021 peaks above USD 10,000/FEU—normalized to roughly USD 2,000/FEU in 2024 (Drewry), lowering delivered costs but leaving lead-time volatility. Port congestion and US trucking shortages (ATA estimated shortfall ~80,000 drivers in 2022–23) continue to erode service levels. Nearshoring to Mexico and regional hubs has improved reliability, while digital freight-visibility adoption (major providers report >60% carrier/shipper uptake by 2024) optimizes routing and costs.

- Rates: Drewry ~USD 2,000/FEU (2024)

- Trucking shortfall: ~80,000 drivers (ATA, 2022–23)

- Nearshoring: rising Mexico/region volumes (2023–24)

- Visibility: >60% adoption of digital tools (2024)

Tariffs, 57% China steel share and local-content rules reshape pipe pricing

Commodity swings (HRC, billet, scrap) drove double‑digit margin moves in 2024–25; indexed contracts, surcharges and tight inventories limited exposure. Construction permits ~1.4M units (2024) and PMI ~50 tempered pipeline demand, extending sales cycles and credit risk. Higher rates (Fed 5.25–5.50% mid‑2025; RBI ~6.5% 2025) raised working‑capital cost ~+200–300 bps, increasing focus on receivables insurance and shorter CCC.

| Metric | Value |

|---|---|

| Building permits (US, 2024) | ~1.4M units |

| Fed funds (mid‑2025) | 5.25–5.50% |

| RBI repo (2025) | ~6.5% |

| Ocean rates (2024) | ~USD 2,000/FEU |

| WC funding cost vs 2021 | +200–300 bps |

Preview Before You Purchase

Mayer Steel Pipe PESTLE Analysis

The preview shown here is the exact Mayer Steel Pipe PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying and the content, structure, and layout match the downloadable file. No placeholders or teasers: the file is complete and professionally structured. After payment you’ll instantly receive this same final document.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Discover how political shifts, economic cycles, social trends, technological advances, legal changes, and environmental pressures shape Mayer Steel Pipe’s strategic outlook in our concise PESTLE snapshot. Ideal for investors, consultants, and managers, this brief highlights key external risks and opportunities you can act on immediately. Purchase the full PESTLE analysis to access detailed insights, data tables, and actionable recommendations for confident decision-making.

Political factors

Trade policy and tariffs

Import duties such as the US Section 232 25% steel tariff and other country-level levies materially shape Mayer Steel Pipe price competitiveness across markets. Sudden tariff hikes or anti-dumping measures have repeatedly disrupted sourcing and route-to-market plans, especially given China’s 57% share of global crude steel output (World Steel Association 2023). Proactive hedging of supply sources and localized finishing can mitigate policy shocks, while close monitoring of bilateral trade agreements is essential to protect margins.

Infrastructure spending priorities

Government-funded construction and utilities form Mayer Steel Pipe’s baseline demand, with major programs such as the US Bipartisan Infrastructure Law committing about 550 billion USD of new federal investment driving sustained pipe volumes. Shifts in budgets toward water, energy and transport change product mix and can swing annual volumes by double-digit percentages on large contracts. Public–private partnerships and improved advocacy and tender readiness raise win rates and accelerate project pipelines across regions.

Political stability and security

Political stability directly affects project execution, logistics safety and investor confidence; global FDI fell 12% to about $1.02 trillion in 2023 (UNCTAD), illustrating sensitivity to instability. Elections and policy transitions commonly delay approvals and public works; geopolitical tensions raise freight insurance and rerouting costs. Diversifying end-markets and staging inventory buffers reduce exposure.

Local content and industrial policy

Local content mandates and buy-local rules—often setting thresholds in the 30–60% range—affect Mayer Steel Pipe’s sourcing, certification costs and pricing power while driving demand for domestic inputs.

2024–25 incentives for domestic manufacturing (tax credits, capital subsidies) can justify capex in mills and coating lines; compliance opens preferential tenders but raises audit and reporting burdens.

Strategic JVs or tolling arrangements provide efficient routes to meet content thresholds without full upstream investment.

- Impact: higher sourcing/certification costs

- Incentives: capex support for mills/coating lines

- Access: preferential tenders vs audit burden

- Mitigation: JV/tolling to meet thresholds

Energy policy and subsidies

Power tariffs, fuel taxes and grid reliability materially affect Mayer Steel Pipe mill costs—industrial electricity often drives 15–25% of OPEX and unplanned outages raise per-ton costs; fuel levies (e.g., diesel excise) further squeeze margins. Subsidies for pipeline gas or renewables can cut EAF and heat-treatment energy spend; in 2024 corporate renewable PPAs reached prices as low as $20/MWh (~2 c/kWh). Policy-driven energy transitions will likely force capital expenditure for boiler/electric arc furnace upgrades and grid-interactive controls, while long-term PPAs stabilize cost curves and hedge volatility.

- Tariff exposure: high OPEX share

- Subsidies: lower EAF/heat costs

- Capex: equipment upgrades required

- PPAs: price stability (as low as $20/MWh in 2024)

Tariffs, 57% China steel share and local-content rules reshape pipe pricing

Import tariffs (eg US Section 232 25%) and anti-dumping actions plus China’s 57% share of crude steel (World Steel Association 2023) materially affect Mayer Steel Pipe pricing and sourcing. Government infrastructure spend (US Bipartisan Infrastructure Law ~550 billion USD) and local-content rules (commonly 30–60%) shape demand and bid access. Energy policy, PPAs as low as $20/MWh (2024), and political instability (FDI $1.02T 2023) drive OPEX, capex and route-to-market risk.

| Factor | Key stat | Impact |

|---|---|---|

| Tariffs | US 25% | Price competitiveness |

| Demand | 550B USD | Volume upside |

| Local content | 30–60% | Sourcing/certification |

| Energy | $20/MWh | Lower OPEX |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely impact Mayer Steel Pipe, with data-backed trends and region-specific regulatory insights; designed for executives and investors to identify risks, opportunities and forward-looking scenarios ready for inclusion in plans, decks, or reports.

A clean, visually segmented PESTLE summary of Mayer Steel Pipe that’s easily droppable into presentations and shared across teams, helping stakeholders quickly align on external risks, market positioning and action points during planning sessions.

Economic factors

Raw material price volatility

Hot-rolled coil, billet and scrap dominate Mayer Steel Pipe's COGS, and 2024–25 commodity swings produced double-digit percentage moves that quickly compress or expand spreads. Commodity cycles and supply shocks—notably regional scrap tightness in 2024—drive short-term margin volatility. Indexed contracts, flexible surcharges and multi-sourcing combined with tight inventory discipline have been used to preserve margins and reduce exposure.

Construction and industrial cycles

Pipeline demand closely follows building permits and capex trends: US building permits averaged about 1.4 million units in 2024 while manufacturing PMI dipped around the 50 mark for much of 2024, signaling tepid industrial activity. Slowdowns defer project starts, extending sales cycles and raising receivable and credit risk for Mayer Steel Pipe. Counter-cyclical maintenance and repair work, which rose in spend share during 2023–24 downturns, and product diversification help balance these cyclical swings.

Exchange rates and export competitiveness

FX movements affect Mayer Steel Pipe by changing imported input costs and export pricing; global FX turnover averaged about $7.5 trillion per day in April 2022 (BIS), underscoring market liquidity and volatility. A weaker home currency can boost overseas sales but raise input inflation, so currency-matched sourcing creates natural hedges. Formal hedging programs cut earnings volatility and stabilize margins during swings.

Interest rates and financing

- Working capital cost increase: +200–300 bps vs 2021

- Benchmark rates: Fed 5.25–5.50% (mid‑2025), RBI repo ~6.5% (2025)

- Customer financing tighter → order delays

- Focus: supplier credit terms, receivables insurance, shorter CCC

Logistics and freight economics

Ocean and domestic freight rates—after 2021 peaks above USD 10,000/FEU—normalized to roughly USD 2,000/FEU in 2024 (Drewry), lowering delivered costs but leaving lead-time volatility. Port congestion and US trucking shortages (ATA estimated shortfall ~80,000 drivers in 2022–23) continue to erode service levels. Nearshoring to Mexico and regional hubs has improved reliability, while digital freight-visibility adoption (major providers report >60% carrier/shipper uptake by 2024) optimizes routing and costs.

- Rates: Drewry ~USD 2,000/FEU (2024)

- Trucking shortfall: ~80,000 drivers (ATA, 2022–23)

- Nearshoring: rising Mexico/region volumes (2023–24)

- Visibility: >60% adoption of digital tools (2024)

Tariffs, 57% China steel share and local-content rules reshape pipe pricing

Commodity swings (HRC, billet, scrap) drove double‑digit margin moves in 2024–25; indexed contracts, surcharges and tight inventories limited exposure. Construction permits ~1.4M units (2024) and PMI ~50 tempered pipeline demand, extending sales cycles and credit risk. Higher rates (Fed 5.25–5.50% mid‑2025; RBI ~6.5% 2025) raised working‑capital cost ~+200–300 bps, increasing focus on receivables insurance and shorter CCC.

| Metric | Value |

|---|---|

| Building permits (US, 2024) | ~1.4M units |

| Fed funds (mid‑2025) | 5.25–5.50% |

| RBI repo (2025) | ~6.5% |

| Ocean rates (2024) | ~USD 2,000/FEU |

| WC funding cost vs 2021 | +200–300 bps |

Preview Before You Purchase

Mayer Steel Pipe PESTLE Analysis

The preview shown here is the exact Mayer Steel Pipe PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. This is a real screenshot of the product you’re buying and the content, structure, and layout match the downloadable file. No placeholders or teasers: the file is complete and professionally structured. After payment you’ll instantly receive this same final document.