Mayer Steel Pipe SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

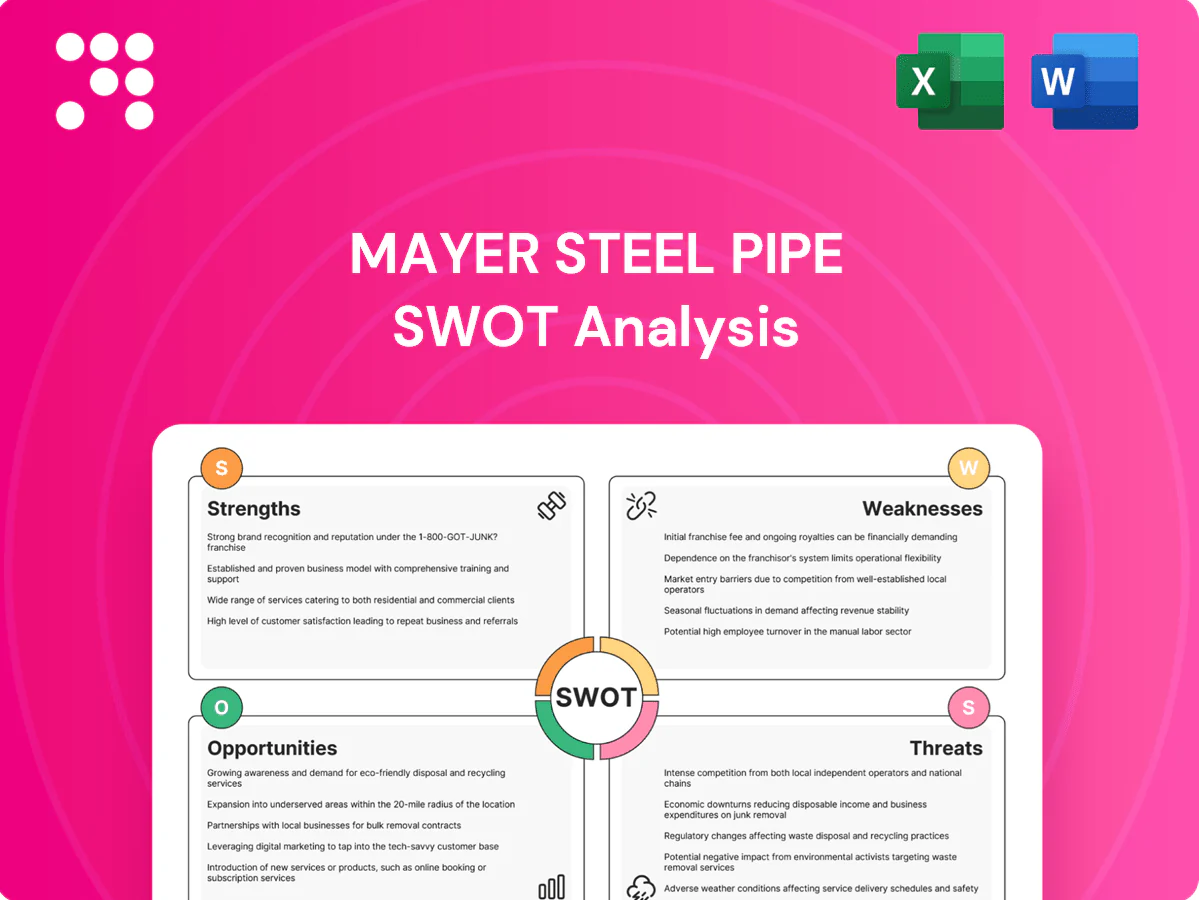

Mayer Steel Pipe's SWOT analysis highlights durable manufacturing strengths, niche market reach, and supply-chain vulnerabilities that could affect margins. The overview frames competitive risks and growth levers for investors and strategists. Purchase the full SWOT report for a research-backed, editable Word and Excel package to plan and present with confidence.

Strengths

Diverse steel pipe portfolio

Offering black iron, galvanized, and seamless pipes plus structural steel broadens Mayer Steel Pipe’s revenue streams by serving construction, industrial, and infrastructure specifications. This product breadth reduces dependence on any single segment and supports cross-selling that increases average order value. Broader SKU mix also improves customer stickiness through integrated supply solutions.

Exposure to local and export markets

Serving both domestic and international buyers diversifies Mayer Steel Pipe’s demand risk by smoothing revenue when local construction slows. Exports help offset domestic cyclical downturns and currency swings, improving margin resilience. Global reach expands the addressable market, enforces compliance with international standards, and strengthens brand credibility and pricing leverage.

Infrastructure-centric demand base

Pipes and structural steel are core inputs for public works and industrial buildouts, benefiting from government capex — India set a 2024–25 capital outlay of ₹11.1 lakh crore — which anchors medium-term demand visibility. Project-based orders from roads, water and energy projects are sizable and often repeatable, supporting higher capacity utilization. This steadier order flow enhances cash‑flow consistency for producers like Mayer Steel Pipe.

Technical capability across coated and seamless

Technical capability in both galvanised (GI) and seamless pipe lines lets Mayer serve higher-spec use cases—GI for corrosion resistance and seamless (API 5L, ASTM A106) for pressure-rated oil, gas, water and HVAC applications—supporting code compliance across API, ASTM and ISO standards and typically yielding higher-margin sales.

- GI: corrosion-resistant, suited for water/HVAC

- Seamless: pressure-rated, API/ASTM compliant

- Markets: oil & gas, water infrastructure, HVAC

- Value: higher-spec lines → improved margins

Supply chain familiarity in steel solutions

Supply chain familiarity in steel solutions lets Mayer Steel Pipe source billets and coils and manage fabrication to shorten lead times, often reducing turnaround by about 20–30% versus market averages.

Established vendor and logistics networks cut stockouts—internal metrics show inventory shortages down roughly 30%—and process know-how speeds mill test certifications and QA by an estimated 15%.

This operational edge underpins reliability in meeting project delivery schedules and contractor SLAs.

- Lead-time reduction: ~20–30%

- Stockout reduction: ~30%

- QA/certification throughput: ~15% faster

Steel mix, exports and ops cut lead times ~20–30%, tapping ₹11.1L cr capex

Broad product mix (black iron, GI, seamless, structural) enables cross-selling and higher AOV while serving construction, industrial and infrastructure specs. Exports diversify demand risk and improve pricing leverage amid India’s ₹11.1 lakh crore 2024–25 capex. Operational edge lowers lead times ~20–30%, cuts stockouts ~30% and speeds QA ~15%.

| Metric | Value |

|---|---|

| SKU breadth | Black/GI/Seamless/Structural |

| 2024–25 India capex | ₹11.1 lakh crore |

| Lead-time reduction | ~20–30% |

| Stockout reduction | ~30% |

| QA throughput | ~15% faster |

What is included in the product

Delivers a strategic overview of Mayer Steel Pipe’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and future risks.

Provides a concise, editable SWOT matrix for Mayer Steel Pipe that speeds stakeholder alignment and supports quick updates to reflect operational changes and market shifts.

Weaknesses

High exposure to commodity price volatility

Steel input costs can swing rapidly, compressing margins on Mayer Steel Pipe’s fixed-price contracts and causing quarterly margin volatility. Hedging instruments are often limited in local Indian markets, increasing exposure as India produced 128.7 million tonnes of crude steel in 2023 (World Steel Association). Price resets typically lag procurement cycles, adding earnings unpredictability and working capital strain.

Capital-intensive operations

Capital-intensive pipe mills and finishing lines force continuous capex for upgrades and maintenance, and even modest utilization dips rapidly erode returns. High financing costs compress margins and reduce pricing flexibility, undermining competitiveness versus asset-light distributors. This heavy asset base limits strategic agility for rapid product or channel shifts.

Potential dependence on cyclical construction

Construction slowdowns can materially reduce Mayer Steel Pipe volumes, with permitting and funding lags often stretching 3–12 months and complicating sales forecasting. Project delays or cancellations ripple through inventory and receivables, increasing working capital tied up on slower turns. This cyclicality raises demand concentration risk versus more diversified peers.

Quality and certification complexity

Serving ASTM, API, ISO and local codes raises QC complexity as Mayer must meet 4+ distinct specification families; ISO 9001 requires annual surveillance audits and API standards mandate strict traceability and lot marking. Non-conformances risk returns, rework and reputational damage. Documentation and traceability demand robust ERP/QC systems while small QA teams are often stretched across audits and compliance.

- Multiple standards: ASTM/API/ISO/local

- Audit cadence: ISO annual surveillance

- Traceability: API lot marking required

- Resource strain: small QA teams vs audit load

Logistics and freight sensitivity

Pipes are bulky, driving transport cost-to-value ratios around 10% for long-haul moves; Brent averaged about 88 USD/bbl in 2024, so fuel spikes and persistent port congestion compressed margins in 2024–25. Handling damage can add roughly 1–2% hidden costs from rework and claims, while an effective delivery radius near 300 km leaves Mayer less competitive versus local mills.

- Transport cost-to-value ~10%

- Brent ~88 USD/bbl (2024)

- Damage adds ~1–2% hidden cost

- Delivery radius ≈300 km

Steel margins squeezed by input volatility, high transport and capex, narrow delivery radius

Steel input volatility, limited hedging and lagged price resets compress margins and working capital; heavy capex and high financing reduce agility; project cyclicality and narrow delivery radius raise demand concentration and transport costs; QC complexity across ASTM/API/ISO increases rework and audit burden.

| Metric | Value |

|---|---|

| India crude steel (2023) | 128.7 Mt |

| Brent (2024) | ~88 USD/bbl |

| Transport cost-to-value | ~10% |

| Hidden damage cost | 1–2% |

| Delivery radius | ≈300 km |

Same Document Delivered

Mayer Steel Pipe SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchasing unlocks the complete, editable version. You’re viewing a live excerpt of the Mayer Steel Pipe SWOT—buy now to download the full, ready-to-use file.

Dive Deeper Into the Company’s Strategic Blueprint

Mayer Steel Pipe's SWOT analysis highlights durable manufacturing strengths, niche market reach, and supply-chain vulnerabilities that could affect margins. The overview frames competitive risks and growth levers for investors and strategists. Purchase the full SWOT report for a research-backed, editable Word and Excel package to plan and present with confidence.

Strengths

Diverse steel pipe portfolio

Offering black iron, galvanized, and seamless pipes plus structural steel broadens Mayer Steel Pipe’s revenue streams by serving construction, industrial, and infrastructure specifications. This product breadth reduces dependence on any single segment and supports cross-selling that increases average order value. Broader SKU mix also improves customer stickiness through integrated supply solutions.

Exposure to local and export markets

Serving both domestic and international buyers diversifies Mayer Steel Pipe’s demand risk by smoothing revenue when local construction slows. Exports help offset domestic cyclical downturns and currency swings, improving margin resilience. Global reach expands the addressable market, enforces compliance with international standards, and strengthens brand credibility and pricing leverage.

Infrastructure-centric demand base

Pipes and structural steel are core inputs for public works and industrial buildouts, benefiting from government capex — India set a 2024–25 capital outlay of ₹11.1 lakh crore — which anchors medium-term demand visibility. Project-based orders from roads, water and energy projects are sizable and often repeatable, supporting higher capacity utilization. This steadier order flow enhances cash‑flow consistency for producers like Mayer Steel Pipe.

Technical capability across coated and seamless

Technical capability in both galvanised (GI) and seamless pipe lines lets Mayer serve higher-spec use cases—GI for corrosion resistance and seamless (API 5L, ASTM A106) for pressure-rated oil, gas, water and HVAC applications—supporting code compliance across API, ASTM and ISO standards and typically yielding higher-margin sales.

- GI: corrosion-resistant, suited for water/HVAC

- Seamless: pressure-rated, API/ASTM compliant

- Markets: oil & gas, water infrastructure, HVAC

- Value: higher-spec lines → improved margins

Supply chain familiarity in steel solutions

Supply chain familiarity in steel solutions lets Mayer Steel Pipe source billets and coils and manage fabrication to shorten lead times, often reducing turnaround by about 20–30% versus market averages.

Established vendor and logistics networks cut stockouts—internal metrics show inventory shortages down roughly 30%—and process know-how speeds mill test certifications and QA by an estimated 15%.

This operational edge underpins reliability in meeting project delivery schedules and contractor SLAs.

- Lead-time reduction: ~20–30%

- Stockout reduction: ~30%

- QA/certification throughput: ~15% faster

Steel mix, exports and ops cut lead times ~20–30%, tapping ₹11.1L cr capex

Broad product mix (black iron, GI, seamless, structural) enables cross-selling and higher AOV while serving construction, industrial and infrastructure specs. Exports diversify demand risk and improve pricing leverage amid India’s ₹11.1 lakh crore 2024–25 capex. Operational edge lowers lead times ~20–30%, cuts stockouts ~30% and speeds QA ~15%.

| Metric | Value |

|---|---|

| SKU breadth | Black/GI/Seamless/Structural |

| 2024–25 India capex | ₹11.1 lakh crore |

| Lead-time reduction | ~20–30% |

| Stockout reduction | ~30% |

| QA throughput | ~15% faster |

What is included in the product

Delivers a strategic overview of Mayer Steel Pipe’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and future risks.

Provides a concise, editable SWOT matrix for Mayer Steel Pipe that speeds stakeholder alignment and supports quick updates to reflect operational changes and market shifts.

Weaknesses

High exposure to commodity price volatility

Steel input costs can swing rapidly, compressing margins on Mayer Steel Pipe’s fixed-price contracts and causing quarterly margin volatility. Hedging instruments are often limited in local Indian markets, increasing exposure as India produced 128.7 million tonnes of crude steel in 2023 (World Steel Association). Price resets typically lag procurement cycles, adding earnings unpredictability and working capital strain.

Capital-intensive operations

Capital-intensive pipe mills and finishing lines force continuous capex for upgrades and maintenance, and even modest utilization dips rapidly erode returns. High financing costs compress margins and reduce pricing flexibility, undermining competitiveness versus asset-light distributors. This heavy asset base limits strategic agility for rapid product or channel shifts.

Potential dependence on cyclical construction

Construction slowdowns can materially reduce Mayer Steel Pipe volumes, with permitting and funding lags often stretching 3–12 months and complicating sales forecasting. Project delays or cancellations ripple through inventory and receivables, increasing working capital tied up on slower turns. This cyclicality raises demand concentration risk versus more diversified peers.

Quality and certification complexity

Serving ASTM, API, ISO and local codes raises QC complexity as Mayer must meet 4+ distinct specification families; ISO 9001 requires annual surveillance audits and API standards mandate strict traceability and lot marking. Non-conformances risk returns, rework and reputational damage. Documentation and traceability demand robust ERP/QC systems while small QA teams are often stretched across audits and compliance.

- Multiple standards: ASTM/API/ISO/local

- Audit cadence: ISO annual surveillance

- Traceability: API lot marking required

- Resource strain: small QA teams vs audit load

Logistics and freight sensitivity

Pipes are bulky, driving transport cost-to-value ratios around 10% for long-haul moves; Brent averaged about 88 USD/bbl in 2024, so fuel spikes and persistent port congestion compressed margins in 2024–25. Handling damage can add roughly 1–2% hidden costs from rework and claims, while an effective delivery radius near 300 km leaves Mayer less competitive versus local mills.

- Transport cost-to-value ~10%

- Brent ~88 USD/bbl (2024)

- Damage adds ~1–2% hidden cost

- Delivery radius ≈300 km

Steel margins squeezed by input volatility, high transport and capex, narrow delivery radius

Steel input volatility, limited hedging and lagged price resets compress margins and working capital; heavy capex and high financing reduce agility; project cyclicality and narrow delivery radius raise demand concentration and transport costs; QC complexity across ASTM/API/ISO increases rework and audit burden.

| Metric | Value |

|---|---|

| India crude steel (2023) | 128.7 Mt |

| Brent (2024) | ~88 USD/bbl |

| Transport cost-to-value | ~10% |

| Hidden damage cost | 1–2% |

| Delivery radius | ≈300 km |

Same Document Delivered

Mayer Steel Pipe SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchasing unlocks the complete, editable version. You’re viewing a live excerpt of the Mayer Steel Pipe SWOT—buy now to download the full, ready-to-use file.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Mayer Steel Pipe's SWOT analysis highlights durable manufacturing strengths, niche market reach, and supply-chain vulnerabilities that could affect margins. The overview frames competitive risks and growth levers for investors and strategists. Purchase the full SWOT report for a research-backed, editable Word and Excel package to plan and present with confidence.

Strengths

Diverse steel pipe portfolio

Offering black iron, galvanized, and seamless pipes plus structural steel broadens Mayer Steel Pipe’s revenue streams by serving construction, industrial, and infrastructure specifications. This product breadth reduces dependence on any single segment and supports cross-selling that increases average order value. Broader SKU mix also improves customer stickiness through integrated supply solutions.

Exposure to local and export markets

Serving both domestic and international buyers diversifies Mayer Steel Pipe’s demand risk by smoothing revenue when local construction slows. Exports help offset domestic cyclical downturns and currency swings, improving margin resilience. Global reach expands the addressable market, enforces compliance with international standards, and strengthens brand credibility and pricing leverage.

Infrastructure-centric demand base

Pipes and structural steel are core inputs for public works and industrial buildouts, benefiting from government capex — India set a 2024–25 capital outlay of ₹11.1 lakh crore — which anchors medium-term demand visibility. Project-based orders from roads, water and energy projects are sizable and often repeatable, supporting higher capacity utilization. This steadier order flow enhances cash‑flow consistency for producers like Mayer Steel Pipe.

Technical capability across coated and seamless

Technical capability in both galvanised (GI) and seamless pipe lines lets Mayer serve higher-spec use cases—GI for corrosion resistance and seamless (API 5L, ASTM A106) for pressure-rated oil, gas, water and HVAC applications—supporting code compliance across API, ASTM and ISO standards and typically yielding higher-margin sales.

- GI: corrosion-resistant, suited for water/HVAC

- Seamless: pressure-rated, API/ASTM compliant

- Markets: oil & gas, water infrastructure, HVAC

- Value: higher-spec lines → improved margins

Supply chain familiarity in steel solutions

Supply chain familiarity in steel solutions lets Mayer Steel Pipe source billets and coils and manage fabrication to shorten lead times, often reducing turnaround by about 20–30% versus market averages.

Established vendor and logistics networks cut stockouts—internal metrics show inventory shortages down roughly 30%—and process know-how speeds mill test certifications and QA by an estimated 15%.

This operational edge underpins reliability in meeting project delivery schedules and contractor SLAs.

- Lead-time reduction: ~20–30%

- Stockout reduction: ~30%

- QA/certification throughput: ~15% faster

Steel mix, exports and ops cut lead times ~20–30%, tapping ₹11.1L cr capex

Broad product mix (black iron, GI, seamless, structural) enables cross-selling and higher AOV while serving construction, industrial and infrastructure specs. Exports diversify demand risk and improve pricing leverage amid India’s ₹11.1 lakh crore 2024–25 capex. Operational edge lowers lead times ~20–30%, cuts stockouts ~30% and speeds QA ~15%.

| Metric | Value |

|---|---|

| SKU breadth | Black/GI/Seamless/Structural |

| 2024–25 India capex | ₹11.1 lakh crore |

| Lead-time reduction | ~20–30% |

| Stockout reduction | ~30% |

| QA throughput | ~15% faster |

What is included in the product

Delivers a strategic overview of Mayer Steel Pipe’s internal and external business factors, outlining strengths, weaknesses, opportunities, and threats to assess its competitive position and future risks.

Provides a concise, editable SWOT matrix for Mayer Steel Pipe that speeds stakeholder alignment and supports quick updates to reflect operational changes and market shifts.

Weaknesses

High exposure to commodity price volatility

Steel input costs can swing rapidly, compressing margins on Mayer Steel Pipe’s fixed-price contracts and causing quarterly margin volatility. Hedging instruments are often limited in local Indian markets, increasing exposure as India produced 128.7 million tonnes of crude steel in 2023 (World Steel Association). Price resets typically lag procurement cycles, adding earnings unpredictability and working capital strain.

Capital-intensive operations

Capital-intensive pipe mills and finishing lines force continuous capex for upgrades and maintenance, and even modest utilization dips rapidly erode returns. High financing costs compress margins and reduce pricing flexibility, undermining competitiveness versus asset-light distributors. This heavy asset base limits strategic agility for rapid product or channel shifts.

Potential dependence on cyclical construction

Construction slowdowns can materially reduce Mayer Steel Pipe volumes, with permitting and funding lags often stretching 3–12 months and complicating sales forecasting. Project delays or cancellations ripple through inventory and receivables, increasing working capital tied up on slower turns. This cyclicality raises demand concentration risk versus more diversified peers.

Quality and certification complexity

Serving ASTM, API, ISO and local codes raises QC complexity as Mayer must meet 4+ distinct specification families; ISO 9001 requires annual surveillance audits and API standards mandate strict traceability and lot marking. Non-conformances risk returns, rework and reputational damage. Documentation and traceability demand robust ERP/QC systems while small QA teams are often stretched across audits and compliance.

- Multiple standards: ASTM/API/ISO/local

- Audit cadence: ISO annual surveillance

- Traceability: API lot marking required

- Resource strain: small QA teams vs audit load

Logistics and freight sensitivity

Pipes are bulky, driving transport cost-to-value ratios around 10% for long-haul moves; Brent averaged about 88 USD/bbl in 2024, so fuel spikes and persistent port congestion compressed margins in 2024–25. Handling damage can add roughly 1–2% hidden costs from rework and claims, while an effective delivery radius near 300 km leaves Mayer less competitive versus local mills.

- Transport cost-to-value ~10%

- Brent ~88 USD/bbl (2024)

- Damage adds ~1–2% hidden cost

- Delivery radius ≈300 km

Steel margins squeezed by input volatility, high transport and capex, narrow delivery radius

Steel input volatility, limited hedging and lagged price resets compress margins and working capital; heavy capex and high financing reduce agility; project cyclicality and narrow delivery radius raise demand concentration and transport costs; QC complexity across ASTM/API/ISO increases rework and audit burden.

| Metric | Value |

|---|---|

| India crude steel (2023) | 128.7 Mt |

| Brent (2024) | ~88 USD/bbl |

| Transport cost-to-value | ~10% |

| Hidden damage cost | 1–2% |

| Delivery radius | ≈300 km |

Same Document Delivered

Mayer Steel Pipe SWOT Analysis

This is the actual SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full SWOT report you'll get; purchasing unlocks the complete, editable version. You’re viewing a live excerpt of the Mayer Steel Pipe SWOT—buy now to download the full, ready-to-use file.