McCarthy Holdings Porter's Five Forces Analysis

Don't Miss the Bigger Picture

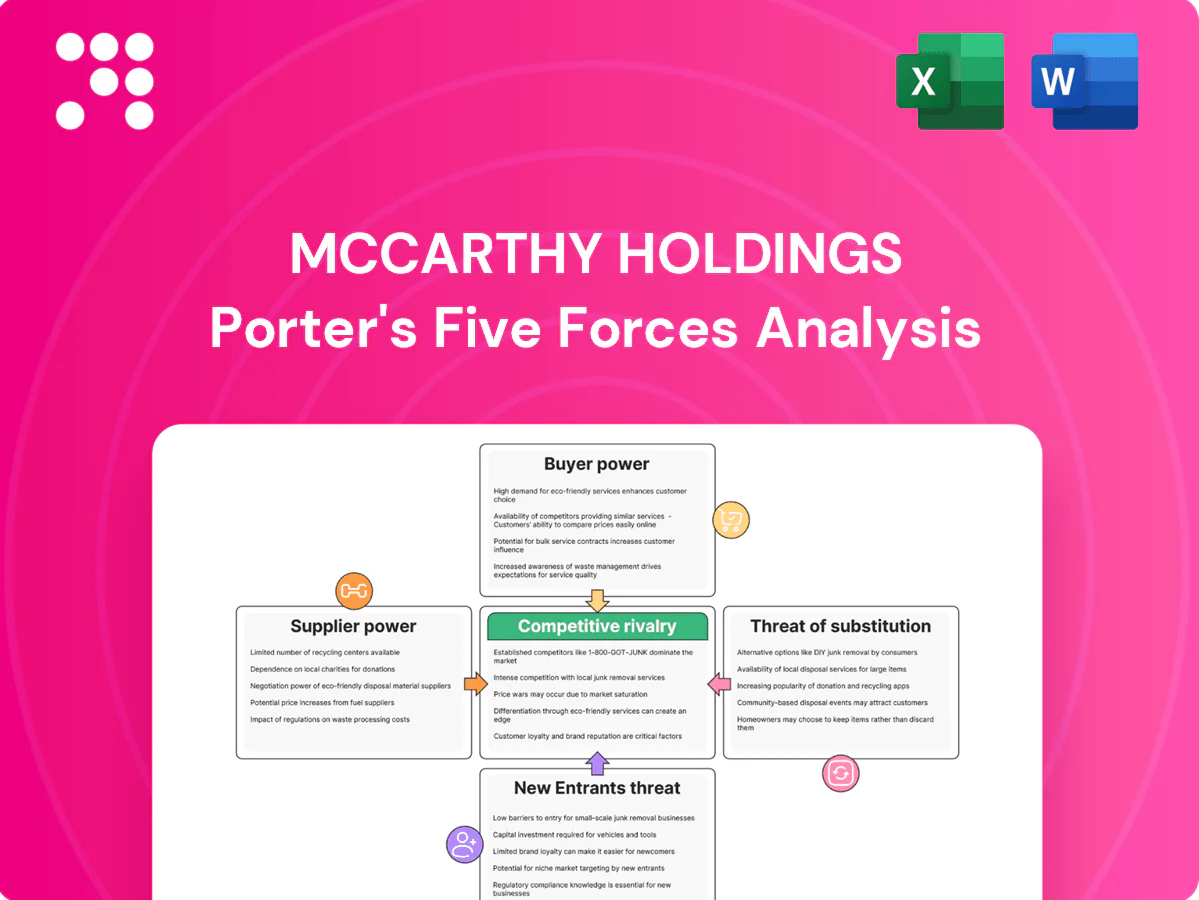

McCarthy Holdings faces moderate supplier and buyer power, high industry rivalry, and evolving substitute and entrant pressures driven by construction tech and regulated margins. This snapshot highlights strategic strengths in scale and backlog but also areas of vulnerability in labor and material cost exposure. Ready for deeper insights? Unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated critical materials

Structural steel, cement, and specialized medical-grade materials are supplied by a concentrated set of qualified vendors, giving suppliers leverage over price and lead times. Global commodity cycles and logistics chokepoints intermittently tighten availability and escalate costs. McCarthy mitigates risk through long-term agreements, value engineering, and early procurement. Project-spec constraints often limit substitution across equivalent materials.

Skilled labor and union trades

Unionized trades and scarce specialties (MEP, welders, controls) gain leverage in peak 2024 markets, with localized wage escalations often reaching high single digits and overtime driving costs; work rules can compress schedules and reduce productivity. McCarthy’s national scale, targeted training programs and preferred subcontractor network temper these pressures, but tight local labor markets can still shift bargaining power to trades.

Specialty subcontractors dependency

Complex healthcare, cleanroom, and renewable projects rely on niche subs with proprietary know‑how, creating high switching costs mid‑project and concentrated supplier leverage. McCarthy mitigates single‑point exposure via prequalification, multi‑bid strategies and design‑assist partnerships, while performance bonds (typically 1–3% of contract value) and incentive structures align delivery but cannot fully eliminate dependency.

Equipment and technology platforms

Equipment and technology platforms such as heavy equipment rental firms and BIM/VDC software vendors can push operating costs higher; the US equipment rental market surpassed 40 billion USD in 2024, increasing supplier leverage. Vendor lock-in, certification and training create switching frictions, while McCarthy reduces dependency through multi-vendor stacks, fleet planning and national sourcing agreements to preserve negotiating leverage.

- Rental market size: >40B USD (US, 2024)

- Switching friction: training + certification

- Mitigation: multi-vendor stacks, fleet planning

- Leverage: volume commitments, national contracts

Logistics and lead-time risks

- Lead-time ranges: switchgear 20–28w, chillers 12–30w, transformers 20–40w, inverters 12–24w

- Delay impact: 15–25% schedule slippage; 5–12% added labor/rework costs

- Mitigants: early coordination, procurement schedules, alternative suppliers, prefabrication

Supply tightness, long lead times and union labor drive 15–25% delays

Concentrated suppliers for steel, cement and specialty materials and 2024 commodity/logistics tightness give vendors price and timing leverage.

Unionized trades and niche subs (MEP, welders, controls) raise labor costs and switching friction; bonds 1–3% and McCarthy scale mitigate but do not eliminate risk.

US equipment rental >40B (2024); lead times (switchgear 20–28w, chillers 12–30w) drive 15–25% schedule slippage and 5–12% extra costs.

| Metric | 2024 Value |

|---|---|

| Equipment rental | >40B USD |

| Performance bonds | 1–3% |

| Lead times | switchgear 20–28w; chillers 12–30w |

| Delay impact | 15–25% slippage; 5–12% cost |

What is included in the product

Tailored Porter’s Five Forces for McCarthy Holdings revealing competitive intensity, supplier and buyer leverage, barriers deterring entrants, threats from substitutes and disruptors, and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for McCarthy Holdings—instantly reveal construction-sector pressures and where margins are most at risk. Customizable pressure levels and a ready-to-use radar view make it easy to slot into decks or dashboards for fast strategic decisions.

Customers Bargaining Power

Large institutional owners

Large institutional owners—roughly 6,000 U.S. hospitals, ~4,000 degree-granting colleges, and 500 Fortune 500 corporations—buy construction at scale and press for aggressive pricing and contract terms.

Their repeat volume and reputational pull boost negotiating power, but McCarthy leverages proven delivery on complex healthcare and campus projects and lifecycle value to defend margins.

Strong performance history and safety records materially temper pure price pressure.

Public sector and RFP-driven procurement

Transparent bidding, strict prequalification, and best-value scoring in public RFPs increase buyer leverage by making selection criteria and trade-offs explicit, allowing owners to demand contract structures, liquidated damages, and extended warranty obligations. McCarthy emphasizes technical approach, team composition, and documented past performance to win on factors beyond lowest price. Use of CMAR and design-build shifts procurement toward qualifications-driven selection, further pressuring margin capture through demonstrated delivery and risk mitigation.

Design-build and risk allocation

Integrated delivery shifts design and performance risks to the contractor, aligning cost incentives but increasing exposure for McCarthy; sophisticated owners increasingly demand fixed-price or GMP contracts that compress margins. McCarthy mitigates through robust preconstruction, target value design, and contingency planning, and collaborative execution has reduced downstream disputes and claims frequency, improving delivery outcomes for both parties.

Switching and multi-sourcing

Owners often maintain panels of GCs, creating project-by-project competitive tension; switching costs are moderate pre-award but become high once construction is underway, giving owners leverage early and contractors leverage mid-project. McCarthy pursues repeat awards via service quality and programmatic agreements, while post-project reviews and scorecards amplify buyer power when expectations fall short.

- Panel use: increases buyer leverage

- Switching costs: moderate pre-award, high mid-project

- McCarthy strategy: repeat awards through quality and programs

- Post-project reviews: decisive in future selection

Payment terms and cash flow

Owners extending pay cycles and imposing 5–10% retainage squeeze contractor working capital and elevate financing costs; audit rights and onerous documentation add administrative burden and days of delay. McCarthy leverages its balance-sheet strength and surety partnerships to absorb timing gaps, while the federal Prompt Payment Act and state prompt-pay laws plus milestone billing help mitigate cash-flow strain.

- Retainage: 5–10% industry norm

- Federal Prompt Payment Act: affects federal projects

- Surety/finance: liquidity buffer for McCarthy

- Milestone billing: reduces DSO pressure

Buyers wield pricing power; retainage 5–10% strains working capital

Large institutional owners (≈6,000 U.S. hospitals, ≈4,000 degree-granting colleges, 500 Fortune 500 firms) exert strong price and contract pressure; repeat volume and panels boost buyer leverage. McCarthy defends margins via proven delivery, safety record, CMAR/design-build expertise, and balance-sheet liquidity. Retainage (5–10%) and extended pay cycles raise working-capital costs; federal Prompt Payment Act aids federal projects.

| Metric | Value | Impact |

|---|---|---|

| Hospitals | ≈6,000 | High volume buyers |

| Colleges | ≈4,000 | Repeat campus programs |

| Retainage | 5–10% | Working-capital squeeze |

| Prompt Payment | Federal law | Improves federal cash flow |

Same Document Delivered

McCarthy Holdings Porter's Five Forces Analysis

This preview shows the exact McCarthy Holdings Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The file includes supplier and buyer power, competitive rivalry, threat of entry and substitutes, plus strategic implications and actionable insights, fully formatted and ready for download.

Don't Miss the Bigger Picture

McCarthy Holdings faces moderate supplier and buyer power, high industry rivalry, and evolving substitute and entrant pressures driven by construction tech and regulated margins. This snapshot highlights strategic strengths in scale and backlog but also areas of vulnerability in labor and material cost exposure. Ready for deeper insights? Unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated critical materials

Structural steel, cement, and specialized medical-grade materials are supplied by a concentrated set of qualified vendors, giving suppliers leverage over price and lead times. Global commodity cycles and logistics chokepoints intermittently tighten availability and escalate costs. McCarthy mitigates risk through long-term agreements, value engineering, and early procurement. Project-spec constraints often limit substitution across equivalent materials.

Skilled labor and union trades

Unionized trades and scarce specialties (MEP, welders, controls) gain leverage in peak 2024 markets, with localized wage escalations often reaching high single digits and overtime driving costs; work rules can compress schedules and reduce productivity. McCarthy’s national scale, targeted training programs and preferred subcontractor network temper these pressures, but tight local labor markets can still shift bargaining power to trades.

Specialty subcontractors dependency

Complex healthcare, cleanroom, and renewable projects rely on niche subs with proprietary know‑how, creating high switching costs mid‑project and concentrated supplier leverage. McCarthy mitigates single‑point exposure via prequalification, multi‑bid strategies and design‑assist partnerships, while performance bonds (typically 1–3% of contract value) and incentive structures align delivery but cannot fully eliminate dependency.

Equipment and technology platforms

Equipment and technology platforms such as heavy equipment rental firms and BIM/VDC software vendors can push operating costs higher; the US equipment rental market surpassed 40 billion USD in 2024, increasing supplier leverage. Vendor lock-in, certification and training create switching frictions, while McCarthy reduces dependency through multi-vendor stacks, fleet planning and national sourcing agreements to preserve negotiating leverage.

- Rental market size: >40B USD (US, 2024)

- Switching friction: training + certification

- Mitigation: multi-vendor stacks, fleet planning

- Leverage: volume commitments, national contracts

Logistics and lead-time risks

- Lead-time ranges: switchgear 20–28w, chillers 12–30w, transformers 20–40w, inverters 12–24w

- Delay impact: 15–25% schedule slippage; 5–12% added labor/rework costs

- Mitigants: early coordination, procurement schedules, alternative suppliers, prefabrication

Supply tightness, long lead times and union labor drive 15–25% delays

Concentrated suppliers for steel, cement and specialty materials and 2024 commodity/logistics tightness give vendors price and timing leverage.

Unionized trades and niche subs (MEP, welders, controls) raise labor costs and switching friction; bonds 1–3% and McCarthy scale mitigate but do not eliminate risk.

US equipment rental >40B (2024); lead times (switchgear 20–28w, chillers 12–30w) drive 15–25% schedule slippage and 5–12% extra costs.

| Metric | 2024 Value |

|---|---|

| Equipment rental | >40B USD |

| Performance bonds | 1–3% |

| Lead times | switchgear 20–28w; chillers 12–30w |

| Delay impact | 15–25% slippage; 5–12% cost |

What is included in the product

Tailored Porter’s Five Forces for McCarthy Holdings revealing competitive intensity, supplier and buyer leverage, barriers deterring entrants, threats from substitutes and disruptors, and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for McCarthy Holdings—instantly reveal construction-sector pressures and where margins are most at risk. Customizable pressure levels and a ready-to-use radar view make it easy to slot into decks or dashboards for fast strategic decisions.

Customers Bargaining Power

Large institutional owners

Large institutional owners—roughly 6,000 U.S. hospitals, ~4,000 degree-granting colleges, and 500 Fortune 500 corporations—buy construction at scale and press for aggressive pricing and contract terms.

Their repeat volume and reputational pull boost negotiating power, but McCarthy leverages proven delivery on complex healthcare and campus projects and lifecycle value to defend margins.

Strong performance history and safety records materially temper pure price pressure.

Public sector and RFP-driven procurement

Transparent bidding, strict prequalification, and best-value scoring in public RFPs increase buyer leverage by making selection criteria and trade-offs explicit, allowing owners to demand contract structures, liquidated damages, and extended warranty obligations. McCarthy emphasizes technical approach, team composition, and documented past performance to win on factors beyond lowest price. Use of CMAR and design-build shifts procurement toward qualifications-driven selection, further pressuring margin capture through demonstrated delivery and risk mitigation.

Design-build and risk allocation

Integrated delivery shifts design and performance risks to the contractor, aligning cost incentives but increasing exposure for McCarthy; sophisticated owners increasingly demand fixed-price or GMP contracts that compress margins. McCarthy mitigates through robust preconstruction, target value design, and contingency planning, and collaborative execution has reduced downstream disputes and claims frequency, improving delivery outcomes for both parties.

Switching and multi-sourcing

Owners often maintain panels of GCs, creating project-by-project competitive tension; switching costs are moderate pre-award but become high once construction is underway, giving owners leverage early and contractors leverage mid-project. McCarthy pursues repeat awards via service quality and programmatic agreements, while post-project reviews and scorecards amplify buyer power when expectations fall short.

- Panel use: increases buyer leverage

- Switching costs: moderate pre-award, high mid-project

- McCarthy strategy: repeat awards through quality and programs

- Post-project reviews: decisive in future selection

Payment terms and cash flow

Owners extending pay cycles and imposing 5–10% retainage squeeze contractor working capital and elevate financing costs; audit rights and onerous documentation add administrative burden and days of delay. McCarthy leverages its balance-sheet strength and surety partnerships to absorb timing gaps, while the federal Prompt Payment Act and state prompt-pay laws plus milestone billing help mitigate cash-flow strain.

- Retainage: 5–10% industry norm

- Federal Prompt Payment Act: affects federal projects

- Surety/finance: liquidity buffer for McCarthy

- Milestone billing: reduces DSO pressure

Buyers wield pricing power; retainage 5–10% strains working capital

Large institutional owners (≈6,000 U.S. hospitals, ≈4,000 degree-granting colleges, 500 Fortune 500 firms) exert strong price and contract pressure; repeat volume and panels boost buyer leverage. McCarthy defends margins via proven delivery, safety record, CMAR/design-build expertise, and balance-sheet liquidity. Retainage (5–10%) and extended pay cycles raise working-capital costs; federal Prompt Payment Act aids federal projects.

| Metric | Value | Impact |

|---|---|---|

| Hospitals | ≈6,000 | High volume buyers |

| Colleges | ≈4,000 | Repeat campus programs |

| Retainage | 5–10% | Working-capital squeeze |

| Prompt Payment | Federal law | Improves federal cash flow |

Same Document Delivered

McCarthy Holdings Porter's Five Forces Analysis

This preview shows the exact McCarthy Holdings Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The file includes supplier and buyer power, competitive rivalry, threat of entry and substitutes, plus strategic implications and actionable insights, fully formatted and ready for download.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

McCarthy Holdings faces moderate supplier and buyer power, high industry rivalry, and evolving substitute and entrant pressures driven by construction tech and regulated margins. This snapshot highlights strategic strengths in scale and backlog but also areas of vulnerability in labor and material cost exposure. Ready for deeper insights? Unlock the full Porter’s Five Forces Analysis to explore force-by-force ratings, visuals, and actionable recommendations.

Suppliers Bargaining Power

Concentrated critical materials

Structural steel, cement, and specialized medical-grade materials are supplied by a concentrated set of qualified vendors, giving suppliers leverage over price and lead times. Global commodity cycles and logistics chokepoints intermittently tighten availability and escalate costs. McCarthy mitigates risk through long-term agreements, value engineering, and early procurement. Project-spec constraints often limit substitution across equivalent materials.

Skilled labor and union trades

Unionized trades and scarce specialties (MEP, welders, controls) gain leverage in peak 2024 markets, with localized wage escalations often reaching high single digits and overtime driving costs; work rules can compress schedules and reduce productivity. McCarthy’s national scale, targeted training programs and preferred subcontractor network temper these pressures, but tight local labor markets can still shift bargaining power to trades.

Specialty subcontractors dependency

Complex healthcare, cleanroom, and renewable projects rely on niche subs with proprietary know‑how, creating high switching costs mid‑project and concentrated supplier leverage. McCarthy mitigates single‑point exposure via prequalification, multi‑bid strategies and design‑assist partnerships, while performance bonds (typically 1–3% of contract value) and incentive structures align delivery but cannot fully eliminate dependency.

Equipment and technology platforms

Equipment and technology platforms such as heavy equipment rental firms and BIM/VDC software vendors can push operating costs higher; the US equipment rental market surpassed 40 billion USD in 2024, increasing supplier leverage. Vendor lock-in, certification and training create switching frictions, while McCarthy reduces dependency through multi-vendor stacks, fleet planning and national sourcing agreements to preserve negotiating leverage.

- Rental market size: >40B USD (US, 2024)

- Switching friction: training + certification

- Mitigation: multi-vendor stacks, fleet planning

- Leverage: volume commitments, national contracts

Logistics and lead-time risks

- Lead-time ranges: switchgear 20–28w, chillers 12–30w, transformers 20–40w, inverters 12–24w

- Delay impact: 15–25% schedule slippage; 5–12% added labor/rework costs

- Mitigants: early coordination, procurement schedules, alternative suppliers, prefabrication

Supply tightness, long lead times and union labor drive 15–25% delays

Concentrated suppliers for steel, cement and specialty materials and 2024 commodity/logistics tightness give vendors price and timing leverage.

Unionized trades and niche subs (MEP, welders, controls) raise labor costs and switching friction; bonds 1–3% and McCarthy scale mitigate but do not eliminate risk.

US equipment rental >40B (2024); lead times (switchgear 20–28w, chillers 12–30w) drive 15–25% schedule slippage and 5–12% extra costs.

| Metric | 2024 Value |

|---|---|

| Equipment rental | >40B USD |

| Performance bonds | 1–3% |

| Lead times | switchgear 20–28w; chillers 12–30w |

| Delay impact | 15–25% slippage; 5–12% cost |

What is included in the product

Tailored Porter’s Five Forces for McCarthy Holdings revealing competitive intensity, supplier and buyer leverage, barriers deterring entrants, threats from substitutes and disruptors, and strategic implications for pricing and profitability.

A concise one-sheet Porter's Five Forces for McCarthy Holdings—instantly reveal construction-sector pressures and where margins are most at risk. Customizable pressure levels and a ready-to-use radar view make it easy to slot into decks or dashboards for fast strategic decisions.

Customers Bargaining Power

Large institutional owners

Large institutional owners—roughly 6,000 U.S. hospitals, ~4,000 degree-granting colleges, and 500 Fortune 500 corporations—buy construction at scale and press for aggressive pricing and contract terms.

Their repeat volume and reputational pull boost negotiating power, but McCarthy leverages proven delivery on complex healthcare and campus projects and lifecycle value to defend margins.

Strong performance history and safety records materially temper pure price pressure.

Public sector and RFP-driven procurement

Transparent bidding, strict prequalification, and best-value scoring in public RFPs increase buyer leverage by making selection criteria and trade-offs explicit, allowing owners to demand contract structures, liquidated damages, and extended warranty obligations. McCarthy emphasizes technical approach, team composition, and documented past performance to win on factors beyond lowest price. Use of CMAR and design-build shifts procurement toward qualifications-driven selection, further pressuring margin capture through demonstrated delivery and risk mitigation.

Design-build and risk allocation

Integrated delivery shifts design and performance risks to the contractor, aligning cost incentives but increasing exposure for McCarthy; sophisticated owners increasingly demand fixed-price or GMP contracts that compress margins. McCarthy mitigates through robust preconstruction, target value design, and contingency planning, and collaborative execution has reduced downstream disputes and claims frequency, improving delivery outcomes for both parties.

Switching and multi-sourcing

Owners often maintain panels of GCs, creating project-by-project competitive tension; switching costs are moderate pre-award but become high once construction is underway, giving owners leverage early and contractors leverage mid-project. McCarthy pursues repeat awards via service quality and programmatic agreements, while post-project reviews and scorecards amplify buyer power when expectations fall short.

- Panel use: increases buyer leverage

- Switching costs: moderate pre-award, high mid-project

- McCarthy strategy: repeat awards through quality and programs

- Post-project reviews: decisive in future selection

Payment terms and cash flow

Owners extending pay cycles and imposing 5–10% retainage squeeze contractor working capital and elevate financing costs; audit rights and onerous documentation add administrative burden and days of delay. McCarthy leverages its balance-sheet strength and surety partnerships to absorb timing gaps, while the federal Prompt Payment Act and state prompt-pay laws plus milestone billing help mitigate cash-flow strain.

- Retainage: 5–10% industry norm

- Federal Prompt Payment Act: affects federal projects

- Surety/finance: liquidity buffer for McCarthy

- Milestone billing: reduces DSO pressure

Buyers wield pricing power; retainage 5–10% strains working capital

Large institutional owners (≈6,000 U.S. hospitals, ≈4,000 degree-granting colleges, 500 Fortune 500 firms) exert strong price and contract pressure; repeat volume and panels boost buyer leverage. McCarthy defends margins via proven delivery, safety record, CMAR/design-build expertise, and balance-sheet liquidity. Retainage (5–10%) and extended pay cycles raise working-capital costs; federal Prompt Payment Act aids federal projects.

| Metric | Value | Impact |

|---|---|---|

| Hospitals | ≈6,000 | High volume buyers |

| Colleges | ≈4,000 | Repeat campus programs |

| Retainage | 5–10% | Working-capital squeeze |

| Prompt Payment | Federal law | Improves federal cash flow |

Same Document Delivered

McCarthy Holdings Porter's Five Forces Analysis

This preview shows the exact McCarthy Holdings Porter's Five Forces analysis you'll receive immediately after purchase—no surprises or placeholders. The file includes supplier and buyer power, competitive rivalry, threat of entry and substitutes, plus strategic implications and actionable insights, fully formatted and ready for download.