McDermott SWOT Analysis

Your Strategic Toolkit Starts Here

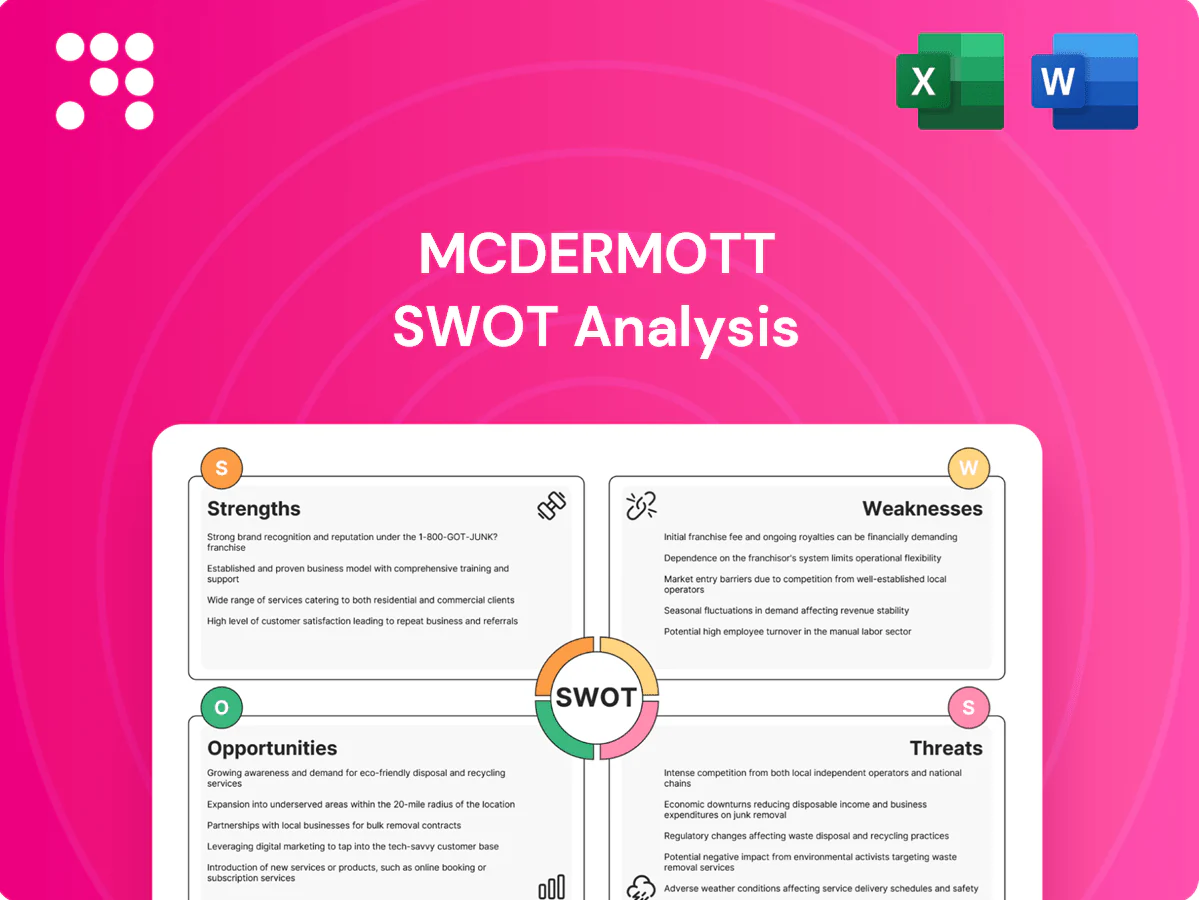

Explore McDermott's strategic position through our concise SWOT preview highlighting strengths, weaknesses, market risks and growth opportunities. Want the full picture with financial context, expert commentary and actionable strategy? Purchase the complete SWOT—editable Word and Excel deliverables ready for pitching, planning and investment decisions.

Strengths

Integrated EPCI capabilities

McDermott delivers engineering, procurement, construction and installation under one roof, reducing interfaces and schedule risk for clients and supporting turnkey execution from concept through commissioning. This integration drives cost and schedule synergies across phases, contributing to improved project predictability; the company reported a backlog of roughly $9.4 billion in mid-2024, reflecting strong demand for integrated EPCI. Clients value single-point accountability on complex offshore and onshore projects, simplifying risk transfer and contract management.

Deep offshore and subsea expertise

Founded in 1923, McDermott brings over a century of experience in fixed and floating production facilities, pipelines and subsea systems, with a proven track record in the Gulf of Mexico and North Sea. Specialized vessels, installation know‑how and repeatable methodologies enable execution in harsh environments. This capability underpins brownfield tie‑backs and greenfield developments and distinguishes McDermott on technically demanding scopes.

Global footprint and fabrication network

Strategically located yards and project offices across the Middle East, Asia and the Americas support regional content and logistics efficiency, enabling compliance with in-country value programs such as Saudi IKTVA and other national local content requirements. Local execution shortens lead times and improves responsiveness through closer client proximity. This footprint also diversifies revenue across multiple basins, reducing single-market exposure.

End-to-end lifecycle service

McDermott offers end-to-end lifecycle services from concept and FEED through detailed engineering, fabrication, installation and commissioning, enabling seamless handoffs and fewer claims from design–build disconnects. Lifecycle coverage drives repeat business and long-term client relationships and allows service bundling for margin uplift. McDermott reported fiscal 2024 revenue of $6.7 billion and a backlog near $9.5 billion.

- Scope: concept→commissioning

- Benefit: fewer claims, smoother handoffs

- Commercial: repeat clients, higher LTV

- Margin: bundling optionality

Reputation with NOCs and IOCs

McDermott serves major NOCs and IOCs on large LNG, offshore platform and pipeline programs, with a reported backlog of roughly $6.4 billion and about 11,000 employees as of 2024, reinforcing credibility on complex EPC delivery and long-cycle awards.

- Reputation: long-standing NOC/IOC relationships

- Project pedigree: LNG, offshore platforms, pipelines

- Systems: established prequalification and HSE

- Commercial: strong ties support sustained regional backlog

EPCI cuts interfaces; backlog ~9.5B

McDermott integrates EPCI to cut interfaces and schedule risk; backlog ~9.5B (mid‑2024). Century of experience and specialized vessels underpin LNG/offshore pedigree. Global yards enable local content compliance; FY2024 revenue 6.7B and ~11,000 employees.

| Metric | Value |

|---|---|

| Backlog | ~9.5B (mid‑2024) |

| FY2024 Revenue | 6.7B |

| Employees | ~11,000 |

What is included in the product

Provides a strategic overview of McDermott’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and risks shaping its future.

Provides a concise, executive-ready SWOT matrix for McDermott that clears analytical bottlenecks and enables rapid alignment of strategy and resource decisions.

Weaknesses

Exposure to oil and gas cyclicality

Revenue for McDermott is tightly tied to upstream and midstream capital spending cycles; when E&P capex weakens projects are delayed and awards fall, compressing margins and forcing competitive pricing. Volatile oil and gas demand complicates resource planning and vessel utilization, increasing idle time and costs. This dependence amplifies quarterly earnings variability for a company heavily exposed to hydrocarbon project flows.

Project execution and lump-sum risk

McDermott's EPCI focus leaves it exposed to fixed-price change-order risk and lump-sum losses; its 2020 Chapter 11 showed how single-project overruns can threaten the firm. Cost inflation and supply-chain delays continue to erode margins, with contractors pursuing multi-hundred-million-dollar claims and protracted recoveries. Robust risk management and claims resolution remain constant challenges.

Leverage and legacy restructuring overhang

Historical Chapter 11 in Jan 2020 with emergence in Jan 2021 has left leverage and legacy restructuring that constrain strategic flexibility; perceived credit risk has increased bonding scrutiny and limited bid capacity on large EPCI awards. Counterparties demand tighter payment and collateral terms, pressuring cash flow, while the overhang complicates talent retention and supplier negotiations.

Narrower technology ownership post-divestitures

Divestments have narrowed McDermott’s in-house proprietary process offerings, reducing captive IP that previously supported differentiation in onshore petrochemicals and integrated EPC bids; reliance on third-party licensors can compress margin levers and prolong bid cycles and approvals.

- Reduced proprietary IP

- Weaker differentiation in onshore petrochemicals

- Higher royalty/licensing dependence

- Longer bid cycles and approval timelines

Concentration in large, complex projects

Revenue is heavily concentrated in megaprojects with multi-year durations and milestone-based cash flows; in 2024 McDermott reported approximately $8.6 billion in revenue, with a large share tied to a handful of long-cycle contracts. Any dispute or delay can sharply strain working capital and liquidity when milestone receipts shift, and the firm’s ability to balance its portfolio with smaller, faster-turn projects is limited. This concentration elevates execution and counterparty risk, increasing volatility in margins and cash conversion.

- Concentration: majority of revenue from megaprojects

- Duration: contracts commonly span 2–5+ years

- Cashflow: milestone payments create liquidity spikes and gaps

- Risk: higher execution and counterparty exposure

Cyclical hydrocarbon megaproject player: 2024 revenue ~8.6B, overrun and bonding risks

McDermott’s revenue and margins are cyclical and concentrated in hydrocarbon megaprojects (2024 revenue ~$8.6B), exposing it to E&P capex swings, fixed‑price overrun risk (2020 Chapter 11 revealed vulnerability), legacy leverage limiting bonding/bid capacity, and reduced proprietary IP raising licensing costs and bid timelines.

| Weakness | Key data |

|---|---|

| Revenue concentration | 2024 revenue ~$8.6B; majority megaprojects |

| Bankruptcy legacy | Chapter 11 Jan 2020; emergence Jan 2021 |

| Contract risk | 2–5+ yr EPCI; fixed-price overruns |

Same Document Delivered

McDermott SWOT Analysis

This is the actual McDermott SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the structure, findings, and editable content included in the download. Buy now to unlock the complete, detailed version immediately after payment.

Your Strategic Toolkit Starts Here

Explore McDermott's strategic position through our concise SWOT preview highlighting strengths, weaknesses, market risks and growth opportunities. Want the full picture with financial context, expert commentary and actionable strategy? Purchase the complete SWOT—editable Word and Excel deliverables ready for pitching, planning and investment decisions.

Strengths

Integrated EPCI capabilities

McDermott delivers engineering, procurement, construction and installation under one roof, reducing interfaces and schedule risk for clients and supporting turnkey execution from concept through commissioning. This integration drives cost and schedule synergies across phases, contributing to improved project predictability; the company reported a backlog of roughly $9.4 billion in mid-2024, reflecting strong demand for integrated EPCI. Clients value single-point accountability on complex offshore and onshore projects, simplifying risk transfer and contract management.

Deep offshore and subsea expertise

Founded in 1923, McDermott brings over a century of experience in fixed and floating production facilities, pipelines and subsea systems, with a proven track record in the Gulf of Mexico and North Sea. Specialized vessels, installation know‑how and repeatable methodologies enable execution in harsh environments. This capability underpins brownfield tie‑backs and greenfield developments and distinguishes McDermott on technically demanding scopes.

Global footprint and fabrication network

Strategically located yards and project offices across the Middle East, Asia and the Americas support regional content and logistics efficiency, enabling compliance with in-country value programs such as Saudi IKTVA and other national local content requirements. Local execution shortens lead times and improves responsiveness through closer client proximity. This footprint also diversifies revenue across multiple basins, reducing single-market exposure.

End-to-end lifecycle service

McDermott offers end-to-end lifecycle services from concept and FEED through detailed engineering, fabrication, installation and commissioning, enabling seamless handoffs and fewer claims from design–build disconnects. Lifecycle coverage drives repeat business and long-term client relationships and allows service bundling for margin uplift. McDermott reported fiscal 2024 revenue of $6.7 billion and a backlog near $9.5 billion.

- Scope: concept→commissioning

- Benefit: fewer claims, smoother handoffs

- Commercial: repeat clients, higher LTV

- Margin: bundling optionality

Reputation with NOCs and IOCs

McDermott serves major NOCs and IOCs on large LNG, offshore platform and pipeline programs, with a reported backlog of roughly $6.4 billion and about 11,000 employees as of 2024, reinforcing credibility on complex EPC delivery and long-cycle awards.

- Reputation: long-standing NOC/IOC relationships

- Project pedigree: LNG, offshore platforms, pipelines

- Systems: established prequalification and HSE

- Commercial: strong ties support sustained regional backlog

EPCI cuts interfaces; backlog ~9.5B

McDermott integrates EPCI to cut interfaces and schedule risk; backlog ~9.5B (mid‑2024). Century of experience and specialized vessels underpin LNG/offshore pedigree. Global yards enable local content compliance; FY2024 revenue 6.7B and ~11,000 employees.

| Metric | Value |

|---|---|

| Backlog | ~9.5B (mid‑2024) |

| FY2024 Revenue | 6.7B |

| Employees | ~11,000 |

What is included in the product

Provides a strategic overview of McDermott’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and risks shaping its future.

Provides a concise, executive-ready SWOT matrix for McDermott that clears analytical bottlenecks and enables rapid alignment of strategy and resource decisions.

Weaknesses

Exposure to oil and gas cyclicality

Revenue for McDermott is tightly tied to upstream and midstream capital spending cycles; when E&P capex weakens projects are delayed and awards fall, compressing margins and forcing competitive pricing. Volatile oil and gas demand complicates resource planning and vessel utilization, increasing idle time and costs. This dependence amplifies quarterly earnings variability for a company heavily exposed to hydrocarbon project flows.

Project execution and lump-sum risk

McDermott's EPCI focus leaves it exposed to fixed-price change-order risk and lump-sum losses; its 2020 Chapter 11 showed how single-project overruns can threaten the firm. Cost inflation and supply-chain delays continue to erode margins, with contractors pursuing multi-hundred-million-dollar claims and protracted recoveries. Robust risk management and claims resolution remain constant challenges.

Leverage and legacy restructuring overhang

Historical Chapter 11 in Jan 2020 with emergence in Jan 2021 has left leverage and legacy restructuring that constrain strategic flexibility; perceived credit risk has increased bonding scrutiny and limited bid capacity on large EPCI awards. Counterparties demand tighter payment and collateral terms, pressuring cash flow, while the overhang complicates talent retention and supplier negotiations.

Narrower technology ownership post-divestitures

Divestments have narrowed McDermott’s in-house proprietary process offerings, reducing captive IP that previously supported differentiation in onshore petrochemicals and integrated EPC bids; reliance on third-party licensors can compress margin levers and prolong bid cycles and approvals.

- Reduced proprietary IP

- Weaker differentiation in onshore petrochemicals

- Higher royalty/licensing dependence

- Longer bid cycles and approval timelines

Concentration in large, complex projects

Revenue is heavily concentrated in megaprojects with multi-year durations and milestone-based cash flows; in 2024 McDermott reported approximately $8.6 billion in revenue, with a large share tied to a handful of long-cycle contracts. Any dispute or delay can sharply strain working capital and liquidity when milestone receipts shift, and the firm’s ability to balance its portfolio with smaller, faster-turn projects is limited. This concentration elevates execution and counterparty risk, increasing volatility in margins and cash conversion.

- Concentration: majority of revenue from megaprojects

- Duration: contracts commonly span 2–5+ years

- Cashflow: milestone payments create liquidity spikes and gaps

- Risk: higher execution and counterparty exposure

Cyclical hydrocarbon megaproject player: 2024 revenue ~8.6B, overrun and bonding risks

McDermott’s revenue and margins are cyclical and concentrated in hydrocarbon megaprojects (2024 revenue ~$8.6B), exposing it to E&P capex swings, fixed‑price overrun risk (2020 Chapter 11 revealed vulnerability), legacy leverage limiting bonding/bid capacity, and reduced proprietary IP raising licensing costs and bid timelines.

| Weakness | Key data |

|---|---|

| Revenue concentration | 2024 revenue ~$8.6B; majority megaprojects |

| Bankruptcy legacy | Chapter 11 Jan 2020; emergence Jan 2021 |

| Contract risk | 2–5+ yr EPCI; fixed-price overruns |

Same Document Delivered

McDermott SWOT Analysis

This is the actual McDermott SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the structure, findings, and editable content included in the download. Buy now to unlock the complete, detailed version immediately after payment.

Original: $10.00

-65%$10.00

$3.50Description

Your Strategic Toolkit Starts Here

Explore McDermott's strategic position through our concise SWOT preview highlighting strengths, weaknesses, market risks and growth opportunities. Want the full picture with financial context, expert commentary and actionable strategy? Purchase the complete SWOT—editable Word and Excel deliverables ready for pitching, planning and investment decisions.

Strengths

Integrated EPCI capabilities

McDermott delivers engineering, procurement, construction and installation under one roof, reducing interfaces and schedule risk for clients and supporting turnkey execution from concept through commissioning. This integration drives cost and schedule synergies across phases, contributing to improved project predictability; the company reported a backlog of roughly $9.4 billion in mid-2024, reflecting strong demand for integrated EPCI. Clients value single-point accountability on complex offshore and onshore projects, simplifying risk transfer and contract management.

Deep offshore and subsea expertise

Founded in 1923, McDermott brings over a century of experience in fixed and floating production facilities, pipelines and subsea systems, with a proven track record in the Gulf of Mexico and North Sea. Specialized vessels, installation know‑how and repeatable methodologies enable execution in harsh environments. This capability underpins brownfield tie‑backs and greenfield developments and distinguishes McDermott on technically demanding scopes.

Global footprint and fabrication network

Strategically located yards and project offices across the Middle East, Asia and the Americas support regional content and logistics efficiency, enabling compliance with in-country value programs such as Saudi IKTVA and other national local content requirements. Local execution shortens lead times and improves responsiveness through closer client proximity. This footprint also diversifies revenue across multiple basins, reducing single-market exposure.

End-to-end lifecycle service

McDermott offers end-to-end lifecycle services from concept and FEED through detailed engineering, fabrication, installation and commissioning, enabling seamless handoffs and fewer claims from design–build disconnects. Lifecycle coverage drives repeat business and long-term client relationships and allows service bundling for margin uplift. McDermott reported fiscal 2024 revenue of $6.7 billion and a backlog near $9.5 billion.

- Scope: concept→commissioning

- Benefit: fewer claims, smoother handoffs

- Commercial: repeat clients, higher LTV

- Margin: bundling optionality

Reputation with NOCs and IOCs

McDermott serves major NOCs and IOCs on large LNG, offshore platform and pipeline programs, with a reported backlog of roughly $6.4 billion and about 11,000 employees as of 2024, reinforcing credibility on complex EPC delivery and long-cycle awards.

- Reputation: long-standing NOC/IOC relationships

- Project pedigree: LNG, offshore platforms, pipelines

- Systems: established prequalification and HSE

- Commercial: strong ties support sustained regional backlog

EPCI cuts interfaces; backlog ~9.5B

McDermott integrates EPCI to cut interfaces and schedule risk; backlog ~9.5B (mid‑2024). Century of experience and specialized vessels underpin LNG/offshore pedigree. Global yards enable local content compliance; FY2024 revenue 6.7B and ~11,000 employees.

| Metric | Value |

|---|---|

| Backlog | ~9.5B (mid‑2024) |

| FY2024 Revenue | 6.7B |

| Employees | ~11,000 |

What is included in the product

Provides a strategic overview of McDermott’s internal strengths and weaknesses and external opportunities and threats, highlighting competitive position, growth drivers, operational gaps, and risks shaping its future.

Provides a concise, executive-ready SWOT matrix for McDermott that clears analytical bottlenecks and enables rapid alignment of strategy and resource decisions.

Weaknesses

Exposure to oil and gas cyclicality

Revenue for McDermott is tightly tied to upstream and midstream capital spending cycles; when E&P capex weakens projects are delayed and awards fall, compressing margins and forcing competitive pricing. Volatile oil and gas demand complicates resource planning and vessel utilization, increasing idle time and costs. This dependence amplifies quarterly earnings variability for a company heavily exposed to hydrocarbon project flows.

Project execution and lump-sum risk

McDermott's EPCI focus leaves it exposed to fixed-price change-order risk and lump-sum losses; its 2020 Chapter 11 showed how single-project overruns can threaten the firm. Cost inflation and supply-chain delays continue to erode margins, with contractors pursuing multi-hundred-million-dollar claims and protracted recoveries. Robust risk management and claims resolution remain constant challenges.

Leverage and legacy restructuring overhang

Historical Chapter 11 in Jan 2020 with emergence in Jan 2021 has left leverage and legacy restructuring that constrain strategic flexibility; perceived credit risk has increased bonding scrutiny and limited bid capacity on large EPCI awards. Counterparties demand tighter payment and collateral terms, pressuring cash flow, while the overhang complicates talent retention and supplier negotiations.

Narrower technology ownership post-divestitures

Divestments have narrowed McDermott’s in-house proprietary process offerings, reducing captive IP that previously supported differentiation in onshore petrochemicals and integrated EPC bids; reliance on third-party licensors can compress margin levers and prolong bid cycles and approvals.

- Reduced proprietary IP

- Weaker differentiation in onshore petrochemicals

- Higher royalty/licensing dependence

- Longer bid cycles and approval timelines

Concentration in large, complex projects

Revenue is heavily concentrated in megaprojects with multi-year durations and milestone-based cash flows; in 2024 McDermott reported approximately $8.6 billion in revenue, with a large share tied to a handful of long-cycle contracts. Any dispute or delay can sharply strain working capital and liquidity when milestone receipts shift, and the firm’s ability to balance its portfolio with smaller, faster-turn projects is limited. This concentration elevates execution and counterparty risk, increasing volatility in margins and cash conversion.

- Concentration: majority of revenue from megaprojects

- Duration: contracts commonly span 2–5+ years

- Cashflow: milestone payments create liquidity spikes and gaps

- Risk: higher execution and counterparty exposure

Cyclical hydrocarbon megaproject player: 2024 revenue ~8.6B, overrun and bonding risks

McDermott’s revenue and margins are cyclical and concentrated in hydrocarbon megaprojects (2024 revenue ~$8.6B), exposing it to E&P capex swings, fixed‑price overrun risk (2020 Chapter 11 revealed vulnerability), legacy leverage limiting bonding/bid capacity, and reduced proprietary IP raising licensing costs and bid timelines.

| Weakness | Key data |

|---|---|

| Revenue concentration | 2024 revenue ~$8.6B; majority megaprojects |

| Bankruptcy legacy | Chapter 11 Jan 2020; emergence Jan 2021 |

| Contract risk | 2–5+ yr EPCI; fixed-price overruns |

Same Document Delivered

McDermott SWOT Analysis

This is the actual McDermott SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the structure, findings, and editable content included in the download. Buy now to unlock the complete, detailed version immediately after payment.