McWane Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

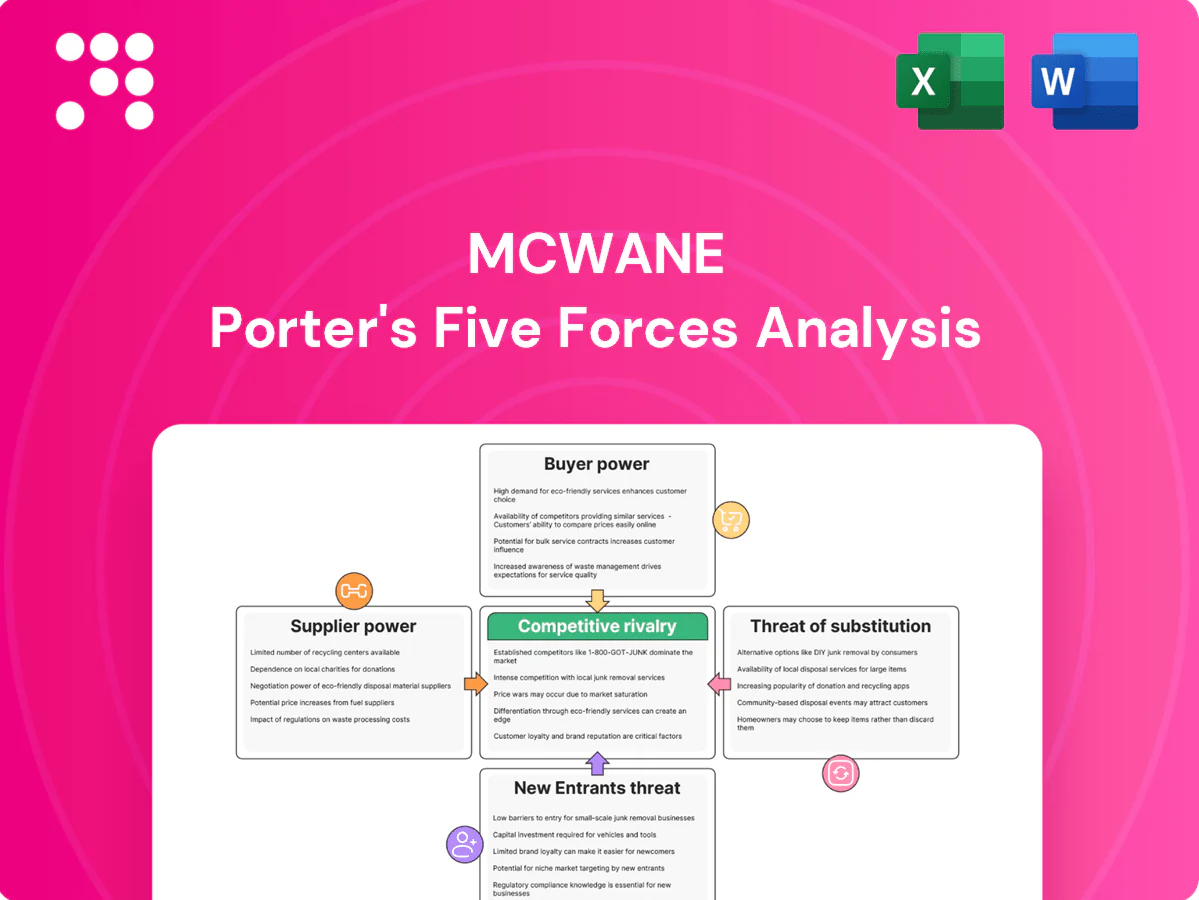

McWane’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, substitutes, and entry barriers to frame industry risks and opportunities. This brief overview teases force-by-force impacts, but the full report delivers ratings, visuals, and actionable strategy. Ready to dig deeper? Unlock the complete analysis to inform investment and strategic decisions.

Suppliers Bargaining Power

Concentrated raw materials

McWane depends on scrap iron, pig iron, alloys, refractories and specialty linings with few qualified sources, and 2024 commodity cycles and regional scrap constraints pushed spot scrap tightness, raising input costs industrywide. Supplier concentration for critical inputs like epoxy resins and coke increases supplier leverage. Long-term contracts and multi-sourcing mitigate but do not eliminate this risk.

Energy and freight volatility

Melting and casting are energy intensive, exposing McWane to utility pricing — U.S. industrial electricity averaged about $0.08/kWh in 2024 and Henry Hub gas near $2.80/MMBtu — increasing input volatility. Rail and trucking capacity constraints drove carrier surcharges through 2024, with diesel ~ $3.60/gal and fuel surcharges commonly 10–25%. Fuel and freight are large supplier pass‑throughs; hedging and plant location help but cannot fully neutralize spikes.

Specification-grade inputs

Specification-grade inputs for waterworks must meet AWWA, NSF/ANSI 61 and UL/FM requirements, and AWWA's ~50,000 members in 2024 reinforce strict certification norms that narrow approved supplier pools. Qualified materials and linings limit substitution flexibility during disruptions, while mandatory compliance testing and traceability create switching frictions and longer qualification lead times. In tight 2024 markets, approved vendors therefore hold elevated bargaining power.

Capital equipment and MRO dependencies

Foundry furnaces, molds, cores and automation come from a handful of OEMs and toolers, and in 2024 global supply concentration remained high with typical lead times of 16–28 weeks; proprietary parts and service give OEMs pricing leverage on spares. Downtime risk materially raises willingness to pay for expedited parts and service. Preventive maintenance contracts partially rebalance negotiating power by locking in service and pricing.

- High OEM concentration (few global suppliers)

- Lead times 16–28 weeks (2024)

- Proprietary spares → pricing leverage

- Preventive maintenance reduces supplier power

Electronics and software components

Supplier leverage spikes: tight scrap, long OEM lead times, energy volatility, chip shortages

Suppliers hold elevated power for critical inputs (scrap tight in 2024), specification materials (AWWA ~50,000 members) and OEM spares (lead times 16–28w). Energy/freight volatility (US industrial electricity ~$0.08/kWh; Henry Hub ~$2.80/MMBtu; diesel ~$3.60/gal) increases pass‑through risk. Semiconductors (market ~$600B, LT ~8–12w) and platform lock‑in (switching costs ~20–30%) sustain supplier leverage.

| Metric | 2024 |

|---|---|

| Electricity | $0.08/kWh |

| Henry Hub | $2.80/MMBtu |

| Diesel | $3.60/gal |

| Semiconductors | $600B |

What is included in the product

Tailored Porter’s Five Forces analysis for McWane that uncovers competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and disruptive forces—providing data-backed insights and strategic implications for pricing, margins, and market defense.

A one-sheet Porter’s Five Forces for McWane that visualizes supplier, buyer, competitor and regulatory pressures with clear relief actions—ideal for quick strategic decision-making and slide-ready summaries.

Customers Bargaining Power

Municipal and utility buyers

Municipalities, utilities and ~50,000 US community water systems purchase via competitive tenders, creating strong price pressure despite stated emphasis on lifecycle cost and regulatory compliance; the Bipartisan Infrastructure Law added roughly $55 billion for water systems, increasing multi-year volume and buyer leverage. Prequalification lists limit suppliers to approved standards, concentrating bargaining power among purchasers who often award low bids.

Distributors and consolidators

Large distributors and buying groups—including major retailers such as Home Depot (FY2024 sales ~$162.6B) and Lowe’s (FY2024 sales ~$96.9B)—aggregate demand and leverage scale to negotiate discounts and payment terms. Their private-label strategies and alternative sourcing increase bargaining leverage, while expectations for fill-rate guarantees, rebates and consignment shift margin to channels. Manufacturers counter with differentiated SKUs and service SLAs to protect pricing.

Project timing and lead-time sensitivity

Contractors prioritize on-time delivery and quick turns, using schedule risk to extract concessions; in 2024 McWane, with roughly $1.2B revenue, faced frequent schedule-driven discounting on large municipal contracts. When capacity is ample, buyers push harder on price and payment terms; in tight 2024 markets expediting premiums — often 5–15% on rush orders — partially reversed buyer leverage. Forecast visibility reduced opportunistic bargaining as buyers who provided 12+ week forecasts secured steadier pricing and terms.

Standardized product comparability

Standardized ductile iron pipe, valves, and hydrants (ASTM/EN specs) enable direct apples-to-apples comparisons, raising buyers’ leverage to switch among approved brands. Low product differentiation shifts negotiations toward performance guarantees and warranties as primary levers. Suppliers defend price through superior service, logistics reliability, and digital asset tracking/support.

- Standards: ASTM/EN compliance

- Buyer leverage: high

- Negotiation tools: warranties/performance guarantees

- Defensive levers: service, logistics, digital support

Bundling and total solution deals

Buyers in 2024 favor bundled packages across pipe, valves, fittings, hydrants and asset management, driven by scale from infrastructure programs such as the IIJA's $55 billion water funding; bundles yield larger negotiations and volume-based discounts while integrated software/hardware raises switching costs. Value-based pricing can counteract discount pressure when performance outcomes are measurable.

- Bundling increases deal size and leverage

- Integrated systems raise switching costs

- Volume discounts vs value-based pricing

Public tenders and $55B IIJA water funds concentrate buying power, boosting distributor leverage

Public buyers (50k systems) drive strong price pressure via tenders; IIJA/IIEF added ~$55B for water through 2024, boosting buyer leverage. Large distributors (Home Depot FY2024 ~$162.6B; Lowe’s FY2024 ~$96.9B) aggregate demand; McWane 2024 revenue ~ $1.2B faced 5–15% expediting premiums. ASTM/EN standardization raises switching; suppliers defend with service, logistics and bundled solutions.

| Metric | 2024 |

|---|---|

| IIJA water funding | $55B |

| Home Depot sales | $162.6B |

| Lowe’s sales | $96.9B |

| McWane revenue | $1.2B |

Full Version Awaits

McWane Porter's Five Forces Analysis

This preview shows the exact McWane Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The analysis provides a concise evaluation of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes tailored to McWane's market position. It's fully formatted, ready to download and use the moment you buy.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

McWane’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, substitutes, and entry barriers to frame industry risks and opportunities. This brief overview teases force-by-force impacts, but the full report delivers ratings, visuals, and actionable strategy. Ready to dig deeper? Unlock the complete analysis to inform investment and strategic decisions.

Suppliers Bargaining Power

Concentrated raw materials

McWane depends on scrap iron, pig iron, alloys, refractories and specialty linings with few qualified sources, and 2024 commodity cycles and regional scrap constraints pushed spot scrap tightness, raising input costs industrywide. Supplier concentration for critical inputs like epoxy resins and coke increases supplier leverage. Long-term contracts and multi-sourcing mitigate but do not eliminate this risk.

Energy and freight volatility

Melting and casting are energy intensive, exposing McWane to utility pricing — U.S. industrial electricity averaged about $0.08/kWh in 2024 and Henry Hub gas near $2.80/MMBtu — increasing input volatility. Rail and trucking capacity constraints drove carrier surcharges through 2024, with diesel ~ $3.60/gal and fuel surcharges commonly 10–25%. Fuel and freight are large supplier pass‑throughs; hedging and plant location help but cannot fully neutralize spikes.

Specification-grade inputs

Specification-grade inputs for waterworks must meet AWWA, NSF/ANSI 61 and UL/FM requirements, and AWWA's ~50,000 members in 2024 reinforce strict certification norms that narrow approved supplier pools. Qualified materials and linings limit substitution flexibility during disruptions, while mandatory compliance testing and traceability create switching frictions and longer qualification lead times. In tight 2024 markets, approved vendors therefore hold elevated bargaining power.

Capital equipment and MRO dependencies

Foundry furnaces, molds, cores and automation come from a handful of OEMs and toolers, and in 2024 global supply concentration remained high with typical lead times of 16–28 weeks; proprietary parts and service give OEMs pricing leverage on spares. Downtime risk materially raises willingness to pay for expedited parts and service. Preventive maintenance contracts partially rebalance negotiating power by locking in service and pricing.

- High OEM concentration (few global suppliers)

- Lead times 16–28 weeks (2024)

- Proprietary spares → pricing leverage

- Preventive maintenance reduces supplier power

Electronics and software components

Supplier leverage spikes: tight scrap, long OEM lead times, energy volatility, chip shortages

Suppliers hold elevated power for critical inputs (scrap tight in 2024), specification materials (AWWA ~50,000 members) and OEM spares (lead times 16–28w). Energy/freight volatility (US industrial electricity ~$0.08/kWh; Henry Hub ~$2.80/MMBtu; diesel ~$3.60/gal) increases pass‑through risk. Semiconductors (market ~$600B, LT ~8–12w) and platform lock‑in (switching costs ~20–30%) sustain supplier leverage.

| Metric | 2024 |

|---|---|

| Electricity | $0.08/kWh |

| Henry Hub | $2.80/MMBtu |

| Diesel | $3.60/gal |

| Semiconductors | $600B |

What is included in the product

Tailored Porter’s Five Forces analysis for McWane that uncovers competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and disruptive forces—providing data-backed insights and strategic implications for pricing, margins, and market defense.

A one-sheet Porter’s Five Forces for McWane that visualizes supplier, buyer, competitor and regulatory pressures with clear relief actions—ideal for quick strategic decision-making and slide-ready summaries.

Customers Bargaining Power

Municipal and utility buyers

Municipalities, utilities and ~50,000 US community water systems purchase via competitive tenders, creating strong price pressure despite stated emphasis on lifecycle cost and regulatory compliance; the Bipartisan Infrastructure Law added roughly $55 billion for water systems, increasing multi-year volume and buyer leverage. Prequalification lists limit suppliers to approved standards, concentrating bargaining power among purchasers who often award low bids.

Distributors and consolidators

Large distributors and buying groups—including major retailers such as Home Depot (FY2024 sales ~$162.6B) and Lowe’s (FY2024 sales ~$96.9B)—aggregate demand and leverage scale to negotiate discounts and payment terms. Their private-label strategies and alternative sourcing increase bargaining leverage, while expectations for fill-rate guarantees, rebates and consignment shift margin to channels. Manufacturers counter with differentiated SKUs and service SLAs to protect pricing.

Project timing and lead-time sensitivity

Contractors prioritize on-time delivery and quick turns, using schedule risk to extract concessions; in 2024 McWane, with roughly $1.2B revenue, faced frequent schedule-driven discounting on large municipal contracts. When capacity is ample, buyers push harder on price and payment terms; in tight 2024 markets expediting premiums — often 5–15% on rush orders — partially reversed buyer leverage. Forecast visibility reduced opportunistic bargaining as buyers who provided 12+ week forecasts secured steadier pricing and terms.

Standardized product comparability

Standardized ductile iron pipe, valves, and hydrants (ASTM/EN specs) enable direct apples-to-apples comparisons, raising buyers’ leverage to switch among approved brands. Low product differentiation shifts negotiations toward performance guarantees and warranties as primary levers. Suppliers defend price through superior service, logistics reliability, and digital asset tracking/support.

- Standards: ASTM/EN compliance

- Buyer leverage: high

- Negotiation tools: warranties/performance guarantees

- Defensive levers: service, logistics, digital support

Bundling and total solution deals

Buyers in 2024 favor bundled packages across pipe, valves, fittings, hydrants and asset management, driven by scale from infrastructure programs such as the IIJA's $55 billion water funding; bundles yield larger negotiations and volume-based discounts while integrated software/hardware raises switching costs. Value-based pricing can counteract discount pressure when performance outcomes are measurable.

- Bundling increases deal size and leverage

- Integrated systems raise switching costs

- Volume discounts vs value-based pricing

Public tenders and $55B IIJA water funds concentrate buying power, boosting distributor leverage

Public buyers (50k systems) drive strong price pressure via tenders; IIJA/IIEF added ~$55B for water through 2024, boosting buyer leverage. Large distributors (Home Depot FY2024 ~$162.6B; Lowe’s FY2024 ~$96.9B) aggregate demand; McWane 2024 revenue ~ $1.2B faced 5–15% expediting premiums. ASTM/EN standardization raises switching; suppliers defend with service, logistics and bundled solutions.

| Metric | 2024 |

|---|---|

| IIJA water funding | $55B |

| Home Depot sales | $162.6B |

| Lowe’s sales | $96.9B |

| McWane revenue | $1.2B |

Full Version Awaits

McWane Porter's Five Forces Analysis

This preview shows the exact McWane Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The analysis provides a concise evaluation of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes tailored to McWane's market position. It's fully formatted, ready to download and use the moment you buy.

Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

McWane’s Porter's Five Forces snapshot highlights supplier leverage, buyer power, competitive rivalry, substitutes, and entry barriers to frame industry risks and opportunities. This brief overview teases force-by-force impacts, but the full report delivers ratings, visuals, and actionable strategy. Ready to dig deeper? Unlock the complete analysis to inform investment and strategic decisions.

Suppliers Bargaining Power

Concentrated raw materials

McWane depends on scrap iron, pig iron, alloys, refractories and specialty linings with few qualified sources, and 2024 commodity cycles and regional scrap constraints pushed spot scrap tightness, raising input costs industrywide. Supplier concentration for critical inputs like epoxy resins and coke increases supplier leverage. Long-term contracts and multi-sourcing mitigate but do not eliminate this risk.

Energy and freight volatility

Melting and casting are energy intensive, exposing McWane to utility pricing — U.S. industrial electricity averaged about $0.08/kWh in 2024 and Henry Hub gas near $2.80/MMBtu — increasing input volatility. Rail and trucking capacity constraints drove carrier surcharges through 2024, with diesel ~ $3.60/gal and fuel surcharges commonly 10–25%. Fuel and freight are large supplier pass‑throughs; hedging and plant location help but cannot fully neutralize spikes.

Specification-grade inputs

Specification-grade inputs for waterworks must meet AWWA, NSF/ANSI 61 and UL/FM requirements, and AWWA's ~50,000 members in 2024 reinforce strict certification norms that narrow approved supplier pools. Qualified materials and linings limit substitution flexibility during disruptions, while mandatory compliance testing and traceability create switching frictions and longer qualification lead times. In tight 2024 markets, approved vendors therefore hold elevated bargaining power.

Capital equipment and MRO dependencies

Foundry furnaces, molds, cores and automation come from a handful of OEMs and toolers, and in 2024 global supply concentration remained high with typical lead times of 16–28 weeks; proprietary parts and service give OEMs pricing leverage on spares. Downtime risk materially raises willingness to pay for expedited parts and service. Preventive maintenance contracts partially rebalance negotiating power by locking in service and pricing.

- High OEM concentration (few global suppliers)

- Lead times 16–28 weeks (2024)

- Proprietary spares → pricing leverage

- Preventive maintenance reduces supplier power

Electronics and software components

Supplier leverage spikes: tight scrap, long OEM lead times, energy volatility, chip shortages

Suppliers hold elevated power for critical inputs (scrap tight in 2024), specification materials (AWWA ~50,000 members) and OEM spares (lead times 16–28w). Energy/freight volatility (US industrial electricity ~$0.08/kWh; Henry Hub ~$2.80/MMBtu; diesel ~$3.60/gal) increases pass‑through risk. Semiconductors (market ~$600B, LT ~8–12w) and platform lock‑in (switching costs ~20–30%) sustain supplier leverage.

| Metric | 2024 |

|---|---|

| Electricity | $0.08/kWh |

| Henry Hub | $2.80/MMBtu |

| Diesel | $3.60/gal |

| Semiconductors | $600B |

What is included in the product

Tailored Porter’s Five Forces analysis for McWane that uncovers competitive intensity, supplier and buyer power, threat of new entrants and substitutes, and disruptive forces—providing data-backed insights and strategic implications for pricing, margins, and market defense.

A one-sheet Porter’s Five Forces for McWane that visualizes supplier, buyer, competitor and regulatory pressures with clear relief actions—ideal for quick strategic decision-making and slide-ready summaries.

Customers Bargaining Power

Municipal and utility buyers

Municipalities, utilities and ~50,000 US community water systems purchase via competitive tenders, creating strong price pressure despite stated emphasis on lifecycle cost and regulatory compliance; the Bipartisan Infrastructure Law added roughly $55 billion for water systems, increasing multi-year volume and buyer leverage. Prequalification lists limit suppliers to approved standards, concentrating bargaining power among purchasers who often award low bids.

Distributors and consolidators

Large distributors and buying groups—including major retailers such as Home Depot (FY2024 sales ~$162.6B) and Lowe’s (FY2024 sales ~$96.9B)—aggregate demand and leverage scale to negotiate discounts and payment terms. Their private-label strategies and alternative sourcing increase bargaining leverage, while expectations for fill-rate guarantees, rebates and consignment shift margin to channels. Manufacturers counter with differentiated SKUs and service SLAs to protect pricing.

Project timing and lead-time sensitivity

Contractors prioritize on-time delivery and quick turns, using schedule risk to extract concessions; in 2024 McWane, with roughly $1.2B revenue, faced frequent schedule-driven discounting on large municipal contracts. When capacity is ample, buyers push harder on price and payment terms; in tight 2024 markets expediting premiums — often 5–15% on rush orders — partially reversed buyer leverage. Forecast visibility reduced opportunistic bargaining as buyers who provided 12+ week forecasts secured steadier pricing and terms.

Standardized product comparability

Standardized ductile iron pipe, valves, and hydrants (ASTM/EN specs) enable direct apples-to-apples comparisons, raising buyers’ leverage to switch among approved brands. Low product differentiation shifts negotiations toward performance guarantees and warranties as primary levers. Suppliers defend price through superior service, logistics reliability, and digital asset tracking/support.

- Standards: ASTM/EN compliance

- Buyer leverage: high

- Negotiation tools: warranties/performance guarantees

- Defensive levers: service, logistics, digital support

Bundling and total solution deals

Buyers in 2024 favor bundled packages across pipe, valves, fittings, hydrants and asset management, driven by scale from infrastructure programs such as the IIJA's $55 billion water funding; bundles yield larger negotiations and volume-based discounts while integrated software/hardware raises switching costs. Value-based pricing can counteract discount pressure when performance outcomes are measurable.

- Bundling increases deal size and leverage

- Integrated systems raise switching costs

- Volume discounts vs value-based pricing

Public tenders and $55B IIJA water funds concentrate buying power, boosting distributor leverage

Public buyers (50k systems) drive strong price pressure via tenders; IIJA/IIEF added ~$55B for water through 2024, boosting buyer leverage. Large distributors (Home Depot FY2024 ~$162.6B; Lowe’s FY2024 ~$96.9B) aggregate demand; McWane 2024 revenue ~ $1.2B faced 5–15% expediting premiums. ASTM/EN standardization raises switching; suppliers defend with service, logistics and bundled solutions.

| Metric | 2024 |

|---|---|

| IIJA water funding | $55B |

| Home Depot sales | $162.6B |

| Lowe’s sales | $96.9B |

| McWane revenue | $1.2B |

Full Version Awaits

McWane Porter's Five Forces Analysis

This preview shows the exact McWane Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises, no placeholders. The analysis provides a concise evaluation of competitive rivalry, threat of new entrants, bargaining power of suppliers and buyers, and threat of substitutes tailored to McWane's market position. It's fully formatted, ready to download and use the moment you buy.