Mitsubishi Estate Porter's Five Forces Analysis

Go Beyond the Preview—Access the Full Strategic Report

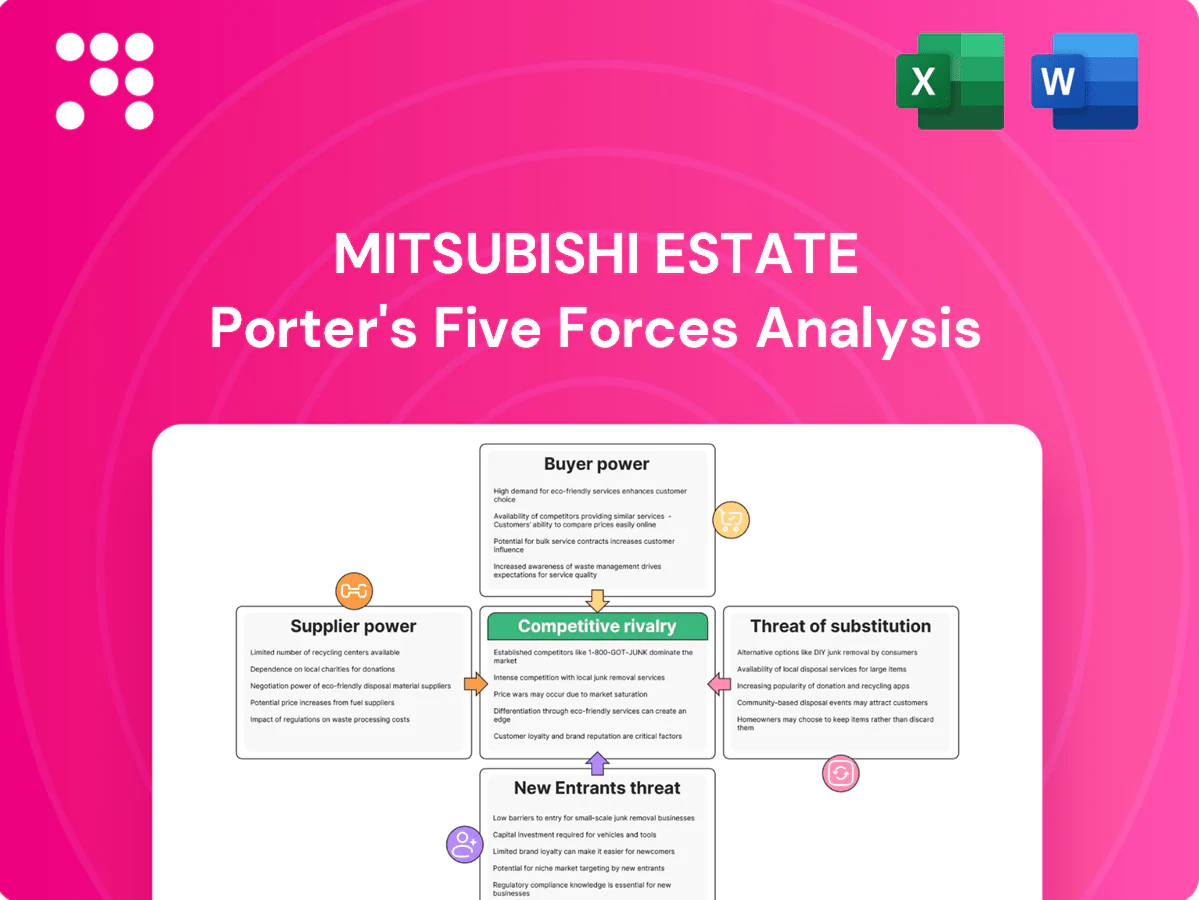

Mitsubishi Estate faces evolving competitive pressures—from tenant bargaining power and regulatory constraints to the threat of new entrants in real estate tech and mixed-use developments. This snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform strategy or investment decisions.

Suppliers Bargaining Power

Prime land scarcity

Prime sites in Tokyo and other major cities are limited and concentrated among a few owners, and Mitsubishi Estate itself holds roughly 30% of the Marunouchi district, giving land sellers strong leverage on price and terms. Focus on Marunouchi and urban nodes heightens exposure to scarcity and tight vacancy (around 2% in central Tokyo in 2024). Long negotiation cycles and pre-emptive rights partially mitigate upward pressure. Active portfolio recycling and joint ventures are used to access sites without overpaying.

Construction capacity cycles

During building booms general contractors and specialty trades exert upward pricing and longer lead times, with Japan facing a skilled-construction labor decline of about 10% since 2014 that tightens supply; long-term framework agreements and project bundling have lowered peak markups for major developers like Mitsubishi Estate by an estimated several percentage points in 2024, while value engineering and modularization cut dependency on peak-capacity pricing and shorten schedules.

Materials and energy inputs

Suppliers of steel, cement, glass and energy can pass through volatility, with global steel spot prices rising roughly 10% in 2024 and Brent crude averaging about $85/bbl, pressuring Mitsubishi Estate project IRRs and bidding margins. Yen depreciation near 8% vs USD in 2024 amplified import costs for materials priced offshore. Hedging, multi-sourcing and specs optimization reduce exposure, but demand for green materials—certified low-carbon cement and recycled glass—has narrowed supplier pools, increasing supplier leverage.

Tech and building systems

- Proprietary platforms: higher switching costs

- Portfolio licensing: reduces unit cost

- Open standards + in-house data: lower supplier power

Utilities and municipal services

Utilities, transit access and city infrastructure act as quasi-monopoly inputs for Mitsubishi Estate, where 2024 permitting and connection timelines materially affect project feasibility and cashflow; connection fees, stricter sustainability standards and staged network upgrades raise upfront costs and scheduling risk. Strong government relationships in Japan and host cities improve coordination and can shorten approval timelines. Deploying district energy or on-site renewables reduces exposure to supplier constraints and energy price volatility.

- Quasi-monopoly inputs: utilities, transit, municipal permits

- Cost drivers: connection fees, timelines, sustainability compliance

- Mitigation: government coordination, district energy, on-site renewables

Prime land ~30%, vacancy ~2%, labor -10%

Prime urban land concentration (Mitsubishi Estate ~30% of Marunouchi) and central Tokyo vacancy ~2% in 2024 give land suppliers strong leverage; construction labor down ~10% since 2014 tightens capacity. Global steel +10% in 2024 and Brent ~$85/bbl, plus yen -8% vs USD in 2024, raised material costs; tech vendors create switching costs. Mitigations: JV/site recycling, long-term contracts, portfolio licenses, district energy.

| Input | 2024 metric | Impact |

|---|---|---|

| Land | Marunouchi share ~30% / vacancy ~2% | High price leverage |

| Labor | -10% since 2014 | Longer timelines, higher bids |

| Materials | Steel +10% / Brent $85 / Yen -8% | Cost pressure on IRR |

| Tech | Proprietary platforms | Switching costs |

What is included in the product

Concise Porter's Five Forces analysis tailored to Mitsubishi Estate, assessing competitive rivalry, buyer and supplier power, entry barriers and substitutes in Japan's real estate and property development market, highlighting regulatory, capital intensity, and urban portfolio advantages that shape profitability and strategic risks.

A concise Porter's Five Forces toolkit tailored to Mitsubishi Estate—clarifies competitive, tenant, and regulatory pressures for faster strategic decisions. Editable pressure levels and an instant radar chart make slide-ready, boardroom-friendly summaries simple to update and share.

Customers Bargaining Power

Blue-chip office tenants

Large blue-chip tenants exert strong bargaining power on rent, fit-out and lease flexibility, particularly in soft markets, yet Mitsubishi Estate’s long WALEs in prime districts (often multi-year leases) reduce churn and stabilize cash flow; JLL reported 2024 Grade-A rent growth of about 6% in major APAC CBDs, reflecting flight-to-quality that strengthens Mitsubishi Estate’s pricing power, while bundled services and ESG credentials support premium rents.

Retail and F&B tenants

Smaller retail and F&B tenants are fragmented but highly sales‑sensitive, prompting demands for turnover‑linked rents and short‑term concessions; turnover rents now appear in roughly 20–30% of new high‑street and mall deals in Japan. Rising e‑commerce penetration (about 12.5% of Japan retail sales in 2024) heightens tenant bargaining pressure. Mitsubishi Estate’s curated destination centers sustain >95% occupancy and command 5–10% rent premiums, while shorter 3–5 year leases enable faster remixing and repricing.

Residential buyers and renters

Individual buyers remain price-sensitive but prioritize location, design and brand, and 2024 market reports show premium projects in Tokyo and Osaka sustain price premiums despite wider affordability pressures. In supply-constrained central wards buyer bargaining power is limited, keeping margins for developers. Rental customers face stronger bargaining as nearby stock and new completions increase competition, driving concessions. Amenity packages and energy-efficiency certifications defend pricing and reduce churn.

Institutional capital partners

Institutional capital partners—REITs, insurers and sovereign funds—co-invest with Mitsubishi Estate, negotiating fees and promote but facing tradeoffs as alternatives scale; sovereign wealth funds held about $11.4 trillion AUM in 2024, increasing their bargaining leverage while also feeding deal flow. Mitsubishi Estate’s track record and pipeline depth enable structured fees and co-GP or club deals that align incentives and preserve upside.

- Co-invest types: REITs, insurers, sovereign funds

- Bargaining drivers: scale, alternatives, AUM ~$11.4T (2024)

- Mitsubishi strengths: track record, pipeline, structured terms

- Alignment: co-GP and club deals retain upside

Hotel guests and operators

Brands and operators strongly influence owner returns through management and franchise fee negotiations that can shift margin; guests remain price-sensitive and channel-shift to OTAs, which accounted for around 40% of online hotel bookings in 2024, pressuring rates. Mitsubishi Estate’s prime Tokyo assets and mixed-use synergies enhance RevPAR resilience, while direct-booking initiatives and experiential F&B/amenity upgrades cut intermediary dependence.

- Management fees: impact on NOI

- OTA share ~40% (2024)

- Prime locations = stronger rate power

- Direct booking + experiences = lower commission

APAC Grade-A rents ~6%, >95% occupancy limit tenant churn amid e-commerce rise

Large blue‑chip tenants wield strong rent and lease leverage but Mitsubishi Estate’s long WALEs and 95%+ occupancy in prime assets limit churn; 2024 APAC Grade‑A rent growth ~6% supports pricing. Retail turnover rents rising with e‑commerce ~12.5% of Japan retail (2024) increase tenant sensitivity. Institutional co‑investors (sovereign AUM ~$11.4T) press fees but accept structured co‑GP deals.

| Metric | 2024 |

|---|---|

| Grade‑A rent growth (APAC) | ~6% |

| Prime occupancy | >95% |

| Japan e‑commerce share | ~12.5% |

| Sovereign AUM | $11.4T |

Same Document Delivered

Mitsubishi Estate Porter's Five Forces Analysis

This preview shows the exact Mitsubishi Estate Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is complete, professionally formatted and ready for download and use upon payment. What you see is what you get.

Go Beyond the Preview—Access the Full Strategic Report

Mitsubishi Estate faces evolving competitive pressures—from tenant bargaining power and regulatory constraints to the threat of new entrants in real estate tech and mixed-use developments. This snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform strategy or investment decisions.

Suppliers Bargaining Power

Prime land scarcity

Prime sites in Tokyo and other major cities are limited and concentrated among a few owners, and Mitsubishi Estate itself holds roughly 30% of the Marunouchi district, giving land sellers strong leverage on price and terms. Focus on Marunouchi and urban nodes heightens exposure to scarcity and tight vacancy (around 2% in central Tokyo in 2024). Long negotiation cycles and pre-emptive rights partially mitigate upward pressure. Active portfolio recycling and joint ventures are used to access sites without overpaying.

Construction capacity cycles

During building booms general contractors and specialty trades exert upward pricing and longer lead times, with Japan facing a skilled-construction labor decline of about 10% since 2014 that tightens supply; long-term framework agreements and project bundling have lowered peak markups for major developers like Mitsubishi Estate by an estimated several percentage points in 2024, while value engineering and modularization cut dependency on peak-capacity pricing and shorten schedules.

Materials and energy inputs

Suppliers of steel, cement, glass and energy can pass through volatility, with global steel spot prices rising roughly 10% in 2024 and Brent crude averaging about $85/bbl, pressuring Mitsubishi Estate project IRRs and bidding margins. Yen depreciation near 8% vs USD in 2024 amplified import costs for materials priced offshore. Hedging, multi-sourcing and specs optimization reduce exposure, but demand for green materials—certified low-carbon cement and recycled glass—has narrowed supplier pools, increasing supplier leverage.

Tech and building systems

- Proprietary platforms: higher switching costs

- Portfolio licensing: reduces unit cost

- Open standards + in-house data: lower supplier power

Utilities and municipal services

Utilities, transit access and city infrastructure act as quasi-monopoly inputs for Mitsubishi Estate, where 2024 permitting and connection timelines materially affect project feasibility and cashflow; connection fees, stricter sustainability standards and staged network upgrades raise upfront costs and scheduling risk. Strong government relationships in Japan and host cities improve coordination and can shorten approval timelines. Deploying district energy or on-site renewables reduces exposure to supplier constraints and energy price volatility.

- Quasi-monopoly inputs: utilities, transit, municipal permits

- Cost drivers: connection fees, timelines, sustainability compliance

- Mitigation: government coordination, district energy, on-site renewables

Prime land ~30%, vacancy ~2%, labor -10%

Prime urban land concentration (Mitsubishi Estate ~30% of Marunouchi) and central Tokyo vacancy ~2% in 2024 give land suppliers strong leverage; construction labor down ~10% since 2014 tightens capacity. Global steel +10% in 2024 and Brent ~$85/bbl, plus yen -8% vs USD in 2024, raised material costs; tech vendors create switching costs. Mitigations: JV/site recycling, long-term contracts, portfolio licenses, district energy.

| Input | 2024 metric | Impact |

|---|---|---|

| Land | Marunouchi share ~30% / vacancy ~2% | High price leverage |

| Labor | -10% since 2014 | Longer timelines, higher bids |

| Materials | Steel +10% / Brent $85 / Yen -8% | Cost pressure on IRR |

| Tech | Proprietary platforms | Switching costs |

What is included in the product

Concise Porter's Five Forces analysis tailored to Mitsubishi Estate, assessing competitive rivalry, buyer and supplier power, entry barriers and substitutes in Japan's real estate and property development market, highlighting regulatory, capital intensity, and urban portfolio advantages that shape profitability and strategic risks.

A concise Porter's Five Forces toolkit tailored to Mitsubishi Estate—clarifies competitive, tenant, and regulatory pressures for faster strategic decisions. Editable pressure levels and an instant radar chart make slide-ready, boardroom-friendly summaries simple to update and share.

Customers Bargaining Power

Blue-chip office tenants

Large blue-chip tenants exert strong bargaining power on rent, fit-out and lease flexibility, particularly in soft markets, yet Mitsubishi Estate’s long WALEs in prime districts (often multi-year leases) reduce churn and stabilize cash flow; JLL reported 2024 Grade-A rent growth of about 6% in major APAC CBDs, reflecting flight-to-quality that strengthens Mitsubishi Estate’s pricing power, while bundled services and ESG credentials support premium rents.

Retail and F&B tenants

Smaller retail and F&B tenants are fragmented but highly sales‑sensitive, prompting demands for turnover‑linked rents and short‑term concessions; turnover rents now appear in roughly 20–30% of new high‑street and mall deals in Japan. Rising e‑commerce penetration (about 12.5% of Japan retail sales in 2024) heightens tenant bargaining pressure. Mitsubishi Estate’s curated destination centers sustain >95% occupancy and command 5–10% rent premiums, while shorter 3–5 year leases enable faster remixing and repricing.

Residential buyers and renters

Individual buyers remain price-sensitive but prioritize location, design and brand, and 2024 market reports show premium projects in Tokyo and Osaka sustain price premiums despite wider affordability pressures. In supply-constrained central wards buyer bargaining power is limited, keeping margins for developers. Rental customers face stronger bargaining as nearby stock and new completions increase competition, driving concessions. Amenity packages and energy-efficiency certifications defend pricing and reduce churn.

Institutional capital partners

Institutional capital partners—REITs, insurers and sovereign funds—co-invest with Mitsubishi Estate, negotiating fees and promote but facing tradeoffs as alternatives scale; sovereign wealth funds held about $11.4 trillion AUM in 2024, increasing their bargaining leverage while also feeding deal flow. Mitsubishi Estate’s track record and pipeline depth enable structured fees and co-GP or club deals that align incentives and preserve upside.

- Co-invest types: REITs, insurers, sovereign funds

- Bargaining drivers: scale, alternatives, AUM ~$11.4T (2024)

- Mitsubishi strengths: track record, pipeline, structured terms

- Alignment: co-GP and club deals retain upside

Hotel guests and operators

Brands and operators strongly influence owner returns through management and franchise fee negotiations that can shift margin; guests remain price-sensitive and channel-shift to OTAs, which accounted for around 40% of online hotel bookings in 2024, pressuring rates. Mitsubishi Estate’s prime Tokyo assets and mixed-use synergies enhance RevPAR resilience, while direct-booking initiatives and experiential F&B/amenity upgrades cut intermediary dependence.

- Management fees: impact on NOI

- OTA share ~40% (2024)

- Prime locations = stronger rate power

- Direct booking + experiences = lower commission

APAC Grade-A rents ~6%, >95% occupancy limit tenant churn amid e-commerce rise

Large blue‑chip tenants wield strong rent and lease leverage but Mitsubishi Estate’s long WALEs and 95%+ occupancy in prime assets limit churn; 2024 APAC Grade‑A rent growth ~6% supports pricing. Retail turnover rents rising with e‑commerce ~12.5% of Japan retail (2024) increase tenant sensitivity. Institutional co‑investors (sovereign AUM ~$11.4T) press fees but accept structured co‑GP deals.

| Metric | 2024 |

|---|---|

| Grade‑A rent growth (APAC) | ~6% |

| Prime occupancy | >95% |

| Japan e‑commerce share | ~12.5% |

| Sovereign AUM | $11.4T |

Same Document Delivered

Mitsubishi Estate Porter's Five Forces Analysis

This preview shows the exact Mitsubishi Estate Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is complete, professionally formatted and ready for download and use upon payment. What you see is what you get.

Original: $10.00

-65%$10.00

$3.50Description

Go Beyond the Preview—Access the Full Strategic Report

Mitsubishi Estate faces evolving competitive pressures—from tenant bargaining power and regulatory constraints to the threat of new entrants in real estate tech and mixed-use developments. This snapshot highlights key dynamics but only scratches the surface. Unlock the full Porter's Five Forces Analysis for force-by-force ratings, visuals, and actionable insights to inform strategy or investment decisions.

Suppliers Bargaining Power

Prime land scarcity

Prime sites in Tokyo and other major cities are limited and concentrated among a few owners, and Mitsubishi Estate itself holds roughly 30% of the Marunouchi district, giving land sellers strong leverage on price and terms. Focus on Marunouchi and urban nodes heightens exposure to scarcity and tight vacancy (around 2% in central Tokyo in 2024). Long negotiation cycles and pre-emptive rights partially mitigate upward pressure. Active portfolio recycling and joint ventures are used to access sites without overpaying.

Construction capacity cycles

During building booms general contractors and specialty trades exert upward pricing and longer lead times, with Japan facing a skilled-construction labor decline of about 10% since 2014 that tightens supply; long-term framework agreements and project bundling have lowered peak markups for major developers like Mitsubishi Estate by an estimated several percentage points in 2024, while value engineering and modularization cut dependency on peak-capacity pricing and shorten schedules.

Materials and energy inputs

Suppliers of steel, cement, glass and energy can pass through volatility, with global steel spot prices rising roughly 10% in 2024 and Brent crude averaging about $85/bbl, pressuring Mitsubishi Estate project IRRs and bidding margins. Yen depreciation near 8% vs USD in 2024 amplified import costs for materials priced offshore. Hedging, multi-sourcing and specs optimization reduce exposure, but demand for green materials—certified low-carbon cement and recycled glass—has narrowed supplier pools, increasing supplier leverage.

Tech and building systems

- Proprietary platforms: higher switching costs

- Portfolio licensing: reduces unit cost

- Open standards + in-house data: lower supplier power

Utilities and municipal services

Utilities, transit access and city infrastructure act as quasi-monopoly inputs for Mitsubishi Estate, where 2024 permitting and connection timelines materially affect project feasibility and cashflow; connection fees, stricter sustainability standards and staged network upgrades raise upfront costs and scheduling risk. Strong government relationships in Japan and host cities improve coordination and can shorten approval timelines. Deploying district energy or on-site renewables reduces exposure to supplier constraints and energy price volatility.

- Quasi-monopoly inputs: utilities, transit, municipal permits

- Cost drivers: connection fees, timelines, sustainability compliance

- Mitigation: government coordination, district energy, on-site renewables

Prime land ~30%, vacancy ~2%, labor -10%

Prime urban land concentration (Mitsubishi Estate ~30% of Marunouchi) and central Tokyo vacancy ~2% in 2024 give land suppliers strong leverage; construction labor down ~10% since 2014 tightens capacity. Global steel +10% in 2024 and Brent ~$85/bbl, plus yen -8% vs USD in 2024, raised material costs; tech vendors create switching costs. Mitigations: JV/site recycling, long-term contracts, portfolio licenses, district energy.

| Input | 2024 metric | Impact |

|---|---|---|

| Land | Marunouchi share ~30% / vacancy ~2% | High price leverage |

| Labor | -10% since 2014 | Longer timelines, higher bids |

| Materials | Steel +10% / Brent $85 / Yen -8% | Cost pressure on IRR |

| Tech | Proprietary platforms | Switching costs |

What is included in the product

Concise Porter's Five Forces analysis tailored to Mitsubishi Estate, assessing competitive rivalry, buyer and supplier power, entry barriers and substitutes in Japan's real estate and property development market, highlighting regulatory, capital intensity, and urban portfolio advantages that shape profitability and strategic risks.

A concise Porter's Five Forces toolkit tailored to Mitsubishi Estate—clarifies competitive, tenant, and regulatory pressures for faster strategic decisions. Editable pressure levels and an instant radar chart make slide-ready, boardroom-friendly summaries simple to update and share.

Customers Bargaining Power

Blue-chip office tenants

Large blue-chip tenants exert strong bargaining power on rent, fit-out and lease flexibility, particularly in soft markets, yet Mitsubishi Estate’s long WALEs in prime districts (often multi-year leases) reduce churn and stabilize cash flow; JLL reported 2024 Grade-A rent growth of about 6% in major APAC CBDs, reflecting flight-to-quality that strengthens Mitsubishi Estate’s pricing power, while bundled services and ESG credentials support premium rents.

Retail and F&B tenants

Smaller retail and F&B tenants are fragmented but highly sales‑sensitive, prompting demands for turnover‑linked rents and short‑term concessions; turnover rents now appear in roughly 20–30% of new high‑street and mall deals in Japan. Rising e‑commerce penetration (about 12.5% of Japan retail sales in 2024) heightens tenant bargaining pressure. Mitsubishi Estate’s curated destination centers sustain >95% occupancy and command 5–10% rent premiums, while shorter 3–5 year leases enable faster remixing and repricing.

Residential buyers and renters

Individual buyers remain price-sensitive but prioritize location, design and brand, and 2024 market reports show premium projects in Tokyo and Osaka sustain price premiums despite wider affordability pressures. In supply-constrained central wards buyer bargaining power is limited, keeping margins for developers. Rental customers face stronger bargaining as nearby stock and new completions increase competition, driving concessions. Amenity packages and energy-efficiency certifications defend pricing and reduce churn.

Institutional capital partners

Institutional capital partners—REITs, insurers and sovereign funds—co-invest with Mitsubishi Estate, negotiating fees and promote but facing tradeoffs as alternatives scale; sovereign wealth funds held about $11.4 trillion AUM in 2024, increasing their bargaining leverage while also feeding deal flow. Mitsubishi Estate’s track record and pipeline depth enable structured fees and co-GP or club deals that align incentives and preserve upside.

- Co-invest types: REITs, insurers, sovereign funds

- Bargaining drivers: scale, alternatives, AUM ~$11.4T (2024)

- Mitsubishi strengths: track record, pipeline, structured terms

- Alignment: co-GP and club deals retain upside

Hotel guests and operators

Brands and operators strongly influence owner returns through management and franchise fee negotiations that can shift margin; guests remain price-sensitive and channel-shift to OTAs, which accounted for around 40% of online hotel bookings in 2024, pressuring rates. Mitsubishi Estate’s prime Tokyo assets and mixed-use synergies enhance RevPAR resilience, while direct-booking initiatives and experiential F&B/amenity upgrades cut intermediary dependence.

- Management fees: impact on NOI

- OTA share ~40% (2024)

- Prime locations = stronger rate power

- Direct booking + experiences = lower commission

APAC Grade-A rents ~6%, >95% occupancy limit tenant churn amid e-commerce rise

Large blue‑chip tenants wield strong rent and lease leverage but Mitsubishi Estate’s long WALEs and 95%+ occupancy in prime assets limit churn; 2024 APAC Grade‑A rent growth ~6% supports pricing. Retail turnover rents rising with e‑commerce ~12.5% of Japan retail (2024) increase tenant sensitivity. Institutional co‑investors (sovereign AUM ~$11.4T) press fees but accept structured co‑GP deals.

| Metric | 2024 |

|---|---|

| Grade‑A rent growth (APAC) | ~6% |

| Prime occupancy | >95% |

| Japan e‑commerce share | ~12.5% |

| Sovereign AUM | $11.4T |

Same Document Delivered

Mitsubishi Estate Porter's Five Forces Analysis

This preview shows the exact Mitsubishi Estate Porter's Five Forces analysis you'll receive immediately after purchase—no placeholders or mockups. The file is complete, professionally formatted and ready for download and use upon payment. What you see is what you get.