Mebuki Financial Group PESTLE Analysis

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic advantage with our PESTLE analysis of Mebuki Financial Group—concise insight into political, economic, social, technological, legal, and environmental forces shaping its prospects. Ideal for investors and advisors seeking evidence-based foresight. Purchase the full report to access actionable intelligence, charts, and recommendations ready for immediate use.

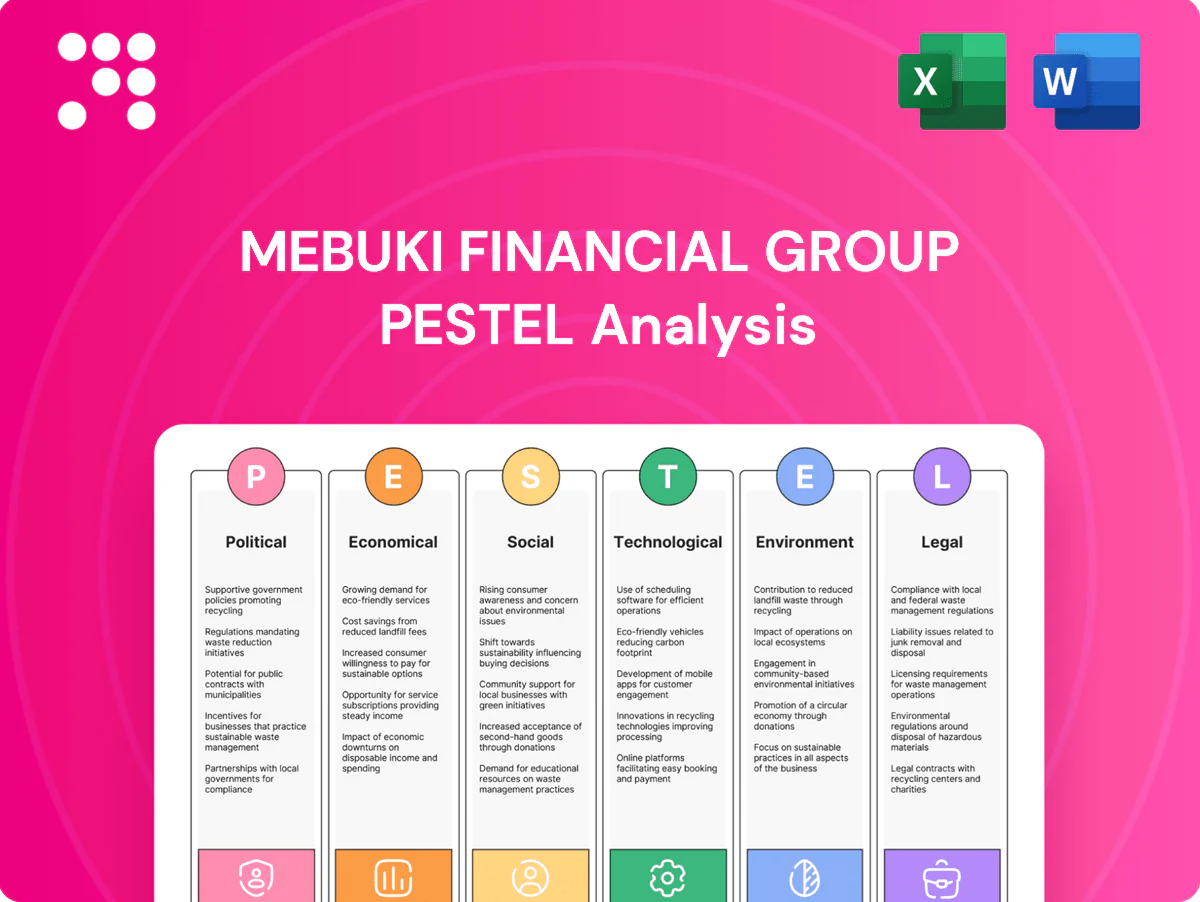

Political factors

Stable governance and regional revitalization

Japan’s long-standing political stability underpins predictable banking policy and budgeting, supporting steady operating conditions for regional banks. Ibaraki (≈2.8 million) and Tochigi (≈1.9 million) are focal prefectures for national regional revitalization programs that channel central funds to local projects. Mebuki can align lending to infrastructure and SME initiatives to tap available subsidies and credit guarantees. Close ties with prefectural authorities can improve deal flow and public–private project participation.

FSA supervision and prudential stance

Japan’s Financial Services Agency 2024 supervisory priorities emphasize customer-oriented finance, stronger risk governance and conduct, with heightened scrutiny of credit risk, interest-rate risk in the banking book and stress testing. These supervisory themes affect capital planning as firms must demonstrate resilience under stress scenarios; the Basel III CET1 regulatory minimum is 4.5% and Japanese banks typically target higher buffers. Strong compliance and risk frameworks help Mebuki maintain credibility and avoid remediation burdens, while early engagement with the FSA can smooth approvals for new products.

Monetary–fiscal coordination effects

As the BoJ moved away from ultra‑easy policy in 2023–24 (ending negative rates/yield‑curve control) and market 10‑yr JGB yields rose toward 0.6–1.0%, fiscal measures—notably ~¥10 trillion in 2024 energy and SME support—can cushion credit stress; Mebuki must balance policy‑driven lending with strict underwriting and transparent pricing/support communications to sustain stakeholder trust.

Geopolitical tensions and supply chains

Geopolitical tensions since 2024 have disrupted supply chains for auto, electronics and agriculture clients along Kanto’s northern corridor, prompting demand and input shocks that may require covenant flexibility for export-oriented borrowers.

- Resilience drives: reshoring loans and capex finance up in 2024–25

- Portfolio action: scenario planning improves stress readiness

- Risk: regional security elevates concentration and supplier risk

Digital policy and public infrastructure

Government drives — led by the Digital Agency (est. 2021) and universal My Number coverage (~125 million residents) plus cashless promotion — are reshaping public-sector DX and payment rails, so joining government platforms can materially lower onboarding friction and compliance costs for Mebuki. Political emphasis on digital inclusion mandates maintained access for elderly users, making a balanced digital/branch channel strategy important to secure public grants and meet expectations.

- My Number coverage: ~125 million residents

- Digital Agency: est. 2021 — central DX policy driver

- Onboarding/compliance cost reduction via gov platforms

- Requirement: preserve elderly access → balanced channel strategy

Prefectural funds (Ibaraki 2.8M, Tochigi 1.9M), BoJ normalization & onboarding risks

Political stability, prefectural revitalization funds (Ibaraki ~2.8M, Tochigi ~1.9M) and FSA 2024 priorities (customer‑oriented finance, stricter risk governance) shape Mebuki’s capital and compliance needs. BoJ policy normalization (10y JGB ~0.6–1.0%) and ¥10T 2024 fiscal support affect credit demand and stress scenarios. Digital Agency push and My Number (~125M) lower onboarding costs but require elderly access safeguards.

| Factor | Key data |

|---|---|

| Prefectures | Ibaraki 2.8M / Tochigi 1.9M |

| FSA focus | 2024: conduct, credit & IRRBB |

| Macro | 10y JGB 0.6–1.0% / ¥10T fiscal |

| Digital | My Number ~125M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Mebuki Financial Group’s risk and opportunity profile, with data-backed trends and region-specific regulatory context; designed for executives and advisors to inform strategy, scenario planning and investor communications.

A concise, visually segmented PESTLE summary of Mebuki Financial Group that distills external risks and market drivers for quick reference in meetings or presentations, easily shareable and ready to drop into slides to align teams and support strategic planning.

Economic factors

Rate normalization and NIM dynamics

BoJ exit from negative rates in 2023 has pushed loan yields up while deposit costs have started rising, with 10-year JGB yields moving into roughly 0.8–1.0% by 2024–H1 2025. ALM is now critical as term premia and the curve steepen. Repricing lags can temporarily widen NIM if managed well. Hedging strategies and loan/deposit product mix will drive earnings stability.

Regional growth and SME health

Ibaraki and Tochigi economies hinge on autos, machinery, logistics and agribusiness, making regional SMEs sensitive to slower growth or inventory cycles that can strain cash flows and raise probabilities of default. SMEs account for 99.7% of Japanese firms and employ roughly 70% of the workforce, concentrating credit exposure locally. Proactive advisory and working‑capital solutions have been shown to stabilise clients and reduce NPLs, while sector diversification cuts concentration risk.

Inflation, wages, and household behavior

Moderate inflation around 3% in 2024 with gradual wage gains of roughly 2–3% is nudging households from cash holdings into time deposits and investment products. Shifts in consumption mix are already affecting card transaction volumes and merchant fee income. Expanded NISA reforms from 2024 have lifted financial planning demand, and Mebuki can capture flows via low‑cost index and ETF wrappers.

Real estate and collateral values

Regional property trends directly affect collateral coverage across Mebuki’s SME and mortgage books; higher rates since 2023 have begun to cool valuations and can extend disposal timelines by several months. Maintaining conservative LTVs (typically 60–70%) and frequent reappraisals limits loss severity. Focused redevelopment finance for station-area hubs can unlock value and improve collateral quality.

- Collateral sensitivity: regional gaps widen risk

- LTV band: 60–70%

- Sale delays: +3–6 months

- Redevelopment: station hubs boost recovery

Yen volatility and trade exposure

FX swings—yen around 155 JPY/USD in H1 2025 with ~12% 1‑yr realized vol—hit exporters and importers across Mebuki’s customer base, pushing demand for hedging, trade finance and supply‑chain solutions; credit stress could rise among energy‑intensive and import‑reliant SMEs (Japan imports ~90% of energy), while cross‑sell of risk‑management products aids fee diversification as exports remain ~18% of GDP.

- FX impact: 155 JPY/USD, ~12% vol

- Trade exposure: exports ~18% of GDP

- Energy reliance: ~90% imported

- Opportunity: hedging/trade finance = fee diversification

Prefectural funds (Ibaraki 2.8M, Tochigi 1.9M), BoJ normalization & onboarding risks

BoJ exit and 10y JGB ~0.9% (2024–H1 2025) raised loan yields and ALM risk; repricing gaps can widen NIM but hedging and product mix support stability. Regional SME concentration (99.7% of firms; ~70% workforce) and local auto/machinery exposure elevate credit sensitivity. CPI ~3% (2024) with wage gains ~2–3% shifts savings to time deposits/NISA flows; yen ~155 JPY/USD boosts hedging demand.

| Metric | Value |

|---|---|

| 10y JGB | ~0.9% |

| CPI (2024) | ~3% |

| Wage growth | 2–3% |

| Yen | ~155 JPY/USD |

| SME share | 99.7% |

| Energy imports | ~90% |

| LTV guideline | 60–70% |

Full Version Awaits

Mebuki Financial Group PESTLE Analysis

The Mebuki Financial Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment as presented. No placeholders or teasers—this is the final, downloadable file.

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic advantage with our PESTLE analysis of Mebuki Financial Group—concise insight into political, economic, social, technological, legal, and environmental forces shaping its prospects. Ideal for investors and advisors seeking evidence-based foresight. Purchase the full report to access actionable intelligence, charts, and recommendations ready for immediate use.

Political factors

Stable governance and regional revitalization

Japan’s long-standing political stability underpins predictable banking policy and budgeting, supporting steady operating conditions for regional banks. Ibaraki (≈2.8 million) and Tochigi (≈1.9 million) are focal prefectures for national regional revitalization programs that channel central funds to local projects. Mebuki can align lending to infrastructure and SME initiatives to tap available subsidies and credit guarantees. Close ties with prefectural authorities can improve deal flow and public–private project participation.

FSA supervision and prudential stance

Japan’s Financial Services Agency 2024 supervisory priorities emphasize customer-oriented finance, stronger risk governance and conduct, with heightened scrutiny of credit risk, interest-rate risk in the banking book and stress testing. These supervisory themes affect capital planning as firms must demonstrate resilience under stress scenarios; the Basel III CET1 regulatory minimum is 4.5% and Japanese banks typically target higher buffers. Strong compliance and risk frameworks help Mebuki maintain credibility and avoid remediation burdens, while early engagement with the FSA can smooth approvals for new products.

Monetary–fiscal coordination effects

As the BoJ moved away from ultra‑easy policy in 2023–24 (ending negative rates/yield‑curve control) and market 10‑yr JGB yields rose toward 0.6–1.0%, fiscal measures—notably ~¥10 trillion in 2024 energy and SME support—can cushion credit stress; Mebuki must balance policy‑driven lending with strict underwriting and transparent pricing/support communications to sustain stakeholder trust.

Geopolitical tensions and supply chains

Geopolitical tensions since 2024 have disrupted supply chains for auto, electronics and agriculture clients along Kanto’s northern corridor, prompting demand and input shocks that may require covenant flexibility for export-oriented borrowers.

- Resilience drives: reshoring loans and capex finance up in 2024–25

- Portfolio action: scenario planning improves stress readiness

- Risk: regional security elevates concentration and supplier risk

Digital policy and public infrastructure

Government drives — led by the Digital Agency (est. 2021) and universal My Number coverage (~125 million residents) plus cashless promotion — are reshaping public-sector DX and payment rails, so joining government platforms can materially lower onboarding friction and compliance costs for Mebuki. Political emphasis on digital inclusion mandates maintained access for elderly users, making a balanced digital/branch channel strategy important to secure public grants and meet expectations.

- My Number coverage: ~125 million residents

- Digital Agency: est. 2021 — central DX policy driver

- Onboarding/compliance cost reduction via gov platforms

- Requirement: preserve elderly access → balanced channel strategy

Prefectural funds (Ibaraki 2.8M, Tochigi 1.9M), BoJ normalization & onboarding risks

Political stability, prefectural revitalization funds (Ibaraki ~2.8M, Tochigi ~1.9M) and FSA 2024 priorities (customer‑oriented finance, stricter risk governance) shape Mebuki’s capital and compliance needs. BoJ policy normalization (10y JGB ~0.6–1.0%) and ¥10T 2024 fiscal support affect credit demand and stress scenarios. Digital Agency push and My Number (~125M) lower onboarding costs but require elderly access safeguards.

| Factor | Key data |

|---|---|

| Prefectures | Ibaraki 2.8M / Tochigi 1.9M |

| FSA focus | 2024: conduct, credit & IRRBB |

| Macro | 10y JGB 0.6–1.0% / ¥10T fiscal |

| Digital | My Number ~125M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Mebuki Financial Group’s risk and opportunity profile, with data-backed trends and region-specific regulatory context; designed for executives and advisors to inform strategy, scenario planning and investor communications.

A concise, visually segmented PESTLE summary of Mebuki Financial Group that distills external risks and market drivers for quick reference in meetings or presentations, easily shareable and ready to drop into slides to align teams and support strategic planning.

Economic factors

Rate normalization and NIM dynamics

BoJ exit from negative rates in 2023 has pushed loan yields up while deposit costs have started rising, with 10-year JGB yields moving into roughly 0.8–1.0% by 2024–H1 2025. ALM is now critical as term premia and the curve steepen. Repricing lags can temporarily widen NIM if managed well. Hedging strategies and loan/deposit product mix will drive earnings stability.

Regional growth and SME health

Ibaraki and Tochigi economies hinge on autos, machinery, logistics and agribusiness, making regional SMEs sensitive to slower growth or inventory cycles that can strain cash flows and raise probabilities of default. SMEs account for 99.7% of Japanese firms and employ roughly 70% of the workforce, concentrating credit exposure locally. Proactive advisory and working‑capital solutions have been shown to stabilise clients and reduce NPLs, while sector diversification cuts concentration risk.

Inflation, wages, and household behavior

Moderate inflation around 3% in 2024 with gradual wage gains of roughly 2–3% is nudging households from cash holdings into time deposits and investment products. Shifts in consumption mix are already affecting card transaction volumes and merchant fee income. Expanded NISA reforms from 2024 have lifted financial planning demand, and Mebuki can capture flows via low‑cost index and ETF wrappers.

Real estate and collateral values

Regional property trends directly affect collateral coverage across Mebuki’s SME and mortgage books; higher rates since 2023 have begun to cool valuations and can extend disposal timelines by several months. Maintaining conservative LTVs (typically 60–70%) and frequent reappraisals limits loss severity. Focused redevelopment finance for station-area hubs can unlock value and improve collateral quality.

- Collateral sensitivity: regional gaps widen risk

- LTV band: 60–70%

- Sale delays: +3–6 months

- Redevelopment: station hubs boost recovery

Yen volatility and trade exposure

FX swings—yen around 155 JPY/USD in H1 2025 with ~12% 1‑yr realized vol—hit exporters and importers across Mebuki’s customer base, pushing demand for hedging, trade finance and supply‑chain solutions; credit stress could rise among energy‑intensive and import‑reliant SMEs (Japan imports ~90% of energy), while cross‑sell of risk‑management products aids fee diversification as exports remain ~18% of GDP.

- FX impact: 155 JPY/USD, ~12% vol

- Trade exposure: exports ~18% of GDP

- Energy reliance: ~90% imported

- Opportunity: hedging/trade finance = fee diversification

Prefectural funds (Ibaraki 2.8M, Tochigi 1.9M), BoJ normalization & onboarding risks

BoJ exit and 10y JGB ~0.9% (2024–H1 2025) raised loan yields and ALM risk; repricing gaps can widen NIM but hedging and product mix support stability. Regional SME concentration (99.7% of firms; ~70% workforce) and local auto/machinery exposure elevate credit sensitivity. CPI ~3% (2024) with wage gains ~2–3% shifts savings to time deposits/NISA flows; yen ~155 JPY/USD boosts hedging demand.

| Metric | Value |

|---|---|

| 10y JGB | ~0.9% |

| CPI (2024) | ~3% |

| Wage growth | 2–3% |

| Yen | ~155 JPY/USD |

| SME share | 99.7% |

| Energy imports | ~90% |

| LTV guideline | 60–70% |

Full Version Awaits

Mebuki Financial Group PESTLE Analysis

The Mebuki Financial Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment as presented. No placeholders or teasers—this is the final, downloadable file.

Original: $10.00

-65%$10.00

$3.50Description

Make Smarter Strategic Decisions with a Complete PESTEL View

Unlock strategic advantage with our PESTLE analysis of Mebuki Financial Group—concise insight into political, economic, social, technological, legal, and environmental forces shaping its prospects. Ideal for investors and advisors seeking evidence-based foresight. Purchase the full report to access actionable intelligence, charts, and recommendations ready for immediate use.

Political factors

Stable governance and regional revitalization

Japan’s long-standing political stability underpins predictable banking policy and budgeting, supporting steady operating conditions for regional banks. Ibaraki (≈2.8 million) and Tochigi (≈1.9 million) are focal prefectures for national regional revitalization programs that channel central funds to local projects. Mebuki can align lending to infrastructure and SME initiatives to tap available subsidies and credit guarantees. Close ties with prefectural authorities can improve deal flow and public–private project participation.

FSA supervision and prudential stance

Japan’s Financial Services Agency 2024 supervisory priorities emphasize customer-oriented finance, stronger risk governance and conduct, with heightened scrutiny of credit risk, interest-rate risk in the banking book and stress testing. These supervisory themes affect capital planning as firms must demonstrate resilience under stress scenarios; the Basel III CET1 regulatory minimum is 4.5% and Japanese banks typically target higher buffers. Strong compliance and risk frameworks help Mebuki maintain credibility and avoid remediation burdens, while early engagement with the FSA can smooth approvals for new products.

Monetary–fiscal coordination effects

As the BoJ moved away from ultra‑easy policy in 2023–24 (ending negative rates/yield‑curve control) and market 10‑yr JGB yields rose toward 0.6–1.0%, fiscal measures—notably ~¥10 trillion in 2024 energy and SME support—can cushion credit stress; Mebuki must balance policy‑driven lending with strict underwriting and transparent pricing/support communications to sustain stakeholder trust.

Geopolitical tensions and supply chains

Geopolitical tensions since 2024 have disrupted supply chains for auto, electronics and agriculture clients along Kanto’s northern corridor, prompting demand and input shocks that may require covenant flexibility for export-oriented borrowers.

- Resilience drives: reshoring loans and capex finance up in 2024–25

- Portfolio action: scenario planning improves stress readiness

- Risk: regional security elevates concentration and supplier risk

Digital policy and public infrastructure

Government drives — led by the Digital Agency (est. 2021) and universal My Number coverage (~125 million residents) plus cashless promotion — are reshaping public-sector DX and payment rails, so joining government platforms can materially lower onboarding friction and compliance costs for Mebuki. Political emphasis on digital inclusion mandates maintained access for elderly users, making a balanced digital/branch channel strategy important to secure public grants and meet expectations.

- My Number coverage: ~125 million residents

- Digital Agency: est. 2021 — central DX policy driver

- Onboarding/compliance cost reduction via gov platforms

- Requirement: preserve elderly access → balanced channel strategy

Prefectural funds (Ibaraki 2.8M, Tochigi 1.9M), BoJ normalization & onboarding risks

Political stability, prefectural revitalization funds (Ibaraki ~2.8M, Tochigi ~1.9M) and FSA 2024 priorities (customer‑oriented finance, stricter risk governance) shape Mebuki’s capital and compliance needs. BoJ policy normalization (10y JGB ~0.6–1.0%) and ¥10T 2024 fiscal support affect credit demand and stress scenarios. Digital Agency push and My Number (~125M) lower onboarding costs but require elderly access safeguards.

| Factor | Key data |

|---|---|

| Prefectures | Ibaraki 2.8M / Tochigi 1.9M |

| FSA focus | 2024: conduct, credit & IRRBB |

| Macro | 10y JGB 0.6–1.0% / ¥10T fiscal |

| Digital | My Number ~125M |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely shape Mebuki Financial Group’s risk and opportunity profile, with data-backed trends and region-specific regulatory context; designed for executives and advisors to inform strategy, scenario planning and investor communications.

A concise, visually segmented PESTLE summary of Mebuki Financial Group that distills external risks and market drivers for quick reference in meetings or presentations, easily shareable and ready to drop into slides to align teams and support strategic planning.

Economic factors

Rate normalization and NIM dynamics

BoJ exit from negative rates in 2023 has pushed loan yields up while deposit costs have started rising, with 10-year JGB yields moving into roughly 0.8–1.0% by 2024–H1 2025. ALM is now critical as term premia and the curve steepen. Repricing lags can temporarily widen NIM if managed well. Hedging strategies and loan/deposit product mix will drive earnings stability.

Regional growth and SME health

Ibaraki and Tochigi economies hinge on autos, machinery, logistics and agribusiness, making regional SMEs sensitive to slower growth or inventory cycles that can strain cash flows and raise probabilities of default. SMEs account for 99.7% of Japanese firms and employ roughly 70% of the workforce, concentrating credit exposure locally. Proactive advisory and working‑capital solutions have been shown to stabilise clients and reduce NPLs, while sector diversification cuts concentration risk.

Inflation, wages, and household behavior

Moderate inflation around 3% in 2024 with gradual wage gains of roughly 2–3% is nudging households from cash holdings into time deposits and investment products. Shifts in consumption mix are already affecting card transaction volumes and merchant fee income. Expanded NISA reforms from 2024 have lifted financial planning demand, and Mebuki can capture flows via low‑cost index and ETF wrappers.

Real estate and collateral values

Regional property trends directly affect collateral coverage across Mebuki’s SME and mortgage books; higher rates since 2023 have begun to cool valuations and can extend disposal timelines by several months. Maintaining conservative LTVs (typically 60–70%) and frequent reappraisals limits loss severity. Focused redevelopment finance for station-area hubs can unlock value and improve collateral quality.

- Collateral sensitivity: regional gaps widen risk

- LTV band: 60–70%

- Sale delays: +3–6 months

- Redevelopment: station hubs boost recovery

Yen volatility and trade exposure

FX swings—yen around 155 JPY/USD in H1 2025 with ~12% 1‑yr realized vol—hit exporters and importers across Mebuki’s customer base, pushing demand for hedging, trade finance and supply‑chain solutions; credit stress could rise among energy‑intensive and import‑reliant SMEs (Japan imports ~90% of energy), while cross‑sell of risk‑management products aids fee diversification as exports remain ~18% of GDP.

- FX impact: 155 JPY/USD, ~12% vol

- Trade exposure: exports ~18% of GDP

- Energy reliance: ~90% imported

- Opportunity: hedging/trade finance = fee diversification

Prefectural funds (Ibaraki 2.8M, Tochigi 1.9M), BoJ normalization & onboarding risks

BoJ exit and 10y JGB ~0.9% (2024–H1 2025) raised loan yields and ALM risk; repricing gaps can widen NIM but hedging and product mix support stability. Regional SME concentration (99.7% of firms; ~70% workforce) and local auto/machinery exposure elevate credit sensitivity. CPI ~3% (2024) with wage gains ~2–3% shifts savings to time deposits/NISA flows; yen ~155 JPY/USD boosts hedging demand.

| Metric | Value |

|---|---|

| 10y JGB | ~0.9% |

| CPI (2024) | ~3% |

| Wage growth | 2–3% |

| Yen | ~155 JPY/USD |

| SME share | 99.7% |

| Energy imports | ~90% |

| LTV guideline | 60–70% |

Full Version Awaits

Mebuki Financial Group PESTLE Analysis

The Mebuki Financial Group PESTLE Analysis preview shown here is the exact document you’ll receive after purchase—fully formatted and ready to use. It includes the complete political, economic, social, technological, legal, and environmental assessment as presented. No placeholders or teasers—this is the final, downloadable file.