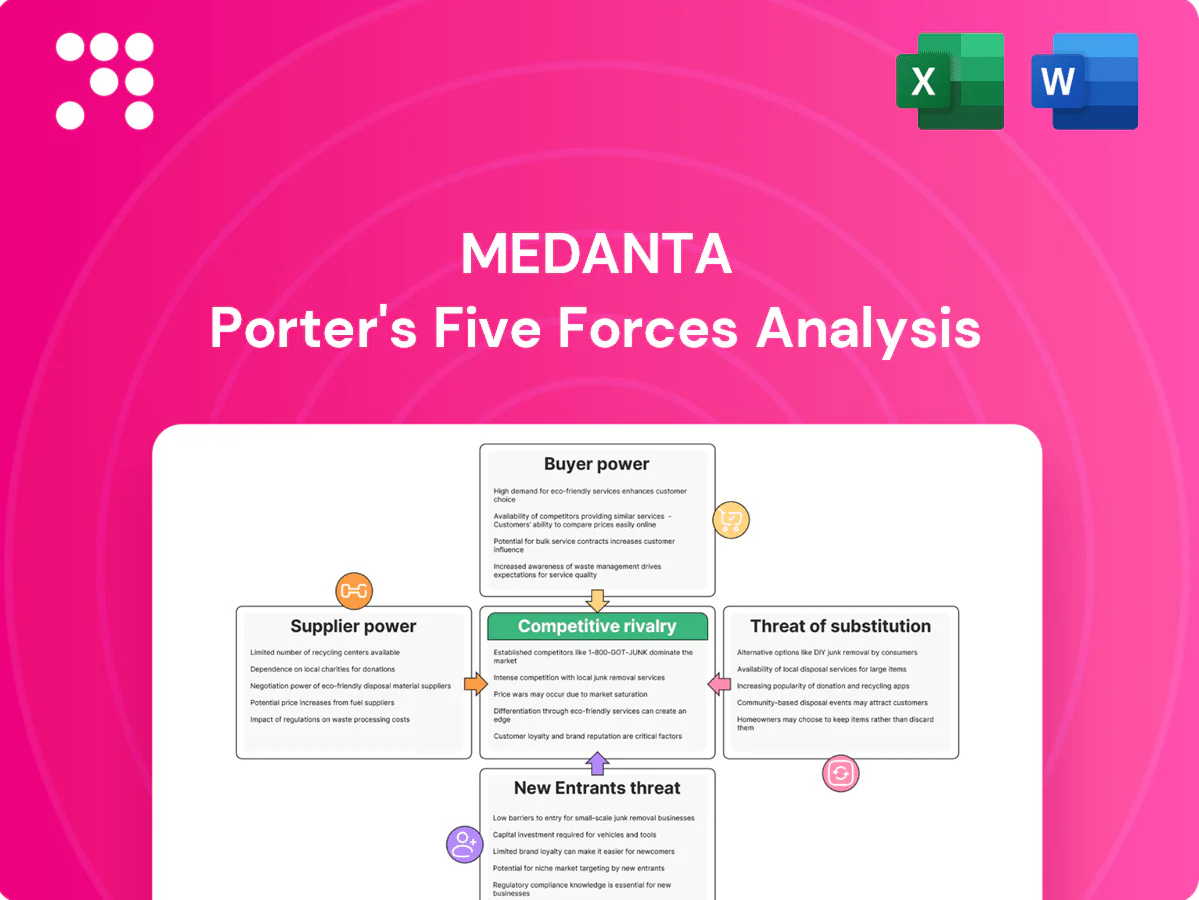

Medanta Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Medanta's Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers shaping its healthcare positioning. The brief identifies key pressures on margins and growth prospects to guide quick decisions. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Medanta’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated device suppliers

High-end devices for Medanta are sourced from a few OEMs—Siemens, GE, Philips control ~70% of MRI/CT in 2024 and Intuitive holds ~80% of surgical robots—creating high switching costs and maintenance lock-in. Limited alternatives boost pricing power for service contracts, typically 10–20% of equipment value annually. Multi-year procurement and vendor diversification reduce leverage, while group buying consortia can cut acquisition/service costs by ~5–15%.

Pharma and consumables scale

Drugs and disposables at Medanta are largely commoditized with dozens of suppliers, enabling competitive bidding and national formularies that drive better rebates and payment terms. Large-volume purchasing in 2024 leveraged scale to secure roughly 10–15% procurement savings via GPO contracts. Specialty oncology biologics and cardiovascular stents remain premium-priced, while inventory management and GPOs raised fill rates toward 95%+ to reduce leakage and stockouts.

Talent as a critical supplier

Star clinicians and specialized nurses at Medanta act as scarce suppliers with high bargaining power; Medanta employed over 2,000 clinicians in 2024, driving patient inflows and complex case mix and pressuring compensation and privileges. Long credentialing cycles and multi-year training pipelines add rigidity to staffing. Retention programs and academic affiliations help mitigate dependence.

IT and data infrastructure lock-in

EHR, PACS, LIS and cybersecurity vendors create integration lock-in at Medanta via proprietary workflows; global EHR market was valued at about USD 32.6 billion in 2024, underscoring vendor scale and bargaining power. High migration costs and downtime risks amplify vendor leverage, while negotiating modular architectures and open APIs and co-developing analytics with partners can rebalance dynamics.

- Integration lock-in: EHR/PACS/LIS workflows

- Cost driver: high migration/downtime risk

- Mitigation: modular design + open APIs

- Rebalance: co-develop analytics with vendors

Real estate and utilities constraints

Prime urban land and constrained utility access in Gurugram raise capital and operating costs for Medanta; in 2024 prime NCR land values and long municipal fit-out approvals increase lease rigidity and capex timelines.

Power reliability and medical gas supply affect clinical resilience and OPEX volatility; renewable PPAs and captive generation (solar + batteries) can cut grid exposure and lower energy spend.

Long leases limit site flexibility, so multi-site network planning across Delhi NCR and tier-2 cities diversifies location and supply risk.

- Prime land pressure: higher upfront capex and long approvals

- Utilities: grid risk mitigated by renewable PPAs / captive assets

- Medical gas suppliers: key single-source dependency

- Strategy: multi-site planning reduces concentration risk

OEMs 70–80% share; service fees 10–20%; EHR lock-in

High-end device OEMs (Siemens/GE/Philips ~70% MRI/CT; Intuitive ~80% robots in 2024) exert strong pricing/maintenance leverage; service contracts ~10–20% of equipment value annually. Commoditized drugs/disposables enable 10–15% GPO savings. Specialist clinicians and EHR/PACS vendors create integration/retention lock-in, raising switching costs.

| Supplier | Metric 2024 | Impact |

|---|---|---|

| High-end devices | 70–80% share | High leverage |

| Drugs/disposables | 10–15% GPO savings | Low power |

| Clinicians/EHR | 2,000+ clinicians; EHR market $32.6B | High lock-in |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Medanta; evaluates supplier and buyer power, substitutes and disruptive threats, and identifies barriers protecting its incumbency—delivered in editable format for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter's Five Forces analysis for Medanta that highlights competitive pressures and strategic levers—ideal for quick boardroom decisions. Easy to customize and export to decks or reports, it relieves strategic ambiguity and helps prioritize immediate actions.

Customers Bargaining Power

Insurers and TPAs aggregation

Payers steer volumes and impose package rates, documentation and denial protocols that compress hospital margins. Network inclusion and authorization turnaround times materially influence bargaining outcomes and cash flows. Case-mix optimization and robust outcome data can justify higher tariffs for specialist centers. Direct-to-employer deals reduce intermediary dependence while PM-JAY covers about 500 million beneficiaries in 2024, enhancing payer leverage.

Price-sensitive self-paying patients

Price-sensitive self-paying patients compare package rates and EMI options across hospitals, driving negotiation on margins; in 2024 Medanta operates over 1,250 beds, intensifying cross-hospital comparisons. Transparent pricing and easy access to second opinions elevate patient bargaining power, forcing clearer fee schedules. Bundled clinical pathways and public infection-rate disclosures justify premiums. Financing tie-ups (EMI/health loans) blunt sticker shock while preserving realized margins.

Government schemes influence

Public programs set capped reimbursements with strict audits; PM-JAY, covering over 540 million beneficiaries by 2024, drives high inpatient volumes but yields typically lower than private tariffs and elevates administrative burden. Hospitals optimize by selective participation across specialties and regions to protect margins and capacity. Excellence in compliance — robust audit trails and coding accuracy — reduces clawbacks and payment delays, preserving cash flow.

Corporate clients and referrals

Employer panels demand negotiated discounts, SLAs and minimum health-check volumes, compressing margins and increasing bargaining leverage; physician referral networks channel high-complexity cases that shape service mix and pricing power. Relationship management and CME outreach sustain referral inflows, while robust outcomes reporting strengthens Medanta’s negotiating stance with corporates and insurers.

- Negotiated discounts, SLAs, volumes

- Referral networks drive complex-case mix

- CME/relationship management sustain inflows

- Outcomes reporting boosts leverage

Digital transparency and reviews

- Online ratings increase comparison

- Outcome dashboards build trust

- Tele-consults raise switching

- Loyalty + care coordinators improve retention

Payer pressure and price transparency squeeze tariffs; premium tertiary hospitals protect margins

Payer bargaining (PM-JAY: 540 million beneficiaries in 2024) and employer panels compress tariffs and impose SLAs; patient price-sensitivity and online transparency raise switching and demand clearer fees. Medanta’s 1,250+ beds and outcome reporting reinforce premium pricing for specialist care while selective payer participation protects margins.

| Metric | 2024 |

|---|---|

| PM-JAY beneficiaries | 540 million |

| Medanta beds | 1,250+ |

| Payer leverage | High |

| Patient price sensitivity | High |

Preview the Actual Deliverable

Medanta Porter's Five Forces Analysis

This preview shows the exact Medanta Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Once you complete payment, you’ll get instant access to this same file for your strategic or investment needs.

Don't Miss the Bigger Picture

Medanta's Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers shaping its healthcare positioning. The brief identifies key pressures on margins and growth prospects to guide quick decisions. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Medanta’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated device suppliers

High-end devices for Medanta are sourced from a few OEMs—Siemens, GE, Philips control ~70% of MRI/CT in 2024 and Intuitive holds ~80% of surgical robots—creating high switching costs and maintenance lock-in. Limited alternatives boost pricing power for service contracts, typically 10–20% of equipment value annually. Multi-year procurement and vendor diversification reduce leverage, while group buying consortia can cut acquisition/service costs by ~5–15%.

Pharma and consumables scale

Drugs and disposables at Medanta are largely commoditized with dozens of suppliers, enabling competitive bidding and national formularies that drive better rebates and payment terms. Large-volume purchasing in 2024 leveraged scale to secure roughly 10–15% procurement savings via GPO contracts. Specialty oncology biologics and cardiovascular stents remain premium-priced, while inventory management and GPOs raised fill rates toward 95%+ to reduce leakage and stockouts.

Talent as a critical supplier

Star clinicians and specialized nurses at Medanta act as scarce suppliers with high bargaining power; Medanta employed over 2,000 clinicians in 2024, driving patient inflows and complex case mix and pressuring compensation and privileges. Long credentialing cycles and multi-year training pipelines add rigidity to staffing. Retention programs and academic affiliations help mitigate dependence.

IT and data infrastructure lock-in

EHR, PACS, LIS and cybersecurity vendors create integration lock-in at Medanta via proprietary workflows; global EHR market was valued at about USD 32.6 billion in 2024, underscoring vendor scale and bargaining power. High migration costs and downtime risks amplify vendor leverage, while negotiating modular architectures and open APIs and co-developing analytics with partners can rebalance dynamics.

- Integration lock-in: EHR/PACS/LIS workflows

- Cost driver: high migration/downtime risk

- Mitigation: modular design + open APIs

- Rebalance: co-develop analytics with vendors

Real estate and utilities constraints

Prime urban land and constrained utility access in Gurugram raise capital and operating costs for Medanta; in 2024 prime NCR land values and long municipal fit-out approvals increase lease rigidity and capex timelines.

Power reliability and medical gas supply affect clinical resilience and OPEX volatility; renewable PPAs and captive generation (solar + batteries) can cut grid exposure and lower energy spend.

Long leases limit site flexibility, so multi-site network planning across Delhi NCR and tier-2 cities diversifies location and supply risk.

- Prime land pressure: higher upfront capex and long approvals

- Utilities: grid risk mitigated by renewable PPAs / captive assets

- Medical gas suppliers: key single-source dependency

- Strategy: multi-site planning reduces concentration risk

OEMs 70–80% share; service fees 10–20%; EHR lock-in

High-end device OEMs (Siemens/GE/Philips ~70% MRI/CT; Intuitive ~80% robots in 2024) exert strong pricing/maintenance leverage; service contracts ~10–20% of equipment value annually. Commoditized drugs/disposables enable 10–15% GPO savings. Specialist clinicians and EHR/PACS vendors create integration/retention lock-in, raising switching costs.

| Supplier | Metric 2024 | Impact |

|---|---|---|

| High-end devices | 70–80% share | High leverage |

| Drugs/disposables | 10–15% GPO savings | Low power |

| Clinicians/EHR | 2,000+ clinicians; EHR market $32.6B | High lock-in |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Medanta; evaluates supplier and buyer power, substitutes and disruptive threats, and identifies barriers protecting its incumbency—delivered in editable format for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter's Five Forces analysis for Medanta that highlights competitive pressures and strategic levers—ideal for quick boardroom decisions. Easy to customize and export to decks or reports, it relieves strategic ambiguity and helps prioritize immediate actions.

Customers Bargaining Power

Insurers and TPAs aggregation

Payers steer volumes and impose package rates, documentation and denial protocols that compress hospital margins. Network inclusion and authorization turnaround times materially influence bargaining outcomes and cash flows. Case-mix optimization and robust outcome data can justify higher tariffs for specialist centers. Direct-to-employer deals reduce intermediary dependence while PM-JAY covers about 500 million beneficiaries in 2024, enhancing payer leverage.

Price-sensitive self-paying patients

Price-sensitive self-paying patients compare package rates and EMI options across hospitals, driving negotiation on margins; in 2024 Medanta operates over 1,250 beds, intensifying cross-hospital comparisons. Transparent pricing and easy access to second opinions elevate patient bargaining power, forcing clearer fee schedules. Bundled clinical pathways and public infection-rate disclosures justify premiums. Financing tie-ups (EMI/health loans) blunt sticker shock while preserving realized margins.

Government schemes influence

Public programs set capped reimbursements with strict audits; PM-JAY, covering over 540 million beneficiaries by 2024, drives high inpatient volumes but yields typically lower than private tariffs and elevates administrative burden. Hospitals optimize by selective participation across specialties and regions to protect margins and capacity. Excellence in compliance — robust audit trails and coding accuracy — reduces clawbacks and payment delays, preserving cash flow.

Corporate clients and referrals

Employer panels demand negotiated discounts, SLAs and minimum health-check volumes, compressing margins and increasing bargaining leverage; physician referral networks channel high-complexity cases that shape service mix and pricing power. Relationship management and CME outreach sustain referral inflows, while robust outcomes reporting strengthens Medanta’s negotiating stance with corporates and insurers.

- Negotiated discounts, SLAs, volumes

- Referral networks drive complex-case mix

- CME/relationship management sustain inflows

- Outcomes reporting boosts leverage

Digital transparency and reviews

- Online ratings increase comparison

- Outcome dashboards build trust

- Tele-consults raise switching

- Loyalty + care coordinators improve retention

Payer pressure and price transparency squeeze tariffs; premium tertiary hospitals protect margins

Payer bargaining (PM-JAY: 540 million beneficiaries in 2024) and employer panels compress tariffs and impose SLAs; patient price-sensitivity and online transparency raise switching and demand clearer fees. Medanta’s 1,250+ beds and outcome reporting reinforce premium pricing for specialist care while selective payer participation protects margins.

| Metric | 2024 |

|---|---|

| PM-JAY beneficiaries | 540 million |

| Medanta beds | 1,250+ |

| Payer leverage | High |

| Patient price sensitivity | High |

Preview the Actual Deliverable

Medanta Porter's Five Forces Analysis

This preview shows the exact Medanta Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Once you complete payment, you’ll get instant access to this same file for your strategic or investment needs.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Medanta's Porter’s Five Forces snapshot highlights competitive rivalry, supplier and buyer power, threat of substitutes, and entry barriers shaping its healthcare positioning. The brief identifies key pressures on margins and growth prospects to guide quick decisions. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Medanta’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Concentrated device suppliers

High-end devices for Medanta are sourced from a few OEMs—Siemens, GE, Philips control ~70% of MRI/CT in 2024 and Intuitive holds ~80% of surgical robots—creating high switching costs and maintenance lock-in. Limited alternatives boost pricing power for service contracts, typically 10–20% of equipment value annually. Multi-year procurement and vendor diversification reduce leverage, while group buying consortia can cut acquisition/service costs by ~5–15%.

Pharma and consumables scale

Drugs and disposables at Medanta are largely commoditized with dozens of suppliers, enabling competitive bidding and national formularies that drive better rebates and payment terms. Large-volume purchasing in 2024 leveraged scale to secure roughly 10–15% procurement savings via GPO contracts. Specialty oncology biologics and cardiovascular stents remain premium-priced, while inventory management and GPOs raised fill rates toward 95%+ to reduce leakage and stockouts.

Talent as a critical supplier

Star clinicians and specialized nurses at Medanta act as scarce suppliers with high bargaining power; Medanta employed over 2,000 clinicians in 2024, driving patient inflows and complex case mix and pressuring compensation and privileges. Long credentialing cycles and multi-year training pipelines add rigidity to staffing. Retention programs and academic affiliations help mitigate dependence.

IT and data infrastructure lock-in

EHR, PACS, LIS and cybersecurity vendors create integration lock-in at Medanta via proprietary workflows; global EHR market was valued at about USD 32.6 billion in 2024, underscoring vendor scale and bargaining power. High migration costs and downtime risks amplify vendor leverage, while negotiating modular architectures and open APIs and co-developing analytics with partners can rebalance dynamics.

- Integration lock-in: EHR/PACS/LIS workflows

- Cost driver: high migration/downtime risk

- Mitigation: modular design + open APIs

- Rebalance: co-develop analytics with vendors

Real estate and utilities constraints

Prime urban land and constrained utility access in Gurugram raise capital and operating costs for Medanta; in 2024 prime NCR land values and long municipal fit-out approvals increase lease rigidity and capex timelines.

Power reliability and medical gas supply affect clinical resilience and OPEX volatility; renewable PPAs and captive generation (solar + batteries) can cut grid exposure and lower energy spend.

Long leases limit site flexibility, so multi-site network planning across Delhi NCR and tier-2 cities diversifies location and supply risk.

- Prime land pressure: higher upfront capex and long approvals

- Utilities: grid risk mitigated by renewable PPAs / captive assets

- Medical gas suppliers: key single-source dependency

- Strategy: multi-site planning reduces concentration risk

OEMs 70–80% share; service fees 10–20%; EHR lock-in

High-end device OEMs (Siemens/GE/Philips ~70% MRI/CT; Intuitive ~80% robots in 2024) exert strong pricing/maintenance leverage; service contracts ~10–20% of equipment value annually. Commoditized drugs/disposables enable 10–15% GPO savings. Specialist clinicians and EHR/PACS vendors create integration/retention lock-in, raising switching costs.

| Supplier | Metric 2024 | Impact |

|---|---|---|

| High-end devices | 70–80% share | High leverage |

| Drugs/disposables | 10–15% GPO savings | Low power |

| Clinicians/EHR | 2,000+ clinicians; EHR market $32.6B | High lock-in |

What is included in the product

Uncovers key drivers of competition, customer influence, and market entry risks for Medanta; evaluates supplier and buyer power, substitutes and disruptive threats, and identifies barriers protecting its incumbency—delivered in editable format for use in investor materials, strategy decks, or academic projects.

A concise, one-sheet Porter's Five Forces analysis for Medanta that highlights competitive pressures and strategic levers—ideal for quick boardroom decisions. Easy to customize and export to decks or reports, it relieves strategic ambiguity and helps prioritize immediate actions.

Customers Bargaining Power

Insurers and TPAs aggregation

Payers steer volumes and impose package rates, documentation and denial protocols that compress hospital margins. Network inclusion and authorization turnaround times materially influence bargaining outcomes and cash flows. Case-mix optimization and robust outcome data can justify higher tariffs for specialist centers. Direct-to-employer deals reduce intermediary dependence while PM-JAY covers about 500 million beneficiaries in 2024, enhancing payer leverage.

Price-sensitive self-paying patients

Price-sensitive self-paying patients compare package rates and EMI options across hospitals, driving negotiation on margins; in 2024 Medanta operates over 1,250 beds, intensifying cross-hospital comparisons. Transparent pricing and easy access to second opinions elevate patient bargaining power, forcing clearer fee schedules. Bundled clinical pathways and public infection-rate disclosures justify premiums. Financing tie-ups (EMI/health loans) blunt sticker shock while preserving realized margins.

Government schemes influence

Public programs set capped reimbursements with strict audits; PM-JAY, covering over 540 million beneficiaries by 2024, drives high inpatient volumes but yields typically lower than private tariffs and elevates administrative burden. Hospitals optimize by selective participation across specialties and regions to protect margins and capacity. Excellence in compliance — robust audit trails and coding accuracy — reduces clawbacks and payment delays, preserving cash flow.

Corporate clients and referrals

Employer panels demand negotiated discounts, SLAs and minimum health-check volumes, compressing margins and increasing bargaining leverage; physician referral networks channel high-complexity cases that shape service mix and pricing power. Relationship management and CME outreach sustain referral inflows, while robust outcomes reporting strengthens Medanta’s negotiating stance with corporates and insurers.

- Negotiated discounts, SLAs, volumes

- Referral networks drive complex-case mix

- CME/relationship management sustain inflows

- Outcomes reporting boosts leverage

Digital transparency and reviews

- Online ratings increase comparison

- Outcome dashboards build trust

- Tele-consults raise switching

- Loyalty + care coordinators improve retention

Payer pressure and price transparency squeeze tariffs; premium tertiary hospitals protect margins

Payer bargaining (PM-JAY: 540 million beneficiaries in 2024) and employer panels compress tariffs and impose SLAs; patient price-sensitivity and online transparency raise switching and demand clearer fees. Medanta’s 1,250+ beds and outcome reporting reinforce premium pricing for specialist care while selective payer participation protects margins.

| Metric | 2024 |

|---|---|

| PM-JAY beneficiaries | 540 million |

| Medanta beds | 1,250+ |

| Payer leverage | High |

| Patient price sensitivity | High |

Preview the Actual Deliverable

Medanta Porter's Five Forces Analysis

This preview shows the exact Medanta Porter's Five Forces Analysis you'll receive after purchase—no placeholders or mockups. The document is fully formatted, professionally written, and ready for immediate download and use. Once you complete payment, you’ll get instant access to this same file for your strategic or investment needs.