Medanta SWOT Analysis

Dive Deeper Into the Company’s Strategic Blueprint

Medanta's strong brand, clinical expertise, and multi-specialty footprint position it well against rising healthcare demand, yet regulatory pressures and margin risks warrant close attention; purchase the full SWOT analysis for a detailed, editable report and Excel tools to guide strategic, investment, and operational decisions.

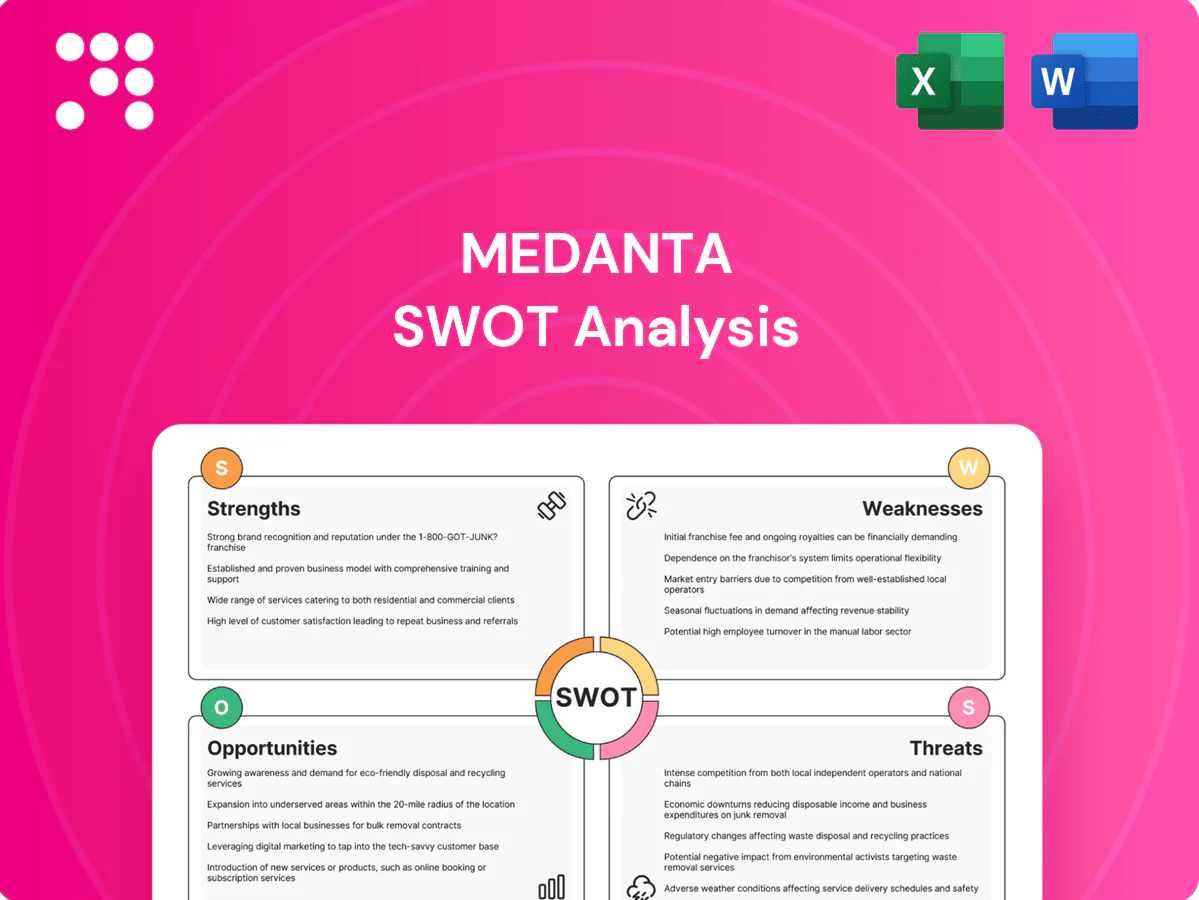

Strengths

Integrated multi-specialty care

Medanta’s integrated multi-specialty platform spans cardiology, oncology, neurosciences, orthopaedics and other tertiary disciplines, enabling end-to-end care under one roof. Integrated diagnostics-to-surgery pathways tighten coordination and reduce time-to-treatment, supporting faster clinical decision-making. The breadth of services boosts cross-referrals and share of patient wallet while enabling management of complex cases and improved outcomes.

Advanced tertiary and quaternary capabilities

Medanta manages high-acuity procedures, transplants and advanced critical care, differentiating it from general hospitals and attracting complex referrals and tertiary cases.

Access to cutting-edge technology—robotics, ECMO and advanced imaging—boosts precision and outcomes; in 2024 Medanta operated over 1,400 beds across campuses with a clinician base exceeding 1,500.

These tertiary/quaternary capabilities command premium pricing and reinforce brand equity among patients and referring clinicians.

Strong brand and clinical reputation

Recognized for quality and reliability, Medanta benefits from strong patient trust and widespread physician endorsements, lowering acquisition costs and enabling premium service lines. Positive clinical outcomes and national accreditations reinforce credibility and referral volumes. This brand strength strengthens Medanta’s position in payer negotiations and strategic partnerships.

Experienced clinician leadership

Senior specialists and program heads anchor Medanta's centers of excellence, driving standardized protocols, continuous training and rapid adoption of clinical research; this leadership has yielded measurable improvements in case mix management and complication rates. Stable clinician leadership strengthens referral networks and helps attract top talent and institutional academic collaborations. These leaders also oversee quality metrics and specialty program growth.

- leadership-driven protocols

- improved case mix & outcomes

- talent attraction & academic ties

Robust diagnostics and critical care infrastructure

Robust diagnostics and ICUs at Medanta—comprehensive imaging, labs and multi-disciplinary ICUs—enable rapid, accurate clinical decisions while in-house capabilities cut turnaround times and patient leakage. High fixed-asset utilization raises operating leverage, supporting sustained margins. This backbone underpins both emergency throughput and elective surgical volumes.

- Comprehensive imaging and labs

- In-house testing reduces TAT and leakage

- High fixed-asset utilization improves operating leverage

- Supports emergency and elective volumes

Tertiary/quaternary care platform delivering high-acuity procedures and premium pricing

Medanta’s multi‑specialty tertiary/quaternary platform (cardio, oncology, neuro, ortho) delivers end‑to‑end care, high‑acuity procedures and premium pricing, backed by advanced tech and strong clinician leadership; in 2024 it operated over 1,400 beds with a clinician base exceeding 1,500, supporting high asset utilization, strong referral volumes and national accreditations.

| Metric | Value |

|---|---|

| Beds (2024) | >1,400 |

| Clinicians | >1,500 |

| Core strengths | Tertiary care, tech, accreditations |

What is included in the product

Provides a clear SWOT framework for analyzing Medanta’s business strategy, highlighting internal capabilities, market strengths, growth drivers, operational gaps, and risks shaping its competitive position.

Provides a concise Medanta SWOT matrix for fast alignment of clinical, operational and growth priorities, enabling quick stakeholder briefings and actionable planning.

Weaknesses

Capital-intensive cost structure

High upfront investments in advanced diagnostic and surgical equipment and facility expansion raise depreciation and interest burdens for Medanta, while high operating leverage makes margins and net income sensitive to patient-volume swings; ongoing maintenance capex to keep technology current further limits free cash flow in downcycles, constraining reinvestment and balance-sheet flexibility.

Urban concentration risk

Medanta's facilities are concentrated in metro hubs—its flagship in Gurugram plus other city centres—exposing the network to intense local competition and market saturation. Dependence on city catchments increases sensitivity to regional disruptions and limits patient diversification. Urban real estate and skilled labor premiums—often 20–40% higher than non-metro rates—can compress margins versus a diversified footprint.

Talent dependence and retention

Clinical volumes at Medanta hinge on a small set of super‑specialists, so attrition of key doctors can materially shift case mix and revenue concentration risk. India's doctor density is about 0.9 per 1,000 population (WHO), intensifying competition for talent and driving higher payroll and incentive pressure. Global clinician burnout remains high—Medscape 2023 found ~47% of physicians reporting burnout—reducing productivity and outcomes, while depth of succession pipelines is costly and difficult to sustain.

Complex operational workflows

Complex multi-specialty pathways at Medanta raise coordination overhead across its large network (flagship Medicity ~1,250 beds), causing interdepartmental variability that can create bottlenecks and longer average LOS in high-acuity units; standardization and IT integration require significant CAPEX and training, and operational inefficiencies risk eroding patient experience and margins.

- Coordination overhead

- Interdepartmental variability

- High CAPEX for IT

- Patient experience & margin risk

Payor mix exposure

Medanta’s payor mix exposes it to insurer/TPA pricing pressure and authorization delays, while government schemes like Ayushman Bharat carry lower tariffs and slower reimbursements, straining margins and working capital; management has noted rising claim denials impacting cash flows and variable negotiating power across specialties and regions.

- Higher insurer/TPA dependence

- Lower tariffs, delayed govt payments

- Rising denial rates hurt cash flow

- Negotiating power varies by specialty/region

High fixed costs, CAPEX and 20-40% staff premiums squeeze margins; payor mix delays cash

High fixed costs and ongoing tech CAPEX at flagship Medicity (~1,250 beds) make margins volume‑sensitive; urban real‑estate and skilled‑staff premiums (20–40% higher) compress returns. Heavy dependence on super‑specialists amid India doctor density ~0.9/1,000 and physician burnout ~47% raises attrition risk. Payor mix leans on insurers/TPAs and low‑tariff govt schemes, increasing reimbursement delays and denial exposure.

| Weakness | Metric | Impact |

|---|---|---|

| Fixed/CAPEX | Medicity ~1,250 beds | High depreciation, cash strain |

| Labor risk | 0.9 doctors/1,000; 47% burnout | Attrition, higher pay |

| Urban costs | 20–40% premium | Margin compression |

Preview Before You Purchase

Medanta SWOT Analysis

This is the actual Medanta SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get. Once purchased, the complete, editable version is unlocked for download. Buy now to access the entire in-depth analysis.

Dive Deeper Into the Company’s Strategic Blueprint

Medanta's strong brand, clinical expertise, and multi-specialty footprint position it well against rising healthcare demand, yet regulatory pressures and margin risks warrant close attention; purchase the full SWOT analysis for a detailed, editable report and Excel tools to guide strategic, investment, and operational decisions.

Strengths

Integrated multi-specialty care

Medanta’s integrated multi-specialty platform spans cardiology, oncology, neurosciences, orthopaedics and other tertiary disciplines, enabling end-to-end care under one roof. Integrated diagnostics-to-surgery pathways tighten coordination and reduce time-to-treatment, supporting faster clinical decision-making. The breadth of services boosts cross-referrals and share of patient wallet while enabling management of complex cases and improved outcomes.

Advanced tertiary and quaternary capabilities

Medanta manages high-acuity procedures, transplants and advanced critical care, differentiating it from general hospitals and attracting complex referrals and tertiary cases.

Access to cutting-edge technology—robotics, ECMO and advanced imaging—boosts precision and outcomes; in 2024 Medanta operated over 1,400 beds across campuses with a clinician base exceeding 1,500.

These tertiary/quaternary capabilities command premium pricing and reinforce brand equity among patients and referring clinicians.

Strong brand and clinical reputation

Recognized for quality and reliability, Medanta benefits from strong patient trust and widespread physician endorsements, lowering acquisition costs and enabling premium service lines. Positive clinical outcomes and national accreditations reinforce credibility and referral volumes. This brand strength strengthens Medanta’s position in payer negotiations and strategic partnerships.

Experienced clinician leadership

Senior specialists and program heads anchor Medanta's centers of excellence, driving standardized protocols, continuous training and rapid adoption of clinical research; this leadership has yielded measurable improvements in case mix management and complication rates. Stable clinician leadership strengthens referral networks and helps attract top talent and institutional academic collaborations. These leaders also oversee quality metrics and specialty program growth.

- leadership-driven protocols

- improved case mix & outcomes

- talent attraction & academic ties

Robust diagnostics and critical care infrastructure

Robust diagnostics and ICUs at Medanta—comprehensive imaging, labs and multi-disciplinary ICUs—enable rapid, accurate clinical decisions while in-house capabilities cut turnaround times and patient leakage. High fixed-asset utilization raises operating leverage, supporting sustained margins. This backbone underpins both emergency throughput and elective surgical volumes.

- Comprehensive imaging and labs

- In-house testing reduces TAT and leakage

- High fixed-asset utilization improves operating leverage

- Supports emergency and elective volumes

Tertiary/quaternary care platform delivering high-acuity procedures and premium pricing

Medanta’s multi‑specialty tertiary/quaternary platform (cardio, oncology, neuro, ortho) delivers end‑to‑end care, high‑acuity procedures and premium pricing, backed by advanced tech and strong clinician leadership; in 2024 it operated over 1,400 beds with a clinician base exceeding 1,500, supporting high asset utilization, strong referral volumes and national accreditations.

| Metric | Value |

|---|---|

| Beds (2024) | >1,400 |

| Clinicians | >1,500 |

| Core strengths | Tertiary care, tech, accreditations |

What is included in the product

Provides a clear SWOT framework for analyzing Medanta’s business strategy, highlighting internal capabilities, market strengths, growth drivers, operational gaps, and risks shaping its competitive position.

Provides a concise Medanta SWOT matrix for fast alignment of clinical, operational and growth priorities, enabling quick stakeholder briefings and actionable planning.

Weaknesses

Capital-intensive cost structure

High upfront investments in advanced diagnostic and surgical equipment and facility expansion raise depreciation and interest burdens for Medanta, while high operating leverage makes margins and net income sensitive to patient-volume swings; ongoing maintenance capex to keep technology current further limits free cash flow in downcycles, constraining reinvestment and balance-sheet flexibility.

Urban concentration risk

Medanta's facilities are concentrated in metro hubs—its flagship in Gurugram plus other city centres—exposing the network to intense local competition and market saturation. Dependence on city catchments increases sensitivity to regional disruptions and limits patient diversification. Urban real estate and skilled labor premiums—often 20–40% higher than non-metro rates—can compress margins versus a diversified footprint.

Talent dependence and retention

Clinical volumes at Medanta hinge on a small set of super‑specialists, so attrition of key doctors can materially shift case mix and revenue concentration risk. India's doctor density is about 0.9 per 1,000 population (WHO), intensifying competition for talent and driving higher payroll and incentive pressure. Global clinician burnout remains high—Medscape 2023 found ~47% of physicians reporting burnout—reducing productivity and outcomes, while depth of succession pipelines is costly and difficult to sustain.

Complex operational workflows

Complex multi-specialty pathways at Medanta raise coordination overhead across its large network (flagship Medicity ~1,250 beds), causing interdepartmental variability that can create bottlenecks and longer average LOS in high-acuity units; standardization and IT integration require significant CAPEX and training, and operational inefficiencies risk eroding patient experience and margins.

- Coordination overhead

- Interdepartmental variability

- High CAPEX for IT

- Patient experience & margin risk

Payor mix exposure

Medanta’s payor mix exposes it to insurer/TPA pricing pressure and authorization delays, while government schemes like Ayushman Bharat carry lower tariffs and slower reimbursements, straining margins and working capital; management has noted rising claim denials impacting cash flows and variable negotiating power across specialties and regions.

- Higher insurer/TPA dependence

- Lower tariffs, delayed govt payments

- Rising denial rates hurt cash flow

- Negotiating power varies by specialty/region

High fixed costs, CAPEX and 20-40% staff premiums squeeze margins; payor mix delays cash

High fixed costs and ongoing tech CAPEX at flagship Medicity (~1,250 beds) make margins volume‑sensitive; urban real‑estate and skilled‑staff premiums (20–40% higher) compress returns. Heavy dependence on super‑specialists amid India doctor density ~0.9/1,000 and physician burnout ~47% raises attrition risk. Payor mix leans on insurers/TPAs and low‑tariff govt schemes, increasing reimbursement delays and denial exposure.

| Weakness | Metric | Impact |

|---|---|---|

| Fixed/CAPEX | Medicity ~1,250 beds | High depreciation, cash strain |

| Labor risk | 0.9 doctors/1,000; 47% burnout | Attrition, higher pay |

| Urban costs | 20–40% premium | Margin compression |

Preview Before You Purchase

Medanta SWOT Analysis

This is the actual Medanta SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get. Once purchased, the complete, editable version is unlocked for download. Buy now to access the entire in-depth analysis.

Original: $10.00

-65%$10.00

$3.50Description

Dive Deeper Into the Company’s Strategic Blueprint

Medanta's strong brand, clinical expertise, and multi-specialty footprint position it well against rising healthcare demand, yet regulatory pressures and margin risks warrant close attention; purchase the full SWOT analysis for a detailed, editable report and Excel tools to guide strategic, investment, and operational decisions.

Strengths

Integrated multi-specialty care

Medanta’s integrated multi-specialty platform spans cardiology, oncology, neurosciences, orthopaedics and other tertiary disciplines, enabling end-to-end care under one roof. Integrated diagnostics-to-surgery pathways tighten coordination and reduce time-to-treatment, supporting faster clinical decision-making. The breadth of services boosts cross-referrals and share of patient wallet while enabling management of complex cases and improved outcomes.

Advanced tertiary and quaternary capabilities

Medanta manages high-acuity procedures, transplants and advanced critical care, differentiating it from general hospitals and attracting complex referrals and tertiary cases.

Access to cutting-edge technology—robotics, ECMO and advanced imaging—boosts precision and outcomes; in 2024 Medanta operated over 1,400 beds across campuses with a clinician base exceeding 1,500.

These tertiary/quaternary capabilities command premium pricing and reinforce brand equity among patients and referring clinicians.

Strong brand and clinical reputation

Recognized for quality and reliability, Medanta benefits from strong patient trust and widespread physician endorsements, lowering acquisition costs and enabling premium service lines. Positive clinical outcomes and national accreditations reinforce credibility and referral volumes. This brand strength strengthens Medanta’s position in payer negotiations and strategic partnerships.

Experienced clinician leadership

Senior specialists and program heads anchor Medanta's centers of excellence, driving standardized protocols, continuous training and rapid adoption of clinical research; this leadership has yielded measurable improvements in case mix management and complication rates. Stable clinician leadership strengthens referral networks and helps attract top talent and institutional academic collaborations. These leaders also oversee quality metrics and specialty program growth.

- leadership-driven protocols

- improved case mix & outcomes

- talent attraction & academic ties

Robust diagnostics and critical care infrastructure

Robust diagnostics and ICUs at Medanta—comprehensive imaging, labs and multi-disciplinary ICUs—enable rapid, accurate clinical decisions while in-house capabilities cut turnaround times and patient leakage. High fixed-asset utilization raises operating leverage, supporting sustained margins. This backbone underpins both emergency throughput and elective surgical volumes.

- Comprehensive imaging and labs

- In-house testing reduces TAT and leakage

- High fixed-asset utilization improves operating leverage

- Supports emergency and elective volumes

Tertiary/quaternary care platform delivering high-acuity procedures and premium pricing

Medanta’s multi‑specialty tertiary/quaternary platform (cardio, oncology, neuro, ortho) delivers end‑to‑end care, high‑acuity procedures and premium pricing, backed by advanced tech and strong clinician leadership; in 2024 it operated over 1,400 beds with a clinician base exceeding 1,500, supporting high asset utilization, strong referral volumes and national accreditations.

| Metric | Value |

|---|---|

| Beds (2024) | >1,400 |

| Clinicians | >1,500 |

| Core strengths | Tertiary care, tech, accreditations |

What is included in the product

Provides a clear SWOT framework for analyzing Medanta’s business strategy, highlighting internal capabilities, market strengths, growth drivers, operational gaps, and risks shaping its competitive position.

Provides a concise Medanta SWOT matrix for fast alignment of clinical, operational and growth priorities, enabling quick stakeholder briefings and actionable planning.

Weaknesses

Capital-intensive cost structure

High upfront investments in advanced diagnostic and surgical equipment and facility expansion raise depreciation and interest burdens for Medanta, while high operating leverage makes margins and net income sensitive to patient-volume swings; ongoing maintenance capex to keep technology current further limits free cash flow in downcycles, constraining reinvestment and balance-sheet flexibility.

Urban concentration risk

Medanta's facilities are concentrated in metro hubs—its flagship in Gurugram plus other city centres—exposing the network to intense local competition and market saturation. Dependence on city catchments increases sensitivity to regional disruptions and limits patient diversification. Urban real estate and skilled labor premiums—often 20–40% higher than non-metro rates—can compress margins versus a diversified footprint.

Talent dependence and retention

Clinical volumes at Medanta hinge on a small set of super‑specialists, so attrition of key doctors can materially shift case mix and revenue concentration risk. India's doctor density is about 0.9 per 1,000 population (WHO), intensifying competition for talent and driving higher payroll and incentive pressure. Global clinician burnout remains high—Medscape 2023 found ~47% of physicians reporting burnout—reducing productivity and outcomes, while depth of succession pipelines is costly and difficult to sustain.

Complex operational workflows

Complex multi-specialty pathways at Medanta raise coordination overhead across its large network (flagship Medicity ~1,250 beds), causing interdepartmental variability that can create bottlenecks and longer average LOS in high-acuity units; standardization and IT integration require significant CAPEX and training, and operational inefficiencies risk eroding patient experience and margins.

- Coordination overhead

- Interdepartmental variability

- High CAPEX for IT

- Patient experience & margin risk

Payor mix exposure

Medanta’s payor mix exposes it to insurer/TPA pricing pressure and authorization delays, while government schemes like Ayushman Bharat carry lower tariffs and slower reimbursements, straining margins and working capital; management has noted rising claim denials impacting cash flows and variable negotiating power across specialties and regions.

- Higher insurer/TPA dependence

- Lower tariffs, delayed govt payments

- Rising denial rates hurt cash flow

- Negotiating power varies by specialty/region

High fixed costs, CAPEX and 20-40% staff premiums squeeze margins; payor mix delays cash

High fixed costs and ongoing tech CAPEX at flagship Medicity (~1,250 beds) make margins volume‑sensitive; urban real‑estate and skilled‑staff premiums (20–40% higher) compress returns. Heavy dependence on super‑specialists amid India doctor density ~0.9/1,000 and physician burnout ~47% raises attrition risk. Payor mix leans on insurers/TPAs and low‑tariff govt schemes, increasing reimbursement delays and denial exposure.

| Weakness | Metric | Impact |

|---|---|---|

| Fixed/CAPEX | Medicity ~1,250 beds | High depreciation, cash strain |

| Labor risk | 0.9 doctors/1,000; 47% burnout | Attrition, higher pay |

| Urban costs | 20–40% premium | Margin compression |

Preview Before You Purchase

Medanta SWOT Analysis

This is the actual Medanta SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report you'll get. Once purchased, the complete, editable version is unlocked for download. Buy now to access the entire in-depth analysis.