Media World LLC Porter's Five Forces Analysis

Don't Miss the Bigger Picture

Media World LLC's Porter's Five Forces snapshot highlights high competitive rivalry, moderate buyer power, supplier leverage from key content providers, rising substitute threats from streaming platforms, and barriers that limit new entrants. This concise view identifies strategic pressure points and opportunity areas. The complete report reveals force-by-force ratings, visuals, and actionable implications. Unlock the full Porter's Five Forces Analysis to guide smart investment and strategy decisions.

Suppliers Bargaining Power

Concentrated site rights

Prime arterial sites in the UAE are controlled by municipalities, the RTA and a handful of landlords, concentrating supply and raising supplier leverage over fees and terms. Limited concession windows and exclusivities force higher upfront and ongoing charges, squeezing operator margins. Renewal risk often triggers steep rent escalations tied to market resets. Diversifying across the seven Emirates reduces exposure to any single authority.

Permit and compliance dependence

Regulatory approvals, safety codes and content rules are critical inputs that suppliers of permits can use to delay or constrain inventory, cutting Media World LLCs flexibility and bargaining power; EU GDPR-related fines topped about €1.6 billion in 2023 and regulatory enforcement persisted into 2024, raising compliance stakes. Non-compliance penalties materially raise effective costs and switching is often infeasible, though a strong compliance record can modestly soften authorities stance.

Hardware and tech vendors

Hardware and tech vendors—LED screen makers, structure fabricators and CMS providers—retain leverage in a quality-driven DOOH market where the top 5 LED manufacturers capture over 60% of global display revenues; 2024 industry reports show panel lead times of roughly 12–20 weeks and import/tariff-driven cost uplifts commonly cited near 8–12%, while multi-vendor frameworks and standards-based CMS reduce vendor lock-in.

Maintenance and ops services

Maintenance and ops services—cranes, cleaning, electrical, monitoring—are essential to uptime SLAs; skilled high-mast technicians are scarce and certified electrician median pay was about $62,000 in 2024, increasing supplier leverage and rates. Downtime penalties drive operators to accept costly terms; building in-house teams or locking multi-year contracts can shift bargaining power back.

- Essential services: cranes, cleaning, electrical, monitoring

- Labor scarcity: certified technicians scarce; electrician median pay ~62,000 (2024)

- Downtime risk: penalties push acceptance of supplier terms

- Mitigants: in-house capability or long-term contracts

Utility and data inputs

Utility and data input suppliers meaningfully affect Media World LLC: US commercial electricity averaged about $0.13/kWh in 2024, raising site operating costs while incumbent utility monopolies in many regions limit negotiation latitude; data connectivity and CDN fees vary with 5G and fiber penetration, and audience analytics vendors owning unique mobility datasets commanded premium pricing in 2024, often 15–25% above commodity rates, while bundled contracts lowered per-site costs.

- Electricity: US commercial ≈ $0.13/kWh (2024)

- Vendor power: utility monopolies reduce leverage

- Analytics: mobility datasets +15–25% premium (2024)

- Bundling: lowers per-site unit cost

Supplier leverage: top-5 LEDs > 60%, 12-20 wk lead, electricity ~$0.13/kWh

Suppliers exert high leverage via concentrated prime-site landlords, regulatory permit authorities and dominant LED/analytics vendors, compressing margins and raising switching costs. Critical inputs (LEDs, technicians, utilities, data) showed 2024 pressures: top-5 LED makers >60% share, panel lead times 12–20 weeks, electrician median pay ~$62,000, US commercial electricity ~$0.13/kWh. Long-term contracts, vertical ops and geographic diversification are key mitigants.

| Input | 2024 metric | Impact |

|---|---|---|

| Landlords/permits | High concentration | Fee leverage, escalations |

| LED vendors | Top-5 >60% share; 12–20 wk lead | Price & supply risk |

| Technicians | Median pay ~$62,000 | Higher Opex |

| Electricity | US commercial ~$0.13/kWh | Site cost pressure |

| Analytics | Premium +15–25% | Higher data costs |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, barriers to entry, substitutes and disruptive threats specific to Media World LLC, with strategic commentary and editable Word-ready insights for investor decks and internal planning.

One-sheet Porter's Five Forces for Media World LLC that visualizes competitive pressure with an editable spider chart—customize inputs, swap labels, and copy straight into pitch decks or Excel dashboards for instant strategic clarity.

Customers Bargaining Power

Agency-led consolidation

Global and regional media agencies aggregate client spend—Magna forecasted global ad revenues near $850B in 2024—allowing them to negotiate volume discounts, makegoods and value-adds that compress vendor margins. Preferred partner lists and centralized buying can shave margins by several percentage points and limit pricing power. Media World tempers this by building direct-client relationships and bespoke offerings to reclaim margin and control of data.

Large-brand budget leverage

Telco, finance, government and FMCG advertisers in the UAE exert outsized control over OOH budgets, leveraging scale to demand rate concessions and secure premium sites across a market serving roughly 10 million residents (2024 est.).

Their briefs routinely require bespoke creative and data-backed reporting, driving suppliers to provide end-to-end turnkey solutions that bundle inventory, production and analytics.

Such integrated offerings raise switching costs and entrench incumbent media owners when large clients seek guaranteed reach and measurement consistency.

Performance and accountability

Buyers increasingly demand mobility-based reach, cross-device attribution, and dynamic content triggers, with 72% of advertisers in 2024 citing cross-channel attribution as a top buying requirement.

Lack of a standardized currency weakens pricing power unless Media World offers robust, transparent measurement; DOOH proof-of-play and third-party verification became baseline requirements in 2024 market RFPs.

Investing in analytics and verified attribution platforms reduces buyer pushback and can increase win rates and CPMs by double digits versus unverified inventory.

Substitution threats in negotiations

Clients shift to social, mobile, CTV and search when OOH pricing rises; digital took about 62% of global ad spend in 2024, strengthening buyer leverage. CTV ad spend grew roughly 21% YoY in 2024, making it a credible outside option. Bundled cross-format packages blunt substitution, while seasonal demand spikes still allow yield management on prime OOH sites.

- Buyers leverage: digital 62% share (2024)

- CTV growth ≈21% YoY (2024)

- Bundle mitigation vs seasonal yield on prime sites

Contract flexibility expectations

Buyers increasingly demand contract flexibility—shorter terms, option holds, and cancellation clauses—driven by event-driven budgets and economic cycles; in 2024 roughly 45% of media buyers cited agility and rate protections as top priorities, raising bargaining power versus platforms like Media World LLC.

- Shorter terms favored

- Option holds common

- Cancellation clauses demanded

- Tiered pricing + dynamic avail balance risk

Buyers Tighten Media Margins: Digital Share, CTV Growth and Measurement Demand Shift Power

Large advertisers and global agencies (Magna: global ad revenue ~$850B in 2024) secure discounts and flexible terms, compressing Media World margins. 62% digital share and 21% CTV growth in 2024 increase buyer substitution. Demand for verified measurement and shorter contracts raises buyer leverage; analytics investments restore pricing power.

| Metric | 2024 | Impact |

|---|---|---|

| Global ad revenue | $850B | Higher buyer clout |

| Digital share | 62% | Substitution risk |

| CTV YoY | 21% | Alternative channel |

| Buyers prioritizing agility | 45% | Shorter contracts |

| UAE population | ~10M | Concentrated OOH demand |

Preview the Actual Deliverable

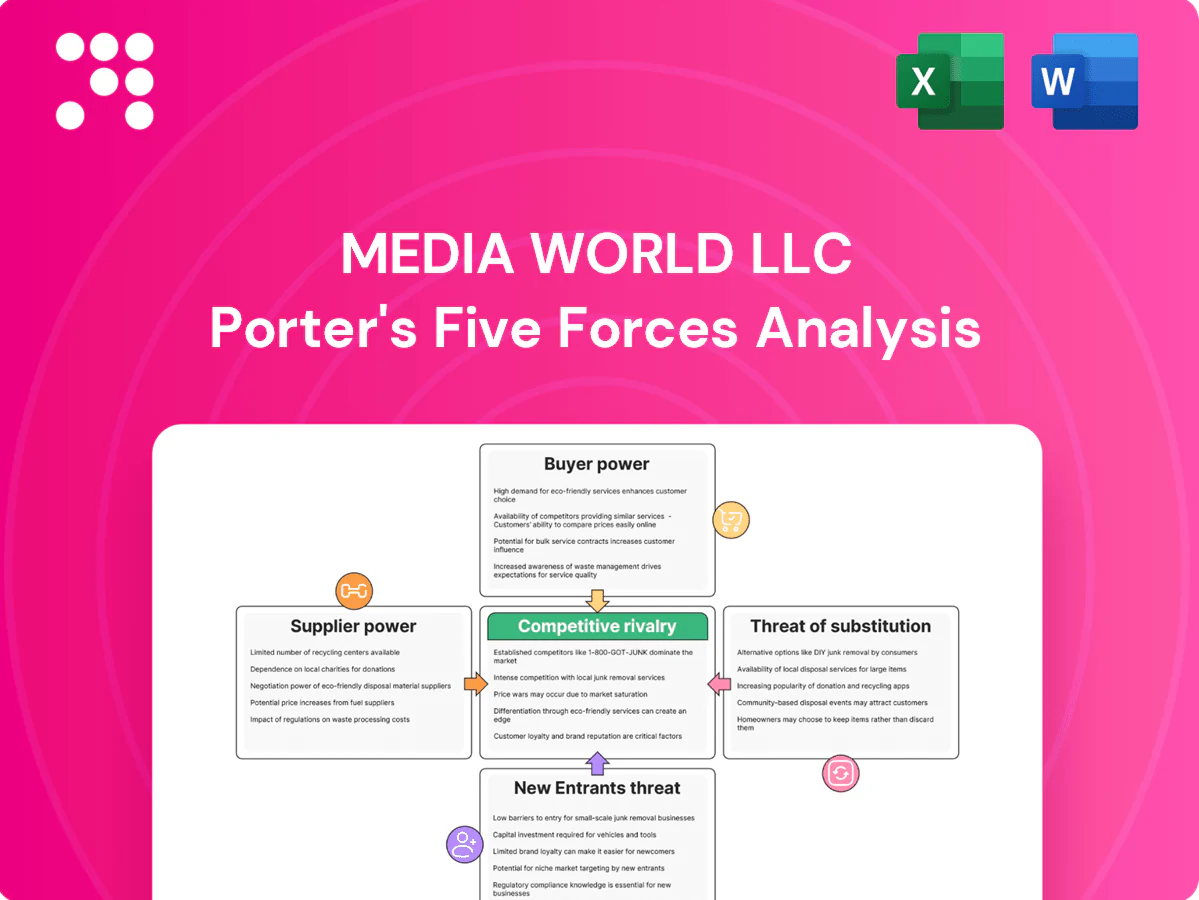

Media World LLC Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Media World LLC you will receive immediately after purchase—fully formatted, fully sourced, and ready to use. It is the complete professional document, not a sample or mockup, and contains the same insights, data points, and strategic implications as the downloadable file. No placeholders or additional setup required; buy and access this identical file instantly.

Don't Miss the Bigger Picture

Media World LLC's Porter's Five Forces snapshot highlights high competitive rivalry, moderate buyer power, supplier leverage from key content providers, rising substitute threats from streaming platforms, and barriers that limit new entrants. This concise view identifies strategic pressure points and opportunity areas. The complete report reveals force-by-force ratings, visuals, and actionable implications. Unlock the full Porter's Five Forces Analysis to guide smart investment and strategy decisions.

Suppliers Bargaining Power

Concentrated site rights

Prime arterial sites in the UAE are controlled by municipalities, the RTA and a handful of landlords, concentrating supply and raising supplier leverage over fees and terms. Limited concession windows and exclusivities force higher upfront and ongoing charges, squeezing operator margins. Renewal risk often triggers steep rent escalations tied to market resets. Diversifying across the seven Emirates reduces exposure to any single authority.

Permit and compliance dependence

Regulatory approvals, safety codes and content rules are critical inputs that suppliers of permits can use to delay or constrain inventory, cutting Media World LLCs flexibility and bargaining power; EU GDPR-related fines topped about €1.6 billion in 2023 and regulatory enforcement persisted into 2024, raising compliance stakes. Non-compliance penalties materially raise effective costs and switching is often infeasible, though a strong compliance record can modestly soften authorities stance.

Hardware and tech vendors

Hardware and tech vendors—LED screen makers, structure fabricators and CMS providers—retain leverage in a quality-driven DOOH market where the top 5 LED manufacturers capture over 60% of global display revenues; 2024 industry reports show panel lead times of roughly 12–20 weeks and import/tariff-driven cost uplifts commonly cited near 8–12%, while multi-vendor frameworks and standards-based CMS reduce vendor lock-in.

Maintenance and ops services

Maintenance and ops services—cranes, cleaning, electrical, monitoring—are essential to uptime SLAs; skilled high-mast technicians are scarce and certified electrician median pay was about $62,000 in 2024, increasing supplier leverage and rates. Downtime penalties drive operators to accept costly terms; building in-house teams or locking multi-year contracts can shift bargaining power back.

- Essential services: cranes, cleaning, electrical, monitoring

- Labor scarcity: certified technicians scarce; electrician median pay ~62,000 (2024)

- Downtime risk: penalties push acceptance of supplier terms

- Mitigants: in-house capability or long-term contracts

Utility and data inputs

Utility and data input suppliers meaningfully affect Media World LLC: US commercial electricity averaged about $0.13/kWh in 2024, raising site operating costs while incumbent utility monopolies in many regions limit negotiation latitude; data connectivity and CDN fees vary with 5G and fiber penetration, and audience analytics vendors owning unique mobility datasets commanded premium pricing in 2024, often 15–25% above commodity rates, while bundled contracts lowered per-site costs.

- Electricity: US commercial ≈ $0.13/kWh (2024)

- Vendor power: utility monopolies reduce leverage

- Analytics: mobility datasets +15–25% premium (2024)

- Bundling: lowers per-site unit cost

Supplier leverage: top-5 LEDs > 60%, 12-20 wk lead, electricity ~$0.13/kWh

Suppliers exert high leverage via concentrated prime-site landlords, regulatory permit authorities and dominant LED/analytics vendors, compressing margins and raising switching costs. Critical inputs (LEDs, technicians, utilities, data) showed 2024 pressures: top-5 LED makers >60% share, panel lead times 12–20 weeks, electrician median pay ~$62,000, US commercial electricity ~$0.13/kWh. Long-term contracts, vertical ops and geographic diversification are key mitigants.

| Input | 2024 metric | Impact |

|---|---|---|

| Landlords/permits | High concentration | Fee leverage, escalations |

| LED vendors | Top-5 >60% share; 12–20 wk lead | Price & supply risk |

| Technicians | Median pay ~$62,000 | Higher Opex |

| Electricity | US commercial ~$0.13/kWh | Site cost pressure |

| Analytics | Premium +15–25% | Higher data costs |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, barriers to entry, substitutes and disruptive threats specific to Media World LLC, with strategic commentary and editable Word-ready insights for investor decks and internal planning.

One-sheet Porter's Five Forces for Media World LLC that visualizes competitive pressure with an editable spider chart—customize inputs, swap labels, and copy straight into pitch decks or Excel dashboards for instant strategic clarity.

Customers Bargaining Power

Agency-led consolidation

Global and regional media agencies aggregate client spend—Magna forecasted global ad revenues near $850B in 2024—allowing them to negotiate volume discounts, makegoods and value-adds that compress vendor margins. Preferred partner lists and centralized buying can shave margins by several percentage points and limit pricing power. Media World tempers this by building direct-client relationships and bespoke offerings to reclaim margin and control of data.

Large-brand budget leverage

Telco, finance, government and FMCG advertisers in the UAE exert outsized control over OOH budgets, leveraging scale to demand rate concessions and secure premium sites across a market serving roughly 10 million residents (2024 est.).

Their briefs routinely require bespoke creative and data-backed reporting, driving suppliers to provide end-to-end turnkey solutions that bundle inventory, production and analytics.

Such integrated offerings raise switching costs and entrench incumbent media owners when large clients seek guaranteed reach and measurement consistency.

Performance and accountability

Buyers increasingly demand mobility-based reach, cross-device attribution, and dynamic content triggers, with 72% of advertisers in 2024 citing cross-channel attribution as a top buying requirement.

Lack of a standardized currency weakens pricing power unless Media World offers robust, transparent measurement; DOOH proof-of-play and third-party verification became baseline requirements in 2024 market RFPs.

Investing in analytics and verified attribution platforms reduces buyer pushback and can increase win rates and CPMs by double digits versus unverified inventory.

Substitution threats in negotiations

Clients shift to social, mobile, CTV and search when OOH pricing rises; digital took about 62% of global ad spend in 2024, strengthening buyer leverage. CTV ad spend grew roughly 21% YoY in 2024, making it a credible outside option. Bundled cross-format packages blunt substitution, while seasonal demand spikes still allow yield management on prime OOH sites.

- Buyers leverage: digital 62% share (2024)

- CTV growth ≈21% YoY (2024)

- Bundle mitigation vs seasonal yield on prime sites

Contract flexibility expectations

Buyers increasingly demand contract flexibility—shorter terms, option holds, and cancellation clauses—driven by event-driven budgets and economic cycles; in 2024 roughly 45% of media buyers cited agility and rate protections as top priorities, raising bargaining power versus platforms like Media World LLC.

- Shorter terms favored

- Option holds common

- Cancellation clauses demanded

- Tiered pricing + dynamic avail balance risk

Buyers Tighten Media Margins: Digital Share, CTV Growth and Measurement Demand Shift Power

Large advertisers and global agencies (Magna: global ad revenue ~$850B in 2024) secure discounts and flexible terms, compressing Media World margins. 62% digital share and 21% CTV growth in 2024 increase buyer substitution. Demand for verified measurement and shorter contracts raises buyer leverage; analytics investments restore pricing power.

| Metric | 2024 | Impact |

|---|---|---|

| Global ad revenue | $850B | Higher buyer clout |

| Digital share | 62% | Substitution risk |

| CTV YoY | 21% | Alternative channel |

| Buyers prioritizing agility | 45% | Shorter contracts |

| UAE population | ~10M | Concentrated OOH demand |

Preview the Actual Deliverable

Media World LLC Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Media World LLC you will receive immediately after purchase—fully formatted, fully sourced, and ready to use. It is the complete professional document, not a sample or mockup, and contains the same insights, data points, and strategic implications as the downloadable file. No placeholders or additional setup required; buy and access this identical file instantly.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Media World LLC's Porter's Five Forces snapshot highlights high competitive rivalry, moderate buyer power, supplier leverage from key content providers, rising substitute threats from streaming platforms, and barriers that limit new entrants. This concise view identifies strategic pressure points and opportunity areas. The complete report reveals force-by-force ratings, visuals, and actionable implications. Unlock the full Porter's Five Forces Analysis to guide smart investment and strategy decisions.

Suppliers Bargaining Power

Concentrated site rights

Prime arterial sites in the UAE are controlled by municipalities, the RTA and a handful of landlords, concentrating supply and raising supplier leverage over fees and terms. Limited concession windows and exclusivities force higher upfront and ongoing charges, squeezing operator margins. Renewal risk often triggers steep rent escalations tied to market resets. Diversifying across the seven Emirates reduces exposure to any single authority.

Permit and compliance dependence

Regulatory approvals, safety codes and content rules are critical inputs that suppliers of permits can use to delay or constrain inventory, cutting Media World LLCs flexibility and bargaining power; EU GDPR-related fines topped about €1.6 billion in 2023 and regulatory enforcement persisted into 2024, raising compliance stakes. Non-compliance penalties materially raise effective costs and switching is often infeasible, though a strong compliance record can modestly soften authorities stance.

Hardware and tech vendors

Hardware and tech vendors—LED screen makers, structure fabricators and CMS providers—retain leverage in a quality-driven DOOH market where the top 5 LED manufacturers capture over 60% of global display revenues; 2024 industry reports show panel lead times of roughly 12–20 weeks and import/tariff-driven cost uplifts commonly cited near 8–12%, while multi-vendor frameworks and standards-based CMS reduce vendor lock-in.

Maintenance and ops services

Maintenance and ops services—cranes, cleaning, electrical, monitoring—are essential to uptime SLAs; skilled high-mast technicians are scarce and certified electrician median pay was about $62,000 in 2024, increasing supplier leverage and rates. Downtime penalties drive operators to accept costly terms; building in-house teams or locking multi-year contracts can shift bargaining power back.

- Essential services: cranes, cleaning, electrical, monitoring

- Labor scarcity: certified technicians scarce; electrician median pay ~62,000 (2024)

- Downtime risk: penalties push acceptance of supplier terms

- Mitigants: in-house capability or long-term contracts

Utility and data inputs

Utility and data input suppliers meaningfully affect Media World LLC: US commercial electricity averaged about $0.13/kWh in 2024, raising site operating costs while incumbent utility monopolies in many regions limit negotiation latitude; data connectivity and CDN fees vary with 5G and fiber penetration, and audience analytics vendors owning unique mobility datasets commanded premium pricing in 2024, often 15–25% above commodity rates, while bundled contracts lowered per-site costs.

- Electricity: US commercial ≈ $0.13/kWh (2024)

- Vendor power: utility monopolies reduce leverage

- Analytics: mobility datasets +15–25% premium (2024)

- Bundling: lowers per-site unit cost

Supplier leverage: top-5 LEDs > 60%, 12-20 wk lead, electricity ~$0.13/kWh

Suppliers exert high leverage via concentrated prime-site landlords, regulatory permit authorities and dominant LED/analytics vendors, compressing margins and raising switching costs. Critical inputs (LEDs, technicians, utilities, data) showed 2024 pressures: top-5 LED makers >60% share, panel lead times 12–20 weeks, electrician median pay ~$62,000, US commercial electricity ~$0.13/kWh. Long-term contracts, vertical ops and geographic diversification are key mitigants.

| Input | 2024 metric | Impact |

|---|---|---|

| Landlords/permits | High concentration | Fee leverage, escalations |

| LED vendors | Top-5 >60% share; 12–20 wk lead | Price & supply risk |

| Technicians | Median pay ~$62,000 | Higher Opex |

| Electricity | US commercial ~$0.13/kWh | Site cost pressure |

| Analytics | Premium +15–25% | Higher data costs |

What is included in the product

Uncovers key drivers of competition, buyer and supplier power, barriers to entry, substitutes and disruptive threats specific to Media World LLC, with strategic commentary and editable Word-ready insights for investor decks and internal planning.

One-sheet Porter's Five Forces for Media World LLC that visualizes competitive pressure with an editable spider chart—customize inputs, swap labels, and copy straight into pitch decks or Excel dashboards for instant strategic clarity.

Customers Bargaining Power

Agency-led consolidation

Global and regional media agencies aggregate client spend—Magna forecasted global ad revenues near $850B in 2024—allowing them to negotiate volume discounts, makegoods and value-adds that compress vendor margins. Preferred partner lists and centralized buying can shave margins by several percentage points and limit pricing power. Media World tempers this by building direct-client relationships and bespoke offerings to reclaim margin and control of data.

Large-brand budget leverage

Telco, finance, government and FMCG advertisers in the UAE exert outsized control over OOH budgets, leveraging scale to demand rate concessions and secure premium sites across a market serving roughly 10 million residents (2024 est.).

Their briefs routinely require bespoke creative and data-backed reporting, driving suppliers to provide end-to-end turnkey solutions that bundle inventory, production and analytics.

Such integrated offerings raise switching costs and entrench incumbent media owners when large clients seek guaranteed reach and measurement consistency.

Performance and accountability

Buyers increasingly demand mobility-based reach, cross-device attribution, and dynamic content triggers, with 72% of advertisers in 2024 citing cross-channel attribution as a top buying requirement.

Lack of a standardized currency weakens pricing power unless Media World offers robust, transparent measurement; DOOH proof-of-play and third-party verification became baseline requirements in 2024 market RFPs.

Investing in analytics and verified attribution platforms reduces buyer pushback and can increase win rates and CPMs by double digits versus unverified inventory.

Substitution threats in negotiations

Clients shift to social, mobile, CTV and search when OOH pricing rises; digital took about 62% of global ad spend in 2024, strengthening buyer leverage. CTV ad spend grew roughly 21% YoY in 2024, making it a credible outside option. Bundled cross-format packages blunt substitution, while seasonal demand spikes still allow yield management on prime OOH sites.

- Buyers leverage: digital 62% share (2024)

- CTV growth ≈21% YoY (2024)

- Bundle mitigation vs seasonal yield on prime sites

Contract flexibility expectations

Buyers increasingly demand contract flexibility—shorter terms, option holds, and cancellation clauses—driven by event-driven budgets and economic cycles; in 2024 roughly 45% of media buyers cited agility and rate protections as top priorities, raising bargaining power versus platforms like Media World LLC.

- Shorter terms favored

- Option holds common

- Cancellation clauses demanded

- Tiered pricing + dynamic avail balance risk

Buyers Tighten Media Margins: Digital Share, CTV Growth and Measurement Demand Shift Power

Large advertisers and global agencies (Magna: global ad revenue ~$850B in 2024) secure discounts and flexible terms, compressing Media World margins. 62% digital share and 21% CTV growth in 2024 increase buyer substitution. Demand for verified measurement and shorter contracts raises buyer leverage; analytics investments restore pricing power.

| Metric | 2024 | Impact |

|---|---|---|

| Global ad revenue | $850B | Higher buyer clout |

| Digital share | 62% | Substitution risk |

| CTV YoY | 21% | Alternative channel |

| Buyers prioritizing agility | 45% | Shorter contracts |

| UAE population | ~10M | Concentrated OOH demand |

Preview the Actual Deliverable

Media World LLC Porter's Five Forces Analysis

This preview shows the exact Porter's Five Forces analysis of Media World LLC you will receive immediately after purchase—fully formatted, fully sourced, and ready to use. It is the complete professional document, not a sample or mockup, and contains the same insights, data points, and strategic implications as the downloadable file. No placeholders or additional setup required; buy and access this identical file instantly.