Medica Group PESTLE Analysis

Plan Smarter. Present Sharper. Compete Stronger.

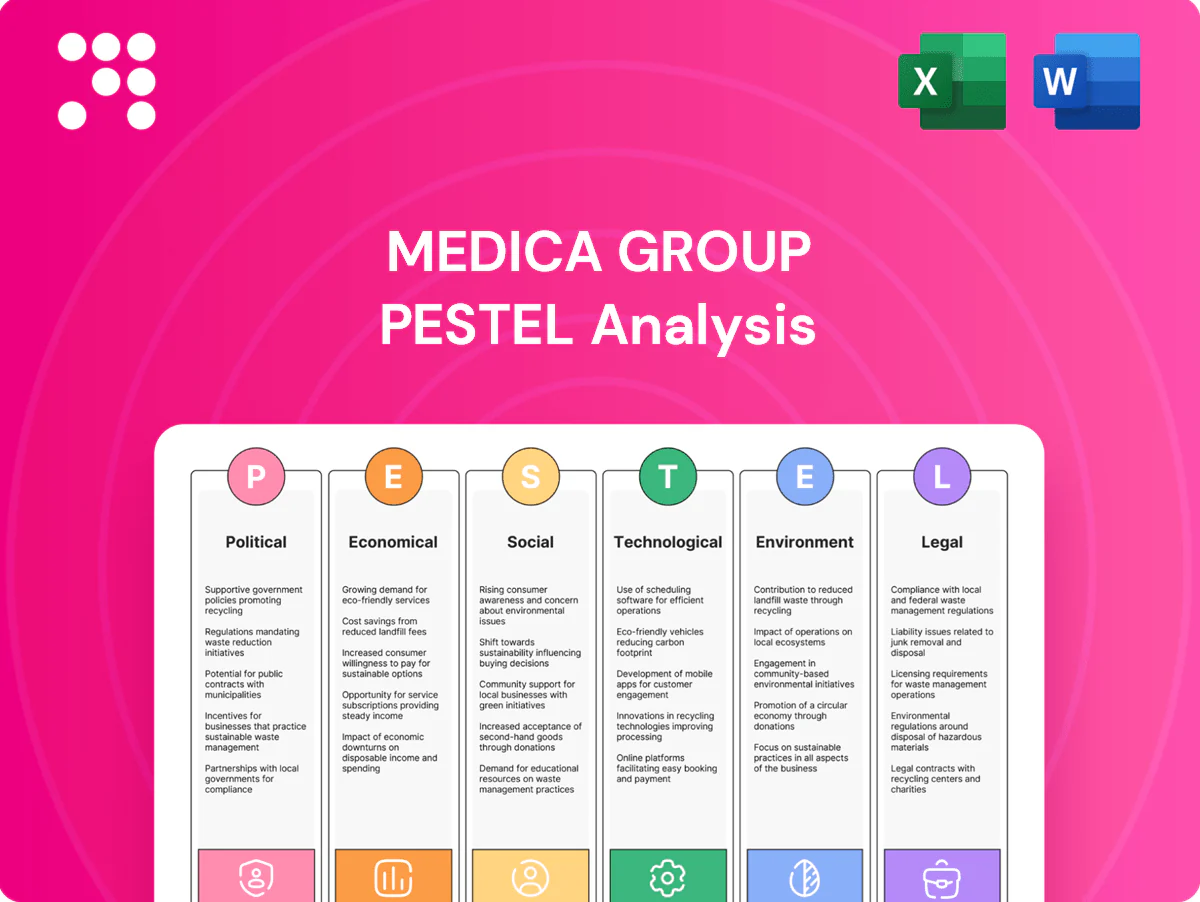

Unlock strategic clarity with our concise PESTLE Analysis of Medica Group—three to five key external forces explained and tied to actionable risks and opportunities. Ideal for investors and strategists who need fast, reliable insight. Purchase the full report for the complete deep-dive and ready-to-use recommendations.

Political factors

NHS policy shifts

NHS policy and commissioning priorities drive demand for outsourced teleradiology as trusts face a national elective care backlog of over 7 million patients and a stated NHS England target to eliminate 6‑week diagnostic waits by March 2025, accelerating procurement of external imaging capacity. Ongoing shifts to Integrated Care Systems (established 2022) are changing contracting routes, while political turnover risks resetting funding emphasis and timelines.

Public healthcare funding

Public healthcare budget allocations—for example the NHS diagnostics capital programme (roughly £2.3bn committed to scanners and diagnostics upgrades)—directly shape throughput and outsourcing appetite, with austerity cuts or spending boosts driving visible volume swings. Capital provision for scanners without parallel investment in reporting capacity increases reliance on outsourced providers like Medica, while EU Cross-border Healthcare Directive adds policy complexity for cross-border operations.

Trade and workforce mobility

Immigration rules materially affect Medica Group’s access to radiologists and clinicians, with 28% of UK doctors trained abroad (GMC 2023) illustrating reliance on international hires. Recognition of foreign qualifications constrains supply flexibility, while the global teleradiology market was valued at about USD 2.1bn in 2023, underscoring need for stable trade and telehealth agreements; political friction can delay credentialing and cross-border data flows.

Geopolitical stability

Geopolitical instability threatens Medica Group’s night-hawk and cross–time-zone coverage through supply-chain interruptions and staff redeployments; SIPRI reported global military spending at 2.3 trillion USD in 2023, reflecting heightened tensions. Currency moves after sanctions (eg, measures since 2022 on Russia) can shift operating costs and pricing for international contracts. Governments boosting health resilience post‑pandemic may favor contracted surge capacity, while sanctions and export controls can restrict vendor partnerships.

- Operational risk: interrupted 24/7 coverage

- Financial risk: FX exposure on international contracts

- Policy tailwind: increased government demand for outsourced capacity

- Compliance risk: sanctions limiting suppliers

Digital health strategies

National telemedicine roadmaps, guided by WHO Global Strategy on Digital Health 2020–2025, set standards for remote diagnostics and clinical workflows; in the US the 21st Century Cures Act enforces API-based interoperability that aids EHR integration with hospital systems. Political backing for AI in healthcare (Horizon Europe budget €95.5 billion for 2021–2027 includes health/AI research funding) can unlock grants, while regulatory skepticism slows pilot approvals and scaling.

- Roadmaps: WHO Global Strategy on Digital Health 2020–2025

- Interoperability: US 21st Century Cures Act (API mandate)

- Funding: Horizon Europe €95.5B (2021–2027) supporting health/AI research

- Risk: regulatory skepticism delays pilots/scaling

NHS over 7m elective backlog and £2.3bn diagnostics push outsourced teleradiology growth

NHS policy and funding (NHS diagnostics capital ~£2.3bn) plus an elective backlog >7m drive outsourced teleradiology demand. Integrated Care Systems reshape contracting and political turnover can redirect funding. Reliance on international clinicians (28% of UK doctors, GMC 2023) and cross‑border rules affect staffing and data flows.

| Indicator | Value | Impact |

|---|---|---|

| Elective backlog | >7m | ↑outsourcing |

| Diagnostics capital | £2.3bn | ↑scanner capacity |

| Intl clinicians | 28% (GMC 2023) | Staffing reliance |

| Teleradiology market | USD 2.1bn (2023) | Market scale |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Medica Group, with each section backed by current data and trends to reflect regional market and regulatory realities; provides forward-looking insights and ready-to-use findings to help executives, consultants and investors identify risks and opportunities.

A concise, visually segmented PESTLE summary of Medica Group that distills external risks and opportunities for quick reference in meetings or slides, editable for region- or business-line notes and easily shareable across teams to align strategy and support risk discussions.

Economic factors

Healthcare cost pressures

Hospital budget constraints drive more outsourcing to variable-cost providers as US health spending reached 17.8% of GDP in 2022 (CMS); labor makes up about 60% of hospital operating expenses, so wage inflation and rising energy prices sharply raise costs. Medica can leverage cost-effective per-report pricing to win volume; sustainability hinges on reimbursement levels, which determine whether thin hospital margins cover outsourced spend.

Macroeconomic cycles

Macroeconomic cycles compress capital spending—IMF estimated 2024 global GDP growth at about 3.1%, so downturns may delay Medica Group IT and site projects while urgent imaging demand for acute care holds. Elective procedure volumes (England waiting list ~7.6m in 2024) drive routine reporting swings. Currency moves affect translated international revenue, and prevailing interest rates near 4–5% in 2024 raise financing costs for IT infrastructure.

Labor market dynamics

US physician shortfall projected by AAMC at up to 139,000 by 2033 drives radiologist demand and fuels teleradiology growth (global market exceeded ~$6B in 2023). Wage competition risks compressing Medica Group margins if pricing lags; offering flexible remote roles widens recruitment across regions, while productivity and AI-enabled workflow tools are essential to offset clinician scarcity and maintain throughput.

Payor mix and tariffs

Payor mix and tariffs drive per-case revenue: public payors account for about 80% of UK health spending (ONS), so changes in NHS tariffs or private insurer rates materially affect income. Case-mix shifts toward urgent care reduce margins as urgent episodes cost more and attract different tariff profiles. Value-based contracts increasingly reward turnaround and quality KPIs; annual NHS national tariff guidance (most recent 2024/25) and contract renegotiations can reset pricing power.

- Tariff exposure: public payor ~80%

- Case-mix risk: urgent vs routine affects margin

- VBC focus: payments tied to turnaround, readmissions, PROMs

- Renegotiation: contracts can reset pricing power

Scale and operating leverage

Higher report volumes spread fixed platform costs across more units, improving margin per report while off-peak international routing increases asset utilization and reduces per-test turnaround time. Economies of scale in credentialing and QA lower unit costs through centralized processes, but scaling demands sustained IT and cybersecurity investment to protect patient data and maintain platform uptime.

- Scale: spreads fixed costs, boosts margins

- Routing: off-peak improves utilization

- QA/Credentialing: lowers unit costs

- Risk: ongoing IT/cybersecurity spend

NHS over 7m elective backlog and £2.3bn diagnostics push outsourced teleradiology growth

Hospital wage and energy inflation plus 17.8% US health spend (CMS 2022) squeeze margins; per-report pricing and scale are critical. IMF 2024 GDP ~3.1% and 2024 interest rates ~4–5% raise financing costs and capex timing. AAMC physician shortfall to 2033 boosts teleradiology demand but intensifies wage pressure on margins.

| Metric | Value (source/year) |

|---|---|

| US health spend | 17.8% (CMS 2022) |

| Global GDP | 3.1% (IMF 2024) |

| Interest rates | ≈4–5% (2024) |

| Public payor UK | ~80% (ONS 2024) |

Same Document Delivered

Medica Group PESTLE Analysis

The preview shown here is the exact Medica Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the same content, structure, and professional layout visible now, with no placeholders or edits pending. Download the final file instantly after checkout.

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our concise PESTLE Analysis of Medica Group—three to five key external forces explained and tied to actionable risks and opportunities. Ideal for investors and strategists who need fast, reliable insight. Purchase the full report for the complete deep-dive and ready-to-use recommendations.

Political factors

NHS policy shifts

NHS policy and commissioning priorities drive demand for outsourced teleradiology as trusts face a national elective care backlog of over 7 million patients and a stated NHS England target to eliminate 6‑week diagnostic waits by March 2025, accelerating procurement of external imaging capacity. Ongoing shifts to Integrated Care Systems (established 2022) are changing contracting routes, while political turnover risks resetting funding emphasis and timelines.

Public healthcare funding

Public healthcare budget allocations—for example the NHS diagnostics capital programme (roughly £2.3bn committed to scanners and diagnostics upgrades)—directly shape throughput and outsourcing appetite, with austerity cuts or spending boosts driving visible volume swings. Capital provision for scanners without parallel investment in reporting capacity increases reliance on outsourced providers like Medica, while EU Cross-border Healthcare Directive adds policy complexity for cross-border operations.

Trade and workforce mobility

Immigration rules materially affect Medica Group’s access to radiologists and clinicians, with 28% of UK doctors trained abroad (GMC 2023) illustrating reliance on international hires. Recognition of foreign qualifications constrains supply flexibility, while the global teleradiology market was valued at about USD 2.1bn in 2023, underscoring need for stable trade and telehealth agreements; political friction can delay credentialing and cross-border data flows.

Geopolitical stability

Geopolitical instability threatens Medica Group’s night-hawk and cross–time-zone coverage through supply-chain interruptions and staff redeployments; SIPRI reported global military spending at 2.3 trillion USD in 2023, reflecting heightened tensions. Currency moves after sanctions (eg, measures since 2022 on Russia) can shift operating costs and pricing for international contracts. Governments boosting health resilience post‑pandemic may favor contracted surge capacity, while sanctions and export controls can restrict vendor partnerships.

- Operational risk: interrupted 24/7 coverage

- Financial risk: FX exposure on international contracts

- Policy tailwind: increased government demand for outsourced capacity

- Compliance risk: sanctions limiting suppliers

Digital health strategies

National telemedicine roadmaps, guided by WHO Global Strategy on Digital Health 2020–2025, set standards for remote diagnostics and clinical workflows; in the US the 21st Century Cures Act enforces API-based interoperability that aids EHR integration with hospital systems. Political backing for AI in healthcare (Horizon Europe budget €95.5 billion for 2021–2027 includes health/AI research funding) can unlock grants, while regulatory skepticism slows pilot approvals and scaling.

- Roadmaps: WHO Global Strategy on Digital Health 2020–2025

- Interoperability: US 21st Century Cures Act (API mandate)

- Funding: Horizon Europe €95.5B (2021–2027) supporting health/AI research

- Risk: regulatory skepticism delays pilots/scaling

NHS over 7m elective backlog and £2.3bn diagnostics push outsourced teleradiology growth

NHS policy and funding (NHS diagnostics capital ~£2.3bn) plus an elective backlog >7m drive outsourced teleradiology demand. Integrated Care Systems reshape contracting and political turnover can redirect funding. Reliance on international clinicians (28% of UK doctors, GMC 2023) and cross‑border rules affect staffing and data flows.

| Indicator | Value | Impact |

|---|---|---|

| Elective backlog | >7m | ↑outsourcing |

| Diagnostics capital | £2.3bn | ↑scanner capacity |

| Intl clinicians | 28% (GMC 2023) | Staffing reliance |

| Teleradiology market | USD 2.1bn (2023) | Market scale |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Medica Group, with each section backed by current data and trends to reflect regional market and regulatory realities; provides forward-looking insights and ready-to-use findings to help executives, consultants and investors identify risks and opportunities.

A concise, visually segmented PESTLE summary of Medica Group that distills external risks and opportunities for quick reference in meetings or slides, editable for region- or business-line notes and easily shareable across teams to align strategy and support risk discussions.

Economic factors

Healthcare cost pressures

Hospital budget constraints drive more outsourcing to variable-cost providers as US health spending reached 17.8% of GDP in 2022 (CMS); labor makes up about 60% of hospital operating expenses, so wage inflation and rising energy prices sharply raise costs. Medica can leverage cost-effective per-report pricing to win volume; sustainability hinges on reimbursement levels, which determine whether thin hospital margins cover outsourced spend.

Macroeconomic cycles

Macroeconomic cycles compress capital spending—IMF estimated 2024 global GDP growth at about 3.1%, so downturns may delay Medica Group IT and site projects while urgent imaging demand for acute care holds. Elective procedure volumes (England waiting list ~7.6m in 2024) drive routine reporting swings. Currency moves affect translated international revenue, and prevailing interest rates near 4–5% in 2024 raise financing costs for IT infrastructure.

Labor market dynamics

US physician shortfall projected by AAMC at up to 139,000 by 2033 drives radiologist demand and fuels teleradiology growth (global market exceeded ~$6B in 2023). Wage competition risks compressing Medica Group margins if pricing lags; offering flexible remote roles widens recruitment across regions, while productivity and AI-enabled workflow tools are essential to offset clinician scarcity and maintain throughput.

Payor mix and tariffs

Payor mix and tariffs drive per-case revenue: public payors account for about 80% of UK health spending (ONS), so changes in NHS tariffs or private insurer rates materially affect income. Case-mix shifts toward urgent care reduce margins as urgent episodes cost more and attract different tariff profiles. Value-based contracts increasingly reward turnaround and quality KPIs; annual NHS national tariff guidance (most recent 2024/25) and contract renegotiations can reset pricing power.

- Tariff exposure: public payor ~80%

- Case-mix risk: urgent vs routine affects margin

- VBC focus: payments tied to turnaround, readmissions, PROMs

- Renegotiation: contracts can reset pricing power

Scale and operating leverage

Higher report volumes spread fixed platform costs across more units, improving margin per report while off-peak international routing increases asset utilization and reduces per-test turnaround time. Economies of scale in credentialing and QA lower unit costs through centralized processes, but scaling demands sustained IT and cybersecurity investment to protect patient data and maintain platform uptime.

- Scale: spreads fixed costs, boosts margins

- Routing: off-peak improves utilization

- QA/Credentialing: lowers unit costs

- Risk: ongoing IT/cybersecurity spend

NHS over 7m elective backlog and £2.3bn diagnostics push outsourced teleradiology growth

Hospital wage and energy inflation plus 17.8% US health spend (CMS 2022) squeeze margins; per-report pricing and scale are critical. IMF 2024 GDP ~3.1% and 2024 interest rates ~4–5% raise financing costs and capex timing. AAMC physician shortfall to 2033 boosts teleradiology demand but intensifies wage pressure on margins.

| Metric | Value (source/year) |

|---|---|

| US health spend | 17.8% (CMS 2022) |

| Global GDP | 3.1% (IMF 2024) |

| Interest rates | ≈4–5% (2024) |

| Public payor UK | ~80% (ONS 2024) |

Same Document Delivered

Medica Group PESTLE Analysis

The preview shown here is the exact Medica Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the same content, structure, and professional layout visible now, with no placeholders or edits pending. Download the final file instantly after checkout.

Original: $10.00

-65%$10.00

$3.50Description

Plan Smarter. Present Sharper. Compete Stronger.

Unlock strategic clarity with our concise PESTLE Analysis of Medica Group—three to five key external forces explained and tied to actionable risks and opportunities. Ideal for investors and strategists who need fast, reliable insight. Purchase the full report for the complete deep-dive and ready-to-use recommendations.

Political factors

NHS policy shifts

NHS policy and commissioning priorities drive demand for outsourced teleradiology as trusts face a national elective care backlog of over 7 million patients and a stated NHS England target to eliminate 6‑week diagnostic waits by March 2025, accelerating procurement of external imaging capacity. Ongoing shifts to Integrated Care Systems (established 2022) are changing contracting routes, while political turnover risks resetting funding emphasis and timelines.

Public healthcare funding

Public healthcare budget allocations—for example the NHS diagnostics capital programme (roughly £2.3bn committed to scanners and diagnostics upgrades)—directly shape throughput and outsourcing appetite, with austerity cuts or spending boosts driving visible volume swings. Capital provision for scanners without parallel investment in reporting capacity increases reliance on outsourced providers like Medica, while EU Cross-border Healthcare Directive adds policy complexity for cross-border operations.

Trade and workforce mobility

Immigration rules materially affect Medica Group’s access to radiologists and clinicians, with 28% of UK doctors trained abroad (GMC 2023) illustrating reliance on international hires. Recognition of foreign qualifications constrains supply flexibility, while the global teleradiology market was valued at about USD 2.1bn in 2023, underscoring need for stable trade and telehealth agreements; political friction can delay credentialing and cross-border data flows.

Geopolitical stability

Geopolitical instability threatens Medica Group’s night-hawk and cross–time-zone coverage through supply-chain interruptions and staff redeployments; SIPRI reported global military spending at 2.3 trillion USD in 2023, reflecting heightened tensions. Currency moves after sanctions (eg, measures since 2022 on Russia) can shift operating costs and pricing for international contracts. Governments boosting health resilience post‑pandemic may favor contracted surge capacity, while sanctions and export controls can restrict vendor partnerships.

- Operational risk: interrupted 24/7 coverage

- Financial risk: FX exposure on international contracts

- Policy tailwind: increased government demand for outsourced capacity

- Compliance risk: sanctions limiting suppliers

Digital health strategies

National telemedicine roadmaps, guided by WHO Global Strategy on Digital Health 2020–2025, set standards for remote diagnostics and clinical workflows; in the US the 21st Century Cures Act enforces API-based interoperability that aids EHR integration with hospital systems. Political backing for AI in healthcare (Horizon Europe budget €95.5 billion for 2021–2027 includes health/AI research funding) can unlock grants, while regulatory skepticism slows pilot approvals and scaling.

- Roadmaps: WHO Global Strategy on Digital Health 2020–2025

- Interoperability: US 21st Century Cures Act (API mandate)

- Funding: Horizon Europe €95.5B (2021–2027) supporting health/AI research

- Risk: regulatory skepticism delays pilots/scaling

NHS over 7m elective backlog and £2.3bn diagnostics push outsourced teleradiology growth

NHS policy and funding (NHS diagnostics capital ~£2.3bn) plus an elective backlog >7m drive outsourced teleradiology demand. Integrated Care Systems reshape contracting and political turnover can redirect funding. Reliance on international clinicians (28% of UK doctors, GMC 2023) and cross‑border rules affect staffing and data flows.

| Indicator | Value | Impact |

|---|---|---|

| Elective backlog | >7m | ↑outsourcing |

| Diagnostics capital | £2.3bn | ↑scanner capacity |

| Intl clinicians | 28% (GMC 2023) | Staffing reliance |

| Teleradiology market | USD 2.1bn (2023) | Market scale |

What is included in the product

Explores how Political, Economic, Social, Technological, Environmental and Legal forces uniquely affect Medica Group, with each section backed by current data and trends to reflect regional market and regulatory realities; provides forward-looking insights and ready-to-use findings to help executives, consultants and investors identify risks and opportunities.

A concise, visually segmented PESTLE summary of Medica Group that distills external risks and opportunities for quick reference in meetings or slides, editable for region- or business-line notes and easily shareable across teams to align strategy and support risk discussions.

Economic factors

Healthcare cost pressures

Hospital budget constraints drive more outsourcing to variable-cost providers as US health spending reached 17.8% of GDP in 2022 (CMS); labor makes up about 60% of hospital operating expenses, so wage inflation and rising energy prices sharply raise costs. Medica can leverage cost-effective per-report pricing to win volume; sustainability hinges on reimbursement levels, which determine whether thin hospital margins cover outsourced spend.

Macroeconomic cycles

Macroeconomic cycles compress capital spending—IMF estimated 2024 global GDP growth at about 3.1%, so downturns may delay Medica Group IT and site projects while urgent imaging demand for acute care holds. Elective procedure volumes (England waiting list ~7.6m in 2024) drive routine reporting swings. Currency moves affect translated international revenue, and prevailing interest rates near 4–5% in 2024 raise financing costs for IT infrastructure.

Labor market dynamics

US physician shortfall projected by AAMC at up to 139,000 by 2033 drives radiologist demand and fuels teleradiology growth (global market exceeded ~$6B in 2023). Wage competition risks compressing Medica Group margins if pricing lags; offering flexible remote roles widens recruitment across regions, while productivity and AI-enabled workflow tools are essential to offset clinician scarcity and maintain throughput.

Payor mix and tariffs

Payor mix and tariffs drive per-case revenue: public payors account for about 80% of UK health spending (ONS), so changes in NHS tariffs or private insurer rates materially affect income. Case-mix shifts toward urgent care reduce margins as urgent episodes cost more and attract different tariff profiles. Value-based contracts increasingly reward turnaround and quality KPIs; annual NHS national tariff guidance (most recent 2024/25) and contract renegotiations can reset pricing power.

- Tariff exposure: public payor ~80%

- Case-mix risk: urgent vs routine affects margin

- VBC focus: payments tied to turnaround, readmissions, PROMs

- Renegotiation: contracts can reset pricing power

Scale and operating leverage

Higher report volumes spread fixed platform costs across more units, improving margin per report while off-peak international routing increases asset utilization and reduces per-test turnaround time. Economies of scale in credentialing and QA lower unit costs through centralized processes, but scaling demands sustained IT and cybersecurity investment to protect patient data and maintain platform uptime.

- Scale: spreads fixed costs, boosts margins

- Routing: off-peak improves utilization

- QA/Credentialing: lowers unit costs

- Risk: ongoing IT/cybersecurity spend

NHS over 7m elective backlog and £2.3bn diagnostics push outsourced teleradiology growth

Hospital wage and energy inflation plus 17.8% US health spend (CMS 2022) squeeze margins; per-report pricing and scale are critical. IMF 2024 GDP ~3.1% and 2024 interest rates ~4–5% raise financing costs and capex timing. AAMC physician shortfall to 2033 boosts teleradiology demand but intensifies wage pressure on margins.

| Metric | Value (source/year) |

|---|---|

| US health spend | 17.8% (CMS 2022) |

| Global GDP | 3.1% (IMF 2024) |

| Interest rates | ≈4–5% (2024) |

| Public payor UK | ~80% (ONS 2024) |

Same Document Delivered

Medica Group PESTLE Analysis

The preview shown here is the exact Medica Group PESTLE Analysis you’ll receive after purchase—fully formatted and ready to use. It contains the same content, structure, and professional layout visible now, with no placeholders or edits pending. Download the final file instantly after checkout.