Medifast SWOT Analysis

Elevate Your Analysis with the Complete SWOT Report

Medifast's SWOT highlights a strong brand in medically oriented weight-loss, scalable DTC and subscription revenue, and margin leverage from product portfolios—tempered by regulatory scrutiny, intense competition, and supply-chain exposure; growth hinges on digital coaching and international expansion. Discover the full SWOT analysis—purchase the complete, editable report for investor-ready insights and strategic tools.

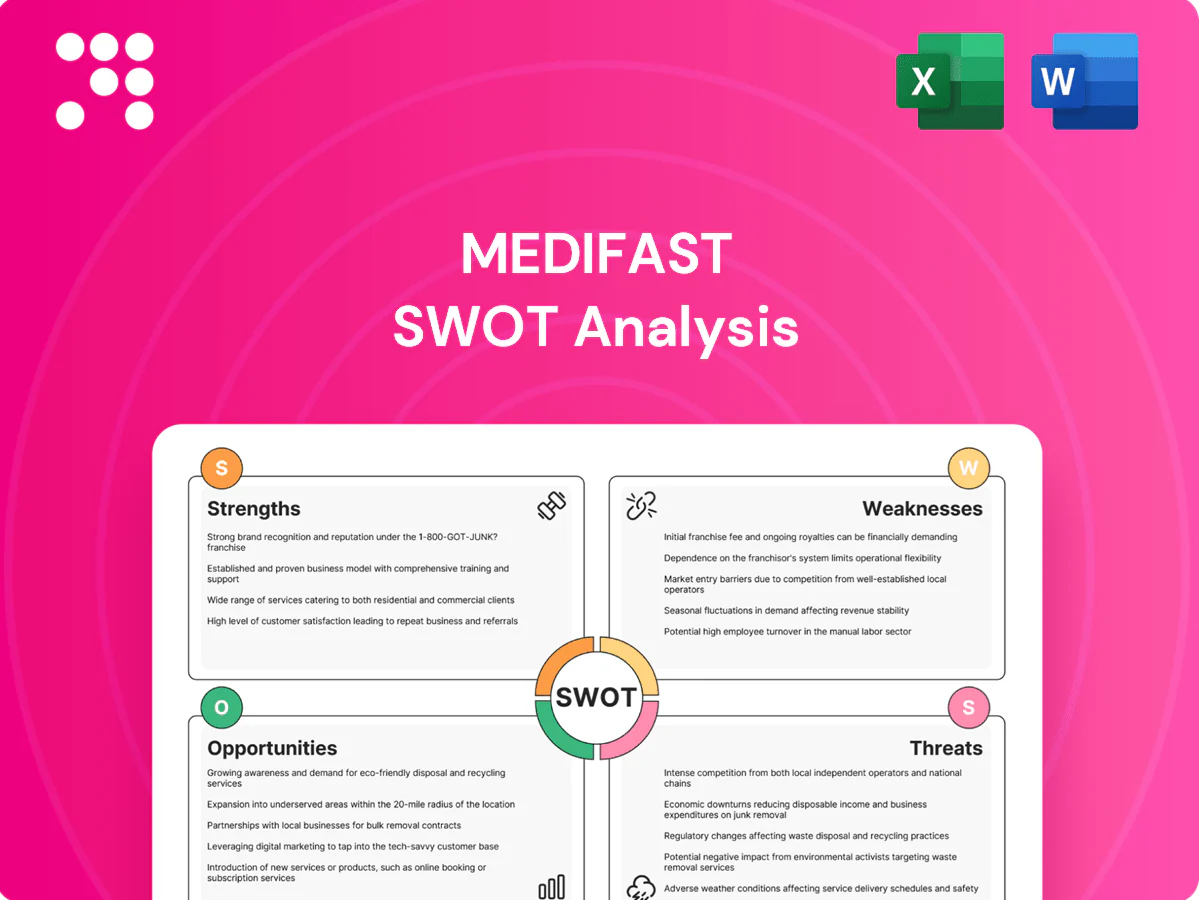

Strengths

Scalable coach-driven direct-selling model

An independent coach network enables rapid, low-capex customer acquisition and personalized guidance at scale; Medifast’s coach-driven Optavia channel—supporting roughly 40,000+ coaches in recent filings—fuels word-of-mouth momentum and peer accountability. The model flexes with demand without fixed retail overhead and boosts lifetime value via recurring orders and upsell, supporting Medifast’s ~$1.06B revenue scale in 2024.

Proprietary OPTAVIA product portfolio

Owned OPTAVIA formulations and portion-controlled meals deliver consistent convenience, underpinning program adherence and supporting Medifast’s scale (net sales $1.07B in FY2023). Exclusive SKUs and brand equity reduce price comparability and limit commoditization. The bundled product ecosystem raises switching costs for clients, helping protect margins and recurring revenue.

Integrated program, education, and community

Combining meal plans with habit-building content drives behavioral change beyond calorie restriction, with behavioral interventions showing ~5–10% greater sustained weight loss at 12 months versus diet-only approaches. Community support improves adherence and outcomes—meta-analyses report roughly a 20–30% boost in adherence with social/coach support. Holistic positioning appeals to long-term wellness seekers and strengthens coach credibility and testimonial validity.

Attractive unit economics and margins

Medifasts direct-to-consumer fulfillment and owned-brand portfolio sustain industry-leading gross margins by capturing retail markup and minimizing third-party fees, while recurring auto-ship and program continuity enhance revenue visibility and lifetime customer value. A variable commission structure ties selling costs to sales flow, preserving margin as volume scales, enabling cash-generative operations during growth periods.

- Direct-to-consumer fulfillment

- Owned brands capture higher margins

- Recurring auto-ship improves visibility

- Variable commissions align costs

- Cash-generative in growth

Brand recognition in weight management

OPTAVIA is widely recognized in structured weight-loss programs and drives the bulk of Medifast revenue, accounting for roughly 80–90% of FY2023 company sales (FY2023 revenue approximately $1.35B). High-profile success stories and documented client transformations amplify social proof, improving coach recruitment and client conversion rates. The narrow focus on weight management sharpens OPTAVIAs value proposition versus general nutrition brands, aiding market differentiation.

- Brand: OPTAVIA dominant revenue driver (~80–90% of ~$1.35B FY2023)

- Social proof: documented success stories boost conversions

- Recruiting: strong brand recall eases coach acquisition

- Positioning: niche clarity vs broad nutrition competitors

Coach-led channel (≈40k) drives recurring auto-ship revenue, FY2024 $1.06B

Medifast’s coach-driven OPTAVIA channel (≈40,000+ coaches) enables low-capex customer acquisition, recurring auto-ship revenue and high lifetime value; OPTAVIA drove ~80–90% of company sales. Own-brand, portion-controlled products support adherence and recurring orders, sustaining scale (FY2024 revenue ≈$1.06B). Direct DTC fulfillment and variable commissions preserve margin and cash generation as volume grows.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.06B |

| OPTAVIA share | ~80–90% |

| Coach network | ≈40,000+ |

What is included in the product

Provides a concise SWOT analysis of Medifast, highlighting internal strengths like brand recognition and product portfolio, weaknesses such as customer concentration and margin pressure, opportunities in digital channels and international expansion, and threats from competitive intensity, regulatory changes, and consumer trends.

Provides a focused Medifast SWOT matrix that clarifies competitive strengths, market risks, and growth opportunities for rapid strategic action; editable format lets teams update factors as regulatory, supply-chain, or consumer trends shift.

Weaknesses

Dependence on independent coaches

Sales velocity is tightly tied to recruiting, training and retaining independent coaches, making growth dependent on headcount expansion. Variability in coach quality can undermine client outcomes and brand consistency, increasing churn; direct-selling networks often see annual turnover exceeding 70%. High turnover creates growth volatility and meaningful onboarding costs, while concentration risk rises if top leader networks churn.

MLM perceptions and compliance complexity

Direct-selling models like Medifast's face skepticism and reputational headwinds that can suppress consumer trust and partner recruitment; Medifast reported roughly $1.13 billion in 2023 revenue, exposing that scale to reputation risk.

Strict income, earnings and health-claim compliance requires significant legal and monitoring spend and any missteps by independent coaches can trigger FTC or state inquiries.

Negative narratives around MLM-like structures have shown to impair recruitment and demand, increasing churn and marketing costs for the Optavia coach network.

Adherence and churn in weight loss

Weight-management customers often relapse—studies show roughly 80% regain lost weight within five years—dampening Medifast retention. Program rigidity and taste fatigue contribute to 30–60% first‑year attrition seen in many structured plans, reducing long‑term engagement. High churn raises acquisition costs and compresses LTV/CAC, while variable results weaken referrals and coach morale.

Product concentration in meal replacements

Medifast's heavy reliance on portion-controlled meal replacements limits product diversification and market flexibility; shifts toward whole-food diets or GLP-1 treatments risk reducing relevance. Limited adjacent services constrain cross-sell potential, while supply or formula disruptions could materially impact revenue—Medifast reported roughly $1.08B in net sales in FY2023.

- High product concentration: majority revenues from meal replacements

- Market shift risk: rising whole-food/pharma alternatives

- Weak cross-sell: few adjacent services

- Supply/formula risk: major revenue exposure

Limited geographic breadth

Operations remain North America–centric with selective international exposure, leaving regulatory and macro risk concentrated; over 90% of net sales derive from the U.S. and Canada as of 2024. Global brand recognition and localized product menus are underdeveloped, limiting cross-border customer acquisition. Scale advantages abroad remain largely untapped, constraining long-term growth diversification.

- Geographic concentration: >90% revenue North America (2024)

- Regulatory/macro risk concentration

- Weak global brand/localization

- Untapped scale abroad

Direct-selling diet firm: coach turnover > 70%, attrition 30-60%

Medifast's growth is highly dependent on recruiting and retaining independent Optavia coaches, with direct-selling turnover often >70% and first‑year program attrition 30–60%, raising CAC and onboarding costs. Heavy product concentration (meal replacements ~majority of $1.13B 2023 revenue) and >90% North America revenue (2024) heighten market and supply risks, while relapse rates (~80% regain within 5 years) depress LTV.

| Metric | Value |

|---|---|

| FY2023 Revenue | $1.13B |

| North America Share (2024) | >90% |

| Coach turnover | >70% |

| Program first‑year attrition | 30–60% |

| 5‑yr weight regain | ~80% |

What You See Is What You Get

Medifast SWOT Analysis

This is the actual Medifast SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, actionable content. Buy now to unlock the complete, editable version ready for download and use.

Elevate Your Analysis with the Complete SWOT Report

Medifast's SWOT highlights a strong brand in medically oriented weight-loss, scalable DTC and subscription revenue, and margin leverage from product portfolios—tempered by regulatory scrutiny, intense competition, and supply-chain exposure; growth hinges on digital coaching and international expansion. Discover the full SWOT analysis—purchase the complete, editable report for investor-ready insights and strategic tools.

Strengths

Scalable coach-driven direct-selling model

An independent coach network enables rapid, low-capex customer acquisition and personalized guidance at scale; Medifast’s coach-driven Optavia channel—supporting roughly 40,000+ coaches in recent filings—fuels word-of-mouth momentum and peer accountability. The model flexes with demand without fixed retail overhead and boosts lifetime value via recurring orders and upsell, supporting Medifast’s ~$1.06B revenue scale in 2024.

Proprietary OPTAVIA product portfolio

Owned OPTAVIA formulations and portion-controlled meals deliver consistent convenience, underpinning program adherence and supporting Medifast’s scale (net sales $1.07B in FY2023). Exclusive SKUs and brand equity reduce price comparability and limit commoditization. The bundled product ecosystem raises switching costs for clients, helping protect margins and recurring revenue.

Integrated program, education, and community

Combining meal plans with habit-building content drives behavioral change beyond calorie restriction, with behavioral interventions showing ~5–10% greater sustained weight loss at 12 months versus diet-only approaches. Community support improves adherence and outcomes—meta-analyses report roughly a 20–30% boost in adherence with social/coach support. Holistic positioning appeals to long-term wellness seekers and strengthens coach credibility and testimonial validity.

Attractive unit economics and margins

Medifasts direct-to-consumer fulfillment and owned-brand portfolio sustain industry-leading gross margins by capturing retail markup and minimizing third-party fees, while recurring auto-ship and program continuity enhance revenue visibility and lifetime customer value. A variable commission structure ties selling costs to sales flow, preserving margin as volume scales, enabling cash-generative operations during growth periods.

- Direct-to-consumer fulfillment

- Owned brands capture higher margins

- Recurring auto-ship improves visibility

- Variable commissions align costs

- Cash-generative in growth

Brand recognition in weight management

OPTAVIA is widely recognized in structured weight-loss programs and drives the bulk of Medifast revenue, accounting for roughly 80–90% of FY2023 company sales (FY2023 revenue approximately $1.35B). High-profile success stories and documented client transformations amplify social proof, improving coach recruitment and client conversion rates. The narrow focus on weight management sharpens OPTAVIAs value proposition versus general nutrition brands, aiding market differentiation.

- Brand: OPTAVIA dominant revenue driver (~80–90% of ~$1.35B FY2023)

- Social proof: documented success stories boost conversions

- Recruiting: strong brand recall eases coach acquisition

- Positioning: niche clarity vs broad nutrition competitors

Coach-led channel (≈40k) drives recurring auto-ship revenue, FY2024 $1.06B

Medifast’s coach-driven OPTAVIA channel (≈40,000+ coaches) enables low-capex customer acquisition, recurring auto-ship revenue and high lifetime value; OPTAVIA drove ~80–90% of company sales. Own-brand, portion-controlled products support adherence and recurring orders, sustaining scale (FY2024 revenue ≈$1.06B). Direct DTC fulfillment and variable commissions preserve margin and cash generation as volume grows.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.06B |

| OPTAVIA share | ~80–90% |

| Coach network | ≈40,000+ |

What is included in the product

Provides a concise SWOT analysis of Medifast, highlighting internal strengths like brand recognition and product portfolio, weaknesses such as customer concentration and margin pressure, opportunities in digital channels and international expansion, and threats from competitive intensity, regulatory changes, and consumer trends.

Provides a focused Medifast SWOT matrix that clarifies competitive strengths, market risks, and growth opportunities for rapid strategic action; editable format lets teams update factors as regulatory, supply-chain, or consumer trends shift.

Weaknesses

Dependence on independent coaches

Sales velocity is tightly tied to recruiting, training and retaining independent coaches, making growth dependent on headcount expansion. Variability in coach quality can undermine client outcomes and brand consistency, increasing churn; direct-selling networks often see annual turnover exceeding 70%. High turnover creates growth volatility and meaningful onboarding costs, while concentration risk rises if top leader networks churn.

MLM perceptions and compliance complexity

Direct-selling models like Medifast's face skepticism and reputational headwinds that can suppress consumer trust and partner recruitment; Medifast reported roughly $1.13 billion in 2023 revenue, exposing that scale to reputation risk.

Strict income, earnings and health-claim compliance requires significant legal and monitoring spend and any missteps by independent coaches can trigger FTC or state inquiries.

Negative narratives around MLM-like structures have shown to impair recruitment and demand, increasing churn and marketing costs for the Optavia coach network.

Adherence and churn in weight loss

Weight-management customers often relapse—studies show roughly 80% regain lost weight within five years—dampening Medifast retention. Program rigidity and taste fatigue contribute to 30–60% first‑year attrition seen in many structured plans, reducing long‑term engagement. High churn raises acquisition costs and compresses LTV/CAC, while variable results weaken referrals and coach morale.

Product concentration in meal replacements

Medifast's heavy reliance on portion-controlled meal replacements limits product diversification and market flexibility; shifts toward whole-food diets or GLP-1 treatments risk reducing relevance. Limited adjacent services constrain cross-sell potential, while supply or formula disruptions could materially impact revenue—Medifast reported roughly $1.08B in net sales in FY2023.

- High product concentration: majority revenues from meal replacements

- Market shift risk: rising whole-food/pharma alternatives

- Weak cross-sell: few adjacent services

- Supply/formula risk: major revenue exposure

Limited geographic breadth

Operations remain North America–centric with selective international exposure, leaving regulatory and macro risk concentrated; over 90% of net sales derive from the U.S. and Canada as of 2024. Global brand recognition and localized product menus are underdeveloped, limiting cross-border customer acquisition. Scale advantages abroad remain largely untapped, constraining long-term growth diversification.

- Geographic concentration: >90% revenue North America (2024)

- Regulatory/macro risk concentration

- Weak global brand/localization

- Untapped scale abroad

Direct-selling diet firm: coach turnover > 70%, attrition 30-60%

Medifast's growth is highly dependent on recruiting and retaining independent Optavia coaches, with direct-selling turnover often >70% and first‑year program attrition 30–60%, raising CAC and onboarding costs. Heavy product concentration (meal replacements ~majority of $1.13B 2023 revenue) and >90% North America revenue (2024) heighten market and supply risks, while relapse rates (~80% regain within 5 years) depress LTV.

| Metric | Value |

|---|---|

| FY2023 Revenue | $1.13B |

| North America Share (2024) | >90% |

| Coach turnover | >70% |

| Program first‑year attrition | 30–60% |

| 5‑yr weight regain | ~80% |

What You See Is What You Get

Medifast SWOT Analysis

This is the actual Medifast SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, actionable content. Buy now to unlock the complete, editable version ready for download and use.

Description

Elevate Your Analysis with the Complete SWOT Report

Medifast's SWOT highlights a strong brand in medically oriented weight-loss, scalable DTC and subscription revenue, and margin leverage from product portfolios—tempered by regulatory scrutiny, intense competition, and supply-chain exposure; growth hinges on digital coaching and international expansion. Discover the full SWOT analysis—purchase the complete, editable report for investor-ready insights and strategic tools.

Strengths

Scalable coach-driven direct-selling model

An independent coach network enables rapid, low-capex customer acquisition and personalized guidance at scale; Medifast’s coach-driven Optavia channel—supporting roughly 40,000+ coaches in recent filings—fuels word-of-mouth momentum and peer accountability. The model flexes with demand without fixed retail overhead and boosts lifetime value via recurring orders and upsell, supporting Medifast’s ~$1.06B revenue scale in 2024.

Proprietary OPTAVIA product portfolio

Owned OPTAVIA formulations and portion-controlled meals deliver consistent convenience, underpinning program adherence and supporting Medifast’s scale (net sales $1.07B in FY2023). Exclusive SKUs and brand equity reduce price comparability and limit commoditization. The bundled product ecosystem raises switching costs for clients, helping protect margins and recurring revenue.

Integrated program, education, and community

Combining meal plans with habit-building content drives behavioral change beyond calorie restriction, with behavioral interventions showing ~5–10% greater sustained weight loss at 12 months versus diet-only approaches. Community support improves adherence and outcomes—meta-analyses report roughly a 20–30% boost in adherence with social/coach support. Holistic positioning appeals to long-term wellness seekers and strengthens coach credibility and testimonial validity.

Attractive unit economics and margins

Medifasts direct-to-consumer fulfillment and owned-brand portfolio sustain industry-leading gross margins by capturing retail markup and minimizing third-party fees, while recurring auto-ship and program continuity enhance revenue visibility and lifetime customer value. A variable commission structure ties selling costs to sales flow, preserving margin as volume scales, enabling cash-generative operations during growth periods.

- Direct-to-consumer fulfillment

- Owned brands capture higher margins

- Recurring auto-ship improves visibility

- Variable commissions align costs

- Cash-generative in growth

Brand recognition in weight management

OPTAVIA is widely recognized in structured weight-loss programs and drives the bulk of Medifast revenue, accounting for roughly 80–90% of FY2023 company sales (FY2023 revenue approximately $1.35B). High-profile success stories and documented client transformations amplify social proof, improving coach recruitment and client conversion rates. The narrow focus on weight management sharpens OPTAVIAs value proposition versus general nutrition brands, aiding market differentiation.

- Brand: OPTAVIA dominant revenue driver (~80–90% of ~$1.35B FY2023)

- Social proof: documented success stories boost conversions

- Recruiting: strong brand recall eases coach acquisition

- Positioning: niche clarity vs broad nutrition competitors

Coach-led channel (≈40k) drives recurring auto-ship revenue, FY2024 $1.06B

Medifast’s coach-driven OPTAVIA channel (≈40,000+ coaches) enables low-capex customer acquisition, recurring auto-ship revenue and high lifetime value; OPTAVIA drove ~80–90% of company sales. Own-brand, portion-controlled products support adherence and recurring orders, sustaining scale (FY2024 revenue ≈$1.06B). Direct DTC fulfillment and variable commissions preserve margin and cash generation as volume grows.

| Metric | Value |

|---|---|

| FY2024 revenue | $1.06B |

| OPTAVIA share | ~80–90% |

| Coach network | ≈40,000+ |

What is included in the product

Provides a concise SWOT analysis of Medifast, highlighting internal strengths like brand recognition and product portfolio, weaknesses such as customer concentration and margin pressure, opportunities in digital channels and international expansion, and threats from competitive intensity, regulatory changes, and consumer trends.

Provides a focused Medifast SWOT matrix that clarifies competitive strengths, market risks, and growth opportunities for rapid strategic action; editable format lets teams update factors as regulatory, supply-chain, or consumer trends shift.

Weaknesses

Dependence on independent coaches

Sales velocity is tightly tied to recruiting, training and retaining independent coaches, making growth dependent on headcount expansion. Variability in coach quality can undermine client outcomes and brand consistency, increasing churn; direct-selling networks often see annual turnover exceeding 70%. High turnover creates growth volatility and meaningful onboarding costs, while concentration risk rises if top leader networks churn.

MLM perceptions and compliance complexity

Direct-selling models like Medifast's face skepticism and reputational headwinds that can suppress consumer trust and partner recruitment; Medifast reported roughly $1.13 billion in 2023 revenue, exposing that scale to reputation risk.

Strict income, earnings and health-claim compliance requires significant legal and monitoring spend and any missteps by independent coaches can trigger FTC or state inquiries.

Negative narratives around MLM-like structures have shown to impair recruitment and demand, increasing churn and marketing costs for the Optavia coach network.

Adherence and churn in weight loss

Weight-management customers often relapse—studies show roughly 80% regain lost weight within five years—dampening Medifast retention. Program rigidity and taste fatigue contribute to 30–60% first‑year attrition seen in many structured plans, reducing long‑term engagement. High churn raises acquisition costs and compresses LTV/CAC, while variable results weaken referrals and coach morale.

Product concentration in meal replacements

Medifast's heavy reliance on portion-controlled meal replacements limits product diversification and market flexibility; shifts toward whole-food diets or GLP-1 treatments risk reducing relevance. Limited adjacent services constrain cross-sell potential, while supply or formula disruptions could materially impact revenue—Medifast reported roughly $1.08B in net sales in FY2023.

- High product concentration: majority revenues from meal replacements

- Market shift risk: rising whole-food/pharma alternatives

- Weak cross-sell: few adjacent services

- Supply/formula risk: major revenue exposure

Limited geographic breadth

Operations remain North America–centric with selective international exposure, leaving regulatory and macro risk concentrated; over 90% of net sales derive from the U.S. and Canada as of 2024. Global brand recognition and localized product menus are underdeveloped, limiting cross-border customer acquisition. Scale advantages abroad remain largely untapped, constraining long-term growth diversification.

- Geographic concentration: >90% revenue North America (2024)

- Regulatory/macro risk concentration

- Weak global brand/localization

- Untapped scale abroad

Direct-selling diet firm: coach turnover > 70%, attrition 30-60%

Medifast's growth is highly dependent on recruiting and retaining independent Optavia coaches, with direct-selling turnover often >70% and first‑year program attrition 30–60%, raising CAC and onboarding costs. Heavy product concentration (meal replacements ~majority of $1.13B 2023 revenue) and >90% North America revenue (2024) heighten market and supply risks, while relapse rates (~80% regain within 5 years) depress LTV.

| Metric | Value |

|---|---|

| FY2023 Revenue | $1.13B |

| North America Share (2024) | >90% |

| Coach turnover | >70% |

| Program first‑year attrition | 30–60% |

| 5‑yr weight regain | ~80% |

What You See Is What You Get

Medifast SWOT Analysis

This is the actual Medifast SWOT analysis document you’ll receive upon purchase—no surprises, just professional quality. The preview below is taken directly from the full report and reflects the same structured, actionable content. Buy now to unlock the complete, editable version ready for download and use.