Medipal Holdings PESTLE Analysis

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of Medipal Holdings—three to five expertly crafted insights reveal how political shifts, economic cycles, and technological change shape its healthcare distribution edge. Ideal for investors, strategists, and consultants, this concise briefing pinpoints risks and growth levers you can act on. Purchase the full report for a complete, ready-to-use external landscape and tactical recommendations.

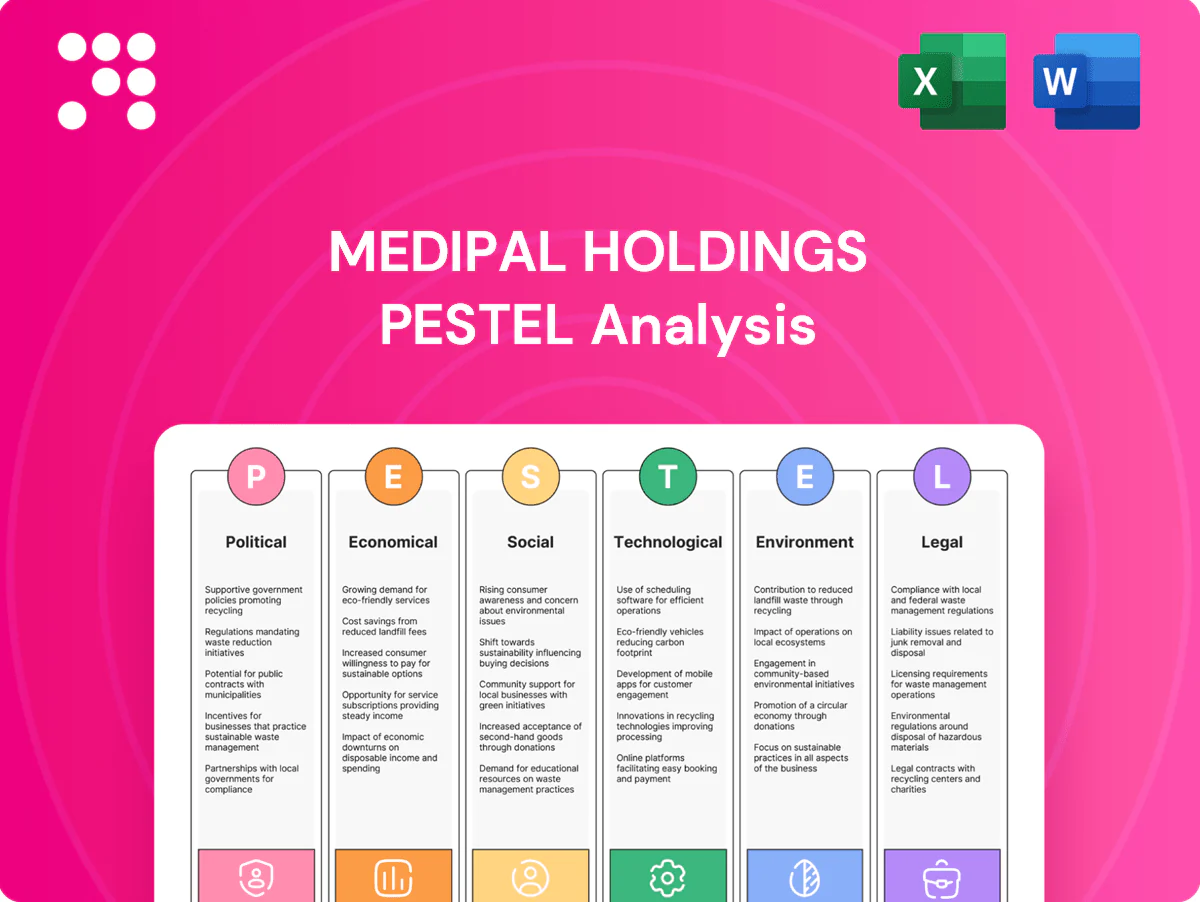

Political factors

Japan’s drug pricing and reimbursement controls

Biennial NHI price revisions (last held 2024 with an overall drug price cut near 0.5%) compress distributor margins and force Medipal to drive procurement and operating efficiencies.

Government push for generics—Japan exceeded its 80% volume target—reshapes product mix and increases rebate/volume-based pricing pressure.

Medipal must align contracting and portfolio strategy with MHLW cost-containment rules, while shifts in reimbursement for specialty and expanding home-care therapies raise logistics complexity and service fee volatility.

Regulatory oversight of pharma distribution

Policies on GDP/GQP and traceability force Medipal to invest in cold-chain monitoring and IT compliance as Japan is the world’s second-largest pharmaceutical market. PMDA and MHLW directives set handling, recall and documentation requirements that directly affect warehouse and transport protocols. Stricter audits raise fixed compliance costs but increase entry barriers for smaller rivals. Alignment with regional health bureaus is vital to retain distribution licenses.

Healthcare system reform and digitalization

Government mandates on e-prescriptions, electronic medical records, and health data linkage are steering Medipal’s information-services roadmap toward robust interoperability and secure APIs. Incentives for community-based integrated care broaden opportunities in last-mile logistics and home-delivery pharmaceuticals, increasing demand for platform-enabled coordination. Policy pilots offer first-mover advantages for compliant platforms able to meet regulatory standards and integrate with national systems.

Geopolitical and trade policy exposure

APAC supply chains for APIs, cosmetics inputs and devices are exposed to export controls and tariffs; China and India account for roughly 70% of global API production, while RCEP covers ~30% of world GDP and CPTPP has 11 members, so Japan’s FTAs and its Economic Security Promotion Act (2021, tightened 2022–23) may reroute sourcing.

Political tensions have lengthened lead times by an estimated 20–30%, prompting higher buffer inventory; close coordination and dual-sourcing with suppliers helps mitigate shortages of critical medicines.

- API concentration ~70%

- RCEP ~30% global GDP

- CPTPP 11 members

- Lead times +20–30%

Disaster preparedness and public health priorities

National disaster-response policy now mandates resilient medical logistics; government stockpiling and emergency distribution frameworks create predictable procurement channels, while pandemic lessons elevated cold-chain and surge-capacity standards.

Japan population 125.4 million with 29.1% aged 65+ (2023), increasing demand for continuity of care; participation in public tenders (TYO:7459 Medipal) hinges on certified crisis-protocol compliance.

- Resilient logistics mandated

- Government stockpiles → stable tenders

- Higher cold-chain & surge standards

- Public tenders require crisis compliance

Japan pharma: NHI cuts, generics pricing, API concentration and aging population squeeze margins

Biennial NHI cuts (2024 ~0.5%) compress margins, forcing procurement and efficiency drives.

Generics policy (Japan >80% volume) and MHLW rebate rules pressure pricing and portfolio mix.

API concentration (~70% in China/India) and geopolitical export controls lengthen lead times +20–30% and raise dual-sourcing needs.

Demographics (Japan 125.4M; 65+ 29.1% in 2023) expand chronic-care demand and public-tender exposure (TYO:7459).

| Metric | Value |

|---|---|

| NHI cut 2024 | ~0.5% |

| API share (China/India) | ~70% |

| Lead times | +20–30% |

| Japan pop / 65+ | 125.4M / 29.1% |

What is included in the product

Explores how macro-environmental factors uniquely affect Medipal Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category grounded in current data and industry trends. Designed to help executives, consultants, and investors identify risks and opportunities, reflect regional market and regulatory dynamics, and support scenario planning and strategic decision-making.

A concise, visually segmented PESTLE summary for Medipal Holdings that’s slide-ready and easily shareable, allowing teams to add regional notes and quickly align on external risks and market positioning during planning sessions.

Economic factors

Aging population–driven healthcare demand

Japan’s 65+ cohort is about 29% of the population (~36 million), supporting steady prescription volumes and baseline throughput for wholesalers; healthcare spending runs near 11% of GDP. A rising share of high-value specialty drugs increases cold-chain and pharmacovigilance complexity, while long-term care/home-care channels—with LTC benefits around ¥11 trillion (2023)—demand tailored delivery and inventory services.

Currency and import cost volatility

Yen volatility—USD/JPY trading in the 145–155 range and a roughly 15% decline in the trade-weighted yen since 2022—raises import costs for drugs, devices and cosmetic inputs, forcing Medipal to use hedging and indexed pricing clauses to protect margins; sudden depreciation stresses working capital and rebate structures, making transparent pass-through mechanisms with providers essential.

Inflation and logistics cost pressures

Rising fuel, labor and packaging costs—with Japan CPI at about 3.2% in 2024 and Brent crude averaging roughly 86 USD/bbl in 2024—elevate Medipal’s distribution expenses and squeeze margins. Route optimization and automation can preserve unit economics by cutting last-mile costs and labor intensity. Energy-efficiency measures reduce exposure to utility price swings, while contract renegotiations may be required to reflect these 2024–25 cost realities.

Provider consolidation and bargaining power

Provider consolidation lets hospital groups, chains and pharmacy networks negotiate aggressively with distributors; in Japan the largest pharmacy chains now capture roughly 40–50% of prescription volume, compressing distributor margins even as they deliver scale and data-sharing that can boost turnover. Larger accounts may shrink gross margins by 3–7% but add volume and analytics revenue; tiered service models let Medipal segment profitability while loss-leader SKUs can be offset by value-added logistics fees and chargebacks.

- Negotiation leverage: top chains ~40–50% share

- Margin squeeze: large-account compression ~3–7%

- Revenue offset: logistics/value-added fees

- Profit levers: tiered service segmentation

Macroeconomic cycles and consumer spending

Daily necessities and cosmetics revenues track real-income trends: global beauty was about 511 billion USD in 2023, with premium beauty more cyclical while essentials show resilience; Medipal’s exposure to staples cushions revenue shocks. Animal health, a roughly 57 billion USD market in 2024, stays relatively steady but can soften in downturns. Portfolio balance across retail, OTC and animal health mitigates segment cyclicality.

- essentials resilient vs income shocks

- premium beauty cyclical, linked to discretionary spend

- animal health steady but vulnerable in recessions

- diversified portfolio reduces volatility

Japan pharma: NHI cuts, generics pricing, API concentration and aging population squeeze margins

Japan 65+ ~29% (~36M) supports stable Rx volumes; healthcare ~11% of GDP and LTC benefits ¥11T (2023).

USD/JPY 145–155 and ~15% trade-weighted yen fall since 2022 raise import costs; hedging/indexed pricing needed.

CPI ~3.2% (2024) and Brent ~$86/bbl (2024) push distribution costs; route optimization and automation cut margins pressure.

Top pharmacy chains 40–50% share compress margins ~3–7%; diversified OTC/animal health (animal health ~$57B 2024) cushions cyclicality.

| Metric | Value |

|---|---|

| 65+ share | 29% (~36M) |

| Healthcare % GDP | ~11% |

| USD/JPY | 145–155 |

| CPI (2024) | 3.2% |

What You See Is What You Get

Medipal Holdings PESTLE Analysis

The preview shown here is the exact Medipal Holdings PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and layout visible in this preview are identical to the downloadable file with no placeholders or surprises. After payment you’ll instantly receive this finished, professionally structured file.

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of Medipal Holdings—three to five expertly crafted insights reveal how political shifts, economic cycles, and technological change shape its healthcare distribution edge. Ideal for investors, strategists, and consultants, this concise briefing pinpoints risks and growth levers you can act on. Purchase the full report for a complete, ready-to-use external landscape and tactical recommendations.

Political factors

Japan’s drug pricing and reimbursement controls

Biennial NHI price revisions (last held 2024 with an overall drug price cut near 0.5%) compress distributor margins and force Medipal to drive procurement and operating efficiencies.

Government push for generics—Japan exceeded its 80% volume target—reshapes product mix and increases rebate/volume-based pricing pressure.

Medipal must align contracting and portfolio strategy with MHLW cost-containment rules, while shifts in reimbursement for specialty and expanding home-care therapies raise logistics complexity and service fee volatility.

Regulatory oversight of pharma distribution

Policies on GDP/GQP and traceability force Medipal to invest in cold-chain monitoring and IT compliance as Japan is the world’s second-largest pharmaceutical market. PMDA and MHLW directives set handling, recall and documentation requirements that directly affect warehouse and transport protocols. Stricter audits raise fixed compliance costs but increase entry barriers for smaller rivals. Alignment with regional health bureaus is vital to retain distribution licenses.

Healthcare system reform and digitalization

Government mandates on e-prescriptions, electronic medical records, and health data linkage are steering Medipal’s information-services roadmap toward robust interoperability and secure APIs. Incentives for community-based integrated care broaden opportunities in last-mile logistics and home-delivery pharmaceuticals, increasing demand for platform-enabled coordination. Policy pilots offer first-mover advantages for compliant platforms able to meet regulatory standards and integrate with national systems.

Geopolitical and trade policy exposure

APAC supply chains for APIs, cosmetics inputs and devices are exposed to export controls and tariffs; China and India account for roughly 70% of global API production, while RCEP covers ~30% of world GDP and CPTPP has 11 members, so Japan’s FTAs and its Economic Security Promotion Act (2021, tightened 2022–23) may reroute sourcing.

Political tensions have lengthened lead times by an estimated 20–30%, prompting higher buffer inventory; close coordination and dual-sourcing with suppliers helps mitigate shortages of critical medicines.

- API concentration ~70%

- RCEP ~30% global GDP

- CPTPP 11 members

- Lead times +20–30%

Disaster preparedness and public health priorities

National disaster-response policy now mandates resilient medical logistics; government stockpiling and emergency distribution frameworks create predictable procurement channels, while pandemic lessons elevated cold-chain and surge-capacity standards.

Japan population 125.4 million with 29.1% aged 65+ (2023), increasing demand for continuity of care; participation in public tenders (TYO:7459 Medipal) hinges on certified crisis-protocol compliance.

- Resilient logistics mandated

- Government stockpiles → stable tenders

- Higher cold-chain & surge standards

- Public tenders require crisis compliance

Japan pharma: NHI cuts, generics pricing, API concentration and aging population squeeze margins

Biennial NHI cuts (2024 ~0.5%) compress margins, forcing procurement and efficiency drives.

Generics policy (Japan >80% volume) and MHLW rebate rules pressure pricing and portfolio mix.

API concentration (~70% in China/India) and geopolitical export controls lengthen lead times +20–30% and raise dual-sourcing needs.

Demographics (Japan 125.4M; 65+ 29.1% in 2023) expand chronic-care demand and public-tender exposure (TYO:7459).

| Metric | Value |

|---|---|

| NHI cut 2024 | ~0.5% |

| API share (China/India) | ~70% |

| Lead times | +20–30% |

| Japan pop / 65+ | 125.4M / 29.1% |

What is included in the product

Explores how macro-environmental factors uniquely affect Medipal Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category grounded in current data and industry trends. Designed to help executives, consultants, and investors identify risks and opportunities, reflect regional market and regulatory dynamics, and support scenario planning and strategic decision-making.

A concise, visually segmented PESTLE summary for Medipal Holdings that’s slide-ready and easily shareable, allowing teams to add regional notes and quickly align on external risks and market positioning during planning sessions.

Economic factors

Aging population–driven healthcare demand

Japan’s 65+ cohort is about 29% of the population (~36 million), supporting steady prescription volumes and baseline throughput for wholesalers; healthcare spending runs near 11% of GDP. A rising share of high-value specialty drugs increases cold-chain and pharmacovigilance complexity, while long-term care/home-care channels—with LTC benefits around ¥11 trillion (2023)—demand tailored delivery and inventory services.

Currency and import cost volatility

Yen volatility—USD/JPY trading in the 145–155 range and a roughly 15% decline in the trade-weighted yen since 2022—raises import costs for drugs, devices and cosmetic inputs, forcing Medipal to use hedging and indexed pricing clauses to protect margins; sudden depreciation stresses working capital and rebate structures, making transparent pass-through mechanisms with providers essential.

Inflation and logistics cost pressures

Rising fuel, labor and packaging costs—with Japan CPI at about 3.2% in 2024 and Brent crude averaging roughly 86 USD/bbl in 2024—elevate Medipal’s distribution expenses and squeeze margins. Route optimization and automation can preserve unit economics by cutting last-mile costs and labor intensity. Energy-efficiency measures reduce exposure to utility price swings, while contract renegotiations may be required to reflect these 2024–25 cost realities.

Provider consolidation and bargaining power

Provider consolidation lets hospital groups, chains and pharmacy networks negotiate aggressively with distributors; in Japan the largest pharmacy chains now capture roughly 40–50% of prescription volume, compressing distributor margins even as they deliver scale and data-sharing that can boost turnover. Larger accounts may shrink gross margins by 3–7% but add volume and analytics revenue; tiered service models let Medipal segment profitability while loss-leader SKUs can be offset by value-added logistics fees and chargebacks.

- Negotiation leverage: top chains ~40–50% share

- Margin squeeze: large-account compression ~3–7%

- Revenue offset: logistics/value-added fees

- Profit levers: tiered service segmentation

Macroeconomic cycles and consumer spending

Daily necessities and cosmetics revenues track real-income trends: global beauty was about 511 billion USD in 2023, with premium beauty more cyclical while essentials show resilience; Medipal’s exposure to staples cushions revenue shocks. Animal health, a roughly 57 billion USD market in 2024, stays relatively steady but can soften in downturns. Portfolio balance across retail, OTC and animal health mitigates segment cyclicality.

- essentials resilient vs income shocks

- premium beauty cyclical, linked to discretionary spend

- animal health steady but vulnerable in recessions

- diversified portfolio reduces volatility

Japan pharma: NHI cuts, generics pricing, API concentration and aging population squeeze margins

Japan 65+ ~29% (~36M) supports stable Rx volumes; healthcare ~11% of GDP and LTC benefits ¥11T (2023).

USD/JPY 145–155 and ~15% trade-weighted yen fall since 2022 raise import costs; hedging/indexed pricing needed.

CPI ~3.2% (2024) and Brent ~$86/bbl (2024) push distribution costs; route optimization and automation cut margins pressure.

Top pharmacy chains 40–50% share compress margins ~3–7%; diversified OTC/animal health (animal health ~$57B 2024) cushions cyclicality.

| Metric | Value |

|---|---|

| 65+ share | 29% (~36M) |

| Healthcare % GDP | ~11% |

| USD/JPY | 145–155 |

| CPI (2024) | 3.2% |

What You See Is What You Get

Medipal Holdings PESTLE Analysis

The preview shown here is the exact Medipal Holdings PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and layout visible in this preview are identical to the downloadable file with no placeholders or surprises. After payment you’ll instantly receive this finished, professionally structured file.

Original: $10.00

-65%$10.00

$3.50Description

Your Competitive Advantage Starts with This Report

Unlock strategic clarity with our PESTLE Analysis of Medipal Holdings—three to five expertly crafted insights reveal how political shifts, economic cycles, and technological change shape its healthcare distribution edge. Ideal for investors, strategists, and consultants, this concise briefing pinpoints risks and growth levers you can act on. Purchase the full report for a complete, ready-to-use external landscape and tactical recommendations.

Political factors

Japan’s drug pricing and reimbursement controls

Biennial NHI price revisions (last held 2024 with an overall drug price cut near 0.5%) compress distributor margins and force Medipal to drive procurement and operating efficiencies.

Government push for generics—Japan exceeded its 80% volume target—reshapes product mix and increases rebate/volume-based pricing pressure.

Medipal must align contracting and portfolio strategy with MHLW cost-containment rules, while shifts in reimbursement for specialty and expanding home-care therapies raise logistics complexity and service fee volatility.

Regulatory oversight of pharma distribution

Policies on GDP/GQP and traceability force Medipal to invest in cold-chain monitoring and IT compliance as Japan is the world’s second-largest pharmaceutical market. PMDA and MHLW directives set handling, recall and documentation requirements that directly affect warehouse and transport protocols. Stricter audits raise fixed compliance costs but increase entry barriers for smaller rivals. Alignment with regional health bureaus is vital to retain distribution licenses.

Healthcare system reform and digitalization

Government mandates on e-prescriptions, electronic medical records, and health data linkage are steering Medipal’s information-services roadmap toward robust interoperability and secure APIs. Incentives for community-based integrated care broaden opportunities in last-mile logistics and home-delivery pharmaceuticals, increasing demand for platform-enabled coordination. Policy pilots offer first-mover advantages for compliant platforms able to meet regulatory standards and integrate with national systems.

Geopolitical and trade policy exposure

APAC supply chains for APIs, cosmetics inputs and devices are exposed to export controls and tariffs; China and India account for roughly 70% of global API production, while RCEP covers ~30% of world GDP and CPTPP has 11 members, so Japan’s FTAs and its Economic Security Promotion Act (2021, tightened 2022–23) may reroute sourcing.

Political tensions have lengthened lead times by an estimated 20–30%, prompting higher buffer inventory; close coordination and dual-sourcing with suppliers helps mitigate shortages of critical medicines.

- API concentration ~70%

- RCEP ~30% global GDP

- CPTPP 11 members

- Lead times +20–30%

Disaster preparedness and public health priorities

National disaster-response policy now mandates resilient medical logistics; government stockpiling and emergency distribution frameworks create predictable procurement channels, while pandemic lessons elevated cold-chain and surge-capacity standards.

Japan population 125.4 million with 29.1% aged 65+ (2023), increasing demand for continuity of care; participation in public tenders (TYO:7459 Medipal) hinges on certified crisis-protocol compliance.

- Resilient logistics mandated

- Government stockpiles → stable tenders

- Higher cold-chain & surge standards

- Public tenders require crisis compliance

Japan pharma: NHI cuts, generics pricing, API concentration and aging population squeeze margins

Biennial NHI cuts (2024 ~0.5%) compress margins, forcing procurement and efficiency drives.

Generics policy (Japan >80% volume) and MHLW rebate rules pressure pricing and portfolio mix.

API concentration (~70% in China/India) and geopolitical export controls lengthen lead times +20–30% and raise dual-sourcing needs.

Demographics (Japan 125.4M; 65+ 29.1% in 2023) expand chronic-care demand and public-tender exposure (TYO:7459).

| Metric | Value |

|---|---|

| NHI cut 2024 | ~0.5% |

| API share (China/India) | ~70% |

| Lead times | +20–30% |

| Japan pop / 65+ | 125.4M / 29.1% |

What is included in the product

Explores how macro-environmental factors uniquely affect Medipal Holdings across Political, Economic, Social, Technological, Environmental, and Legal dimensions, with each category grounded in current data and industry trends. Designed to help executives, consultants, and investors identify risks and opportunities, reflect regional market and regulatory dynamics, and support scenario planning and strategic decision-making.

A concise, visually segmented PESTLE summary for Medipal Holdings that’s slide-ready and easily shareable, allowing teams to add regional notes and quickly align on external risks and market positioning during planning sessions.

Economic factors

Aging population–driven healthcare demand

Japan’s 65+ cohort is about 29% of the population (~36 million), supporting steady prescription volumes and baseline throughput for wholesalers; healthcare spending runs near 11% of GDP. A rising share of high-value specialty drugs increases cold-chain and pharmacovigilance complexity, while long-term care/home-care channels—with LTC benefits around ¥11 trillion (2023)—demand tailored delivery and inventory services.

Currency and import cost volatility

Yen volatility—USD/JPY trading in the 145–155 range and a roughly 15% decline in the trade-weighted yen since 2022—raises import costs for drugs, devices and cosmetic inputs, forcing Medipal to use hedging and indexed pricing clauses to protect margins; sudden depreciation stresses working capital and rebate structures, making transparent pass-through mechanisms with providers essential.

Inflation and logistics cost pressures

Rising fuel, labor and packaging costs—with Japan CPI at about 3.2% in 2024 and Brent crude averaging roughly 86 USD/bbl in 2024—elevate Medipal’s distribution expenses and squeeze margins. Route optimization and automation can preserve unit economics by cutting last-mile costs and labor intensity. Energy-efficiency measures reduce exposure to utility price swings, while contract renegotiations may be required to reflect these 2024–25 cost realities.

Provider consolidation and bargaining power

Provider consolidation lets hospital groups, chains and pharmacy networks negotiate aggressively with distributors; in Japan the largest pharmacy chains now capture roughly 40–50% of prescription volume, compressing distributor margins even as they deliver scale and data-sharing that can boost turnover. Larger accounts may shrink gross margins by 3–7% but add volume and analytics revenue; tiered service models let Medipal segment profitability while loss-leader SKUs can be offset by value-added logistics fees and chargebacks.

- Negotiation leverage: top chains ~40–50% share

- Margin squeeze: large-account compression ~3–7%

- Revenue offset: logistics/value-added fees

- Profit levers: tiered service segmentation

Macroeconomic cycles and consumer spending

Daily necessities and cosmetics revenues track real-income trends: global beauty was about 511 billion USD in 2023, with premium beauty more cyclical while essentials show resilience; Medipal’s exposure to staples cushions revenue shocks. Animal health, a roughly 57 billion USD market in 2024, stays relatively steady but can soften in downturns. Portfolio balance across retail, OTC and animal health mitigates segment cyclicality.

- essentials resilient vs income shocks

- premium beauty cyclical, linked to discretionary spend

- animal health steady but vulnerable in recessions

- diversified portfolio reduces volatility

Japan pharma: NHI cuts, generics pricing, API concentration and aging population squeeze margins

Japan 65+ ~29% (~36M) supports stable Rx volumes; healthcare ~11% of GDP and LTC benefits ¥11T (2023).

USD/JPY 145–155 and ~15% trade-weighted yen fall since 2022 raise import costs; hedging/indexed pricing needed.

CPI ~3.2% (2024) and Brent ~$86/bbl (2024) push distribution costs; route optimization and automation cut margins pressure.

Top pharmacy chains 40–50% share compress margins ~3–7%; diversified OTC/animal health (animal health ~$57B 2024) cushions cyclicality.

| Metric | Value |

|---|---|

| 65+ share | 29% (~36M) |

| Healthcare % GDP | ~11% |

| USD/JPY | 145–155 |

| CPI (2024) | 3.2% |

What You See Is What You Get

Medipal Holdings PESTLE Analysis

The preview shown here is the exact Medipal Holdings PESTLE Analysis document you’ll receive after purchase—fully formatted and ready to use. The content, structure, and layout visible in this preview are identical to the downloadable file with no placeholders or surprises. After payment you’ll instantly receive this finished, professionally structured file.