Medirom Porter's Five Forces Analysis

Don't Miss the Bigger Picture

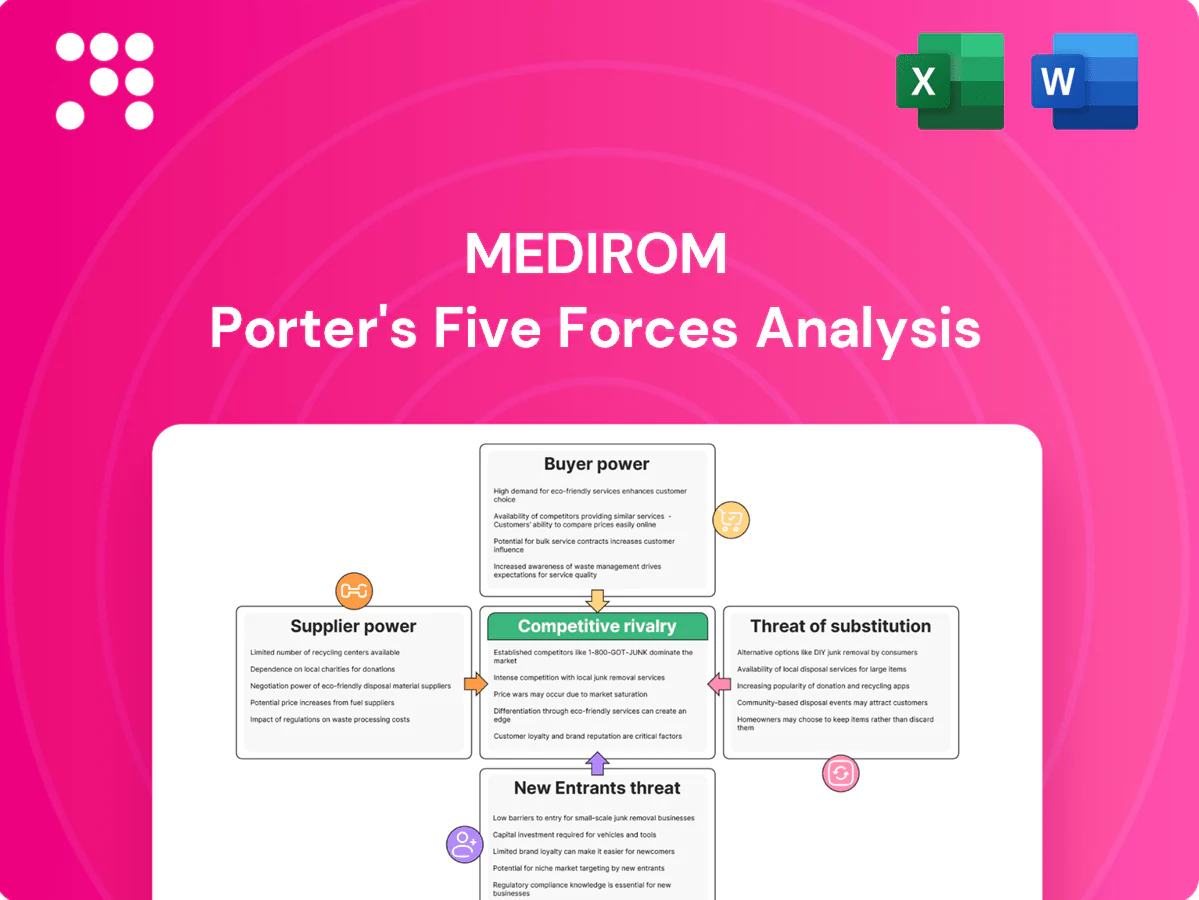

Medirom faces moderate supplier power, discerning buyers, regulatory hurdles, potential new entrants in digital health, and substitution risks from telemedicine platforms. This snapshot highlights competitive intensity, pricing pressure, and strategic levers but omits detailed metrics and force-by-force ratings. Unlock the full Porter's Five Forces Analysis to explore Medirom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

Licensed therapists are a core input; Japan’s tight labor market (unemployment ~2.6% in 2024) and aging population (65+ ~29% in 2024) elevate wage demands and scheduling constraints. In urban centers experienced practitioners command premiums or churn to independents, increasing dependence risk. Medirom’s in-house training reduces but cannot eliminate scarcity, and supplier power spikes in peak seasons and tight markets.

Supplier Power 2

Landlords of high-traffic malls and stations hold leverage over Re.Ra.Ku footfall, with scarce comparable sites often pushing rents and key-money premiums roughly 15–30% in 2024; long leases and fit-out costs (commonly $80k–$200k per site) raise switching frictions and sunk-cost risk, while portfolio-wide lease negotiations can trim landlord leverage, typically yielding 5–10% rent reductions.

Supplier Power 3

Equipment vendors for treatment beds and wearable components remain fragmented, keeping pricing competitive while the global wearable medical device market reached about $31 billion in 2024; however, specialized sensors, proprietary SDKs and small-batch manufacturing create dependency and supplier leverage. Component lead times often exceed 20 weeks and quality variance delays rollouts; dual-sourcing and standards adoption materially lower that risk.

Supplier Power 4

Supplier Power 4: Data and software providers exert strong leverage through platform lock-in; the public cloud market was ≈$600B in 2024 with top vendors holding ~32%/23%/11% (AWS/Azure/GCP), making migrations 6–12 months and often multi‑million dollar projects when accounting for compliance (HIPAA, SOC2) and security integrations. Volume pricing can reduce costs but feature gaps limit viable substitutes, so strategic partnerships buy roadmap influence.

- Platform lock-in: cloud market ≈$600B (2024)

- Top shares: AWS 32% / Azure 23% / GCP 11%

- Migration: 6–12 months, multi‑million enterprise spend

- Mitigation: volume pricing, strategic partnerships for roadmap access

Supplier Power 5

Training, certification bodies, and content creators heavily influence service consistency for Medirom; proprietary curricula limit supplier exposure while accreditation boosts corporate credibility, and the global corporate wellness market reached about $62 billion in 2024, widening buyer options. Standards shifts force retraining, adding measurable time and cost, so internal academies balance quality control with scalable delivery.

- Training dependency: certification bodies drive consistency

- Proprietary curricula: lowers supplier risk

- Accreditation: increases corporate adoption

- Retraining: adds time and cost

- Internal academy: control + scalability

Supplier squeeze: labor tight, rents up, wearables delays, cloud $600B

Licensed therapists, landlords, equipment and cloud providers exert moderate–high supplier power: labor tightness (Japan unemployment 2.6%, 65+ 29% in 2024) raises wages; prime retail rents +15–30%; wearable market $31B (2024) with >20-week lead times; public cloud ≈$600B (2024) dominated by AWS 32%/Azure 23%/GCP 11%.

| Supplier | Key metric (2024) |

|---|---|

| Labor | Unemp 2.6% / 65+ 29% |

| Landlords | Rents +15–30% |

| Cloud | $600B; AWS32%/AZ23%/GCP11% |

What is included in the product

Tailored Porter's Five Forces analysis for Medirom uncovering key drivers of competition, buyer and supplier power, substitutes and new-entry risks, and identifying disruptive threats and protective market dynamics—delivered in a fully editable Word format for investor materials, strategy decks, or academic use.

Medirom's Porter's Five Forces delivers a clear, one-sheet summary of competitive pressures—perfect for quick decision-making and slide-ready insights.

Customers Bargaining Power

Buyer Power 1

Individual retail clients face low switching costs among neighborhood relaxation studios; BrightLocal 2024 found 87% of consumers consult online reviews for local services, amplifying bargaining power. Price transparency via booking apps and review platforms increases comparison shopping. Promotions and packages are expected to drive repeat visits, so differentiation through superior service quality and loyalty programs is vital.

Buyer Power 2

Corporate wellness clients commonly negotiate volume discounts of 10–25% and tailored programs, leveraging bundling and multi-vendor comparisons to increase bargaining power. Contract durations of 12–36 months and outcome KPIs (absenteeism, HRI reductions) create margin pressure. Demonstrated ROI (often cited near 3:1) and detailed data reporting shift discussions from price to outcomes, reducing pure price sensitivity.

Buyer Power 3

Buyer Power 3: Medirom users benchmark against global health-tech leaders as the digital health market reached about $260 billion in 2024; feature parity, UX quality and ecosystem compatibility drive willingness to pay. With average 30‑day retention near 15%, churn risk is high absent unique clinical insights or seamless services integration. Bundling studio benefits with digital offerings can raise switching costs and lock in value.

Buyer Power 4

Peak-time congestion turns scheduling into a commodity decision; 2024 data indicate customers defect to alternatives as wait times rise, increasing buyer leverage. Dynamic pricing can smooth demand but in 2024 sparked fairness concerns and churn in sensitive segments. Capacity planning directly affects perceived value and retention.

- High wait sensitivity — customers switch when delays grow

- Dynamic pricing trade-off — revenue vs fairness risk

- Capacity = perceived value

Buyer Power 5

Enterprise and insurer partnerships can steer large user bases, concentrating buyer power and enabling volume-driven pricing pressure; procurement increasingly demands HIPAA, SOC 2 and ISO 27001 compliance and robust data governance. Multi-year contracts commonly exchange lower margins for revenue visibility, while peer-reviewed case studies and clinical evidence materially strengthen negotiation leverage.

- Buyer concentration: enterprise/insurer deals drive scale

- Compliance: HIPAA, SOC 2, ISO 27001

- Contracting: multi-year = margin for stability

- Evidence: clinical studies boost negotiating position

Review-driven retail churn (15% 30-day) vs enterprise ROI/compliance — UX and integrations decide

Retail customers exhibit high price transparency and low switching costs; 87% consult reviews and 30-day retention is ~15% (2024), raising churn risk.

Corporate buyers secure 10–25% volume discounts, 12–36 month contracts and demand ROI (~3:1) and compliance (HIPAA, SOC 2, ISO 27001).

Market parity (digital health ~$260B in 2024) means feature, UX and integration drive willingness to pay.

| Metric | 2024 Value |

|---|---|

| Reviews Consulted | 87% |

| 30-day Retention | ~15% |

| Corporate Discounts | 10–25% |

| Digital Health Market | $260B |

Same Document Delivered

Medirom Porter's Five Forces Analysis

This preview shows the exact Medirom Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the same final file that will be available to you instantly after payment.

Don't Miss the Bigger Picture

Medirom faces moderate supplier power, discerning buyers, regulatory hurdles, potential new entrants in digital health, and substitution risks from telemedicine platforms. This snapshot highlights competitive intensity, pricing pressure, and strategic levers but omits detailed metrics and force-by-force ratings. Unlock the full Porter's Five Forces Analysis to explore Medirom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

Licensed therapists are a core input; Japan’s tight labor market (unemployment ~2.6% in 2024) and aging population (65+ ~29% in 2024) elevate wage demands and scheduling constraints. In urban centers experienced practitioners command premiums or churn to independents, increasing dependence risk. Medirom’s in-house training reduces but cannot eliminate scarcity, and supplier power spikes in peak seasons and tight markets.

Supplier Power 2

Landlords of high-traffic malls and stations hold leverage over Re.Ra.Ku footfall, with scarce comparable sites often pushing rents and key-money premiums roughly 15–30% in 2024; long leases and fit-out costs (commonly $80k–$200k per site) raise switching frictions and sunk-cost risk, while portfolio-wide lease negotiations can trim landlord leverage, typically yielding 5–10% rent reductions.

Supplier Power 3

Equipment vendors for treatment beds and wearable components remain fragmented, keeping pricing competitive while the global wearable medical device market reached about $31 billion in 2024; however, specialized sensors, proprietary SDKs and small-batch manufacturing create dependency and supplier leverage. Component lead times often exceed 20 weeks and quality variance delays rollouts; dual-sourcing and standards adoption materially lower that risk.

Supplier Power 4

Supplier Power 4: Data and software providers exert strong leverage through platform lock-in; the public cloud market was ≈$600B in 2024 with top vendors holding ~32%/23%/11% (AWS/Azure/GCP), making migrations 6–12 months and often multi‑million dollar projects when accounting for compliance (HIPAA, SOC2) and security integrations. Volume pricing can reduce costs but feature gaps limit viable substitutes, so strategic partnerships buy roadmap influence.

- Platform lock-in: cloud market ≈$600B (2024)

- Top shares: AWS 32% / Azure 23% / GCP 11%

- Migration: 6–12 months, multi‑million enterprise spend

- Mitigation: volume pricing, strategic partnerships for roadmap access

Supplier Power 5

Training, certification bodies, and content creators heavily influence service consistency for Medirom; proprietary curricula limit supplier exposure while accreditation boosts corporate credibility, and the global corporate wellness market reached about $62 billion in 2024, widening buyer options. Standards shifts force retraining, adding measurable time and cost, so internal academies balance quality control with scalable delivery.

- Training dependency: certification bodies drive consistency

- Proprietary curricula: lowers supplier risk

- Accreditation: increases corporate adoption

- Retraining: adds time and cost

- Internal academy: control + scalability

Supplier squeeze: labor tight, rents up, wearables delays, cloud $600B

Licensed therapists, landlords, equipment and cloud providers exert moderate–high supplier power: labor tightness (Japan unemployment 2.6%, 65+ 29% in 2024) raises wages; prime retail rents +15–30%; wearable market $31B (2024) with >20-week lead times; public cloud ≈$600B (2024) dominated by AWS 32%/Azure 23%/GCP 11%.

| Supplier | Key metric (2024) |

|---|---|

| Labor | Unemp 2.6% / 65+ 29% |

| Landlords | Rents +15–30% |

| Cloud | $600B; AWS32%/AZ23%/GCP11% |

What is included in the product

Tailored Porter's Five Forces analysis for Medirom uncovering key drivers of competition, buyer and supplier power, substitutes and new-entry risks, and identifying disruptive threats and protective market dynamics—delivered in a fully editable Word format for investor materials, strategy decks, or academic use.

Medirom's Porter's Five Forces delivers a clear, one-sheet summary of competitive pressures—perfect for quick decision-making and slide-ready insights.

Customers Bargaining Power

Buyer Power 1

Individual retail clients face low switching costs among neighborhood relaxation studios; BrightLocal 2024 found 87% of consumers consult online reviews for local services, amplifying bargaining power. Price transparency via booking apps and review platforms increases comparison shopping. Promotions and packages are expected to drive repeat visits, so differentiation through superior service quality and loyalty programs is vital.

Buyer Power 2

Corporate wellness clients commonly negotiate volume discounts of 10–25% and tailored programs, leveraging bundling and multi-vendor comparisons to increase bargaining power. Contract durations of 12–36 months and outcome KPIs (absenteeism, HRI reductions) create margin pressure. Demonstrated ROI (often cited near 3:1) and detailed data reporting shift discussions from price to outcomes, reducing pure price sensitivity.

Buyer Power 3

Buyer Power 3: Medirom users benchmark against global health-tech leaders as the digital health market reached about $260 billion in 2024; feature parity, UX quality and ecosystem compatibility drive willingness to pay. With average 30‑day retention near 15%, churn risk is high absent unique clinical insights or seamless services integration. Bundling studio benefits with digital offerings can raise switching costs and lock in value.

Buyer Power 4

Peak-time congestion turns scheduling into a commodity decision; 2024 data indicate customers defect to alternatives as wait times rise, increasing buyer leverage. Dynamic pricing can smooth demand but in 2024 sparked fairness concerns and churn in sensitive segments. Capacity planning directly affects perceived value and retention.

- High wait sensitivity — customers switch when delays grow

- Dynamic pricing trade-off — revenue vs fairness risk

- Capacity = perceived value

Buyer Power 5

Enterprise and insurer partnerships can steer large user bases, concentrating buyer power and enabling volume-driven pricing pressure; procurement increasingly demands HIPAA, SOC 2 and ISO 27001 compliance and robust data governance. Multi-year contracts commonly exchange lower margins for revenue visibility, while peer-reviewed case studies and clinical evidence materially strengthen negotiation leverage.

- Buyer concentration: enterprise/insurer deals drive scale

- Compliance: HIPAA, SOC 2, ISO 27001

- Contracting: multi-year = margin for stability

- Evidence: clinical studies boost negotiating position

Review-driven retail churn (15% 30-day) vs enterprise ROI/compliance — UX and integrations decide

Retail customers exhibit high price transparency and low switching costs; 87% consult reviews and 30-day retention is ~15% (2024), raising churn risk.

Corporate buyers secure 10–25% volume discounts, 12–36 month contracts and demand ROI (~3:1) and compliance (HIPAA, SOC 2, ISO 27001).

Market parity (digital health ~$260B in 2024) means feature, UX and integration drive willingness to pay.

| Metric | 2024 Value |

|---|---|

| Reviews Consulted | 87% |

| 30-day Retention | ~15% |

| Corporate Discounts | 10–25% |

| Digital Health Market | $260B |

Same Document Delivered

Medirom Porter's Five Forces Analysis

This preview shows the exact Medirom Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the same final file that will be available to you instantly after payment.

Original: $10.00

-65%$10.00

$3.50Description

Don't Miss the Bigger Picture

Medirom faces moderate supplier power, discerning buyers, regulatory hurdles, potential new entrants in digital health, and substitution risks from telemedicine platforms. This snapshot highlights competitive intensity, pricing pressure, and strategic levers but omits detailed metrics and force-by-force ratings. Unlock the full Porter's Five Forces Analysis to explore Medirom’s competitive dynamics, market pressures, and strategic advantages in detail.

Suppliers Bargaining Power

Supplier Power 1

Licensed therapists are a core input; Japan’s tight labor market (unemployment ~2.6% in 2024) and aging population (65+ ~29% in 2024) elevate wage demands and scheduling constraints. In urban centers experienced practitioners command premiums or churn to independents, increasing dependence risk. Medirom’s in-house training reduces but cannot eliminate scarcity, and supplier power spikes in peak seasons and tight markets.

Supplier Power 2

Landlords of high-traffic malls and stations hold leverage over Re.Ra.Ku footfall, with scarce comparable sites often pushing rents and key-money premiums roughly 15–30% in 2024; long leases and fit-out costs (commonly $80k–$200k per site) raise switching frictions and sunk-cost risk, while portfolio-wide lease negotiations can trim landlord leverage, typically yielding 5–10% rent reductions.

Supplier Power 3

Equipment vendors for treatment beds and wearable components remain fragmented, keeping pricing competitive while the global wearable medical device market reached about $31 billion in 2024; however, specialized sensors, proprietary SDKs and small-batch manufacturing create dependency and supplier leverage. Component lead times often exceed 20 weeks and quality variance delays rollouts; dual-sourcing and standards adoption materially lower that risk.

Supplier Power 4

Supplier Power 4: Data and software providers exert strong leverage through platform lock-in; the public cloud market was ≈$600B in 2024 with top vendors holding ~32%/23%/11% (AWS/Azure/GCP), making migrations 6–12 months and often multi‑million dollar projects when accounting for compliance (HIPAA, SOC2) and security integrations. Volume pricing can reduce costs but feature gaps limit viable substitutes, so strategic partnerships buy roadmap influence.

- Platform lock-in: cloud market ≈$600B (2024)

- Top shares: AWS 32% / Azure 23% / GCP 11%

- Migration: 6–12 months, multi‑million enterprise spend

- Mitigation: volume pricing, strategic partnerships for roadmap access

Supplier Power 5

Training, certification bodies, and content creators heavily influence service consistency for Medirom; proprietary curricula limit supplier exposure while accreditation boosts corporate credibility, and the global corporate wellness market reached about $62 billion in 2024, widening buyer options. Standards shifts force retraining, adding measurable time and cost, so internal academies balance quality control with scalable delivery.

- Training dependency: certification bodies drive consistency

- Proprietary curricula: lowers supplier risk

- Accreditation: increases corporate adoption

- Retraining: adds time and cost

- Internal academy: control + scalability

Supplier squeeze: labor tight, rents up, wearables delays, cloud $600B

Licensed therapists, landlords, equipment and cloud providers exert moderate–high supplier power: labor tightness (Japan unemployment 2.6%, 65+ 29% in 2024) raises wages; prime retail rents +15–30%; wearable market $31B (2024) with >20-week lead times; public cloud ≈$600B (2024) dominated by AWS 32%/Azure 23%/GCP 11%.

| Supplier | Key metric (2024) |

|---|---|

| Labor | Unemp 2.6% / 65+ 29% |

| Landlords | Rents +15–30% |

| Cloud | $600B; AWS32%/AZ23%/GCP11% |

What is included in the product

Tailored Porter's Five Forces analysis for Medirom uncovering key drivers of competition, buyer and supplier power, substitutes and new-entry risks, and identifying disruptive threats and protective market dynamics—delivered in a fully editable Word format for investor materials, strategy decks, or academic use.

Medirom's Porter's Five Forces delivers a clear, one-sheet summary of competitive pressures—perfect for quick decision-making and slide-ready insights.

Customers Bargaining Power

Buyer Power 1

Individual retail clients face low switching costs among neighborhood relaxation studios; BrightLocal 2024 found 87% of consumers consult online reviews for local services, amplifying bargaining power. Price transparency via booking apps and review platforms increases comparison shopping. Promotions and packages are expected to drive repeat visits, so differentiation through superior service quality and loyalty programs is vital.

Buyer Power 2

Corporate wellness clients commonly negotiate volume discounts of 10–25% and tailored programs, leveraging bundling and multi-vendor comparisons to increase bargaining power. Contract durations of 12–36 months and outcome KPIs (absenteeism, HRI reductions) create margin pressure. Demonstrated ROI (often cited near 3:1) and detailed data reporting shift discussions from price to outcomes, reducing pure price sensitivity.

Buyer Power 3

Buyer Power 3: Medirom users benchmark against global health-tech leaders as the digital health market reached about $260 billion in 2024; feature parity, UX quality and ecosystem compatibility drive willingness to pay. With average 30‑day retention near 15%, churn risk is high absent unique clinical insights or seamless services integration. Bundling studio benefits with digital offerings can raise switching costs and lock in value.

Buyer Power 4

Peak-time congestion turns scheduling into a commodity decision; 2024 data indicate customers defect to alternatives as wait times rise, increasing buyer leverage. Dynamic pricing can smooth demand but in 2024 sparked fairness concerns and churn in sensitive segments. Capacity planning directly affects perceived value and retention.

- High wait sensitivity — customers switch when delays grow

- Dynamic pricing trade-off — revenue vs fairness risk

- Capacity = perceived value

Buyer Power 5

Enterprise and insurer partnerships can steer large user bases, concentrating buyer power and enabling volume-driven pricing pressure; procurement increasingly demands HIPAA, SOC 2 and ISO 27001 compliance and robust data governance. Multi-year contracts commonly exchange lower margins for revenue visibility, while peer-reviewed case studies and clinical evidence materially strengthen negotiation leverage.

- Buyer concentration: enterprise/insurer deals drive scale

- Compliance: HIPAA, SOC 2, ISO 27001

- Contracting: multi-year = margin for stability

- Evidence: clinical studies boost negotiating position

Review-driven retail churn (15% 30-day) vs enterprise ROI/compliance — UX and integrations decide

Retail customers exhibit high price transparency and low switching costs; 87% consult reviews and 30-day retention is ~15% (2024), raising churn risk.

Corporate buyers secure 10–25% volume discounts, 12–36 month contracts and demand ROI (~3:1) and compliance (HIPAA, SOC 2, ISO 27001).

Market parity (digital health ~$260B in 2024) means feature, UX and integration drive willingness to pay.

| Metric | 2024 Value |

|---|---|

| Reviews Consulted | 87% |

| 30-day Retention | ~15% |

| Corporate Discounts | 10–25% |

| Digital Health Market | $260B |

Same Document Delivered

Medirom Porter's Five Forces Analysis

This preview shows the exact Medirom Porter's Five Forces Analysis you'll receive immediately after purchase—no surprises or placeholders. The document displayed here is fully formatted, professionally written, and ready for download and use the moment you buy. You're viewing the same final file that will be available to you instantly after payment.