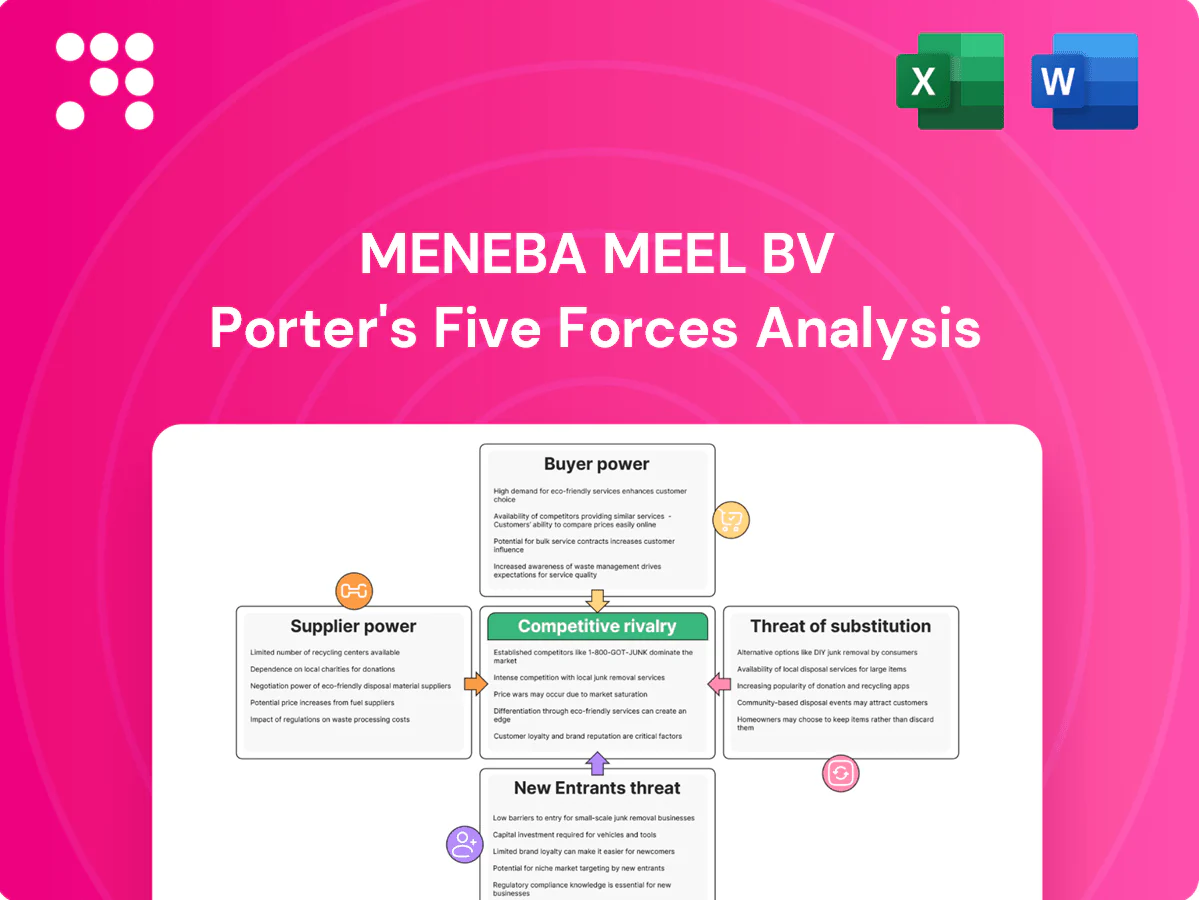

Meneba Meel BV Porter's Five Forces Analysis

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Meneba Meel BV faces moderate supplier leverage, stable buyer demand, and niche rivalry shaped by scale and distribution—yet potential substitutes and regulatory shifts could alter margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Meneba Meel BV’s competitive dynamics, market pressures, and strategic advantages in detail. Get the consultant-grade report with visuals, force ratings, and actionable implications.

Suppliers Bargaining Power

Concentrated grain merchants

European wheat sourcing mixes farmers and a handful of large traders; the four largest global grain merchants still control roughly 60% of grain trade, giving merchants leverage over price and contract terms. In tight 2024 harvests traders prioritized higher‑paying export channels, compressing EU milling margins unless costs were passed through quickly. Hedging reduces but does not remove exposure to short‑term supply squeezes.

Agri-commodity volatility

Weather, geopolitics and freight drove sharp wheat basis and futures swings in 2024 (CBOT wheat averaged about 8.25 USD/bu), reducing input cost predictability and boosting supplier leverage during tight supply windows. Volatility strengthened supplier bargaining power, especially when regional shortages pushed basis premiums over 15–25%. Mills must deploy robust risk management and diversify origins; basis contracts and long-dated cover help stabilize costs.

Quality spec constraints

Flour functionality depends on protein (commonly 8–14%), falling number (industry target often >250 s) and ash (typically 0.40–0.70%), constraining acceptable wheat sources. Narrow specs reduce supplier optionality and increase dependence on origins that meet these parameters, raising bargaining power of qualified suppliers. Blending of lots can widen flexibility but cannot fully substitute for consistently compliant origin-specific traits.

Energy and packaging inputs

Milling is energy intensive and reliant on bags/bulk packaging, giving utilities and converters bargaining power over Meneba Meel BV. Price spikes in gas, electricity and paper/plastics compress margins; IEA noted 2024 gas prices eased from 2022–23 peaks but volatility persists. Long-term supply contracts and efficiency/cogeneration investments temper supplier influence, while demand response adds flexibility.

- Energy dependency: high

- Packaging: bags/bulk critical

- 2024 trend: gas eased but volatile (IEA)

- Mitigants: long-term contracts, efficiency, cogeneration, demand response

Switching costs moderate

Meneba can switch among approved farmers, traders and logistics providers, keeping competitive tension; approved supplier pool exceeded 100 in 2024. Qualifying new suppliers requires technical testing and audits, typically taking 3–6 months and costing €10k–€40k per supplier, which tempers but does not eliminate supplier power. Multi-sourcing strategies remain key.

- Approved suppliers: >100 (2024)

- Qualification time: 3–6 months

- Qualification cost: €10k–€40k

- Mitigation: multi-sourcing

Grain suppliers hold moderate-high leverage: top-4 ~60% market, basis spikes 15-25%

Suppliers wield moderate-high power: four grain merchants control ~60% of trade and 2024 CBOT wheat averaged 8.25 USD/bu, with basis spikes of 15–25% in tight windows. Quality specs (protein 8–14%, falling number >250 s, ash 0.40–0.70%) limit source flexibility. Meneba’s approved pool >100 mitigates risk but qualification takes 3–6 months (€10k–€40k). Energy and packaging add extra supplier leverage.

| Metric | 2024 Value |

|---|---|

| Top-4 market share | ~60% |

| CBOT wheat | 8.25 USD/bu |

| Basis premium | 15–25% |

| Approved suppliers | >100 |

| Qualify time/cost | 3–6 months / €10k–€40k |

What is included in the product

Tailored Porter's Five Forces analysis for Meneba Meel BV, uncovering competitive drivers, supplier and buyer power, threat of new entrants and substitutes, and disruptive forces that affect pricing, profitability and market share, with strategic commentary and editable format for reports.

A concise one-sheet Porter's Five Forces for Meneba Meel BV—quick strategic clarity with adjustable pressure levels, instant spider/radar visualization for scenario planning, clean deck-ready layout, no macros, easy data swaps, and seamless Excel/Word integration to relieve analysis bottlenecks.

Customers Bargaining Power

Large industrial baker leverage

Large industrial bakers and food processors run frequent tenders in 2024, buying high volumes and extracting price and service concessions, often via 12-month contract awards; dual-sourcing is common, increasing buyer leverage. Contractual indexation helps balance commodity volatility but buyers still push for tight spreads and service-level penalties, which compress supplier margins.

Price sensitivity on commoditized SKUs

Standard bread and all-purpose flours are highly commoditized with low differentiation, driving frequent buyer comparisons of landed cost across millers. In 2024 EU soft wheat averaged about €230/tonne, keeping milling margins compressed to low single digits and heightening buyer power. This price sensitivity limits Meneba Meel BV’s margin on core SKUs. Offering value-add blends and technical support reduces pure price focus and recaptures margin.

Switching costs manageable

While reformulation trials and approvals are required, many buyers can switch mills within weeks, so in 2024 this credible threat keeps pricing keen and margins under pressure. Long-standing relationships and consistent on-time performance raise perceived switching costs for key accounts. Certifications (eg HACCP, GMP) and joint R&D projects deepen customer stickiness and reduce churn risk.

Demand for technical support

Buyers prioritize application support, process troubleshooting, and consistent bake performance, and suppliers that resolve yield and quality issues secure premium terms and longer contracts, reducing pure price sensitivity. Onsite trials and transparent data sharing strengthen switching costs and buyer-supplier ties, raising retention and enabling service-based margins.

Private label and contract specs

Retail private label and QSR contract specs drive heavy audits and traceability; private label represented roughly 30% of EU grocery sales in 2024 (Kantar), shifting negotiating power to buyers who can delist fast yet awarding suppliers volume stability when awarded programs.

- Compliance raises supplier costs and risks

- Winning programs = stable volumes

- Balanced SLAs and indexation clauses mitigate margin squeeze

12‑month tenders, dual‑sourcing squeeze milling margins; soft wheat €230/tonne, private label ~30%

Buyers exert high leverage via frequent 12‑month tenders and dual‑sourcing, compressing milling margins to low single digits. EU soft wheat averaged about €230/tonne in 2024 and private label was ~30% of grocery sales, increasing price sensitivity. Value‑add blends, technical support and certifications raise switching costs and secure better terms.

| Metric | 2024 |

|---|---|

| EU soft wheat | €230/tonne |

| Private label share | ~30% |

| Milling margins | Low single digits |

| Typical contract | 12 months |

What You See Is What You Get

Meneba Meel BV Porter's Five Forces Analysis

This preview shows the exact Meneba Meel BV Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and free of placeholders. The document displayed here is the full, ready-to-use deliverable, identical to the download you'll get at checkout. No mockups or samples; purchase grants instant access to this exact file.

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Meneba Meel BV faces moderate supplier leverage, stable buyer demand, and niche rivalry shaped by scale and distribution—yet potential substitutes and regulatory shifts could alter margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Meneba Meel BV’s competitive dynamics, market pressures, and strategic advantages in detail. Get the consultant-grade report with visuals, force ratings, and actionable implications.

Suppliers Bargaining Power

Concentrated grain merchants

European wheat sourcing mixes farmers and a handful of large traders; the four largest global grain merchants still control roughly 60% of grain trade, giving merchants leverage over price and contract terms. In tight 2024 harvests traders prioritized higher‑paying export channels, compressing EU milling margins unless costs were passed through quickly. Hedging reduces but does not remove exposure to short‑term supply squeezes.

Agri-commodity volatility

Weather, geopolitics and freight drove sharp wheat basis and futures swings in 2024 (CBOT wheat averaged about 8.25 USD/bu), reducing input cost predictability and boosting supplier leverage during tight supply windows. Volatility strengthened supplier bargaining power, especially when regional shortages pushed basis premiums over 15–25%. Mills must deploy robust risk management and diversify origins; basis contracts and long-dated cover help stabilize costs.

Quality spec constraints

Flour functionality depends on protein (commonly 8–14%), falling number (industry target often >250 s) and ash (typically 0.40–0.70%), constraining acceptable wheat sources. Narrow specs reduce supplier optionality and increase dependence on origins that meet these parameters, raising bargaining power of qualified suppliers. Blending of lots can widen flexibility but cannot fully substitute for consistently compliant origin-specific traits.

Energy and packaging inputs

Milling is energy intensive and reliant on bags/bulk packaging, giving utilities and converters bargaining power over Meneba Meel BV. Price spikes in gas, electricity and paper/plastics compress margins; IEA noted 2024 gas prices eased from 2022–23 peaks but volatility persists. Long-term supply contracts and efficiency/cogeneration investments temper supplier influence, while demand response adds flexibility.

- Energy dependency: high

- Packaging: bags/bulk critical

- 2024 trend: gas eased but volatile (IEA)

- Mitigants: long-term contracts, efficiency, cogeneration, demand response

Switching costs moderate

Meneba can switch among approved farmers, traders and logistics providers, keeping competitive tension; approved supplier pool exceeded 100 in 2024. Qualifying new suppliers requires technical testing and audits, typically taking 3–6 months and costing €10k–€40k per supplier, which tempers but does not eliminate supplier power. Multi-sourcing strategies remain key.

- Approved suppliers: >100 (2024)

- Qualification time: 3–6 months

- Qualification cost: €10k–€40k

- Mitigation: multi-sourcing

Grain suppliers hold moderate-high leverage: top-4 ~60% market, basis spikes 15-25%

Suppliers wield moderate-high power: four grain merchants control ~60% of trade and 2024 CBOT wheat averaged 8.25 USD/bu, with basis spikes of 15–25% in tight windows. Quality specs (protein 8–14%, falling number >250 s, ash 0.40–0.70%) limit source flexibility. Meneba’s approved pool >100 mitigates risk but qualification takes 3–6 months (€10k–€40k). Energy and packaging add extra supplier leverage.

| Metric | 2024 Value |

|---|---|

| Top-4 market share | ~60% |

| CBOT wheat | 8.25 USD/bu |

| Basis premium | 15–25% |

| Approved suppliers | >100 |

| Qualify time/cost | 3–6 months / €10k–€40k |

What is included in the product

Tailored Porter's Five Forces analysis for Meneba Meel BV, uncovering competitive drivers, supplier and buyer power, threat of new entrants and substitutes, and disruptive forces that affect pricing, profitability and market share, with strategic commentary and editable format for reports.

A concise one-sheet Porter's Five Forces for Meneba Meel BV—quick strategic clarity with adjustable pressure levels, instant spider/radar visualization for scenario planning, clean deck-ready layout, no macros, easy data swaps, and seamless Excel/Word integration to relieve analysis bottlenecks.

Customers Bargaining Power

Large industrial baker leverage

Large industrial bakers and food processors run frequent tenders in 2024, buying high volumes and extracting price and service concessions, often via 12-month contract awards; dual-sourcing is common, increasing buyer leverage. Contractual indexation helps balance commodity volatility but buyers still push for tight spreads and service-level penalties, which compress supplier margins.

Price sensitivity on commoditized SKUs

Standard bread and all-purpose flours are highly commoditized with low differentiation, driving frequent buyer comparisons of landed cost across millers. In 2024 EU soft wheat averaged about €230/tonne, keeping milling margins compressed to low single digits and heightening buyer power. This price sensitivity limits Meneba Meel BV’s margin on core SKUs. Offering value-add blends and technical support reduces pure price focus and recaptures margin.

Switching costs manageable

While reformulation trials and approvals are required, many buyers can switch mills within weeks, so in 2024 this credible threat keeps pricing keen and margins under pressure. Long-standing relationships and consistent on-time performance raise perceived switching costs for key accounts. Certifications (eg HACCP, GMP) and joint R&D projects deepen customer stickiness and reduce churn risk.

Demand for technical support

Buyers prioritize application support, process troubleshooting, and consistent bake performance, and suppliers that resolve yield and quality issues secure premium terms and longer contracts, reducing pure price sensitivity. Onsite trials and transparent data sharing strengthen switching costs and buyer-supplier ties, raising retention and enabling service-based margins.

Private label and contract specs

Retail private label and QSR contract specs drive heavy audits and traceability; private label represented roughly 30% of EU grocery sales in 2024 (Kantar), shifting negotiating power to buyers who can delist fast yet awarding suppliers volume stability when awarded programs.

- Compliance raises supplier costs and risks

- Winning programs = stable volumes

- Balanced SLAs and indexation clauses mitigate margin squeeze

12‑month tenders, dual‑sourcing squeeze milling margins; soft wheat €230/tonne, private label ~30%

Buyers exert high leverage via frequent 12‑month tenders and dual‑sourcing, compressing milling margins to low single digits. EU soft wheat averaged about €230/tonne in 2024 and private label was ~30% of grocery sales, increasing price sensitivity. Value‑add blends, technical support and certifications raise switching costs and secure better terms.

| Metric | 2024 |

|---|---|

| EU soft wheat | €230/tonne |

| Private label share | ~30% |

| Milling margins | Low single digits |

| Typical contract | 12 months |

What You See Is What You Get

Meneba Meel BV Porter's Five Forces Analysis

This preview shows the exact Meneba Meel BV Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and free of placeholders. The document displayed here is the full, ready-to-use deliverable, identical to the download you'll get at checkout. No mockups or samples; purchase grants instant access to this exact file.

Original: $10.00

-65%$10.00

$3.50Description

Elevate Your Analysis with the Complete Porter's Five Forces Analysis

Meneba Meel BV faces moderate supplier leverage, stable buyer demand, and niche rivalry shaped by scale and distribution—yet potential substitutes and regulatory shifts could alter margins. This brief snapshot only scratches the surface. Unlock the full Porter's Five Forces Analysis to explore Meneba Meel BV’s competitive dynamics, market pressures, and strategic advantages in detail. Get the consultant-grade report with visuals, force ratings, and actionable implications.

Suppliers Bargaining Power

Concentrated grain merchants

European wheat sourcing mixes farmers and a handful of large traders; the four largest global grain merchants still control roughly 60% of grain trade, giving merchants leverage over price and contract terms. In tight 2024 harvests traders prioritized higher‑paying export channels, compressing EU milling margins unless costs were passed through quickly. Hedging reduces but does not remove exposure to short‑term supply squeezes.

Agri-commodity volatility

Weather, geopolitics and freight drove sharp wheat basis and futures swings in 2024 (CBOT wheat averaged about 8.25 USD/bu), reducing input cost predictability and boosting supplier leverage during tight supply windows. Volatility strengthened supplier bargaining power, especially when regional shortages pushed basis premiums over 15–25%. Mills must deploy robust risk management and diversify origins; basis contracts and long-dated cover help stabilize costs.

Quality spec constraints

Flour functionality depends on protein (commonly 8–14%), falling number (industry target often >250 s) and ash (typically 0.40–0.70%), constraining acceptable wheat sources. Narrow specs reduce supplier optionality and increase dependence on origins that meet these parameters, raising bargaining power of qualified suppliers. Blending of lots can widen flexibility but cannot fully substitute for consistently compliant origin-specific traits.

Energy and packaging inputs

Milling is energy intensive and reliant on bags/bulk packaging, giving utilities and converters bargaining power over Meneba Meel BV. Price spikes in gas, electricity and paper/plastics compress margins; IEA noted 2024 gas prices eased from 2022–23 peaks but volatility persists. Long-term supply contracts and efficiency/cogeneration investments temper supplier influence, while demand response adds flexibility.

- Energy dependency: high

- Packaging: bags/bulk critical

- 2024 trend: gas eased but volatile (IEA)

- Mitigants: long-term contracts, efficiency, cogeneration, demand response

Switching costs moderate

Meneba can switch among approved farmers, traders and logistics providers, keeping competitive tension; approved supplier pool exceeded 100 in 2024. Qualifying new suppliers requires technical testing and audits, typically taking 3–6 months and costing €10k–€40k per supplier, which tempers but does not eliminate supplier power. Multi-sourcing strategies remain key.

- Approved suppliers: >100 (2024)

- Qualification time: 3–6 months

- Qualification cost: €10k–€40k

- Mitigation: multi-sourcing

Grain suppliers hold moderate-high leverage: top-4 ~60% market, basis spikes 15-25%

Suppliers wield moderate-high power: four grain merchants control ~60% of trade and 2024 CBOT wheat averaged 8.25 USD/bu, with basis spikes of 15–25% in tight windows. Quality specs (protein 8–14%, falling number >250 s, ash 0.40–0.70%) limit source flexibility. Meneba’s approved pool >100 mitigates risk but qualification takes 3–6 months (€10k–€40k). Energy and packaging add extra supplier leverage.

| Metric | 2024 Value |

|---|---|

| Top-4 market share | ~60% |

| CBOT wheat | 8.25 USD/bu |

| Basis premium | 15–25% |

| Approved suppliers | >100 |

| Qualify time/cost | 3–6 months / €10k–€40k |

What is included in the product

Tailored Porter's Five Forces analysis for Meneba Meel BV, uncovering competitive drivers, supplier and buyer power, threat of new entrants and substitutes, and disruptive forces that affect pricing, profitability and market share, with strategic commentary and editable format for reports.

A concise one-sheet Porter's Five Forces for Meneba Meel BV—quick strategic clarity with adjustable pressure levels, instant spider/radar visualization for scenario planning, clean deck-ready layout, no macros, easy data swaps, and seamless Excel/Word integration to relieve analysis bottlenecks.

Customers Bargaining Power

Large industrial baker leverage

Large industrial bakers and food processors run frequent tenders in 2024, buying high volumes and extracting price and service concessions, often via 12-month contract awards; dual-sourcing is common, increasing buyer leverage. Contractual indexation helps balance commodity volatility but buyers still push for tight spreads and service-level penalties, which compress supplier margins.

Price sensitivity on commoditized SKUs

Standard bread and all-purpose flours are highly commoditized with low differentiation, driving frequent buyer comparisons of landed cost across millers. In 2024 EU soft wheat averaged about €230/tonne, keeping milling margins compressed to low single digits and heightening buyer power. This price sensitivity limits Meneba Meel BV’s margin on core SKUs. Offering value-add blends and technical support reduces pure price focus and recaptures margin.

Switching costs manageable

While reformulation trials and approvals are required, many buyers can switch mills within weeks, so in 2024 this credible threat keeps pricing keen and margins under pressure. Long-standing relationships and consistent on-time performance raise perceived switching costs for key accounts. Certifications (eg HACCP, GMP) and joint R&D projects deepen customer stickiness and reduce churn risk.

Demand for technical support

Buyers prioritize application support, process troubleshooting, and consistent bake performance, and suppliers that resolve yield and quality issues secure premium terms and longer contracts, reducing pure price sensitivity. Onsite trials and transparent data sharing strengthen switching costs and buyer-supplier ties, raising retention and enabling service-based margins.

Private label and contract specs

Retail private label and QSR contract specs drive heavy audits and traceability; private label represented roughly 30% of EU grocery sales in 2024 (Kantar), shifting negotiating power to buyers who can delist fast yet awarding suppliers volume stability when awarded programs.

- Compliance raises supplier costs and risks

- Winning programs = stable volumes

- Balanced SLAs and indexation clauses mitigate margin squeeze

12‑month tenders, dual‑sourcing squeeze milling margins; soft wheat €230/tonne, private label ~30%

Buyers exert high leverage via frequent 12‑month tenders and dual‑sourcing, compressing milling margins to low single digits. EU soft wheat averaged about €230/tonne in 2024 and private label was ~30% of grocery sales, increasing price sensitivity. Value‑add blends, technical support and certifications raise switching costs and secure better terms.

| Metric | 2024 |

|---|---|

| EU soft wheat | €230/tonne |

| Private label share | ~30% |

| Milling margins | Low single digits |

| Typical contract | 12 months |

What You See Is What You Get

Meneba Meel BV Porter's Five Forces Analysis

This preview shows the exact Meneba Meel BV Porter's Five Forces Analysis you'll receive immediately after purchase—fully formatted, professionally written, and free of placeholders. The document displayed here is the full, ready-to-use deliverable, identical to the download you'll get at checkout. No mockups or samples; purchase grants instant access to this exact file.