China Mengniu Dairy Porter's Five Forces Analysis

From Overview to Strategy Blueprint

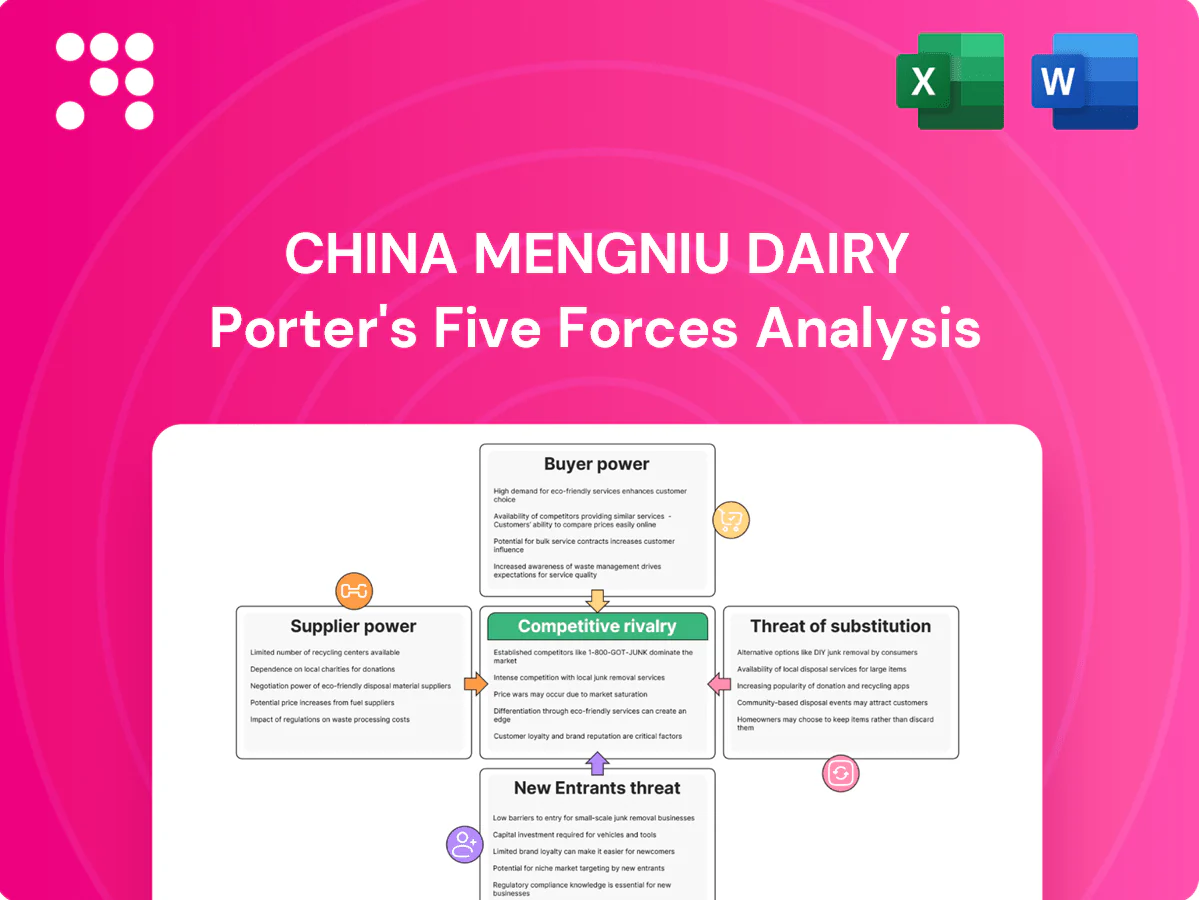

China Mengniu Dairy faces intense rivalry from local and international dairy players, evolving consumer preferences, and rising input costs, while buyer power grows with retail consolidation and private-label expansion. Brand strength and distribution scale mitigate supplier and entrant threats, but substitutes and regulatory shifts remain material. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Mengniu’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Concentrated raw milk sourcing

Raw milk is Mengniu's critical input and sourcing is regionally concentrated, with the company reporting over 40% of supply tied to key northern provinces, giving large farm clusters localized bargaining clout. Seasonal swings and disease outbreaks drove spot raw milk prices up around 15% in 2023, tightening supply and lifting costs. Mengniu mitigates this via diversified sourcing bases and upstream partnerships and owns a significant upstream farm network, but persistent supply tightness can still pressure margins.

Farmer contracts and integration

Long-term contracts with technical support and financing stabilize volumes and reduce opportunism, supporting Mengniu's ~24% China market share in 2024; backward integration into ranches improves quality and traceability, tempering supplier leverage. Switching costs for high-quality herds remain high, while rising compliance and animal welfare standards increase supplier costs and limit alternative sourcing.

Packaging and inputs dependency

Packaging and inputs—Tetra Pak/aseptic cartons, PET, sugar, starter cultures and specialty additives—come from specialized vendors, and strict technical and food‑safety specs narrow approved supplier lists, giving qualified suppliers moderate bargaining power; Mengniu (HKEX:2319) leverages scale for price negotiation and dual‑sourcing, but commodity price swings still flow through to COGS.

Cold-chain logistics partners

Refrigerated transport and cold storage are essential for Mengniu to preserve freshness and safety; peak seasons push third-party rates up roughly 20%, giving national 3PLs modest leverage in 2024. Mengniu’s scale, partial in-house fleets and growing network density reduce dependency, while route optimization and consolidation lower supplier power over time.

- Essentiality: high

- Peak-rate impact: ~20%

- Mitigation: in-house fleets, route optimization

Global dairy commodity volatility

Skim/whole milk powder and whey prices swing with global supply-demand and trade policy; 2024 saw renewed volatility as export restrictions and shipping disruptions tightened supplies. Import options diversify suppliers for Mengniu but add FX and tariff exposure that raised landed costs in 2024. Hedging and inventory buffering reduce risk but are imperfect; price spikes can compress margins before retail prices adjust.

- 2024 volatility: higher supply-risk from export measures

- Importing: increases FX/tariff cost exposure

- Mitigants: hedging/inventory but imperfect

North-heavy supply (>40%) and integration defend ~24%

Mengniu relies on regionally concentrated raw milk (>40% from northern provinces) giving local farms bargaining clout; 2023 spot milk rose ~15%, and 2024 supply volatility remained elevated. Backward integration and long‑term contracts support its ~24% China market share (2024) but switching costs for quality herds stay high. Packaging, powders and cold‑chain suppliers hold moderate leverage; peak transport uplifts ~20%.

| Metric | Value |

|---|---|

| Raw milk concentration | >40% |

| China market share (2024) | ~24% |

| Peak transport impact | ~20% |

What is included in the product

Tailored Porter's Five Forces analysis for China Mengniu Dairy that uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and market barriers shaping pricing, margins, and strategic opportunities.

A single-sheet Porter’s Five Forces analysis for China Mengniu—quickly spot competitive pressures, regulatory risks, supplier bargaining shifts and consumer trends to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Modern retail and e-commerce clout

National chains and leading platforms command shelf space and traffic, extracting rebates and promotions; China online retail sales of physical goods reached RMB 13.8 trillion in 2023, with Alibaba/Tmall holding ~55–60% share and Pinduoduo ~20–25%. Data-sharing and search-ranking algorithms amplify their bargaining power. Mengniu routinely trades tougher terms for visibility and volume on key listings. Rising private-label penetration in select categories further intensifies margin pressures.

Low switching costs for consumers

Functional parity across mainstream SKUs makes swapping brands easy, pressuring margins for Mengniu despite its roughly 20% share of China’s liquid milk market (2024). Frequent promotions normalize price-led switching and erode loyalty. Taste and packaging innovation can defend share but require constant refresh and R&D spend. Trust from consistent quality and safety records remains the primary stickiness lever.

Premium niches dilute price pressure

Premium niches such as probiotic, high-protein, organic and children’s formulas exhibit lower price elasticity as buyers prioritize efficacy, safety and brand over price, softening customer bargaining power. Credentials and clinical backing—third-party certifications and published trials—drive willingness to pay and lower churn. Mengniu’s strategic shift toward higher-margin premium SKUs helps offset mainstream price pressure. Retailers retain influence but face constrained leverage in these specialty segments.

Digital reviews and social influence

Online ratings and KOL-driven content commerce rapidly sway Chinese dairy choice, with live‑commerce GMV surpassing RMB 1 trillion by 2024 and KOLs delivering double‑digit uplifts in category sales; visible complaints amplify buyer leverage via reputational risk. Rapid feedback loops force Mengniu into faster product tweaks and service recovery, while analytics let it preempt churn and tailor offers.

- Online ratings: drive discovery and trust

- KOLs: double‑digit sales uplift

- Visibility: increases reputational risk

- Analytics: preempt churn, personalize offers

Institutional and channel diversity

Institutional and channel diversity—convenience stores, schools and foodservice—gives buyers varied procurement terms, reducing uniform leverage over China Mengniu Dairy.

Outside top retailers the channel base is fragmented, so average buyer bargaining power falls; Mengniu benefits from scale as a top-two player with roughly 20% liquid-milk market share in 2023.

Control of route-to-market through distributors and direct sales strengthens Mengniu's negotiation stance, while whether a SKU is a traffic driver or margin builder determines price flexibility.

- Convenience stores: tailored terms

- Schools/foodservice: contract-based stability

- Fragmentation lowers buyer leverage

- Route-to-market control = stronger pricing

- Category role shapes discounting

Buyers wield leverage; online retail RMB13.8trn, platforms 55–60%, live commerce >RMB1tn

Buyers wield strong leverage via national chains and platforms (online retail RMB13.8trn 2023; Alibaba 55–60%, PDD 20–25%), normalized promotions and easy brand switching; Mengniu holds ~20% liquid-milk share (2024) and offsets pressure via premium SKUs and route-to-market control. Live commerce (GMV >RMB1trn by 2024) and KOLs raise reputational risk but premium segments show lower elasticity.

| Metric | Value |

|---|---|

| Mengniu liquid milk share (2024) | ~20% |

| China online retail (2023) | RMB13.8tn |

| Alibaba/Tmall | 55–60% |

| Pinduoduo | 20–25% |

| Live‑commerce GMV (2024) | >RMB1tn |

Preview Before You Purchase

China Mengniu Dairy Porter's Five Forces Analysis

This Porter's Five Forces analysis of China Mengniu Dairy provides a concise review of competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. This preview is the exact, fully formatted document you’ll receive instantly after purchase. No placeholders or samples—ready to download and use immediately.

From Overview to Strategy Blueprint

China Mengniu Dairy faces intense rivalry from local and international dairy players, evolving consumer preferences, and rising input costs, while buyer power grows with retail consolidation and private-label expansion. Brand strength and distribution scale mitigate supplier and entrant threats, but substitutes and regulatory shifts remain material. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Mengniu’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Concentrated raw milk sourcing

Raw milk is Mengniu's critical input and sourcing is regionally concentrated, with the company reporting over 40% of supply tied to key northern provinces, giving large farm clusters localized bargaining clout. Seasonal swings and disease outbreaks drove spot raw milk prices up around 15% in 2023, tightening supply and lifting costs. Mengniu mitigates this via diversified sourcing bases and upstream partnerships and owns a significant upstream farm network, but persistent supply tightness can still pressure margins.

Farmer contracts and integration

Long-term contracts with technical support and financing stabilize volumes and reduce opportunism, supporting Mengniu's ~24% China market share in 2024; backward integration into ranches improves quality and traceability, tempering supplier leverage. Switching costs for high-quality herds remain high, while rising compliance and animal welfare standards increase supplier costs and limit alternative sourcing.

Packaging and inputs dependency

Packaging and inputs—Tetra Pak/aseptic cartons, PET, sugar, starter cultures and specialty additives—come from specialized vendors, and strict technical and food‑safety specs narrow approved supplier lists, giving qualified suppliers moderate bargaining power; Mengniu (HKEX:2319) leverages scale for price negotiation and dual‑sourcing, but commodity price swings still flow through to COGS.

Cold-chain logistics partners

Refrigerated transport and cold storage are essential for Mengniu to preserve freshness and safety; peak seasons push third-party rates up roughly 20%, giving national 3PLs modest leverage in 2024. Mengniu’s scale, partial in-house fleets and growing network density reduce dependency, while route optimization and consolidation lower supplier power over time.

- Essentiality: high

- Peak-rate impact: ~20%

- Mitigation: in-house fleets, route optimization

Global dairy commodity volatility

Skim/whole milk powder and whey prices swing with global supply-demand and trade policy; 2024 saw renewed volatility as export restrictions and shipping disruptions tightened supplies. Import options diversify suppliers for Mengniu but add FX and tariff exposure that raised landed costs in 2024. Hedging and inventory buffering reduce risk but are imperfect; price spikes can compress margins before retail prices adjust.

- 2024 volatility: higher supply-risk from export measures

- Importing: increases FX/tariff cost exposure

- Mitigants: hedging/inventory but imperfect

North-heavy supply (>40%) and integration defend ~24%

Mengniu relies on regionally concentrated raw milk (>40% from northern provinces) giving local farms bargaining clout; 2023 spot milk rose ~15%, and 2024 supply volatility remained elevated. Backward integration and long‑term contracts support its ~24% China market share (2024) but switching costs for quality herds stay high. Packaging, powders and cold‑chain suppliers hold moderate leverage; peak transport uplifts ~20%.

| Metric | Value |

|---|---|

| Raw milk concentration | >40% |

| China market share (2024) | ~24% |

| Peak transport impact | ~20% |

What is included in the product

Tailored Porter's Five Forces analysis for China Mengniu Dairy that uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and market barriers shaping pricing, margins, and strategic opportunities.

A single-sheet Porter’s Five Forces analysis for China Mengniu—quickly spot competitive pressures, regulatory risks, supplier bargaining shifts and consumer trends to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Modern retail and e-commerce clout

National chains and leading platforms command shelf space and traffic, extracting rebates and promotions; China online retail sales of physical goods reached RMB 13.8 trillion in 2023, with Alibaba/Tmall holding ~55–60% share and Pinduoduo ~20–25%. Data-sharing and search-ranking algorithms amplify their bargaining power. Mengniu routinely trades tougher terms for visibility and volume on key listings. Rising private-label penetration in select categories further intensifies margin pressures.

Low switching costs for consumers

Functional parity across mainstream SKUs makes swapping brands easy, pressuring margins for Mengniu despite its roughly 20% share of China’s liquid milk market (2024). Frequent promotions normalize price-led switching and erode loyalty. Taste and packaging innovation can defend share but require constant refresh and R&D spend. Trust from consistent quality and safety records remains the primary stickiness lever.

Premium niches dilute price pressure

Premium niches such as probiotic, high-protein, organic and children’s formulas exhibit lower price elasticity as buyers prioritize efficacy, safety and brand over price, softening customer bargaining power. Credentials and clinical backing—third-party certifications and published trials—drive willingness to pay and lower churn. Mengniu’s strategic shift toward higher-margin premium SKUs helps offset mainstream price pressure. Retailers retain influence but face constrained leverage in these specialty segments.

Digital reviews and social influence

Online ratings and KOL-driven content commerce rapidly sway Chinese dairy choice, with live‑commerce GMV surpassing RMB 1 trillion by 2024 and KOLs delivering double‑digit uplifts in category sales; visible complaints amplify buyer leverage via reputational risk. Rapid feedback loops force Mengniu into faster product tweaks and service recovery, while analytics let it preempt churn and tailor offers.

- Online ratings: drive discovery and trust

- KOLs: double‑digit sales uplift

- Visibility: increases reputational risk

- Analytics: preempt churn, personalize offers

Institutional and channel diversity

Institutional and channel diversity—convenience stores, schools and foodservice—gives buyers varied procurement terms, reducing uniform leverage over China Mengniu Dairy.

Outside top retailers the channel base is fragmented, so average buyer bargaining power falls; Mengniu benefits from scale as a top-two player with roughly 20% liquid-milk market share in 2023.

Control of route-to-market through distributors and direct sales strengthens Mengniu's negotiation stance, while whether a SKU is a traffic driver or margin builder determines price flexibility.

- Convenience stores: tailored terms

- Schools/foodservice: contract-based stability

- Fragmentation lowers buyer leverage

- Route-to-market control = stronger pricing

- Category role shapes discounting

Buyers wield leverage; online retail RMB13.8trn, platforms 55–60%, live commerce >RMB1tn

Buyers wield strong leverage via national chains and platforms (online retail RMB13.8trn 2023; Alibaba 55–60%, PDD 20–25%), normalized promotions and easy brand switching; Mengniu holds ~20% liquid-milk share (2024) and offsets pressure via premium SKUs and route-to-market control. Live commerce (GMV >RMB1trn by 2024) and KOLs raise reputational risk but premium segments show lower elasticity.

| Metric | Value |

|---|---|

| Mengniu liquid milk share (2024) | ~20% |

| China online retail (2023) | RMB13.8tn |

| Alibaba/Tmall | 55–60% |

| Pinduoduo | 20–25% |

| Live‑commerce GMV (2024) | >RMB1tn |

Preview Before You Purchase

China Mengniu Dairy Porter's Five Forces Analysis

This Porter's Five Forces analysis of China Mengniu Dairy provides a concise review of competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. This preview is the exact, fully formatted document you’ll receive instantly after purchase. No placeholders or samples—ready to download and use immediately.

Original: $10.00

-65%$10.00

$3.50Description

From Overview to Strategy Blueprint

China Mengniu Dairy faces intense rivalry from local and international dairy players, evolving consumer preferences, and rising input costs, while buyer power grows with retail consolidation and private-label expansion. Brand strength and distribution scale mitigate supplier and entrant threats, but substitutes and regulatory shifts remain material. This brief snapshot only scratches the surface—unlock the full Porter's Five Forces Analysis to explore Mengniu’s competitive dynamics and strategic levers in detail.

Suppliers Bargaining Power

Concentrated raw milk sourcing

Raw milk is Mengniu's critical input and sourcing is regionally concentrated, with the company reporting over 40% of supply tied to key northern provinces, giving large farm clusters localized bargaining clout. Seasonal swings and disease outbreaks drove spot raw milk prices up around 15% in 2023, tightening supply and lifting costs. Mengniu mitigates this via diversified sourcing bases and upstream partnerships and owns a significant upstream farm network, but persistent supply tightness can still pressure margins.

Farmer contracts and integration

Long-term contracts with technical support and financing stabilize volumes and reduce opportunism, supporting Mengniu's ~24% China market share in 2024; backward integration into ranches improves quality and traceability, tempering supplier leverage. Switching costs for high-quality herds remain high, while rising compliance and animal welfare standards increase supplier costs and limit alternative sourcing.

Packaging and inputs dependency

Packaging and inputs—Tetra Pak/aseptic cartons, PET, sugar, starter cultures and specialty additives—come from specialized vendors, and strict technical and food‑safety specs narrow approved supplier lists, giving qualified suppliers moderate bargaining power; Mengniu (HKEX:2319) leverages scale for price negotiation and dual‑sourcing, but commodity price swings still flow through to COGS.

Cold-chain logistics partners

Refrigerated transport and cold storage are essential for Mengniu to preserve freshness and safety; peak seasons push third-party rates up roughly 20%, giving national 3PLs modest leverage in 2024. Mengniu’s scale, partial in-house fleets and growing network density reduce dependency, while route optimization and consolidation lower supplier power over time.

- Essentiality: high

- Peak-rate impact: ~20%

- Mitigation: in-house fleets, route optimization

Global dairy commodity volatility

Skim/whole milk powder and whey prices swing with global supply-demand and trade policy; 2024 saw renewed volatility as export restrictions and shipping disruptions tightened supplies. Import options diversify suppliers for Mengniu but add FX and tariff exposure that raised landed costs in 2024. Hedging and inventory buffering reduce risk but are imperfect; price spikes can compress margins before retail prices adjust.

- 2024 volatility: higher supply-risk from export measures

- Importing: increases FX/tariff cost exposure

- Mitigants: hedging/inventory but imperfect

North-heavy supply (>40%) and integration defend ~24%

Mengniu relies on regionally concentrated raw milk (>40% from northern provinces) giving local farms bargaining clout; 2023 spot milk rose ~15%, and 2024 supply volatility remained elevated. Backward integration and long‑term contracts support its ~24% China market share (2024) but switching costs for quality herds stay high. Packaging, powders and cold‑chain suppliers hold moderate leverage; peak transport uplifts ~20%.

| Metric | Value |

|---|---|

| Raw milk concentration | >40% |

| China market share (2024) | ~24% |

| Peak transport impact | ~20% |

What is included in the product

Tailored Porter's Five Forces analysis for China Mengniu Dairy that uncovers competitive drivers, buyer and supplier power, threat of substitutes and new entrants, and identifies disruptive forces and market barriers shaping pricing, margins, and strategic opportunities.

A single-sheet Porter’s Five Forces analysis for China Mengniu—quickly spot competitive pressures, regulatory risks, supplier bargaining shifts and consumer trends to streamline strategic decisions and investor briefings.

Customers Bargaining Power

Modern retail and e-commerce clout

National chains and leading platforms command shelf space and traffic, extracting rebates and promotions; China online retail sales of physical goods reached RMB 13.8 trillion in 2023, with Alibaba/Tmall holding ~55–60% share and Pinduoduo ~20–25%. Data-sharing and search-ranking algorithms amplify their bargaining power. Mengniu routinely trades tougher terms for visibility and volume on key listings. Rising private-label penetration in select categories further intensifies margin pressures.

Low switching costs for consumers

Functional parity across mainstream SKUs makes swapping brands easy, pressuring margins for Mengniu despite its roughly 20% share of China’s liquid milk market (2024). Frequent promotions normalize price-led switching and erode loyalty. Taste and packaging innovation can defend share but require constant refresh and R&D spend. Trust from consistent quality and safety records remains the primary stickiness lever.

Premium niches dilute price pressure

Premium niches such as probiotic, high-protein, organic and children’s formulas exhibit lower price elasticity as buyers prioritize efficacy, safety and brand over price, softening customer bargaining power. Credentials and clinical backing—third-party certifications and published trials—drive willingness to pay and lower churn. Mengniu’s strategic shift toward higher-margin premium SKUs helps offset mainstream price pressure. Retailers retain influence but face constrained leverage in these specialty segments.

Digital reviews and social influence

Online ratings and KOL-driven content commerce rapidly sway Chinese dairy choice, with live‑commerce GMV surpassing RMB 1 trillion by 2024 and KOLs delivering double‑digit uplifts in category sales; visible complaints amplify buyer leverage via reputational risk. Rapid feedback loops force Mengniu into faster product tweaks and service recovery, while analytics let it preempt churn and tailor offers.

- Online ratings: drive discovery and trust

- KOLs: double‑digit sales uplift

- Visibility: increases reputational risk

- Analytics: preempt churn, personalize offers

Institutional and channel diversity

Institutional and channel diversity—convenience stores, schools and foodservice—gives buyers varied procurement terms, reducing uniform leverage over China Mengniu Dairy.

Outside top retailers the channel base is fragmented, so average buyer bargaining power falls; Mengniu benefits from scale as a top-two player with roughly 20% liquid-milk market share in 2023.

Control of route-to-market through distributors and direct sales strengthens Mengniu's negotiation stance, while whether a SKU is a traffic driver or margin builder determines price flexibility.

- Convenience stores: tailored terms

- Schools/foodservice: contract-based stability

- Fragmentation lowers buyer leverage

- Route-to-market control = stronger pricing

- Category role shapes discounting

Buyers wield leverage; online retail RMB13.8trn, platforms 55–60%, live commerce >RMB1tn

Buyers wield strong leverage via national chains and platforms (online retail RMB13.8trn 2023; Alibaba 55–60%, PDD 20–25%), normalized promotions and easy brand switching; Mengniu holds ~20% liquid-milk share (2024) and offsets pressure via premium SKUs and route-to-market control. Live commerce (GMV >RMB1trn by 2024) and KOLs raise reputational risk but premium segments show lower elasticity.

| Metric | Value |

|---|---|

| Mengniu liquid milk share (2024) | ~20% |

| China online retail (2023) | RMB13.8tn |

| Alibaba/Tmall | 55–60% |

| Pinduoduo | 20–25% |

| Live‑commerce GMV (2024) | >RMB1tn |

Preview Before You Purchase

China Mengniu Dairy Porter's Five Forces Analysis

This Porter's Five Forces analysis of China Mengniu Dairy provides a concise review of competitive rivalry, supplier and buyer power, threats of new entrants and substitutes, and strategic implications. This preview is the exact, fully formatted document you’ll receive instantly after purchase. No placeholders or samples—ready to download and use immediately.