Mercury Business Model Canvas

Unlock a Ready-to-Use Business Model Canvas for Fast Strategic Decision-Making

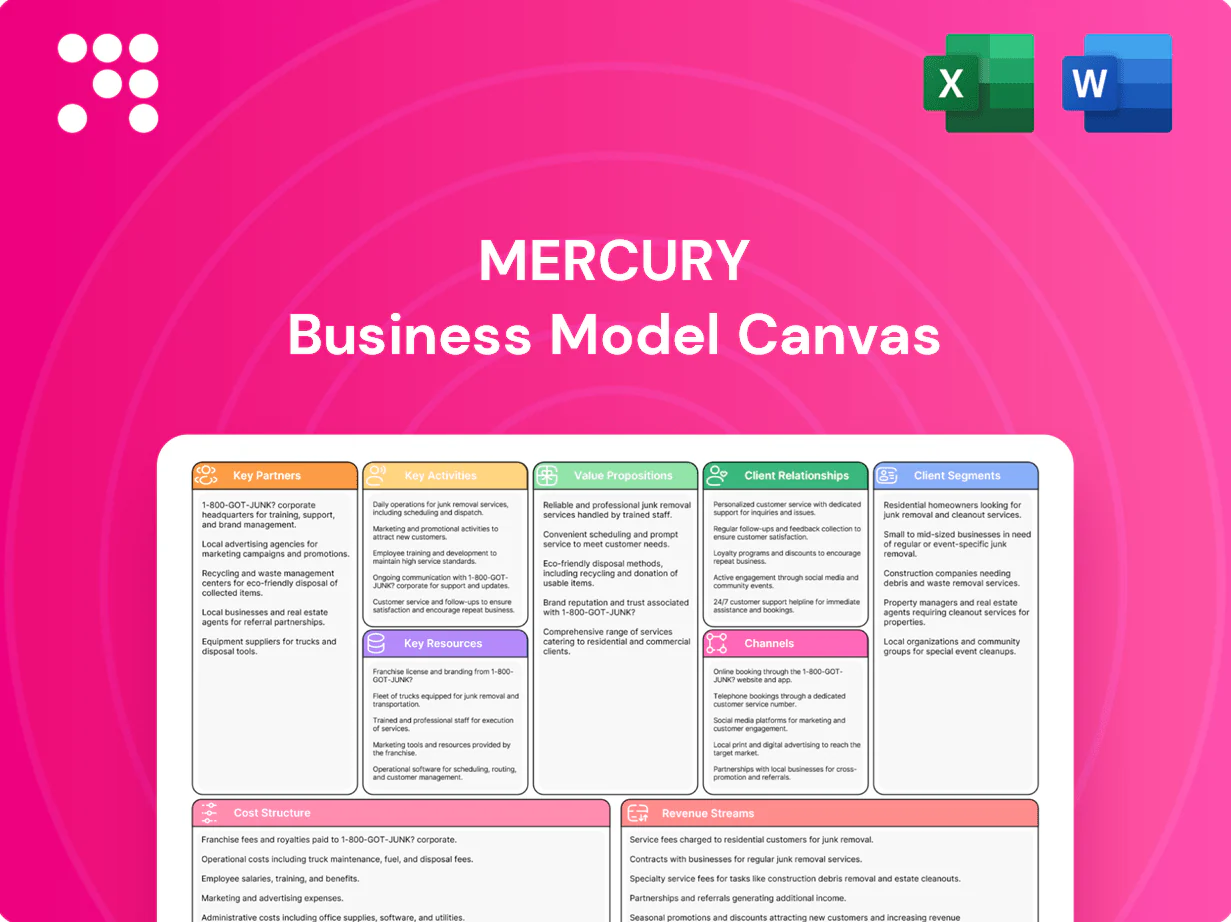

Unlock Mercury's Business Model Canvas and discover the nine strategic building blocks that power its growth—value propositions, revenue streams, key partners, and more. This editable, downloadable canvas is perfect for investors, founders, and consultants ready to benchmark, adapt, and act—purchase the full file for instant strategic clarity.

Partnerships

Independent agents and brokers

Independent agents and brokers are Mercury’s primary distribution allies, sourcing, advising, and binding the majority of commercial policies—accounting for >50% of US commercial placements in 2024—while extending geographic reach without fixed sales overhead. Strong agent relationships boost quote flow, hit ratios, and retention through trusted local advice. Co-op marketing and training align incentives, ensuring product fit and scalable distribution.

Reinsurance providers

Reinsurance partners help Mercury manage catastrophe and severity risk, protecting capital and stabilizing earnings after large events; global reinsurance premiums were about $320bn in 2024, reflecting ample market capacity. Quota‑share and excess‑of‑loss treaties smooth volatility from wildfires and large auto losses. Long‑term reinsurer ties can lower ceding costs and expand capacity, while structured arrangements support ratings and regulatory capital requirements.

Claims service networks

Preferred auto body shops, glass vendors and home-repair contractors cut repair costs ~10% and shorten cycle times ~30% through negotiated rates and quality controls; network pricing and audits improve loss adjustment efficiency and can trim leakage ~15–20% in 2024. Digital estimating partners accelerate estimates and approvals up to 50%, boosting NPS and overall customer satisfaction by ~10–15 points.

Data and technology partners

Data and technology partners — telematics providers, credit and driving data bureaus, and fraud analytics vendors — sharpen underwriting and, according to 2024 industry surveys, telematics adoption among US auto insurers surpassed 30%, improving loss-ratio visibility. Third-party enrichment lifts pricing and segmentation accuracy, while cloud platforms and APIs cut speed-to-quote and improve agent connectivity. Partnerships reduce build time and tech risk, lowering integration costs versus in-house by a reported 20% in benchmark studies.

- telematics: >30% US insurer adoption (2024)

- data bureaus: improved risk signals for pricing

- fraud analytics: lower false positives, faster detection

- cloud/API: faster speed-to-quote, reduced tech risk

Regulators and ratings agencies

Constructive engagement with 51 state and DC insurance regulators ensures filings, rates, and forms move efficiently. Compliance partnerships mitigate fines and reputational risk and help preserve operating licenses. Strong A.M. Best/S&P/Fitch ratings boost agent confidence while transparent reporting sustains long-term license viability.

- Regulators: 51 state+DC

- Compliance: fines & license protection

- Ratings: A.M. Best / S&P / Fitch drive trust

- Reporting: transparency = license sustainability

Agents >50% placements; reinsurers ~$320bn; telematics cut costs ~10%

Independent agents drive distribution—>50% of US commercial placements in 2024—boosting quote flow, hit rates and retention. Reinsurers (global premiums ~$320bn in 2024) stabilize capital via quota‑share and XoL treaties. Repair, telematics and data partners cut repair costs ~10%, cycle times ~30% and telematics adoption >30% (US insurers 2024).

| Partner | Role | 2024 metric |

|---|---|---|

| Agents | Distribution | >50% commercial placements |

| Reinsurers | Risk transfer | Global premiums ~$320bn |

| Repair/telematics | Cost & CX | Costs -10% / telematics >30% |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Mercury’s strategy, organized into the 9 classic BMC blocks with full narrative, insights, and competitive-advantage analysis. It reflects real-world operations, includes linked SWOT, supports validation with real company data, and is polished for presentations, funding discussions, and internal decision-making.

High-level view with editable cells that condenses strategy into a one-page snapshot, saving hours of formatting and enabling fast, shareable collaboration for teams, boardrooms, and quick deliverables.

Activities

Risk selection and pricing

Underwriting classes and targeted rate filings drive portfolio quality and profitability, with insurers modeling segments to meet loss-ratio targets (e.g., aiming sub-60% combined on personal lines). Actuarial models translate loss experience into rates using frequency/severity distributions and loss development factors calibrated to 2024 claim trends. Continuous monitoring adjusts assumptions for inflation and shifts in frequency/severity; filing strategy times submissions to California’s prior-approval cadence (typically 45–120 days review).

Claims handling and fraud control

Timely FNOL intake, triage and settlement (target: 24–72 hours) drive customer satisfaction and lower loss development; faster FNOL workflows correlate with higher retention. SIU units and analytics curb fraud—insurers face roughly $40 billion/year in fraud losses and analytics programs report meaningful reductions. Vendor management tightens repair quality and cost control. Active litigation management contains severity in contested claims.

Distribution management

Recruiting, onboarding, and agent support drive quote volume and conversion—2024 McKinsey data shows digital-enabled onboarding can cut time ~50%, boosting active agent output; targeted compensation, training, and portals raise productivity ~15–25%; localized marketing programs lift lead conversion, while performance dashboards (by agency) steer product mix and profitability in real time.

Product development and filing

Product design for personal auto, homeowners and commercial auto adapts to telematics, catastrophe frequency and supply-chain inflation; rate, rule and form updates track loss trends and state regulation in 2024. Bundling features and discounts—bundle savings up to 20% in 2024—improve competitiveness and retention. Faster filings shorten time-to-market, capturing share.

- Design: multi-line alignment

- Pricing: continuous rate/form updates

- Go-to-market: faster filings, bundle-driven growth

Capital and investment management

Maintaining reserves and strong RBC supports rated growth and solvency; many US carriers targeted RBC above 200% in 2024 to preserve ratings and expansion capacity. Investment of float generates material non-underwriting income; 2024 market yields (10y ~4%) bolstered portfolio returns. ALM balances duration and liquidity to meet claim timing and cash needs. Reinsurance structuring enhances capital efficiency and volatility control.

- RBC target: >200% (2024)

- 10y Treasury ~4% (2024) — supports investment yields

- ALM: duration vs liquidity for claims

- Reinsurance: capital relief and volatility reduction

Target sub-60% combined; 24–72h FNOL; digital onboarding cuts time ~50%; RBC > 200%

Underwrite to sub-60% combined on personal lines; actuarial updates follow 2024 loss-dev and inflation. FNOL targets 24–72h to cut loss development and improve retention. Agent onboarding digital cuts time ~50%, lifting productivity 15–25%. Capital: RBC >200% and 10y ~4% in 2024 support growth and ALM.

| Metric | 2024 |

|---|---|

| Combined ratio target | ~60% |

| FNOL | 24–72h |

| Fraud loss | $40B |

| RBC | >200% |

| 10y | ~4% |

Preview Before You Purchase

Business Model Canvas

The Mercury Business Model Canvas you’re previewing is the exact document you’ll receive—no mockups or samples. After purchase you’ll instantly download the complete, ready-to-use file formatted for editing and presentation. What you see here is what you’ll own.

Unlock a Ready-to-Use Business Model Canvas for Fast Strategic Decision-Making

Unlock Mercury's Business Model Canvas and discover the nine strategic building blocks that power its growth—value propositions, revenue streams, key partners, and more. This editable, downloadable canvas is perfect for investors, founders, and consultants ready to benchmark, adapt, and act—purchase the full file for instant strategic clarity.

Partnerships

Independent agents and brokers

Independent agents and brokers are Mercury’s primary distribution allies, sourcing, advising, and binding the majority of commercial policies—accounting for >50% of US commercial placements in 2024—while extending geographic reach without fixed sales overhead. Strong agent relationships boost quote flow, hit ratios, and retention through trusted local advice. Co-op marketing and training align incentives, ensuring product fit and scalable distribution.

Reinsurance providers

Reinsurance partners help Mercury manage catastrophe and severity risk, protecting capital and stabilizing earnings after large events; global reinsurance premiums were about $320bn in 2024, reflecting ample market capacity. Quota‑share and excess‑of‑loss treaties smooth volatility from wildfires and large auto losses. Long‑term reinsurer ties can lower ceding costs and expand capacity, while structured arrangements support ratings and regulatory capital requirements.

Claims service networks

Preferred auto body shops, glass vendors and home-repair contractors cut repair costs ~10% and shorten cycle times ~30% through negotiated rates and quality controls; network pricing and audits improve loss adjustment efficiency and can trim leakage ~15–20% in 2024. Digital estimating partners accelerate estimates and approvals up to 50%, boosting NPS and overall customer satisfaction by ~10–15 points.

Data and technology partners

Data and technology partners — telematics providers, credit and driving data bureaus, and fraud analytics vendors — sharpen underwriting and, according to 2024 industry surveys, telematics adoption among US auto insurers surpassed 30%, improving loss-ratio visibility. Third-party enrichment lifts pricing and segmentation accuracy, while cloud platforms and APIs cut speed-to-quote and improve agent connectivity. Partnerships reduce build time and tech risk, lowering integration costs versus in-house by a reported 20% in benchmark studies.

- telematics: >30% US insurer adoption (2024)

- data bureaus: improved risk signals for pricing

- fraud analytics: lower false positives, faster detection

- cloud/API: faster speed-to-quote, reduced tech risk

Regulators and ratings agencies

Constructive engagement with 51 state and DC insurance regulators ensures filings, rates, and forms move efficiently. Compliance partnerships mitigate fines and reputational risk and help preserve operating licenses. Strong A.M. Best/S&P/Fitch ratings boost agent confidence while transparent reporting sustains long-term license viability.

- Regulators: 51 state+DC

- Compliance: fines & license protection

- Ratings: A.M. Best / S&P / Fitch drive trust

- Reporting: transparency = license sustainability

Agents >50% placements; reinsurers ~$320bn; telematics cut costs ~10%

Independent agents drive distribution—>50% of US commercial placements in 2024—boosting quote flow, hit rates and retention. Reinsurers (global premiums ~$320bn in 2024) stabilize capital via quota‑share and XoL treaties. Repair, telematics and data partners cut repair costs ~10%, cycle times ~30% and telematics adoption >30% (US insurers 2024).

| Partner | Role | 2024 metric |

|---|---|---|

| Agents | Distribution | >50% commercial placements |

| Reinsurers | Risk transfer | Global premiums ~$320bn |

| Repair/telematics | Cost & CX | Costs -10% / telematics >30% |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Mercury’s strategy, organized into the 9 classic BMC blocks with full narrative, insights, and competitive-advantage analysis. It reflects real-world operations, includes linked SWOT, supports validation with real company data, and is polished for presentations, funding discussions, and internal decision-making.

High-level view with editable cells that condenses strategy into a one-page snapshot, saving hours of formatting and enabling fast, shareable collaboration for teams, boardrooms, and quick deliverables.

Activities

Risk selection and pricing

Underwriting classes and targeted rate filings drive portfolio quality and profitability, with insurers modeling segments to meet loss-ratio targets (e.g., aiming sub-60% combined on personal lines). Actuarial models translate loss experience into rates using frequency/severity distributions and loss development factors calibrated to 2024 claim trends. Continuous monitoring adjusts assumptions for inflation and shifts in frequency/severity; filing strategy times submissions to California’s prior-approval cadence (typically 45–120 days review).

Claims handling and fraud control

Timely FNOL intake, triage and settlement (target: 24–72 hours) drive customer satisfaction and lower loss development; faster FNOL workflows correlate with higher retention. SIU units and analytics curb fraud—insurers face roughly $40 billion/year in fraud losses and analytics programs report meaningful reductions. Vendor management tightens repair quality and cost control. Active litigation management contains severity in contested claims.

Distribution management

Recruiting, onboarding, and agent support drive quote volume and conversion—2024 McKinsey data shows digital-enabled onboarding can cut time ~50%, boosting active agent output; targeted compensation, training, and portals raise productivity ~15–25%; localized marketing programs lift lead conversion, while performance dashboards (by agency) steer product mix and profitability in real time.

Product development and filing

Product design for personal auto, homeowners and commercial auto adapts to telematics, catastrophe frequency and supply-chain inflation; rate, rule and form updates track loss trends and state regulation in 2024. Bundling features and discounts—bundle savings up to 20% in 2024—improve competitiveness and retention. Faster filings shorten time-to-market, capturing share.

- Design: multi-line alignment

- Pricing: continuous rate/form updates

- Go-to-market: faster filings, bundle-driven growth

Capital and investment management

Maintaining reserves and strong RBC supports rated growth and solvency; many US carriers targeted RBC above 200% in 2024 to preserve ratings and expansion capacity. Investment of float generates material non-underwriting income; 2024 market yields (10y ~4%) bolstered portfolio returns. ALM balances duration and liquidity to meet claim timing and cash needs. Reinsurance structuring enhances capital efficiency and volatility control.

- RBC target: >200% (2024)

- 10y Treasury ~4% (2024) — supports investment yields

- ALM: duration vs liquidity for claims

- Reinsurance: capital relief and volatility reduction

Target sub-60% combined; 24–72h FNOL; digital onboarding cuts time ~50%; RBC > 200%

Underwrite to sub-60% combined on personal lines; actuarial updates follow 2024 loss-dev and inflation. FNOL targets 24–72h to cut loss development and improve retention. Agent onboarding digital cuts time ~50%, lifting productivity 15–25%. Capital: RBC >200% and 10y ~4% in 2024 support growth and ALM.

| Metric | 2024 |

|---|---|

| Combined ratio target | ~60% |

| FNOL | 24–72h |

| Fraud loss | $40B |

| RBC | >200% |

| 10y | ~4% |

Preview Before You Purchase

Business Model Canvas

The Mercury Business Model Canvas you’re previewing is the exact document you’ll receive—no mockups or samples. After purchase you’ll instantly download the complete, ready-to-use file formatted for editing and presentation. What you see here is what you’ll own.

Original: $10.00

-65%$10.00

$3.50Description

Unlock a Ready-to-Use Business Model Canvas for Fast Strategic Decision-Making

Unlock Mercury's Business Model Canvas and discover the nine strategic building blocks that power its growth—value propositions, revenue streams, key partners, and more. This editable, downloadable canvas is perfect for investors, founders, and consultants ready to benchmark, adapt, and act—purchase the full file for instant strategic clarity.

Partnerships

Independent agents and brokers

Independent agents and brokers are Mercury’s primary distribution allies, sourcing, advising, and binding the majority of commercial policies—accounting for >50% of US commercial placements in 2024—while extending geographic reach without fixed sales overhead. Strong agent relationships boost quote flow, hit ratios, and retention through trusted local advice. Co-op marketing and training align incentives, ensuring product fit and scalable distribution.

Reinsurance providers

Reinsurance partners help Mercury manage catastrophe and severity risk, protecting capital and stabilizing earnings after large events; global reinsurance premiums were about $320bn in 2024, reflecting ample market capacity. Quota‑share and excess‑of‑loss treaties smooth volatility from wildfires and large auto losses. Long‑term reinsurer ties can lower ceding costs and expand capacity, while structured arrangements support ratings and regulatory capital requirements.

Claims service networks

Preferred auto body shops, glass vendors and home-repair contractors cut repair costs ~10% and shorten cycle times ~30% through negotiated rates and quality controls; network pricing and audits improve loss adjustment efficiency and can trim leakage ~15–20% in 2024. Digital estimating partners accelerate estimates and approvals up to 50%, boosting NPS and overall customer satisfaction by ~10–15 points.

Data and technology partners

Data and technology partners — telematics providers, credit and driving data bureaus, and fraud analytics vendors — sharpen underwriting and, according to 2024 industry surveys, telematics adoption among US auto insurers surpassed 30%, improving loss-ratio visibility. Third-party enrichment lifts pricing and segmentation accuracy, while cloud platforms and APIs cut speed-to-quote and improve agent connectivity. Partnerships reduce build time and tech risk, lowering integration costs versus in-house by a reported 20% in benchmark studies.

- telematics: >30% US insurer adoption (2024)

- data bureaus: improved risk signals for pricing

- fraud analytics: lower false positives, faster detection

- cloud/API: faster speed-to-quote, reduced tech risk

Regulators and ratings agencies

Constructive engagement with 51 state and DC insurance regulators ensures filings, rates, and forms move efficiently. Compliance partnerships mitigate fines and reputational risk and help preserve operating licenses. Strong A.M. Best/S&P/Fitch ratings boost agent confidence while transparent reporting sustains long-term license viability.

- Regulators: 51 state+DC

- Compliance: fines & license protection

- Ratings: A.M. Best / S&P / Fitch drive trust

- Reporting: transparency = license sustainability

Agents >50% placements; reinsurers ~$320bn; telematics cut costs ~10%

Independent agents drive distribution—>50% of US commercial placements in 2024—boosting quote flow, hit rates and retention. Reinsurers (global premiums ~$320bn in 2024) stabilize capital via quota‑share and XoL treaties. Repair, telematics and data partners cut repair costs ~10%, cycle times ~30% and telematics adoption >30% (US insurers 2024).

| Partner | Role | 2024 metric |

|---|---|---|

| Agents | Distribution | >50% commercial placements |

| Reinsurers | Risk transfer | Global premiums ~$320bn |

| Repair/telematics | Cost & CX | Costs -10% / telematics >30% |

What is included in the product

A comprehensive, pre-written Business Model Canvas tailored to Mercury’s strategy, organized into the 9 classic BMC blocks with full narrative, insights, and competitive-advantage analysis. It reflects real-world operations, includes linked SWOT, supports validation with real company data, and is polished for presentations, funding discussions, and internal decision-making.

High-level view with editable cells that condenses strategy into a one-page snapshot, saving hours of formatting and enabling fast, shareable collaboration for teams, boardrooms, and quick deliverables.

Activities

Risk selection and pricing

Underwriting classes and targeted rate filings drive portfolio quality and profitability, with insurers modeling segments to meet loss-ratio targets (e.g., aiming sub-60% combined on personal lines). Actuarial models translate loss experience into rates using frequency/severity distributions and loss development factors calibrated to 2024 claim trends. Continuous monitoring adjusts assumptions for inflation and shifts in frequency/severity; filing strategy times submissions to California’s prior-approval cadence (typically 45–120 days review).

Claims handling and fraud control

Timely FNOL intake, triage and settlement (target: 24–72 hours) drive customer satisfaction and lower loss development; faster FNOL workflows correlate with higher retention. SIU units and analytics curb fraud—insurers face roughly $40 billion/year in fraud losses and analytics programs report meaningful reductions. Vendor management tightens repair quality and cost control. Active litigation management contains severity in contested claims.

Distribution management

Recruiting, onboarding, and agent support drive quote volume and conversion—2024 McKinsey data shows digital-enabled onboarding can cut time ~50%, boosting active agent output; targeted compensation, training, and portals raise productivity ~15–25%; localized marketing programs lift lead conversion, while performance dashboards (by agency) steer product mix and profitability in real time.

Product development and filing

Product design for personal auto, homeowners and commercial auto adapts to telematics, catastrophe frequency and supply-chain inflation; rate, rule and form updates track loss trends and state regulation in 2024. Bundling features and discounts—bundle savings up to 20% in 2024—improve competitiveness and retention. Faster filings shorten time-to-market, capturing share.

- Design: multi-line alignment

- Pricing: continuous rate/form updates

- Go-to-market: faster filings, bundle-driven growth

Capital and investment management

Maintaining reserves and strong RBC supports rated growth and solvency; many US carriers targeted RBC above 200% in 2024 to preserve ratings and expansion capacity. Investment of float generates material non-underwriting income; 2024 market yields (10y ~4%) bolstered portfolio returns. ALM balances duration and liquidity to meet claim timing and cash needs. Reinsurance structuring enhances capital efficiency and volatility control.

- RBC target: >200% (2024)

- 10y Treasury ~4% (2024) — supports investment yields

- ALM: duration vs liquidity for claims

- Reinsurance: capital relief and volatility reduction

Target sub-60% combined; 24–72h FNOL; digital onboarding cuts time ~50%; RBC > 200%

Underwrite to sub-60% combined on personal lines; actuarial updates follow 2024 loss-dev and inflation. FNOL targets 24–72h to cut loss development and improve retention. Agent onboarding digital cuts time ~50%, lifting productivity 15–25%. Capital: RBC >200% and 10y ~4% in 2024 support growth and ALM.

| Metric | 2024 |

|---|---|

| Combined ratio target | ~60% |

| FNOL | 24–72h |

| Fraud loss | $40B |

| RBC | >200% |

| 10y | ~4% |

Preview Before You Purchase

Business Model Canvas

The Mercury Business Model Canvas you’re previewing is the exact document you’ll receive—no mockups or samples. After purchase you’ll instantly download the complete, ready-to-use file formatted for editing and presentation. What you see here is what you’ll own.